How to Get the Best Rate on a Car Loan: Your Ultimate Guide to Saving Thousands

How to Get the Best Rate on a Car Loan: Your Ultimate Guide to Saving Thousands Carloan.Guidemechanic.com

The dream of a new car – or even a reliable used one – often comes with the reality of financing. For most people, a car loan is a necessity, but it doesn’t have to be a financial burden. Securing the best rate on a car loan isn’t just about finding the lowest monthly payment; it’s about understanding the entire process, empowering yourself with knowledge, and ultimately saving thousands of dollars over the life of your loan.

As an expert blogger and SEO content writer with years of experience navigating the world of auto financing, I’ve seen firsthand how a few smart moves can make a monumental difference. This comprehensive guide is designed to be your ultimate resource, providing in-depth strategies, expert tips, and common pitfalls to avoid. Our goal is to equip you with the insights needed to confidently negotiate and secure an auto loan that truly works for your budget, not against it. Let’s dive in and unlock the secrets to lower car loan rates.

How to Get the Best Rate on a Car Loan: Your Ultimate Guide to Saving Thousands

Understanding Car Loan Basics: The Foundation of Smart Borrowing

Before you even think about stepping foot in a dealership or applying for financing, it’s crucial to understand the fundamental components of a car loan. This foundational knowledge will be your compass throughout the entire process. Without it, you’re navigating uncharted waters.

What is APR and Why Does It Matter So Much?

The Annual Percentage Rate (APR) is arguably the most critical number to focus on when securing a car loan. It represents the true annual cost of borrowing money, encompassing not just the interest rate but also any additional fees charged by the lender. A lower APR directly translates to less money paid out of your pocket over the loan term.

Many consumers mistakenly focus solely on the monthly payment. While the monthly payment is important for budgeting, a low monthly payment achieved through a very long loan term with a high APR can cost you significantly more in the long run. Always compare APRs when evaluating different loan offers to get the best auto loan rates.

Key Factors Influencing Your Car Loan Interest Rates

Several variables converge to determine the interest rate you’ll be offered. Understanding these factors allows you to proactively improve your standing before applying. It’s like knowing the rules of the game before you play.

- Your Credit Score: This is, by far, the most influential factor. A higher credit score signals to lenders that you are a responsible borrower, making you eligible for lower interest rates. We’ll delve deeper into this shortly.

- Debt-to-Income (DTI) Ratio: Lenders assess your DTI to gauge your ability to handle additional debt. It’s the percentage of your gross monthly income that goes towards debt payments. A lower DTI is always more attractive.

- Loan Term: The length of time you have to repay the loan significantly impacts the interest rate. Shorter terms typically come with lower interest rates but higher monthly payments, while longer terms often have higher rates but smaller monthly payments.

- Down Payment Amount: A larger down payment reduces the amount you need to borrow, which can lower your risk profile for lenders and potentially lead to better rates. It also means you’re less likely to be "upside down" on your loan.

- Vehicle Type and Age: New cars generally command lower interest rates than used cars due to their higher resale value and perceived reliability. Certain luxury or high-performance vehicles might also have different rates.

- Market Conditions: Broader economic factors, such as the prime rate set by the Federal Reserve, can influence overall interest rates across all loan types, including car loans.

Pro tip from us: Don’t just focus on the monthly payment a salesperson quotes you. Always ask for the total loan amount, the APR, and the full repayment schedule. This transparency is crucial for understanding the true cost.

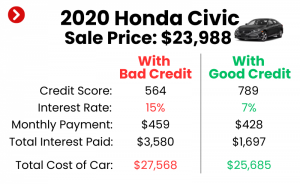

The Credit Score: Your Golden Ticket to Lower Rates

Your credit score is the single most powerful tool in your arsenal when seeking the best rate on a car loan. Lenders use this three-digit number to quickly assess your creditworthiness and predict your likelihood of repaying the loan. A higher score translates directly into more favorable terms and significantly lower car loan rates.

How Credit Impacts Your Interest Rates

Think of your credit score as a financial report card. A stellar report card (a high score, typically 720+) tells lenders you’re a low-risk borrower. This competitive advantage means they’re willing to offer you their most attractive interest rates. Conversely, a lower score suggests a higher risk, prompting lenders to offer higher rates to compensate for that perceived risk. This difference can amount to thousands of dollars over the loan’s duration.

Based on my experience, even a 20-point increase in your FICO score can push you into a new tier of interest rates, unlocking significant savings.

Strategies to Improve Your Credit Score Before Applying

Improving your credit score isn’t an overnight process, but strategic planning can yield substantial results. Start these steps months before you plan to buy a car if possible.

- Pay Your Bills On Time, Every Time: Payment history is the most significant factor in your credit score. Missing payments, even by a few days, can severely damage your score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Your Credit Utilization Ratio: This ratio measures how much credit you’re using compared to your total available credit. Aim to keep this below 30% across all your credit cards and lines of credit. Paying down existing credit card balances can quickly boost this ratio.

- Check Your Credit Report for Errors: Annually, obtain a free copy of your credit report from each of the three major bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com. Dispute any inaccuracies immediately, as even small errors can negatively impact your score.

- Avoid Opening New Credit Accounts: Resist the temptation to open new credit cards or lines of credit in the months leading up to your car loan application. New accounts trigger hard inquiries, which can temporarily lower your score.

- Don’t Close Old Accounts: The length of your credit history also plays a role. Older accounts, especially those with a good payment history, demonstrate a long track record of responsible borrowing. Keeping them open, even if unused, benefits your score.

Common mistakes to avoid are: Applying for multiple new credit cards right before a car loan, as this signals potential financial distress and can lower your score. Also, never let a dealership run your credit multiple times without your explicit consent for a specific loan application.

Financial Preparation: Setting Yourself Up for Success

Beyond your credit score, how you prepare your finances fundamentally impacts the car loan interest rates you’ll be offered. This involves strategic budgeting, saving for a down payment, and managing your existing debt.

Budgeting: Knowing What You Can Truly Afford

Before falling in love with a car, create a realistic budget that encompasses not just the potential monthly car payment but also insurance, fuel, maintenance, and registration fees. These often-overlooked costs can quickly add up, turning a seemingly affordable payment into a financial strain. Use online calculators to estimate total ownership costs.

A responsible car loan fits comfortably within your overall financial picture, allowing you to meet other financial goals like saving or investing. Don’t let emotion override common sense when it comes to your budget.

The Power of a Larger Down Payment

Making a substantial down payment is one of the most effective ways to lower car loan rates and improve your overall loan terms. When you put down more money upfront, you reduce the amount you need to borrow. This lowers the lender’s risk, often leading to a more attractive interest rate.

A larger down payment also helps you avoid being "upside down" on your loan, which means owing more than the car is worth. This can be particularly important in the early years of car ownership due to depreciation.

Pro tips from us: Aim for at least a 20% down payment for a new car and 10% for a used car if possible. This significantly strengthens your position.

Debt-to-Income (DTI) Ratio: Why It’s Crucial

Your Debt-to-Income (DTI) ratio is a key metric lenders use to assess your ability to manage additional debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI indicates you have more disposable income available to cover new loan payments.

Lenders generally prefer a DTI ratio below 36%, though some may accept up to 43%. If your DTI is high, consider paying down existing debts like credit card balances or personal loans before applying for a car loan. This proactive step can make you a more attractive borrower.

Loan Term: The Trade-Offs

Choosing the right loan term is a balancing act. Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates, meaning you pay less interest over the life of the loan. However, they result in higher monthly payments. Longer loan terms (e.g., 60 or 72 months) offer lower monthly payments, but you’ll usually pay a higher overall interest rate and more in total interest.

Based on my experience, many consumers extend the loan term just to reduce the monthly payment, often without realizing how much more they’ll pay in interest. Always consider the total cost of the loan, not just the monthly installment. Try to choose the shortest term you can comfortably afford.

The Power of Pre-Approval: Your Negotiating Weapon

One of the most impactful steps you can take to secure the best rate on a car loan is to get pre-approved for financing before you ever step foot in a dealership. This single action shifts the power dynamic significantly in your favor.

What is Pre-Approval and Why It’s Essential

Pre-approval means a lender has reviewed your financial information (credit score, income, debt) and tentatively agreed to lend you a specific amount of money at a particular interest rate, subject to final verification and vehicle selection. It’s not a final commitment, but it gives you a firm offer in hand.

Why is this essential? Because it arms you with a benchmark. When you walk into a dealership with a pre-approval, you’re no longer solely dependent on their financing department. You know the maximum interest rate you’re willing to accept, and you have leverage to compare against any offers they present.

How to Get Pre-Approved (and Where to Look)

The process of getting pre-approved is relatively straightforward. You’ll typically fill out an application providing personal and financial details. The lender will then perform a "hard inquiry" on your credit report, which will temporarily lower your score by a few points, but the benefit outweighs this minor dip.

- Banks: Your current bank or credit union is an excellent place to start. They often offer competitive rates to existing customers.

- Credit Unions: These member-owned financial institutions are renowned for offering some of the best auto loan rates due to their non-profit structure. It’s often worth joining one just for their loan products.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, or Carvana offer convenient online applications and competitive rates. They provide a quick way to compare multiple offers.

Based on my experience: Obtaining multiple pre-approvals within a 14-45 day window (depending on the credit scoring model) will only count as a single hard inquiry on your credit report. This allows you to shop around without further penalizing your score. Use this window wisely!

Comparing Pre-Approval Offers

Once you have a few pre-approval offers, carefully compare them. Look beyond just the interest rate. Consider:

- APR: This is the most important number.

- Loan Term: Ensure it aligns with your budget and financial goals.

- Fees: Are there any origination fees, application fees, or prepayment penalties?

- Loan Amount: Does it cover the car you intend to buy?

Having these offers empowers you to choose the best one, or use it as a powerful negotiation tool with the dealership’s finance department.

Shopping Around: Don’t Settle for the First Offer

Many car buyers make the mistake of accepting the first financing offer presented to them, often from the dealership. This is a critical error. To truly get the best rate on a car loan, you must shop around and compare multiple lenders.

The Importance of Comparing Multiple Lenders

Just as you wouldn’t buy the first car you see, you shouldn’t take the first loan offer. Different lenders have varying criteria, risk assessments, and profit margins, which means their rates can differ significantly. By comparing offers from banks, credit unions, and online lenders, you ensure you’re getting the most competitive terms available to you.

Remember, the dealership’s finance manager works for the dealership, not for you. While they might offer competitive rates, their primary goal is to maximize profit. Your pre-approval offers provide a crucial baseline for comparison.

Asking the Right Questions

When comparing loan offers, don’t hesitate to ask specific questions:

- What is the exact APR being offered?

- Are there any upfront fees or hidden charges?

- Are there any prepayment penalties if I decide to pay off the loan early?

- What is the total cost of the loan over its term?

- What documents do I need to finalize the loan?

Clarity on these points will prevent any surprises down the line.

Common mistake: Letting the dealership be your only source of financing. This often leads to higher interest rates because they know you haven’t compared their offer against others. Always come prepared with outside offers.

Negotiation Tactics: Mastering the Dealership Dance

Armed with your pre-approval and a clear understanding of your financial limits, you’re ready to negotiate. This stage is where many consumers feel intimidated, but with the right approach, you can secure the best auto loan rates and a fair purchase price.

Separating the Car Price from the Financing

This is a fundamental rule of car buying. Never discuss the monthly payment or financing terms until you have agreed upon the final purchase price of the vehicle. If you discuss them together, the salesperson can manipulate numbers, shifting funds between the car price, trade-in value, and interest rate to make it seem like you’re getting a good deal when you’re not.

Focus on negotiating the "out-the-door" price of the car first, including taxes and fees. Once that’s settled, then you can discuss financing.

Using Your Pre-Approval as Leverage

Your pre-approval is your strongest negotiation tool for financing. Once you’ve agreed on the car’s price, present your pre-approval offer to the dealership’s finance manager. Tell them you’re interested in seeing if they can beat your existing rate.

They may try to match or even slightly beat your outside offer, as they prefer to keep the financing in-house. If they can’t, you simply proceed with your pre-approved loan. This strategy ensures you’re getting the most competitive rate available.

Beware of Add-Ons and Extended Warranties

Once the car price and financing are discussed, the finance manager will often present various add-ons: extended warranties, paint protection, fabric protection, GAP insurance (if you haven’t already secured it), and anti-theft devices. While some might be useful, many are highly profitable for the dealership and can significantly inflate your loan amount.

Pro tips from us: Politely decline any add-ons you don’t genuinely need or haven’t thoroughly researched. You can often purchase extended warranties or GAP insurance separately for less money. Be firm, be polite, and be ready to walk away if you feel pressured. Your prepared self is your best asset.

Understanding the Loan Contract: Read Before You Sign!

This is the final, crucial step before you drive away in your new vehicle. Never sign a document you haven’t fully read and understood. The loan contract contains all the legally binding terms of your auto loan.

Key Terms to Scrutinize

Take your time to review every line of the contract. Pay particular attention to these critical details:

- Annual Percentage Rate (APR): Double-check that the APR listed matches what you agreed upon.

- Total Loan Amount: Ensure this reflects the agreed-upon car price minus your down payment, plus any agreed-upon fees.

- Loan Term: Confirm the number of months matches your understanding.

- Monthly Payment: Verify this is the correct amount.

- Fees: Look for any hidden fees, origination charges, or administrative costs that were not previously disclosed.

- Prepayment Penalties: Check if there are any penalties for paying off the loan early. The best auto loan rates typically come without these.

- Late Payment Penalties: Understand the consequences of missed or late payments.

Don’t be afraid to ask for clarification on any term you don’t understand. A reputable lender will be happy to explain everything.

External Link: For more detailed information on consumer auto financing rights and regulations, visit the Consumer Financial Protection Bureau (CFPB) website. They offer excellent resources on what to look for in an auto loan contract and your rights as a borrower.

Don’t Rush the Process

Dealerships often try to rush you through the signing process, especially at the end of the day. Resist this pressure. Insist on taking your time to read every page thoroughly. If you feel overwhelmed, ask to take a copy home to review or bring a trusted friend or family member with you. This vigilance ensures you’re getting the best rate on a car loan and that all terms are as agreed.

Post-Purchase Strategies: Optimizing Your Loan

Even after you’ve signed the papers and driven off the lot, there are still ways to optimize your car loan and save money. Smart financial habits can continue to benefit you.

Making Extra Payments

If your financial situation improves, consider making extra payments towards your principal. Even small additional payments can significantly reduce the total interest paid and shorten the loan term, saving you money in the long run. Ensure your lender applies these extra payments directly to the principal, not towards future interest.

Refinancing: When and Why It Makes Sense

If you initially secured a higher interest rate due to a lower credit score or unfavorable market conditions, refinancing your car loan might be a smart move. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

When to consider refinancing:

- Your credit score has significantly improved since you took out the original loan.

- Interest rates have dropped since your original purchase.

- You want to lower your monthly payments (though be mindful of extending the loan term and increasing total interest paid).

- You want to remove a co-signer.

Staying on Top of Your Credit Post-Loan

Your car loan is an excellent opportunity to build or rebuild a strong credit history. Make all your payments on time and in full. This positive payment history will contribute to a healthier credit score, which will benefit you for future borrowing needs, whether it’s another car, a mortgage, or other lines of credit.

Special Circumstances: Navigating Unique Situations

While the general principles apply, some situations require a tailored approach when seeking best auto loan rates.

Bad Credit Car Loans: Strategies and Realistic Expectations

If you have a low credit score, securing the best rate on a car loan becomes more challenging, but it’s not impossible. Realistic expectations are key. You likely won’t qualify for the absolute lowest rates, but you can still aim for the best rate available to you.

- Focus on improving your credit score first: Even a small improvement can make a difference.

- Increase your down payment: A larger down payment reduces the risk for lenders.

- Consider a co-signer: A co-signer with excellent credit can help you qualify for better rates, but ensure both parties understand the responsibility.

- Explore subprime lenders: These lenders specialize in working with borrowers with lower credit scores, but be prepared for higher interest rates.

- Start with a less expensive car: This reduces the total loan amount and therefore the risk.

Co-Signers: When They Help, When They Hurt

A co-signer with good credit can be a lifeline for borrowers with limited or poor credit. Their strong credit profile acts as a guarantee for the loan, potentially helping you secure a lower interest rate. However, a co-signer takes on full responsibility for the loan if you default, which can strain relationships if things go wrong. Both parties should fully understand the implications before agreeing.

New vs. Used Car Loans: Differences in Rates

Generally, new car loans tend to have lower interest rates than used car loans. This is because new cars hold their value better initially, making them less risky for lenders. Used cars, especially older ones, depreciate faster and are considered higher risk. Always factor this into your budget and expectations when choosing between a new and used vehicle.

Conclusion: Your Journey to the Best Car Loan Rate Starts Now

Securing the best rate on a car loan is not a matter of luck; it’s the result of informed decisions, diligent preparation, and strategic negotiation. By understanding the factors that influence interest rates, proactively working on your credit score, getting pre-approved, and comparing multiple offers, you empower yourself to make the smartest financial choice for your next vehicle.

Remember, knowledge is power in the world of auto financing. Don’t be rushed, don’t be intimidated, and always advocate for your financial best interest. With the insights provided in this comprehensive guide, you are now well-equipped to navigate the car loan process with confidence and save thousands. Your journey to securing lower car loan rates starts today! Share your car loan tips or questions in the comments below – we’d love to hear from you.