How to Get Your First Car Loan: The Ultimate Beginner’s Guide to Approval and Smart Financing

How to Get Your First Car Loan: The Ultimate Beginner’s Guide to Approval and Smart Financing Carloan.Guidemechanic.com

The thrill of getting your first car is an unparalleled feeling. It represents independence, freedom, and a significant milestone in adulthood. However, for many first-time buyers, the excitement can quickly turn into apprehension when confronted with the prospect of securing a car loan. It’s a complex financial decision, and navigating the world of interest rates, credit scores, and loan terms can feel overwhelming.

But it doesn’t have to be. Getting your first car loan is an achievable goal with the right preparation and understanding. This comprehensive guide is designed to empower you with the knowledge and confidence needed to not only get approved but to secure the best possible financing terms. We’ll break down every step, from understanding your finances to driving off the lot, ensuring you make a smart, informed decision.

How to Get Your First Car Loan: The Ultimate Beginner’s Guide to Approval and Smart Financing

The Foundation: Why Preparation is Key (and What It Entails)

Before you even start browsing car models online, the most critical step is thorough preparation. This isn’t just about showing lenders you’re responsible; it’s about protecting your financial future and ensuring your first car loan is a stepping stone, not a stumbling block. A solid foundation will make the entire process smoother and more successful.

Understanding Your Budget: Beyond the Monthly Payment

Many first-time car buyers make the mistake of focusing solely on the monthly payment. While it’s a crucial component, it’s far from the only cost associated with car ownership. Your budget needs to encompass the entire financial picture, ensuring you can comfortably afford your vehicle without straining your finances.

Beyond the initial purchase price and the monthly loan payment, you must factor in ongoing expenses. These include car insurance premiums, which can be surprisingly high for new drivers or younger individuals. Fuel costs, routine maintenance (oil changes, tire rotations), and potential repairs are also significant considerations. Don’t forget registration fees, taxes, and any unforeseen emergency costs. Based on my experience, many first-time buyers overlook these "hidden" costs, leading to financial stress down the road.

A key metric lenders look at is your debt-to-income (DTI) ratio. This compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates you have more disposable income to manage new debt, making you a more attractive borrower. Calculate your current DTI before applying for a car loan to get a realistic picture of your financial capacity. Aim for a DTI ratio below 36%, if possible, though some lenders may accept higher depending on other factors.

The Credit Score Conundrum: Building Your Financial Reputation

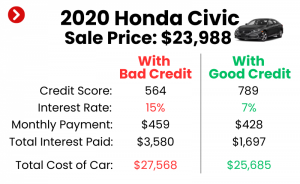

Your credit score is arguably the most influential factor in securing a car loan, especially for a first-time buyer. It’s a three-digit number that summarizes your creditworthiness, telling lenders how reliably you’ve managed debt in the past. A higher score typically leads to lower interest rates, saving you thousands over the life of the loan.

For many first-time buyers, the challenge is having a "thin" credit file or no credit history at all. Lenders have less information to assess your risk, which can result in higher interest rates or even outright denial. Therefore, understanding your credit score and actively working to build or improve it is paramount. You can check your credit score for free through various services like Credit Karma, Experian, or your bank’s online portal. It’s wise to review your credit report for any inaccuracies that could be dragging your score down.

Pro tips from us: If you have no credit history, start building it proactively. Consider becoming an authorized user on a trusted family member’s credit card (if they have good credit). This allows their positive payment history to reflect on your report. Another effective strategy is to open a secured credit card; you put down a deposit that acts as your credit limit, and consistent, on-time payments will build your credit over time. Even small, regular payments on things like student loans or utility bills can contribute positively to your payment history, which is a significant component of your credit score.

The Power of a Down Payment: Why It’s More Than Just Cash

Making a down payment is one of the smartest moves you can make when applying for your first car loan. It’s not just about reducing the initial amount you borrow; it sends a strong signal to lenders about your financial stability and commitment. A substantial down payment significantly mitigates the lender’s risk.

A larger down payment offers several key benefits. Firstly, it directly reduces the principal amount of your loan, leading to lower monthly payments. Secondly, because you’re borrowing less, you’ll pay less in total interest over the life of the loan, saving you a considerable amount of money. Thirdly, it improves your loan-to-value (LTV) ratio, which is another factor lenders consider. A lower LTV ratio means you owe less than the car is worth, making you a less risky borrower.

We generally recommend aiming for at least a 10-20% down payment on a used car and 20% or more on a new car. This helps prevent being "upside down" on your loan, where you owe more than the car is worth, especially considering depreciation. Start saving early and consistently for your down payment. Even a few hundred dollars can make a difference. Consider setting up an automatic transfer from your checking to a dedicated savings account to make the process effortless.

Navigating the Loan Landscape: Where to Look and What to Ask

Once you have a clear understanding of your budget and a handle on your credit situation, the next step is to explore your lending options. The market for car loans is diverse, and knowing where to look can make a significant difference in the terms you receive. Don’t settle for the first offer; smart shopping involves comparing multiple lenders.

Exploring Your Lending Options: Not All Loans Are Created Equal

The financial landscape offers a variety of institutions willing to provide car loans, each with its own advantages and disadvantages. Understanding these differences will help you find the best fit for your situation.

- Banks: Traditional banks are a common source for auto loans. They often have competitive rates for borrowers with good credit and offer a wide range of loan products. You might already have a relationship with a bank, which can sometimes streamline the application process. However, their approval criteria can be stricter for first-time buyers with limited credit history.

- Credit Unions: These member-owned financial cooperatives are often lauded for their customer-centric approach and typically offer lower interest rates and more flexible terms than traditional banks. They are generally more willing to work with individuals who have less-than-perfect credit or are first-time borrowers, as long as you meet their membership requirements. It’s always worth checking out local credit unions.

- Dealership Financing: This is often the most convenient option, as you can apply for a loan right at the dealership. They act as intermediaries, connecting you with various lenders. While convenient, the rates offered might not always be the most competitive, as dealerships often add their own markup. Common mistakes to avoid are accepting dealership financing without comparing it to outside offers; always get independent quotes first.

- Online Lenders: The digital age has brought forth numerous online lenders specializing in auto loans. They often boast quick approval processes and can cater to a wider spectrum of credit profiles, including those with limited credit. Their rates can be very competitive, and it’s easy to compare offers from multiple online lenders from the comfort of your home. However, ensure they are reputable and secure.

Pre-Approval: Your Secret Weapon in Car Shopping

Getting pre-approved for a car loan before you step foot in a dealership is one of the most powerful strategies you can employ as a first-time buyer. It transforms you from a vulnerable shopper into a confident buyer with clear financial boundaries. Pre-approval means a lender has provisionally agreed to lend you a certain amount of money at a specific interest rate, based on a preliminary review of your credit and financial information.

The benefits of pre-approval are manifold. Firstly, it gives you a firm budget to work with, preventing you from falling in love with a car you can’t afford. You’ll know exactly how much you can spend, which narrows down your search and makes the car buying process much more efficient. Secondly, it provides you with significant negotiating power at the dealership. You walk in with an offer already in hand, allowing you to negotiate the car’s price separately from the financing. If the dealership can beat your pre-approved rate, great! If not, you have a solid backup.

Most importantly, pre-approval involves a "soft inquiry" on your credit report, which does not negatively impact your credit score. Once you formally apply for a loan, it becomes a "hard inquiry." Pro tips from us: Apply for pre-approval with a few different lenders within a short timeframe (typically 14-45 days, depending on the credit scoring model). This will be treated as a single inquiry for credit scoring purposes, minimizing the impact on your credit score while maximizing your chances of finding the best rate.

The Application Process: What Lenders Really Want to See

Once you’ve done your homework and explored your options, it’s time to formally apply for your first car loan. This stage requires attention to detail and transparency. Lenders are looking for a complete picture of your financial stability and your ability to repay the loan.

Essential Documents You’ll Need: Be Prepared!

A smooth application process hinges on having all your necessary documents ready. Lenders will require various forms of identification and proof of income and residency to verify your information and assess your risk. Being organized can save you time and prevent delays.

Here’s a common list of documents you should prepare:

- Proof of Identity: A valid government-issued ID, such as a driver’s license or passport.

- Proof of Income: Recent pay stubs (typically the last two or three months), W-2 forms, or tax returns if you are self-employed. Lenders want to confirm your employment stability and income level.

- Proof of Residency: A utility bill (electricity, water, gas) or a lease agreement showing your current address.

- Bank Statements: Recent statements (usually the last two or three months) to show your financial activity and ability to manage funds.

- Social Security Number: Required for credit checks.

- Trade-in Information (if applicable): If you’re trading in a vehicle, you’ll need its title, registration, and any existing loan information.

Pro tips from us: Organize these documents in a folder or digital file before you even start the application process. This shows lenders you are serious and prepared, and it makes your life much easier. Double-check that all information on your documents matches your application exactly. Inconsistencies can raise red flags and cause delays.

Understanding Loan Terms: APR, Loan Term, and Total Cost

When reviewing a loan offer, it’s crucial to understand the key terms beyond just the monthly payment. These factors significantly impact the overall cost of your loan and your financial commitment.

- APR (Annual Percentage Rate): This is the most important number after the loan amount itself. The APR represents the total cost of borrowing money annually, including the interest rate and any fees associated with the loan. A lower APR means less money paid in interest over time. Common mistakes to avoid are confusing the interest rate with the APR; the APR gives you the true cost. For a first-time buyer, your APR might be higher due to limited credit history, so focusing on lowering this percentage should be a priority.

- Loan Term: This refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term generally means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer loan term will result in lower monthly payments, making the car seem more affordable, but you’ll end up paying significantly more in total interest. We advise finding a balance that offers manageable payments without extending the loan term unnecessarily long.

- Total Cost of the Loan: This is the sum of the principal amount borrowed plus all the interest you will pay over the entire loan term. Always ask your lender for this figure. It provides the clearest picture of your total financial commitment and allows for a true comparison between different loan offers. Sometimes, a slightly lower monthly payment with a much longer term can result in a substantially higher total cost.

The Application Itself: Honesty and Accuracy

When filling out the loan application, honesty and accuracy are paramount. Lenders will verify the information you provide, and any discrepancies can lead to delays, denials, or even accusations of fraud. Take your time to fill out every section carefully and completely.

Be truthful about your income, employment history, and existing debts. Lenders use this information to assess your ability to repay the loan responsibly. They will review your credit history, employment stability, and your debt-to-income ratio. If you’re a first-time buyer with a new job, be prepared to explain your employment situation. Don’t exaggerate your income or downplay your financial obligations. Providing false information can have serious consequences beyond just a loan denial. A transparent application builds trust and increases your chances of approval.

Post-Approval and Beyond: Smart Steps for Your New Ride

Congratulations, your loan is approved! This is an exciting moment, but the journey isn’t over. The final steps involve making smart choices about your vehicle, navigating the dealership, and ensuring you maintain a positive financial standing.

Choosing Your Car Wisely: Aligning Your Loan with Your Vehicle

With a pre-approved loan in hand, you now have the power to choose your car wisely. This isn’t just about finding a vehicle you like; it’s about making a practical decision that aligns with your budget and long-term financial goals.

Stick rigorously to your pre-approved budget. It’s easy to get swayed by extra features or a slightly more expensive model once you’re at the dealership, but exceeding your budget can lead to financial strain. Consider cars that are known for reliability, good fuel economy, and strong resale value. These factors will save you money on maintenance, fuel, and depreciation in the long run. Based on my experience, many buyers get emotionally attached to a car that doesn’t fit their budget or needs, leading to buyer’s remorse.

Always test drive any car you’re considering. Don’t rush this step. Drive it on different types of roads, including highways and local streets, to get a true feel for its performance and comfort. Check all the features, listen for any unusual noises, and ensure it meets your practical needs. Consider a pre-purchase inspection by an independent mechanic, especially for used cars, to uncover any hidden issues.

Understanding the Dealership Process: Negotiation and Paperwork

Walking into a dealership prepared is crucial. Remember, you have your pre-approved loan, which gives you leverage. Your primary goal at this stage is to negotiate the price of the car itself, separate from the financing.

Start by negotiating the "out-the-door" price of the vehicle. This includes the car’s price, taxes, and any fees. Once you’ve agreed on a price, you can then present your pre-approved loan offer. If the dealership can beat it, fantastic. If not, you have a solid financing option already secured. Common mistakes to avoid are letting the salesperson combine the car price and loan payments into a single discussion; this can obscure the true cost of each. Be firm but polite in your negotiations.

When it comes to paperwork, do not rush. Read every document carefully before signing. Pay close attention to the final loan agreement, verifying the interest rate (APR), loan term, and total amount financed. Understand all fees, including documentation fees, registration fees, and sales tax. Be wary of pressure to add on extras like extended warranties, rustproofing, or GAP insurance if you haven’t researched them and determined their value for your specific situation. While some add-ons can be beneficial, they also increase your total loan amount and monthly payment.

Making On-Time Payments: Protecting Your Financial Future

Once you drive off the lot, your most important responsibility begins: making your car loan payments on time, every time. This is not just about avoiding late fees; it’s about building a strong credit history and setting yourself up for future financial success.

Late payments can severely damage your credit score, making it harder and more expensive to get future loans (like a mortgage or another car loan). They also incur late fees, adding to your financial burden. To ensure you never miss a payment, set up automatic payments from your bank account if your lender offers this option. Alternatively, set multiple reminders on your phone or calendar a few days before the due date.

Consistent, on-time payments demonstrate financial responsibility and will significantly improve your credit score over time. This positive payment history will make it easier to secure better interest rates and terms on future loans and credit products. Your first car loan is a golden opportunity to establish a robust credit profile, so treat it with the seriousness it deserves.

For more tips on improving your credit score, read our detailed guide on .

Considering whether to buy new or used? Check out our article: .

For an in-depth understanding of how credit scores are calculated and what factors influence them, you can visit the official FICO website at .

Conclusion

Securing your first car loan might seem like a daunting task, but with careful preparation, informed decision-making, and a strategic approach, it’s entirely manageable. This journey is about more than just getting a set of wheels; it’s about laying a solid foundation for your financial future. By understanding your budget, proactively building your credit, exploring all your lending options, and meticulously reviewing loan terms, you empower yourself to make a truly smart and beneficial choice.

Remember, the goal is not just to get approved, but to get approved for the best possible terms that fit your financial situation. Take your time, ask questions, and don’t be afraid to negotiate. Your first car loan is a significant financial step, and by following the advice in this guide, you’ll be well on your way to enjoying the open road with confidence and peace of mind. Start your preparation today, and soon you’ll be cruising in your very own car!