How to Pay Off My Car Loan Faster: Your Ultimate Guide to Financial Freedom

How to Pay Off My Car Loan Faster: Your Ultimate Guide to Financial Freedom Carloan.Guidemechanic.com

The weight of a car loan can feel like a constant companion, silently draining your finances month after month. For many, the dream of owning their vehicle outright, free from interest payments and monthly obligations, is a significant financial milestone. If you’re wondering how to pay off my car loan more quickly, you’ve landed in the right place. This comprehensive guide will equip you with the knowledge and actionable strategies to accelerate your car loan payoff, save a substantial amount in interest, and achieve true financial freedom.

Paying off your car loan early isn’t just about cutting costs; it’s about reclaiming a piece of your financial life. It’s about redirecting funds towards other goals, reducing stress, and building a more robust financial foundation. We’ll dive deep into the undeniable benefits, crucial considerations, and powerful strategies that will help you eliminate that car payment sooner than you ever thought possible.

How to Pay Off My Car Loan Faster: Your Ultimate Guide to Financial Freedom

Why Pay Off Your Car Loan Early? The Undeniable Benefits

Deciding to pay off your car loan early is a proactive financial move that yields a multitude of advantages. It’s not just about getting rid of a bill; it’s about unlocking significant financial benefits that can impact your overall well-being. Let’s explore why this strategy is often a smart choice.

1. Experience True Financial Freedom and Peace of Mind

Imagine a world without that monthly car payment hanging over your head. The psychological relief alone can be immense. Freeing up a significant portion of your budget means less financial stress and more peace of mind. You’ll have greater flexibility to handle unexpected expenses or pursue new financial goals without the added burden of debt.

2. Achieve Significant Interest Savings

This is often the most compelling reason to accelerate your car loan payoff. Car loans, especially those with higher interest rates or longer terms, can accumulate a surprising amount of interest over time. By paying off your loan earlier, you reduce the total number of payments you make, directly cutting down the amount of interest the lender charges you. The sooner you eliminate the principal, the less interest has a chance to accrue.

3. Free Up Cash Flow for Other Important Goals

Once your car loan is paid off, that monthly payment amount becomes available cash in your pocket. This newfound cash flow can be directed towards a variety of other financial priorities. You could bolster your emergency fund, contribute more to retirement savings, invest in a down payment for a home, or tackle other high-interest debts like credit cards. This reallocated money becomes a powerful tool for building wealth.

4. Build Equity Faster and Protect Against Depreciation

Vehicles are depreciating assets, meaning their value decreases over time. When you have a loan, you’re constantly battling against this depreciation. By paying off your car loan faster, you build equity in your vehicle more quickly. This means you’re less likely to be "upside down" on your loan (owing more than the car is worth), which is a common and stressful situation for many car owners. Building equity provides a buffer and a stronger financial position if you ever need to sell or trade in your car.

5. Improve Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a crucial metric lenders use to assess your ability to manage monthly payments and repay debts. By eliminating your car loan, you significantly reduce your overall monthly debt obligations. A lower DTI ratio can make it easier to qualify for other loans in the future, such as a mortgage, and often at more favorable interest rates.

Pro tips from us: Always view an early car loan payoff as an investment in your future self. The money you save in interest and the financial flexibility you gain are tangible rewards for your discipline.

Assessing Your Current Car Loan Situation

Before you can effectively accelerate your car loan payoff, it’s crucial to have a clear understanding of your current loan terms. Knowledge is power, and knowing the specifics of your debt will help you formulate the most effective strategy.

1. Gather Your Loan Documents

Start by collecting all relevant paperwork related to your car loan. This includes your original loan agreement, recent statements, and any online account access information. You’ll need to pinpoint key details such as your current principal balance, annual percentage rate (APR), remaining loan term (number of months), and your exact monthly payment amount. Having these figures readily available is the first step towards taking control.

2. Calculate Your Total Remaining Cost

Don’t just look at your remaining principal. Use an online car loan calculator or consult your lender to understand the total amount you will pay if you only make the minimum payments for the rest of your loan term. This figure includes both the remaining principal and the interest that will accrue over the remaining months. Seeing this larger number can be a powerful motivator to find ways to reduce it.

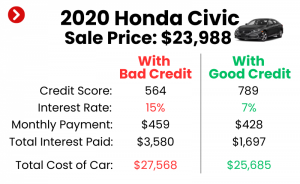

3. Understand Your Interest Rate – Is it High?

Your car loan’s interest rate plays a critical role in how much you’ll save by paying it off early. Generally, the higher your interest rate, the more beneficial it is to pay the loan off quickly. A high APR means a larger portion of your early payments goes towards interest, making early payoff an even more impactful decision. Conversely, if your interest rate is very low, the urgency might be less, but the benefits of freeing up cash flow still apply.

Common mistakes to avoid are guessing your loan details or relying on outdated information. Always verify your current principal balance and interest rate directly with your lender before making any significant payment adjustments. This ensures your efforts are accurately applied and maximizes your savings.

Powerful Strategies to Accelerate Your Car Loan Payoff

Now that you understand the benefits and your current loan situation, let’s explore actionable strategies to help you pay off your car loan faster. These methods range from simple adjustments to more significant financial overhauls, offering something for everyone.

Strategy 1: Making Extra Payments Consistently

This is perhaps the most straightforward and effective method. Every extra dollar you put towards your principal balance directly reduces the amount on which interest is calculated.

- Round Up Your Payments: Even small, consistent efforts add up. If your payment is $345, consider paying $350 or $375 each month. That extra $5-$30 directly attacks your principal without feeling like a huge sacrifice. Over a year, this can amount to hundreds of extra dollars applied.

- Make One Extra Payment Per Year: Divide your monthly payment by 12 and add that amount to each of your regular monthly payments. For example, if your payment is $300, pay an extra $25 each month ($300/12). By the end of the year, you’ll have made the equivalent of an entire extra payment. This simple trick can shave months off your loan term and save you considerable interest.

- Apply Lump Sums: Whenever you receive unexpected money – a work bonus, a tax refund, a gift, or even proceeds from selling something you no longer need – consider dedicating a portion or all of it to your car loan. A single lump sum payment can have a dramatic effect, especially early in the loan term, as it reduces a large chunk of the principal immediately.

Pro tips from us: Always specify to your lender that any extra payments should be applied directly to the principal balance. Otherwise, they might automatically apply it to future payments, which doesn’t accelerate your payoff or save you interest.

Strategy 2: Embrace Bi-Weekly Payments

This clever strategy can help you make an extra payment each year without feeling the pinch. Instead of making one full payment monthly, you make half of your payment every two weeks.

- How it Works: There are 52 weeks in a year, which means 26 bi-weekly periods. If you make half your payment every two weeks, you’ll end up making 26 half-payments annually. This is equivalent to 13 full monthly payments per year, rather than the standard 12. That one extra payment per year can significantly shorten your loan term and reduce total interest paid.

- Set It and Forget It: Many lenders offer bi-weekly payment options. If yours doesn’t, you can manually set up bi-weekly transfers to your loan account or save the half-payment amount every two weeks and then make an additional full payment at the end of the year. This consistency makes it easier to stick to the plan.

Based on my experience, setting up bi-weekly payments as an automatic transfer is one of the easiest ways to accelerate your payoff. It works in the background, making progress without requiring constant attention or difficult budgeting decisions.

Strategy 3: Refinance Your Car Loan for a Better Rate

Refinancing involves taking out a new loan to pay off your existing one, ideally with more favorable terms. This can be a game-changer if your credit score has improved or interest rates have dropped since you originally financed your vehicle.

- When It’s a Good Idea: If your credit score has significantly improved, or if current market interest rates are lower than your existing rate, refinancing could save you a lot of money. You might also refinance to shorten your loan term, even if the interest rate stays similar, which forces you to pay it off faster.

- The Process: Shop around with various lenders – banks, credit unions, and online lenders – to compare interest rates and terms. Get pre-approved to see what rates you qualify for without impacting your credit score. Be sure to compare the total cost of the new loan, including any fees, against the savings you’d get from a lower interest rate. You can find more information on refinancing options from trusted sources like the Consumer Financial Protection Bureau (CFPB) to ensure you’re making an informed decision.

- Pros and Cons: The primary pro is significant interest savings and potentially a lower monthly payment or a shorter loan term. The cons can include closing costs or fees associated with the new loan, and a temporary dip in your credit score from the hard inquiry.

Strategy 4: Dedicate Windfalls and Bonuses

Unexpected money can feel like a gift, and it’s tempting to spend it. However, directing these funds towards your car loan can be one of the quickest ways to make a substantial dent in your debt.

- Tax Refunds: Many people receive tax refunds annually. Instead of viewing it as "extra spending money," consider it an opportunity to fast-track your car loan payoff.

- Work Bonuses or Commissions: If your job offers performance bonuses or commissions, earmark a portion of these funds specifically for your car loan.

- Unexpected Gifts or Inheritances: While these are less common, any unexpected influx of cash can be a powerful tool for debt reduction.

The key is to be intentional with these funds. Before the money even hits your account, make a plan to send it directly to your car loan’s principal.

Strategy 5: Sell Your Current Vehicle (If Financially Prudent)

While this is a more drastic measure, for some, it’s the most effective path to debt freedom. This strategy is particularly relevant if you are "upside down" on your loan or if your current car payment is a significant strain on your budget.

- When This Makes Sense: If you owe more than your car is worth, or if your monthly payments are crippling your budget, selling your car might be a smart move. You’d use the sale proceeds to pay off as much of the loan as possible, then potentially buy a cheaper, more affordable used car (perhaps even paying cash) to eliminate debt entirely.

- Considerations: Research your car’s market value thoroughly. Factor in any potential costs associated with selling (e.g., detailing, minor repairs). Be realistic about what you can afford for a replacement vehicle and ensure it meets your needs. This requires careful planning but can be a powerful reset button for your finances.

Strategy 6: Budgeting and Cutting Expenses

The foundation of any successful debt payoff plan is a solid budget. By identifying areas where you can cut back, you free up more money to direct towards your car loan.

- Create a Detailed Budget: Track every dollar you spend for a month or two. This will reveal exactly where your money is going.

- Identify Areas to Save: Look for non-essential expenses that can be reduced or eliminated. This could include cutting down on dining out, cancelling unused subscriptions, reducing entertainment costs, or finding cheaper alternatives for daily necessities.

- Reallocate Savings: Every dollar you save from your budget should be immediately reallocated to your car loan. Think of it as finding "extra" payments within your existing income. This discipline is paramount for consistent progress.

If you’re looking for more detailed strategies on managing your money, check out our guide on Budgeting for Financial Success: Your Path to Wealth (Internal Link Placeholder).

Strategy 7: Debt Snowball or Avalanche Method

These popular debt payoff strategies can be applied effectively to your car loan, especially if you have other debts as well.

- Debt Snowball: You pay minimums on all debts except the smallest one, which you attack with all extra funds. Once the smallest debt is paid off, you roll that payment amount into the next smallest debt, creating a "snowball" effect. This method is great for building momentum and motivation.

- Debt Avalanche: You pay minimums on all debts except the one with the highest interest rate, which you prioritize. This method saves you the most money in interest over time.

While a car loan might not always be your smallest or highest interest debt, integrating it into one of these strategies can provide a clear roadmap and accelerate its payoff alongside your other financial obligations.

Important Considerations Before Accelerating Your Payments

While paying off your car loan early offers significant advantages, it’s not always the absolute best first step for everyone. There are critical financial considerations to weigh before you aggressively pursue an early payoff.

1. Establish a Robust Emergency Fund First

Before you throw every extra dollar at your car loan, ensure you have a fully funded emergency fund. This fund should ideally cover 3-6 months of essential living expenses. Life is unpredictable, and having a financial safety net is paramount. Without it, an unexpected job loss or medical emergency could force you into more debt, negating your car loan payoff efforts. Common mistakes to avoid are neglecting your emergency fund in pursuit of quick debt payoff. Life happens, and having a financial safety net is paramount.

2. Prioritize High-Interest Debt Over Your Car Loan

If you have other debts with significantly higher interest rates, such as credit card balances (often 18-25% APR or more) or high-interest personal loans, these should typically be your primary focus. The interest savings from eliminating a credit card balance will almost always outweigh the savings from a car loan, which usually has a much lower APR. Tackle the most expensive debt first to maximize your overall financial efficiency.

3. Evaluate Investment Opportunities (Opportunity Cost)

Consider the opportunity cost of paying off your car loan early. If your car loan has a very low interest rate (e.g., 2-3%), you might be able to get a better return by investing that extra money in a retirement account (like a 401k or IRA) or other investment vehicles. While debt freedom is valuable, a low-interest car loan might not be your absolute highest financial priority if your investments are projected to yield a higher return. This is a personal decision based on your risk tolerance and financial goals.

4. Check for Prepayment Penalties

Most car loans do not have prepayment penalties, but it’s crucial to confirm this by reviewing your loan agreement or contacting your lender directly. A prepayment penalty is a fee charged by the lender if you pay off your loan earlier than scheduled. If your loan does have one, calculate whether the penalty outweighs the interest savings you’d achieve by paying it off early. In most cases, the savings will still win out, but it’s a factor to be aware of.

5. Understand the Impact on Your Credit Score

Paying off a loan, including a car loan, is generally positive for your credit score in the long run. It reduces your debt burden and improves your credit utilization. However, you might see a slight, temporary dip in your score immediately after the account is closed. This is because a paid-off account removes an active trade line from your credit report and reduces your average age of accounts. This is usually a minor and temporary effect, and the benefits of debt freedom far outweigh this small fluctuation.

Pro tips from us: Always consider your entire financial picture. An early car loan payoff is a great goal, but it should align with your broader financial plan and not come at the expense of more critical financial foundations like an emergency fund or higher-interest debt.

The Day You Pay It Off: What to Do Next

Congratulations! The day you make that final car loan payment is a moment to celebrate. But your work isn’t quite done. There are a few important steps to take to ensure everything is properly documented and handled.

1. Get Written Confirmation of Payoff

Don’t just assume the loan is closed. Request a formal "paid in full" letter or statement from your lender. This document is your official proof that you no longer owe money on the vehicle. Keep this record in a safe place with your other important financial documents.

2. Obtain Your Vehicle Title

Once the loan is paid off, the lienholder (your lender) no longer has a claim on your vehicle. They are legally obligated to release the title to you. Depending on your state, this might be mailed to you automatically, or you might need to request it. Ensure the title is transferred into your name, free and clear of any liens. This is crucial for selling or trading in your car in the future.

3. Update Your Insurance

While you still need comprehensive and collision coverage to protect your asset, you may no longer be required to carry specific coverage levels mandated by your lender. Review your policy with your insurance provider to adjust coverage if desired. This could potentially lead to further savings on your monthly premiums.

4. Celebrate (Responsibly)!

You’ve worked hard to achieve this financial milestone. Take a moment to acknowledge your accomplishment! Perhaps treat yourself to a nice dinner or a small reward, but avoid falling back into old spending habits. This celebration marks the beginning of a new chapter of financial freedom.

Now that your car loan is paid off, you have a new stream of cash flow. For ideas on how to best utilize this freed-up money, read our article on What to Do After Paying Off Debt: Maximizing Your Newfound Freedom (Internal Link Placeholder).

Drive Towards Financial Freedom

Paying off your car loan is a journey, not a sprint, but it’s a journey well worth taking. From the significant interest savings to the invaluable peace of mind, the benefits are clear. By understanding your current loan, implementing strategic extra payments, considering refinancing, and maintaining a disciplined budget, you can dramatically accelerate your payoff timeline.

Remember to prioritize your emergency fund and higher-interest debts first, ensuring your financial foundation is solid. Once that final payment is made, you’ll not only own your car outright but also unlock a new level of financial flexibility and freedom. Start today, and take control of your car loan – and your financial future.