How to Qualify For a Car Loan: Your Ultimate Guide to Driving Away with Confidence

How to Qualify For a Car Loan: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

The dream of a new set of wheels – the fresh car smell, the open road, the freedom – it’s a powerful vision. But before you can cruise into the sunset, there’s a crucial step: securing a car loan. Understanding how to qualify for a car loan is not just about filling out an application; it’s about strategically positioning yourself as a reliable borrower in the eyes of lenders.

This comprehensive guide will demystify the car loan qualification process, equipping you with the knowledge and actionable strategies to confidently secure the financing you need. We’ll dive deep into every factor lenders consider, from your credit score to your income, and provide insider tips to help you drive away with the best possible terms. Get ready to turn your car ownership dream into a reality!

How to Qualify For a Car Loan: Your Ultimate Guide to Driving Away with Confidence

The Foundation: What Lenders Really Look For

When you apply for a car loan, lenders are essentially assessing risk. They want to know if you’re a responsible borrower who will repay the money on time. This assessment isn’t arbitrary; it’s based on a set of well-defined criteria that paint a picture of your financial health.

Based on my experience in the automotive finance world, the core elements lenders scrutinize can be summarized as the "Five Cs of Credit": Character, Capacity, Capital, Collateral, and Conditions. While this might sound complex, we’ll break down each aspect into easy-to-understand terms, focusing on how you can present the best possible profile.

The Importance of Pre-Approval

One of the most powerful steps you can take before even stepping foot in a dealership is to get pre-approved for a car loan. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a certain amount of money at a specific interest rate, before you’ve even chosen a car.

Pro tips from us: Pre-approval gives you immense bargaining power at the dealership. You walk in knowing your budget and your interest rate, which allows you to focus solely on negotiating the car’s price, rather than being swayed by dealer-offered financing that might not be as competitive. It’s like having cash in hand!

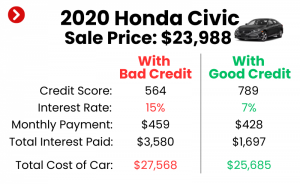

Your Credit Score: The Ultimate Deciding Factor

Your credit score is arguably the most critical factor in determining whether you will qualify for a car loan and what interest rate you’ll receive. It’s a three-digit number that summarizes your entire credit history, acting as a quick snapshot of your reliability as a borrower.

Lenders use this score to predict the likelihood of you repaying your loan. A higher score signals lower risk, potentially leading to better interest rates and more favorable loan terms. Conversely, a lower score can mean higher interest rates or even outright loan denial.

What is a Credit Score?

Credit scores are primarily generated by two major scoring models: FICO and VantageScore. While both assess your creditworthiness, they use slightly different methodologies and scales. FICO scores typically range from 300 to 850, as do VantageScores, though some older VantageScore models used a different range.

These scores are calculated using information from your credit reports, which are maintained by the three major credit bureaus: Experian, Equifax, and TransUnion. Your credit report details your borrowing history, including credit cards, mortgages, and past loans.

Why Your Credit Score Matters for Car Loans

For car loans specifically, lenders often look for a good credit score because the vehicle itself serves as collateral. If you default on the loan, the lender can repossess the car. However, they’d much rather you pay consistently, so they prioritize borrowers with a proven track record of responsible repayment.

A strong credit score can literally save you thousands of dollars over the life of your car loan through lower interest rates. This means your monthly payments will be more manageable, and a larger portion of each payment will go towards paying down the principal balance.

Good, Fair, Poor: What Each Means for You

Understanding the general ranges of credit scores can help you gauge your standing:

- Excellent (780-850): You’re a prime candidate for the best interest rates and loan terms available. Lenders will be eager to work with you.

- Good (670-779): You’re still in a strong position to qualify for a car loan with competitive rates. You might not get the absolute lowest rates, but they will be very good.

- Fair (580-669): This is where it gets trickier. You can likely still get a car loan, but your interest rates will be higher, reflecting the increased risk for the lender.

- Poor (300-579): Qualifying for a traditional car loan will be challenging. You might need to explore subprime lenders, consider a co-signer, or be prepared for very high interest rates and less favorable terms.

Tips to Improve Your Credit Score Before Applying

If your credit score isn’t where you want it to be, don’t despair! There are steps you can take to improve it before you apply.

- Check Your Credit Report: Obtain free copies of your credit reports from AnnualCreditReport.com. Review them for errors and dispute any inaccuracies immediately, as these can negatively impact your score.

- Pay Bills On Time: Payment history is the most significant factor in your credit score. Make sure all your payments – credit cards, utilities, rent – are made punctually.

- Reduce Credit Card Debt: High credit utilization (using a large percentage of your available credit) can hurt your score. Aim to keep your balances below 30% of your credit limits.

- Avoid New Credit: Don’t open new credit accounts right before applying for a car loan, as new inquiries and accounts can temporarily lower your score.

For a deeper dive into boosting your credit health, you might find our article on Understanding and Improving Your Credit Score helpful.

Income and Employment Stability: Proving Your Repayment Ability

Beyond your credit score, lenders need to be confident that you have the financial capacity to make your monthly car loan payments. This is where your income and employment history come into play. Lenders want to see a steady, verifiable source of income that is sufficient to cover your new debt obligations.

Your ability to pay is a cornerstone of the lender’s decision. They’re looking for evidence of consistent earnings that won’t suddenly disappear, leaving them with an unpaid loan.

Minimum Income Requirements

While there isn’t a universal minimum income requirement across all lenders, most will have an internal threshold. This threshold isn’t just about the dollar amount; it’s about the ratio of your income to your existing debts and the proposed new car payment.

Common mistakes to avoid are not accurately representing your income or failing to account for all your monthly expenses. Lenders will scrutinize your income against your debt obligations to determine affordability.

Verifying Your Income

Lenders will require proof of your income. This typically involves:

- Pay stubs: Usually, the most recent one or two will suffice if you’re a W-2 employee.

- Bank statements: Often requested to show consistent direct deposits of your salary.

- Tax returns: Especially if you’re self-employed, these are crucial for verifying income over a longer period.

- Employment verification: Some lenders may contact your employer directly to confirm your employment status and salary.

Ensure you have these documents readily available and that they clearly reflect your current income. Any discrepancies could delay your application or even lead to denial.

Employment History Matters

Lenders prefer borrowers with a stable employment history. Someone who has been in the same job or industry for several years is generally seen as less risky than someone who frequently changes jobs or has significant gaps in employment. A consistent work history demonstrates reliability and a steady income stream.

Pro tips from us: Aim for at least two years of consistent employment with your current employer or in the same industry. If you’ve recently changed jobs but remained in the same field with a promotion or increased salary, explain this clearly to your lender.

Special Cases: Self-Employed or Gig Workers

If you’re self-employed, a freelancer, or a gig worker, proving income can be a bit more complex, but it’s certainly possible to qualify for a car loan. Lenders will typically require:

- Two to three years of tax returns: These are essential to demonstrate consistent income and profitability.

- Bank statements: To show regular deposits and cash flow.

- Profit and Loss (P&L) statements: If you run a business, these provide a clearer picture of your ongoing financial health.

It’s wise to maintain meticulous financial records and keep your business and personal finances separate. This makes income verification much smoother for lenders.

Debt-to-Income (DTI) Ratio: A Key Metric for Lenders

Your Debt-to-Income (DTI) ratio is a critical indicator lenders use to assess your ability to manage monthly payments and take on additional debt. It compares your total monthly debt payments to your gross monthly income. A high DTI suggests you might be overextended, making it riskier for a lender to approve your car loan.

Understanding and managing your DTI is crucial for any major loan application, including a car loan. It’s a clear snapshot of your financial obligations versus your earning capacity.

What is DTI?

Your DTI is expressed as a percentage. It represents how much of your gross monthly income goes towards paying your existing debts. These debts typically include credit card minimum payments, student loan payments, mortgage or rent payments, and any other loan payments (like personal loans).

It does not include living expenses like utilities, groceries, or entertainment. It’s strictly about recurring debt obligations.

How to Calculate Your DTI

Calculating your DTI is straightforward:

- Sum your total monthly debt payments: Add up all your minimum monthly payments for credit cards, student loans, mortgage/rent, and any other loans.

- Determine your gross monthly income: This is your income before taxes and deductions.

- Divide your total monthly debt payments by your gross monthly income: Multiply the result by 100 to get a percentage.

Example: If your total monthly debt payments are $1,000 and your gross monthly income is $4,000, your DTI is ($1,000 / $4,000) * 100 = 25%.

Ideal DTI for Car Loan Approval

Most lenders prefer a DTI ratio of 36% or lower. Some may go up to 43%, but generally, the lower your DTI, the better your chances of approval and securing favorable terms. A low DTI indicates that you have plenty of disposable income to comfortably handle a new car payment.

Common mistakes to avoid are neglecting to calculate your DTI before applying. Knowing this number gives you a realistic understanding of your financial standing from a lender’s perspective.

Strategies to Lower Your DTI

If your DTI is higher than ideal, here are some strategies to improve it:

- Pay Down Existing Debts: Focus on paying off credit card balances or small personal loans. Reducing the principal will lower your minimum monthly payments.

- Increase Your Income: If possible, consider taking on a side hustle or asking for a raise. Even a small increase in gross income can impact your DTI.

- Avoid New Debt: Refrain from taking on any new loans or credit card debt before applying for a car loan. This would only push your DTI higher.

The Down Payment: Showing Your Commitment

A down payment is the initial amount of money you pay upfront when purchasing a car, reducing the amount you need to borrow. While not always strictly required, making a down payment is highly recommended and can significantly improve your chances to qualify for a car loan with better terms.

It signals to the lender that you are financially committed to the purchase and are less likely to default. It also immediately reduces the loan-to-value ratio, which we’ll discuss shortly.

Why a Down Payment is Crucial

A down payment demonstrates your financial stability and reduces the lender’s risk. If you put money down, you have equity in the vehicle from day one. This means if you were to default early in the loan term, the lender would likely recover more of their money by repossessing and selling the car.

Furthermore, a down payment can prevent you from being "upside down" on your loan, which means owing more than the car is worth. This situation can happen quickly with depreciation, especially on new vehicles.

How Much Should You Put Down?

Pro tips from us: While there’s no fixed rule, a general guideline is to aim for at least 10-20% of the car’s purchase price for a used car, and 20% or more for a new car. A larger down payment translates to a smaller loan amount, lower monthly payments, and less interest paid over the life of the loan.

Even a small down payment is better than none. Every dollar you put down reduces the amount you need to finance.

Benefits of a Larger Down Payment

- Lower Monthly Payments: A smaller loan principal means your monthly payments will be more affordable.

- Less Interest Paid: You’ll pay interest on a smaller amount, saving you money over the life of the loan.

- Better Loan Terms: Lenders are often more willing to offer lower interest rates to borrowers who make substantial down payments.

- Reduced Risk of Being Upside Down: A larger down payment provides a buffer against rapid depreciation.

- Easier Qualification: Especially if your credit isn’t perfect, a significant down payment can offset other risk factors, making it easier to qualify for a car loan.

The Vehicle Itself: Its Role in Loan Approval

It might seem counterintuitive, but the car you choose also plays a role in whether you will qualify for a car loan. Lenders evaluate the vehicle’s value, age, and condition because it serves as the collateral for the loan. They need to ensure that the car’s value is sufficient to cover the loan amount if they ever need to repossess and sell it.

This assessment is about protecting their investment. A lender won’t approve a loan for more than a vehicle is realistically worth, as that would put them at significant risk.

New vs. Used Car Considerations

- New Cars: Generally easier to finance because their value is well-established, and they come with manufacturer warranties. Lenders see them as lower risk. However, they depreciate quickly.

- Used Cars: Can be harder to finance, especially older models or those with high mileage. Lenders may impose stricter age or mileage limits. The interest rates on used car loans are also typically higher than for new cars, reflecting the increased risk due to potential mechanical issues and faster depreciation relative to their remaining value.

Common mistakes to avoid are falling in love with a car that’s significantly overpriced or too old for most lenders’ comfort levels. Do your research on vehicle values using resources like Kelley Blue Book or Edmunds.

Vehicle Value and Depreciation

Lenders will assess the car’s market value to ensure the loan amount is reasonable. They use industry guides to determine the car’s current worth. Be aware that cars begin to depreciate the moment they are driven off the lot.

This depreciation can be a factor, particularly if you make a small down payment. If the car’s value drops significantly below your loan balance, you’re "underwater," making it harder to sell or trade in the car without financial loss.

Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) ratio is another crucial metric. It compares the amount you want to borrow to the car’s market value. For example, if a car is valued at $20,000 and you want to borrow $18,000, your LTV is 90% ($18,000 / $20,000).

Lenders generally prefer a lower LTV, as it indicates less risk. An LTV of 100% or less is ideal, meaning you’re borrowing no more than the car is worth. If your LTV is significantly above 100% (e.g., you’re rolling negative equity from a previous car into the new loan), it will be much harder to qualify for a car loan, and the interest rates will be higher.

Collateral and Co-Signers: Additional Avenues to Qualify

Sometimes, even with a decent credit score and stable income, you might need an extra boost to qualify for a car loan, especially if you’re looking for the best rates. This is where understanding collateral and the option of a co-signer comes into play. These elements can significantly strengthen your loan application by reducing the lender’s perceived risk.

They act as safety nets, giving the lender more confidence in your ability to repay the loan, or at least recover their losses if you can’t.

Understanding Collateral

In a car loan, the vehicle itself serves as collateral. This means that if you fail to make your loan payments as agreed, the lender has the legal right to repossess the car to recover the money you owe. This is why lenders pay close attention to the vehicle’s value and condition.

While the car is always the primary collateral, sometimes lenders might look for additional collateral, though this is less common for standard car loans. It’s more typical in situations like a secured personal loan where you might pledge other assets.

The Power of a Co-Signer

A co-signer is someone who agrees to be equally responsible for the loan repayment if the primary borrower defaults. This person’s credit history, income, and assets are considered alongside yours during the application process. Having a co-signer with excellent credit and a stable financial background can significantly improve your chances to qualify for a car loan and secure a better interest rate, especially if you have:

- Poor or no credit history: A co-signer can bridge this gap.

- A high DTI ratio: Their income can help balance the ratio.

- Insufficient income: Their income can boost the perceived repayment capacity.

Pro tips from us: Choose a co-signer wisely. It should be someone you trust deeply and who understands the full implications of their commitment.

Risks and Responsibilities of Co-Signing

While a co-signer can be a lifeline, it’s crucial for both parties to understand the risks:

- Equal Responsibility: The co-signer is legally obligated to repay the loan if the primary borrower cannot. This means their credit will be damaged if payments are missed.

- Impact on Credit: The loan will appear on the co-signer’s credit report, affecting their DTI and their ability to get other loans.

- Damaged Relationships: If the primary borrower defaults, it can strain or even destroy personal relationships.

Common mistakes to avoid are co-signing for someone without fully understanding their financial habits or your own ability to take on their debt if necessary.

Applying for a Car Loan: The Practical Steps

Once you’ve done your homework and are confident in your financial standing, it’s time to take the practical steps to apply for your car loan. This stage involves gathering documents, comparing lenders, and understanding the terms presented to you. Being prepared will make the process smoother and more efficient.

The goal here is not just to qualify for a car loan, but to qualify for the best car loan available to you. This requires diligence and a proactive approach.

Gathering Your Documents

Before you start applying, have all your necessary documents in order. This will streamline the process and demonstrate your readiness to lenders. You’ll typically need:

- Proof of Identity: Driver’s license, state ID.

- Proof of Residence: Utility bill, lease agreement.

- Proof of Income: Recent pay stubs (W-2), tax returns (self-employed), bank statements.

- Social Security Number: For credit checks.

- Employment Information: Employer’s name, address, and phone number.

- Existing Debt Information: Mortgage/rent statements, credit card statements, other loan statements.

Having these documents organized and accessible will save you time and potential headaches during the application process.

Shopping Around for Lenders

Do not settle for the first loan offer you receive, especially if it’s from a dealership. It’s vital to shop around and compare offers from multiple lenders to find the best rates and terms. Lenders include:

- Banks: Your personal bank might offer competitive rates due to your existing relationship.

- Credit Unions: Often known for offering lower interest rates and more flexible terms than traditional banks.

- Online Lenders: Many reputable online platforms specialize in car loans and can provide quick pre-approvals.

- Dealerships: While convenient, their rates might not always be the most competitive. Use their offer as a benchmark after you’ve secured pre-approvals elsewhere.

Pro tips from us: When comparing offers, focus on the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing.

Understanding Loan Terms (APR, Loan Term)

Before you sign any loan agreement, fully understand the key terms:

- Annual Percentage Rate (APR): This is the total cost of borrowing, expressed as a yearly percentage. It includes the interest rate and any additional fees. A lower APR means a cheaper loan.

- Loan Term: This is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term means higher monthly payments but less interest paid overall. A longer term means lower monthly payments but more interest over time.

For more detailed information on loan terminology, check out our guide on Understanding Car Loan Interest Rates and Terms.

The Application Process

Once you’ve chosen a lender, you’ll complete a formal application. This will involve a "hard inquiry" on your credit report, which can slightly lower your score temporarily. However, multiple car loan inquiries within a short period (typically 14-45 days, depending on the scoring model) are usually counted as a single inquiry, so shop around within that window.

Be honest and accurate with all the information you provide. Misrepresenting facts can lead to denial or even legal consequences.

Special Situations: When Qualification Seems Harder

Sometimes, life throws curveballs that make it seem harder to qualify for a car loan. Whether you’ve faced financial setbacks or are just starting your credit journey, there are still pathways to securing vehicle financing. It might require a bit more effort or a different approach, but it’s often achievable.

Understanding these special situations and the strategies to navigate them is key to not giving up on your car ownership goals.

Qualifying for a Car Loan with Bad Credit

Having bad credit (typically a FICO score below 600) makes it challenging, but not impossible, to get a car loan. Here’s what you can expect and how to improve your chances:

- Higher Interest Rates: Lenders will charge significantly higher interest rates to compensate for the increased risk.

- Subprime Lenders: You may need to seek out lenders who specialize in subprime auto loans. These lenders are more willing to work with borrowers with poor credit but will have stricter terms.

- Larger Down Payment: A substantial down payment can greatly improve your chances and offset your credit score.

- Co-Signer: As discussed, a co-signer with good credit can be a game-changer.

- Consider a Less Expensive Car: A cheaper car means a smaller loan, which is less risky for the lender.

- Proof of Stability: Strong proof of stable income and employment becomes even more critical.

Qualifying for a Car Loan with No Credit History

If you’re new to credit, perhaps a recent graduate or someone who has always paid cash, you’ll face the "no credit, no problem… for us, the lender" scenario. Lenders have no history to assess your repayment behavior. Strategies include:

- Start Building Credit: Get a secured credit card or a small personal loan to start building a positive credit history.

- Co-Signer: This is often the most effective route for first-time borrowers.

- Proof of Income & Stability: Emphasize your steady income, employment history, and any savings.

- Utility Bills & Rent Payments: Some alternative lenders may consider on-time utility or rent payments as proof of responsible financial behavior, though this is less common for traditional auto loans.

- Dealership Financing: Some dealerships have programs for first-time buyers, though rates might be higher.

Dealing with Repossessions or Bankruptcies

These are significant negative marks on your credit report that make it very difficult to qualify for a car loan immediately. However, time heals all wounds, especially in credit.

- Time is Your Ally: Wait as long as possible after a bankruptcy (it stays on your report for 7-10 years) or repossession. The further in the past it is, the less impact it will have.

- Rebuild Credit: Focus intensely on rebuilding your credit with new, positive accounts.

- Explanation Letter: Be prepared to write a letter explaining the circumstances that led to the bankruptcy or repossession, demonstrating that you’ve learned from the experience and are now in a better financial position.

- Large Down Payment & Co-Signer: These become almost essential tools in these situations.

Common Mistakes to Avoid

Even with all the right information, it’s easy to make missteps during the car loan process. Avoiding these common mistakes can save you money, time, and stress, ensuring you effectively qualify for a car loan on the best possible terms.

Based on my observations, many borrowers fall into similar traps that could have been easily circumvented with a bit of foresight.

Not Checking Your Credit

One of the most frequent and impactful errors is not checking your credit report and score before you apply. You might be unaware of errors, outdated information, or even identity theft that could be dragging down your score.

Pro tips from us: Always get your free credit reports and review them thoroughly. Dispute any inaccuracies immediately. Knowing your score gives you a realistic expectation of the rates you’ll qualify for.

Applying to Too Many Lenders at Once

While shopping around is crucial, indiscriminately applying to dozens of lenders within a short period can backfire. Each "hard inquiry" can slightly ding your credit score. Although most credit scoring models group multiple auto loan inquiries within a specific timeframe (usually 14-45 days) as a single inquiry, spreading them out over months will negatively impact your score.

Be strategic: Get pre-approved by 2-3 reputable lenders within a concentrated window, then use those offers to negotiate at the dealership.

Ignoring the Total Cost of Ownership

Many borrowers focus solely on the monthly payment. However, the true cost of a car involves much more than just the loan payment. Common mistakes to avoid are neglecting to factor in:

- Insurance: This can be a significant monthly expense, especially for new drivers or expensive vehicles.

- Maintenance & Repairs: Used cars, in particular, can come with unexpected repair costs.

- Fuel: Consider the car’s fuel efficiency based on your driving habits.

- Registration & Taxes: These are often one-time or annual costs.

Look at the bigger picture to ensure the car truly fits within your overall budget.

Not Being Realistic About Your Budget

It’s easy to get caught up in the excitement of car shopping and stretch your budget beyond what’s truly comfortable. Lenders might approve you for a higher amount than you can realistically afford after factoring in all your other living expenses.

Be honest with yourself about your budget. Use a conservative approach and ensure your new car payment, plus all associated costs, leaves you with enough disposable income for emergencies and other necessities.

Conclusion: Drive Away with Confidence

Successfully navigating the journey to qualify for a car loan is about empowerment through knowledge. By understanding the key factors lenders consider – your credit score, income, debt-to-income ratio, down payment, and even the vehicle itself – you can strategically prepare your finances and present yourself as a reliable borrower.

Remember, preparation is your greatest asset. Check your credit, gather your documents, shop around for the best rates, and be realistic about your budget. With these strategies, you’ll not only secure the financing you need but also drive away with the peace of mind that comes from a smart financial decision.

Don’t let the process intimidate you. Take control, follow these steps, and soon you’ll be enjoying the open road in your new vehicle, confident in the choices you’ve made. Happy driving!