How to Renegotiate a Car Loan: Your Ultimate Guide to Better Terms

How to Renegotiate a Car Loan: Your Ultimate Guide to Better Terms Carloan.Guidemechanic.com

Are you feeling the pinch of high monthly car payments? Did you secure your car loan when your credit wasn’t at its best, or have interest rates simply shifted since then? If so, you’re not alone. Many drivers find themselves in a position where their current car loan terms no longer align with their financial reality or goals. The good news is that you don’t have to be stuck. Learning how to renegotiate a car loan can be a powerful financial move, potentially saving you thousands of dollars over the life of your loan and significantly improving your monthly cash flow.

This comprehensive guide will walk you through every step of the process, from understanding why renegotiation is a smart option to preparing your documents, approaching lenders, and ultimately securing better car loan terms. We’ll dive deep into the strategies that work, common pitfalls to avoid, and provide you with expert tips to maximize your chances of success. Our mission is to empower you with the knowledge to take control of your car financing, making it more manageable and aligned with your financial well-being.

How to Renegotiate a Car Loan: Your Ultimate Guide to Better Terms

Why Consider Renegotiating Your Car Loan?

Life happens, and financial circumstances are rarely static. The car loan you signed a year or two ago might no longer be the best fit for your current situation. Understanding the key reasons to explore renegotiation is the first step toward taking action. It’s not just about getting a lower payment; it’s about optimizing your financial health.

One of the most common reasons people consider renegotiating their car loan is a significant change in their financial situation. Perhaps you’ve experienced a job loss, a new family expense, or an unexpected medical bill that makes your current monthly payment a burden. Conversely, you might have landed a better job or received a raise, making you eligible for more favorable terms than when you first applied. Renegotiating can help align your loan with your current income and expenses.

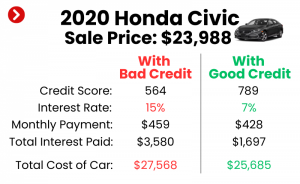

Another major driver for renegotiation is an improvement in your credit score. When you initially financed your vehicle, especially if your credit history was less than perfect, you likely accepted a higher interest rate. If you’ve diligently made on-time payments, paid down other debts, and your credit score has significantly improved, you’re a much more attractive borrower to lenders now. This improvement is a golden opportunity to secure a lower interest rate and reduce your overall cost of borrowing.

Furthermore, market interest rates don’t stand still. What might have been a competitive rate a few years ago could now be significantly higher than what’s currently available. Economic shifts can lead to lower average interest rates, creating an environment where you can potentially refinance your existing loan into a new one with a more attractive rate. Staying informed about these trends can alert you to prime opportunities for car loan renegotiation.

Finally, you might simply want to reduce the total amount of interest you pay over the life of the loan. By securing a lower interest rate, even if your monthly payment doesn’t drastically change, you can save a substantial amount in the long run. Alternatively, you might want to shorten your loan term to pay off the car faster, reducing the total interest paid and freeing up your budget sooner. Whatever your specific goal, renegotiating your car loan offers flexibility and the potential for significant savings.

Key Factors That Influence Car Loan Renegotiation

Before you even pick up the phone, it’s crucial to understand the factors that lenders consider when evaluating a potential car loan renegotiation. These elements will dictate your leverage and the kinds of terms you can expect to achieve. Being aware of these points will help you prepare and present your case effectively.

The single most influential factor is undoubtedly your credit score. Lenders use your credit score as a primary indicator of your creditworthiness and your likelihood of repaying a loan. A higher credit score signals lower risk, which translates to better interest rates and more favorable terms. If your credit score has improved since you first took out your loan, you have a strong argument for renegotiation. Conversely, if your score has dropped, it might be more challenging, but not impossible, to secure better terms.

Current market interest rates also play a pivotal role. The rates available today might be different from when you first financed your car. If general interest rates have fallen, you’re in a better position to renegotiate for a lower rate. Keep an eye on economic indicators and what other lenders are offering; this information will be valuable during your discussions.

Your loan-to-value (LTV) ratio is another critical component. This ratio compares the amount you still owe on your car loan to the car’s current market value. Lenders prefer a lower LTV because it means their risk is reduced; if you default, they can recoup more of their losses by selling the vehicle. If you owe more than your car is worth (you’re "upside down" or have negative equity), renegotiation can be significantly harder. However, if you’ve paid down a good portion of your loan and your car has held its value well, your LTV will be more favorable.

Your payment history on the current car loan is equally important. Consistently making on-time payments demonstrates reliability and responsibility to lenders. It shows that even with your existing terms, you are a dependable borrower. A flawless payment record significantly strengthens your case for better terms, as it proves you’re a low-risk individual who honors their financial commitments.

Finally, your relationship with your current lender can sometimes influence the process. If you have multiple accounts with them or have been a long-standing customer, they might be more willing to work with you to retain your business. However, don’t rely solely on loyalty; always be prepared to explore options with other lenders to ensure you’re getting the best possible deal.

Preparation is Key: What You Need Before You Start

Based on my experience, thorough preparation is half the battle won when it comes to successfully renegotiating a car loan. Walking into a conversation with a lender fully informed and organized not only boosts your confidence but also signals to them that you are serious and financially responsible. This meticulous approach can significantly impact the outcome of your renegotiation efforts.

Your first step should be to gather all relevant documents. This includes your current car loan statements, which detail your remaining balance, interest rate, and original terms. You’ll also need recent pay stubs or proof of income to demonstrate your current financial capacity. Have your car’s Vehicle Identification Number (VIN) and title information readily available. These documents provide the factual basis for your renegotiation and will be requested by any potential lender.

Next, it’s absolutely crucial to check your credit score and report. Your credit score is the most significant determinant of the interest rates you’ll be offered. You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, TransUnion) annually through AnnualCreditReport.com. Review it for any inaccuracies and understand where you stand. If your score has improved since you took out the original loan, this is powerful leverage. Knowing your score beforehand allows you to set realistic expectations and negotiate from a position of strength.

You also need to know your car’s current market value. Websites like Kelley Blue Book (KBB.com) and Edmunds.com provide excellent tools for estimating your vehicle’s trade-in and private party value based on its make, model, year, mileage, and condition. This information is vital for calculating your loan-to-value (LTV) ratio, which, as discussed, is a key factor for lenders. If you owe significantly more than your car is worth, it might make refinancing more challenging.

With all this information, calculate your current loan details thoroughly. Understand not just your monthly payment, but also your total remaining balance, your current interest rate, and how much interest you will pay over the remaining life of the loan. This comprehensive understanding will allow you to accurately compare any new offers and truly grasp the potential savings.

Before engaging with any lender, determine your primary goal for renegotiating. Do you desperately need a lower monthly payment to free up cash flow? Are you more interested in securing a lower interest rate to reduce the total cost of the loan? Or perhaps you want to shorten your loan term to pay off the car faster? Clearly defining your objective will help you evaluate offers and stay focused during negotiations.

Finally, research new loan offers from various lenders. Don’t just rely on your current lender. Explore options from other banks, credit unions, and online lenders. Credit unions, in particular, often offer very competitive rates. Getting pre-qualified or receiving multiple quotes will give you a benchmark and strengthen your negotiating position. You’ll be able to confidently say, "Another lender offered me X%," which can encourage your current lender to match or beat that offer. This step is critical for ensuring you secure the absolute best terms available to you.

Step-by-Step Guide: How to Renegotiate Your Car Loan

Once you’ve done your homework and gathered all the necessary information, you’re ready to actively pursue renegotiating your car loan. This process can be broken down into clear, actionable steps that will guide you toward a successful outcome. Approaching this systematically will help you navigate the options and make an informed decision.

Step 1: Contact Your Current Lender First

Your initial point of contact should always be your current lender. There are several advantages to starting here. They already have your loan information, and depending on your payment history, they might be more willing to work with you to retain your business. Sometimes, securing a better deal with your existing lender can be simpler than going through a full refinancing process with a new institution.

When you call or visit, clearly state your intention: you want to renegotiate your car loan for more favorable terms. Be prepared to present your improved credit score, any changes in your financial situation that make you a stronger borrower, or the fact that market rates have dropped. Ask them what options they can offer, such as a lower interest rate, a different payment schedule, or even a modified loan term. Be polite but firm in your request.

Step 2: Explore Refinancing with Other Lenders

If your current lender can’t or won’t offer terms that meet your goals, or if you simply want to ensure you’re getting the absolute best deal, it’s time to explore refinancing with other financial institutions. This involves taking out a new loan from a different lender to pay off your existing car loan. Many lenders specialize in auto loan refinancing and actively compete for your business.

Look beyond traditional banks. Credit unions often provide very competitive interest rates and personalized service to their members. Online lenders have also become a popular choice, offering streamlined application processes and quick approvals. Apply to several lenders to get multiple quotes. This allows you to compare annual percentage rates (APRs), loan terms, and any associated fees side-by-side. Remember that each application might result in a "hard inquiry" on your credit report, but if done within a short shopping window (typically 14-45 days, depending on the credit model), they will usually be counted as a single inquiry, minimizing the impact on your score.

Step 3: Understand the New Loan Offer

Once you receive offers, don’t just look at the monthly payment. Pro tips from us: Always dig into the details of each new loan offer. Request a complete breakdown of the proposed new loan terms. This includes the new interest rate (APR), the total loan amount, the new loan term, and any fees associated with the refinancing process, such as origination fees or application fees.

It’s crucial to calculate the total cost of the new loan over its entire term, including all interest and fees, and compare it to the remaining total cost of your current loan. A lower monthly payment might sound appealing, but if it comes with a significantly longer loan term, you could end up paying more in total interest. Ensure the new offer genuinely aligns with your financial goals, whether that’s reducing overall cost, lowering monthly payments, or shortening the repayment period.

Step 4: Make Your Decision and Finalize

After carefully comparing all your options, choose the new loan offer that best suits your financial situation and goals. Once you’ve made your decision, the lender will guide you through the final paperwork. This typically involves signing a new loan agreement, and the new lender will then pay off your old loan.

Ensure you read all documents thoroughly before signing. Verify that all the terms you agreed upon are accurately reflected in the contract. Once everything is finalized, keep copies of all your new loan documents for your records. This step officially concludes the renegotiation process, putting you on track with improved car loan terms.

Common Pitfalls and Mistakes to Avoid

While renegotiating your car loan can lead to significant financial benefits, it’s also easy to fall into traps that could undermine your efforts or even leave you worse off. Being aware of these common mistakes can help you navigate the process more effectively and secure the best possible outcome. Avoiding these missteps is just as important as following the correct steps.

One of the most frequent errors is not checking your credit score before starting the process. As we’ve emphasized, your credit score is paramount. Going into negotiations without knowing your score means you’re guessing what terms you might qualify for, and you could miss out on a better deal or waste time applying for loans you won’t get. Always pull your credit report and score first.

Another significant pitfall is focusing only on the monthly payment while ignoring the total interest paid. A lender might offer you a significantly lower monthly payment, but often this is achieved by extending the loan term. While it provides immediate relief to your budget, it almost always means you’ll pay more in total interest over the life of the loan. Always calculate the total cost of the loan, not just the monthly installment.

Similarly, extending the loan term too much is a common mistake. While a longer term reduces your monthly payment, it also means you’ll be paying interest for a longer period. This can lead to paying substantially more overall and potentially puts you at risk of being "upside down" on your loan (owing more than the car is worth) for a longer duration. Carefully weigh the trade-off between a lower payment and the total cost.

Not shopping around for the best rates is another costly error. Settling for the first offer you receive, or only checking with your current lender, means you could be leaving money on the table. Different lenders have different criteria and offer varying rates. As discussed, getting multiple quotes allows you to compare and leverage those offers to get the most competitive terms available.

Finally, ignoring associated fees can add unexpected costs. Some lenders charge origination fees, application fees, or other administrative costs for refinancing. While a new loan might have a lower interest rate, these fees could eat into your savings, especially if the savings aren’t substantial. Always ask for a full breakdown of all fees and factor them into your total cost comparison. A truly beneficial renegotiation considers all these elements to ensure real savings.

When Renegotiation Might Not Be the Best Option

While the idea of securing better car loan terms is appealing, there are specific situations where renegotiating or refinancing might not be the most advantageous move. Understanding these scenarios can save you time and prevent you from incurring unnecessary costs or making a less-than-optimal financial decision. It’s important to be realistic about your options.

One primary instance is if you are significantly upside down on your loan, meaning you owe substantially more than your car’s current market value. Lenders are often hesitant to refinance a loan with a very high loan-to-value (LTV) ratio because it increases their risk. If you have negative equity, it might be better to focus on paying down the principal to improve your LTV before attempting to renegotiate.

Similarly, if your credit score hasn’t significantly improved since you took out the original loan, or if it has even declined, you might not qualify for better interest rates. Lenders base their offers on your creditworthiness, and if that hasn’t changed positively, new terms might not be any better than your current ones. In this case, focusing on credit score improvement should be your priority first.

If you already have a very low interest rate on your existing car loan, the potential for savings through renegotiation might be minimal. The effort involved in applying for a new loan, even if the rate is slightly lower, might not be worth the marginal savings. Carefully calculate the potential interest savings versus the time and effort required.

Finally, if your loan is almost paid off, refinancing might not make sense. The bulk of the interest on a car loan is typically paid in the early years. By the time you’re nearing the end of your loan term, most of your payments are going toward the principal. The small amount of remaining interest might not justify the fees or administrative hassle of taking out a new loan. In such cases, simply continuing to pay off your existing loan as planned is often the most straightforward and cost-effective approach.

Pro Tips for Success

Beyond the step-by-step process, there are several expert strategies and insights that can significantly improve your chances of successfully renegotiating your car loan. These pro tips are drawn from years of experience in financial advising and will give you an edge in securing the best possible terms.

Firstly, be polite but firm in your interactions with lenders. A respectful attitude goes a long way, but don’t shy away from clearly stating your expectations and demonstrating that you’ve done your research. Lenders are more likely to work with a well-informed and articulate customer.

Always have all your information ready before you start any conversation or application. This includes your credit report, current loan statements, proof of income, and your car’s market value. Being organized shows professionalism and makes the process much smoother and faster for both you and the lender.

Understand your ‘why’ deeply. Whether it’s to lower monthly payments, reduce total interest, or shorten the loan term, knowing your primary objective will help you evaluate offers and stay focused during negotiations. Don’t let a lender sway you from your core financial goal.

Consider improving your credit score proactively before even beginning the renegotiation process. Even a small increase in your score can open doors to significantly better interest rates. Pay down other debts, make all payments on time, and avoid opening new credit lines in the months leading up to your renegotiation efforts. For more detailed advice, you can check out our article on .

Lastly, if your credit score isn’t strong enough on its own, or if you’re looking for an even better rate, consider a co-signer. A co-signer with excellent credit can significantly boost your application, potentially allowing you to qualify for lower interest rates that you wouldn’t get on your own. Just ensure both parties understand the responsibilities involved. For a deeper dive into car loan specifics, you might find our guide on helpful.

Conclusion

Renegotiating a car loan might seem like a daunting task, but as this comprehensive guide illustrates, it’s an entirely achievable goal that can lead to substantial financial benefits. By understanding the underlying factors, preparing diligently, and approaching the process strategically, you can take control of your car financing and align it more closely with your current financial reality. Whether your aim is to reduce your monthly payments, lower the overall cost of your loan, or simply achieve more favorable terms, the power to make these changes is within your reach.

Remember, you are not obligated to stick with the original terms forever, especially if your financial situation or the market has changed. Armed with the right information and a clear plan, you can successfully navigate the process of car loan renegotiation, securing a deal that works better for you. Don’t let financial stress dictate your car ownership experience. Start your journey today toward more manageable and cost-effective car loan terms. Your future self will thank you for taking this proactive step towards greater financial freedom.