How to Secure a $14,000 Car Loan: Your Ultimate Guide to Approval and Best Rates

How to Secure a $14,000 Car Loan: Your Ultimate Guide to Approval and Best Rates Carloan.Guidemechanic.com

Embarking on the journey to purchase a vehicle, especially one in the $14,000 range, can feel like a significant financial step. Whether you’re eyeing a reliable used car or an entry-level new model, securing a $14,000 car loan requires careful planning and a clear understanding of the lending landscape. This comprehensive guide is designed to arm you with the knowledge and strategies you need to not only get approved but also lock in the best possible terms.

We’ll delve into everything from understanding your credit score to navigating the pre-approval process, ensuring you’re well-equipped to make an informed decision. Our goal is to make the process of obtaining a 14k car loan as smooth and stress-free as possible, providing real value every step of the way.

How to Secure a $14,000 Car Loan: Your Ultimate Guide to Approval and Best Rates

Understanding the $14,000 Car Loan Landscape

A $14,000 car loan is a very common amount that many people seek. This budget often aligns with the price point of a wide variety of quality used cars, as well as some entry-level new vehicles, making it a popular choice for first-time buyers or those looking for a dependable second car. It’s a sweet spot where affordability meets reliability for many consumers.

When considering a car loan for $14,000, it’s crucial to understand what this amount can typically buy you. You might find a well-maintained sedan a few years old, a compact SUV, or even a smaller, brand-new car with basic features. The market is diverse, so your $14,000 can go a long way if you shop smart.

The key factors influencing your ability to secure a $14,000 car loan and the terms you receive are primarily your creditworthiness, income stability, and the specifics of the vehicle itself. These elements combine to form your financial profile in the eyes of potential lenders.

The Cornerstone: Your Credit Score

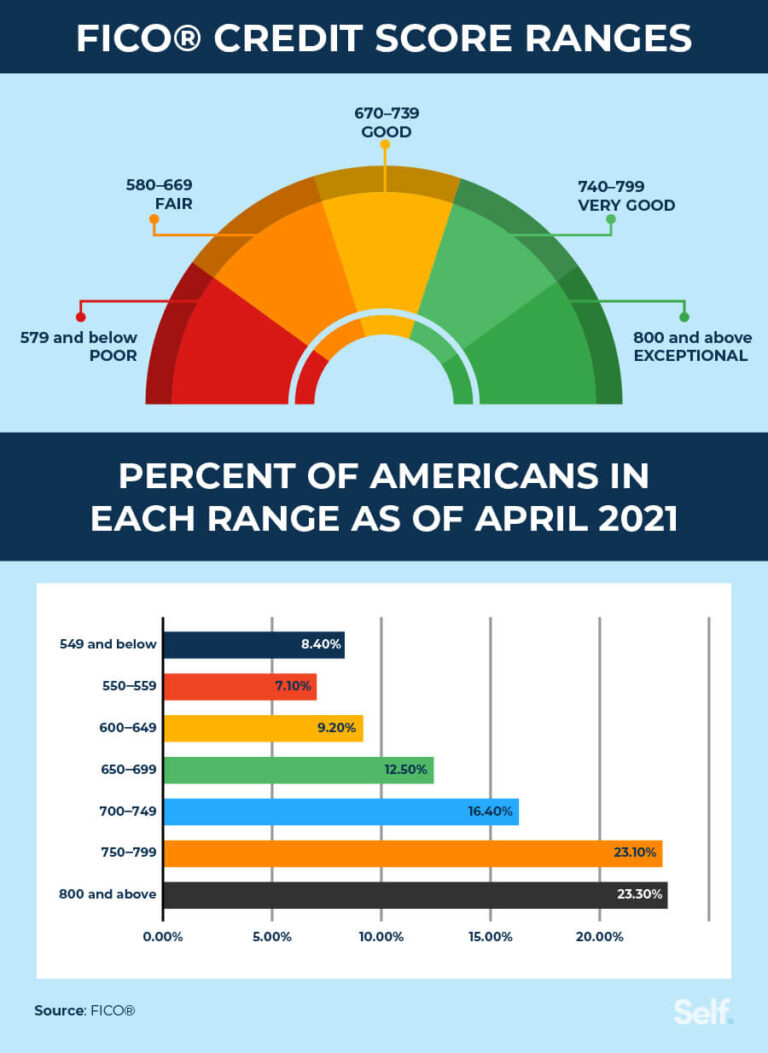

Your credit score is arguably the single most important factor when applying for any loan, including a $14,000 car loan. It’s a three-digit number that summarizes your credit history and predicts your likelihood of repaying debt. Lenders use it to quickly assess your risk level.

Most lenders rely on FICO scores or VantageScores, which range from 300 to 850. A higher score indicates lower risk, translating to better interest rates and more favorable loan terms. Understanding where your credit stands is the first step toward securing an affordable $14,000 car loan.

What Your Credit Score Means for Your Loan

- Excellent Credit (780-850): If you have excellent credit, you’re in an ideal position. Lenders will view you as a very low-risk borrower, offering you the lowest interest rates available. Securing a 14k car loan will be relatively straightforward with highly competitive terms.

- Good Credit (670-739): With good credit, you’ll still qualify for very good interest rates, though perhaps not the absolute lowest. Lenders will be eager to work with you, and your application for a $14,000 car loan should be approved without significant hurdles.

- Fair Credit (580-669): This is where things can get a bit more challenging. While you can still get a $14,000 car loan with fair credit, expect higher interest rates. Lenders see you as a moderate risk, and they compensate for that risk by charging more for the loan.

- Bad Credit (300-579): Obtaining a $14,000 car loan with bad credit is possible, but it comes with considerable challenges. Interest rates will be significantly higher, and you might need to meet additional requirements, such as a larger down payment or a co-signer. Lenders perceive bad credit as a high risk, and the cost of borrowing will reflect that.

Pro tips from us: Before you even start looking at cars, check your credit score and report. You can get free copies of your credit report from AnnualCreditReport.com and many credit card companies or financial apps offer free credit score access. Reviewing your report helps you identify any errors and understand areas for improvement. Based on my experience, correcting even minor inaccuracies can sometimes bump your score up enough to make a difference in your interest rate.

Essential Requirements for a $14,000 Car Loan

Beyond your credit score, lenders will look at several other factors to determine your eligibility for a $14,000 car loan. These requirements help them assess your overall financial health and capacity to repay the debt.

Income and Employment Stability

Lenders want to see a steady source of income. They’ll typically ask for proof of employment, such as pay stubs, W-2s, or tax returns if you’re self-employed. They use this information to calculate your debt-to-income (DTI) ratio, which compares your monthly debt payments to your gross monthly income. A lower DTI ratio indicates you have more disposable income to cover your loan payments, making you a more attractive borrower for a 14k car loan.

Having a stable employment history, typically at least six months to a year at your current job, also signals reliability to lenders. It shows you have a consistent ability to earn.

Down Payment

While not always strictly required, making a down payment significantly improves your chances of approval for a $14,000 car loan and can lead to better terms. A down payment reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the life of the loan.

Furthermore, a down payment demonstrates your commitment to the purchase and reduces the lender’s risk. Common advice suggests a down payment of at least 10-20% for a used car, but even a smaller amount can be beneficial.

Proof of Residence and Identification

You’ll need to provide documents that confirm your identity and current address. This typically includes a valid driver’s license and recent utility bills or a lease agreement. These are standard verification steps for any financial transaction.

Vehicle Specifics

The car you intend to finance also plays a role. Lenders often have requirements regarding the vehicle’s age, mileage, and title status. Older cars or those with very high mileage might be considered higher risk, as their value depreciates faster and they may require more maintenance. The vehicle itself acts as collateral for the $14,000 car loan, so lenders need to ensure it holds sufficient value.

Navigating the Application Process: Step-by-Step

Securing a $14,000 car loan can be a streamlined process if you know the steps. Being prepared and proactive can save you time, money, and stress.

Step 1: Get Pre-Approved

This is perhaps the most crucial step you can take before stepping foot in a dealership. Car loan pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount (like $14,000) at a certain interest rate, pending a final review and vehicle selection.

Pre-approval offers immense benefits. It gives you a clear budget, so you know exactly how much you can afford, and it transforms you into a cash buyer at the dealership. This negotiating power can help you focus solely on the car price, rather than getting caught up in payment discussions.

You can seek pre-approval from various sources: your existing bank or credit union, online lenders, or even through dealer financing departments. Be aware that pre-approval often involves a "soft" credit inquiry, which doesn’t harm your credit score, but a full application will usually trigger a "hard" inquiry.

Step 2: Gather Your Documents

Once you’re ready to apply for a $14,000 car loan, having all your documents in order will expedite the process. Create a checklist to ensure nothing is missed:

- Government-issued ID (driver’s license)

- Proof of income (pay stubs, W-2s, tax returns)

- Proof of residence (utility bill, lease agreement)

- Social Security Number

- Insurance information (once you’ve chosen a vehicle)

- Trade-in vehicle information (if applicable)

Step 3: Compare Loan Offers

Do not settle for the first loan offer you receive. This is a common mistake that can cost you hundreds or even thousands of dollars over the life of your $14,000 car loan. Shop around and compare offers from at least three to five different lenders.

Focus on these key aspects:

- Annual Percentage Rate (APR): This is the true cost of borrowing, encompassing the interest rate and any fees. A lower APR means a cheaper loan.

- Loan Term: This is the length of time you have to repay the loan (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but result in more interest paid overall.

- Monthly Payments: Ensure the monthly payment fits comfortably within your budget.

- Total Cost of the Loan: Calculate the total amount you’ll pay back, including principal and interest, to understand the full financial commitment.

Common mistakes to avoid are focusing solely on the monthly payment. A low monthly payment might seem appealing, but it often comes with a longer loan term and a significantly higher total interest paid. Always consider the APR and the total cost of the loan.

Step 4: Choose Your Vehicle Wisely

With your pre-approval in hand, you can confidently shop for your car. For a $14,000 car loan, you’ll likely be looking at a robust used car market.

- Research: Look up reviews, reliability ratings, and common issues for models within your price range.

- Vehicle History Report: Always get a CarFax or AutoCheck report. This will reveal critical information like accident history, previous owners, and service records.

- Independent Inspection: Based on my experience, spending $100-$200 on an independent mechanic’s inspection before purchasing is invaluable. They can spot hidden problems that could turn your great deal into a money pit.

Understanding Interest Rates and Monthly Payments

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. For a $14,000 car loan, this rate will significantly impact your monthly payments and the total amount you repay. Factors like your credit score, the loan term, and current market conditions all influence the rate you’re offered.

A higher interest rate means more of your monthly payment goes towards interest, and less towards the principal balance. Conversely, a lower rate means you pay off the car faster and save money.

The loan term, or repayment period, is also critical. A shorter term (e.g., 36 or 48 months) means higher monthly payments but less interest paid overall. A longer term (e.g., 60 or 72 months) reduces your monthly payment, making it seem more affordable, but you’ll pay significantly more in interest over the life of the $14,000 car loan.

Calculating Approximate Monthly Payments

Let’s illustrate with an example for a $14,000 car loan:

-

Scenario 1: Excellent Credit

- Loan Amount: $14,000

- Interest Rate (APR): 4.0%

- Loan Term: 60 months

- Approximate Monthly Payment: $258

- Total Interest Paid: Approximately $1,480

-

Scenario 2: Fair Credit

- Loan Amount: $14,000

- Interest Rate (APR): 8.0%

- Loan Term: 60 months

- Approximate Monthly Payment: $284

- Total Interest Paid: Approximately $3,040

As you can see, even a few percentage points difference in the interest rate can significantly impact the total cost of your $14,000 car loan. Using online car loan calculators can help you experiment with different rates and terms to find a payment that works for your budget.

Strategies for Challenging Credit Situations (Bad Credit $14,000 Car Loan)

If you’re looking for a $14,000 car loan with bad credit, the path can be more challenging, but it’s certainly not impossible. "Bad credit" typically refers to a FICO score below 580, indicating a higher risk to lenders.

Lenders offering bad credit 14000 car loan options often specialize in this niche, but they will charge significantly higher interest rates to offset the increased risk. It’s crucial to be cautious and informed.

Strategies to Improve Your Chances:

- Larger Down Payment: This is one of the most effective ways to mitigate bad credit. A substantial down payment reduces the amount you need to borrow and signals to the lender that you’re committed.

- Co-signer: If you have a friend or family member with good credit who is willing to co-sign, it can drastically improve your chances of approval and secure a better interest rate for your $14,000 car loan. Be aware that the co-signer is equally responsible for the debt.

- Secured Loan Options: Some lenders might offer a secured loan where the car itself is the collateral. This is standard for car loans, but for bad credit, they might be more stringent on the vehicle’s value.

- Specialty Lenders: While traditional banks might be hesitant, there are lenders who specifically work with individuals with bad credit. Do thorough research, read reviews, and compare offers carefully to avoid predatory lending practices.

- Improve Your Credit Score First: If you can wait, even a few months of focused effort to improve your credit score can make a huge difference. Pay all bills on time, reduce credit card balances, and avoid applying for new credit. For a deeper dive into improving your credit score, check out our comprehensive guide on .

Based on my experience: When dealing with bad credit, be wary of "guaranteed approval" lenders. Always read the fine print, understand all fees, and ensure the interest rate isn’t exorbitant. It’s better to secure a slightly less ideal loan than to fall into a high-interest trap that damages your finances further.

Beyond the Loan: Protecting Your Investment

Securing your $14,000 car loan is a significant achievement, but your financial responsibilities don’t end there. Protecting your new asset and budgeting for its ongoing costs are vital for long-term financial health.

Car Insurance Requirements

All lenders will require you to carry full coverage insurance (collision and comprehensive) on your vehicle for the duration of the loan. This protects their investment (the car) in case of an accident or damage. The cost of insurance can vary widely based on your age, driving record, location, and the specific vehicle. Get insurance quotes before finalizing your car purchase to ensure it fits into your budget.

Extended Warranties

Dealers often push extended warranties, especially for used cars. These can provide peace of mind, but they also come at a significant cost. Weigh the pros and cons carefully:

- Pros: Protection against unexpected repair costs, especially for older or high-mileage vehicles.

- Cons: High upfront cost, exclusions in coverage, and you might never use it.

Research the vehicle’s reliability and consider your personal risk tolerance before deciding on an extended warranty for your $14,000 car loan purchase.

Budgeting for Maintenance

Beyond your monthly car payment and insurance, remember to budget for regular maintenance (oil changes, tire rotations) and potential repairs. Even a reliable car will need upkeep. Setting aside a small amount each month for a "car fund" can prevent financial surprises down the road.

Boosting Your Chances of Approval and Getting Better Terms

To maximize your chances of getting approved for a $14,000 car loan with the best possible terms, consider these proactive steps:

- Improve Your Credit Score: As discussed, this is paramount. Pay all bills on time, keep credit utilization low, and avoid new credit applications in the months leading up to your loan application.

- Save for a Larger Down Payment: The more you put down, the less you borrow, which reduces the lender’s risk and can lead to a lower interest rate.

- Pay Off Small Debts: Reducing your overall debt load improves your debt-to-income ratio, making you a more attractive borrower.

- Maintain Stable Employment: Lenders prefer to see a consistent work history. If you’re planning a job change, try to secure your loan before making the move.

- Shop Around Aggressively for Lenders: Don’t just go with the first offer. Banks, credit unions, and online lenders all have different rates and criteria. Compare multiple offers within a short window (usually 14-45 days) so that multiple inquiries are treated as a single one by credit bureaus, minimizing impact on your score.

- Consider a Co-Applicant (Co-Signer): If your credit isn’t stellar, a co-signer with good credit can significantly improve your loan terms.

For those still weighing their options between financing a brand new car versus a used one, understanding the different implications can be crucial. Read our detailed comparison of to help you decide which path is best for your financial situation and your $14,000 car loan goals.

Conclusion

Securing a $14,000 car loan is a common and achievable goal for many car buyers. By understanding the critical role of your credit score, preparing your financial documents, and diligently comparing loan offers, you can navigate the process with confidence. Remember to get pre-approved, shop around for the best rates, and always consider the total cost of the loan, not just the monthly payment.

Whether you have excellent credit or are working to improve it, strategic planning and informed decision-making are your best allies. With this comprehensive guide, you are now equipped to approach your 14k car loan journey smartly, ensuring you drive away with a vehicle you love and a loan that fits your financial well-being. Good luck on your car buying adventure!

External Resource:

For more detailed information on understanding your credit and managing debt, consult the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/