How to Secure a $2500 Car Loan with Bad Credit: Your Ultimate Guide to Approval and Affordable Driving

How to Secure a $2500 Car Loan with Bad Credit: Your Ultimate Guide to Approval and Affordable Driving Carloan.Guidemechanic.com

Navigating the world of car loans can feel like a daunting challenge, especially when your credit score isn’t perfect. For many, a reliable vehicle isn’t a luxury; it’s an absolute necessity for work, family, and daily life. The good news is that securing a $2500 car loan, even with bad credit, is often more achievable than you might think.

This comprehensive guide is designed to equip you with the knowledge, strategies, and confidence to find a suitable $2500 car loan. We understand the frustration and apprehension that comes with past financial hiccups. Our goal is to demystify the process, provide actionable advice, and help you drive away in the car you need, while also building a stronger financial future. Let’s dive in.

How to Secure a $2500 Car Loan with Bad Credit: Your Ultimate Guide to Approval and Affordable Driving

Understanding the Landscape: Why a $2500 Car Loan with Bad Credit is Different

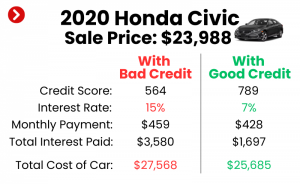

When your credit history has a few bumps, lenders view you as a higher risk. "Bad credit" typically refers to a FICO score below 620, though some subprime lenders might consider scores even lower. This classification impacts the interest rates you’re offered and the types of lenders willing to work with you.

Traditional banks, for instance, often prefer borrowers with excellent credit because they represent a lower risk of default. They have strict criteria and less flexibility. For someone seeking a $2500 car loan bad credit, these institutions might not be the primary avenue.

However, the landscape shifts when you’re looking for a smaller loan amount like $2500. This sum is less intimidating for some lenders compared to a $20,000 or $30,000 loan. While the risks are still present, the potential loss for the lender is significantly smaller, which can open up more opportunities for approval.

It’s crucial to set realistic expectations from the outset. You might not qualify for the lowest interest rates, and the loan terms might be shorter. However, the objective here is to secure a working vehicle and, importantly, to use this loan as a stepping stone to rebuild your credit.

Preparing for Your Loan Application: Your Best Strategy

Success in securing a $2500 car loan with bad credit often hinges on thorough preparation. Walking into the application process informed and organized significantly boosts your chances of approval and helps you secure better terms. This isn’t just about finding a lender; it’s about presenting yourself as the most reliable borrower you can be.

1. Know Your Credit Score and Report Inside Out

Before you even think about approaching a lender, you absolutely must know where you stand. Check your credit score and, more importantly, obtain copies of your full credit reports from all three major bureaus: Experian, Equifax, and TransUnion. You are legally entitled to one free report from each bureau every 12 months via AnnualCreditReport.com.

Based on my experience, many people skip this crucial step, leading to nasty surprises during the application process. Your credit report is a detailed history of your financial reliability. It lists all your credit accounts, payment history, public records (like bankruptcies), and inquiries. Look for any errors or inaccuracies; even a small mistake could be unfairly dragging down your score. Disputing these can sometimes give your score a quick, vital boost. Understanding what’s on your report allows you to anticipate potential lender concerns and address them proactively. For a deeper dive into understanding your credit report and how to dispute errors, we recommend visiting the Federal Trade Commission’s guide at FTC.gov on Credit Reports.

2. Assess Your Financial Health: Budgeting and Income Stability

Lenders want to see that you can comfortably afford the loan payments. This means looking at your income versus your existing debts and monthly expenses. Create a detailed budget. Calculate your total monthly income and then list all your fixed and variable expenses.

What’s left over is your discretionary income, which lenders will use to determine your debt-to-income (DTI) ratio. A lower DTI ratio indicates you have more money available to cover new loan payments, making you a less risky borrower. Showing proof of steady income – through pay stubs, tax returns, or bank statements – is paramount. Lenders want consistency. For detailed budgeting tips that can help you prepare for car ownership, see our guide on .

3. Maximize Your Down Payment Power

Even with a small loan like $2500, a down payment can be a game-changer. While you might think a few hundred dollars won’t make a difference, it signals responsibility and commitment to lenders. A down payment reduces the amount you need to borrow, thereby lowering the lender’s risk.

Pro tips from us: Even if you can only put down $250, $500, or $1000, it significantly improves your application. It shows you have some savings and are willing to invest your own money into the purchase. This can lead to better loan terms, a slightly lower interest rate, or even the difference between approval and denial. Start saving every spare penny you can towards this goal.

4. Gather All Necessary Documents

Being prepared with all your paperwork makes the application process smoother and faster. Lenders will typically ask for:

- Proof of Identity: Driver’s license or state ID.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Income: Recent pay stubs (usually 2-3 months), tax returns (if self-employed), bank statements.

- Proof of Insurance: You’ll need to show you can insure the vehicle.

- References: Sometimes required, especially for subprime lenders.

Having these documents neatly organized demonstrates your seriousness and efficiency, which can leave a positive impression on the lender.

Where to Find a $2500 Car Loan When Your Credit is Less Than Perfect

Finding the right lender is half the battle when you’re seeking a $2500 car loan with bad credit. Not all financial institutions are created equal, and some specialize in working with borrowers who have challenging credit histories. Knowing where to look can save you time, effort, and frustration.

1. Specialty Bad Credit Lenders and Online Platforms

These lenders specifically cater to individuals with lower credit scores. They understand the nuances of bad credit and structure their loans accordingly. While their interest rates might be higher than traditional banks, they offer a viable path to approval.

- Subprime Lenders: These are financial institutions that specialize in lending to borrowers with non-prime credit scores. They assess risk differently and often look beyond just the credit score, considering factors like your income stability and ability to make payments.

- Online Lending Networks: Numerous online platforms act as aggregators, connecting you with multiple lenders who specialize in bad credit auto loans. You fill out one application, and they match you with potential lenders. This can be efficient for comparing offers without multiple hard inquiries on your credit. Be sure to read reviews and check their reputation.

2. Dealerships with In-House Financing (Buy Here, Pay Here)

"Buy Here, Pay Here" (BHPH) dealerships are a common option for those struggling to get approved elsewhere. These dealerships act as both the seller and the lender, providing financing directly to the customer. They often have very flexible approval criteria, as they focus heavily on your income and ability to make payments, sometimes even more than your credit score.

Common mistakes to avoid are not understanding the high interest rates and fees associated with BHPH loans. While they offer convenience and a high approval rate for a $2500 car loan bad credit, their interest rates can be significantly higher than other options. Always scrutinize the full loan terms, including the total cost of the car, the interest rate (APR), and any additional fees. Ensure you understand the payment schedule and what happens if you miss a payment.

3. Credit Unions: A Member-Focused Approach

Credit unions are non-profit financial cooperatives owned by their members. Because of their structure, they often have more flexible lending criteria and are generally more willing to work with members to find solutions, even for those with bad credit. If you’re already a member of a credit union, or if you qualify for membership (often based on location, employer, or association), they can be an excellent resource.

They might offer slightly lower interest rates than subprime lenders and a more personalized approach. It’s always worth checking with a local credit union to see what options they have for a small auto loan.

4. The Co-Signer Option: Shared Responsibility

If you have a trusted friend or family member with good credit, asking them to co-sign your loan can significantly improve your chances of approval and potentially secure a lower interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

However, this is a serious commitment for the co-signer, as their credit will also be impacted if payments are missed. It’s crucial to have an open and honest discussion about the responsibilities and risks involved. Only pursue this option if you are absolutely confident in your ability to make every payment on time.

5. Peer-to-Peer Lending (P2P): An Emerging Alternative

Peer-to-peer lending platforms connect individual borrowers directly with individual investors. While not always the primary choice for auto loans, some platforms may offer personal loans that could be used for a small car purchase. Approval for bad credit can still be challenging, but it’s another avenue to explore if traditional and subprime options don’t pan out. Always compare interest rates and fees carefully.

The Application Process: Tips for Success

Once you’ve identified potential lenders, the application process itself requires careful attention. Approaching it strategically can make a significant difference in whether your $2500 car loan bad credit application is approved and on what terms.

1. Be Honest and Transparent

When filling out your application, provide accurate and truthful information. Lenders will verify details about your income, employment, and residence. Attempting to misrepresent your financial situation will almost certainly lead to a denial and could even be considered fraud. Transparency builds trust, which is especially valuable when dealing with bad credit.

2. Show Stability: Employment and Residence

Lenders are looking for signs of stability. A long history with the same employer, or at least consistent employment, demonstrates your ability to generate income. Similarly, a stable residence (living at the same address for an extended period) suggests reliability. If you’ve recently changed jobs or moved, be prepared to explain the circumstances in a positive light, if possible.

3. Explain Your Situation (If Applicable)

If there’s a specific reason for your bad credit – a medical emergency, job loss, or divorce – some lenders, especially credit unions or smaller institutions, might be willing to listen. Provide a brief, professional explanation of what happened, what steps you’ve taken to mitigate the issue, and how your current situation is stable. This shows accountability and can humanize your application beyond just a credit score.

4. Shop Around, But Wisely

It’s wise to compare offers from a few different lenders to ensure you’re getting the best possible terms. However, be cautious about submitting too many applications within a short period. Each "hard inquiry" on your credit report can temporarily lower your score.

Pro tip from us: Aim to submit all your loan applications within a 14-45 day window. Credit bureaus often count multiple inquiries for the same type of loan within this timeframe as a single inquiry, minimizing the impact on your score. Focus on getting pre-approved first, which often involves a "soft inquiry" that doesn’t affect your credit.

5. Understand the Terms: Interest Rates, APR, and Loan Term

Before signing anything, meticulously review the loan agreement.

- Interest Rate vs. APR: The interest rate is the cost of borrowing the principal. The Annual Percentage Rate (APR) includes the interest rate plus any additional fees, giving you the true annual cost of the loan. Always focus on the APR, as it provides the most accurate picture of what you’ll pay.

- Loan Term: This is the length of time you have to repay the loan. For a $2500 loan, terms are typically shorter (e.g., 12-36 months). A shorter term means higher monthly payments but less interest paid overall. A longer term means lower monthly payments but more interest paid over the life of the loan. Balance affordability with the total cost.

- Fees: Look out for origination fees, late payment fees, or prepayment penalties. Ensure you understand all potential charges.

Don’t be afraid to ask questions until you fully understand every aspect of the agreement.

Beyond the Loan: Building a Better Financial Future

Securing a $2500 car loan with bad credit isn’t just about getting a car; it’s a golden opportunity to start rebuilding your credit and establishing a healthier financial foundation. How you manage this loan will have a direct and lasting impact on your future borrowing capabilities.

1. Making Timely Payments: Your Most Powerful Tool

This cannot be stressed enough: make every single payment on time, every month. Payment history is the single most significant factor in your credit score (accounting for 35% of your FICO score). Consistent, on-time payments on your auto loan will demonstrate financial responsibility to credit bureaus and future lenders.

Even if it means cutting back on other expenses, prioritize your car loan payment. Setting up automatic payments from your bank account can be an excellent way to ensure you never miss a due date. This diligent repayment is the quickest path to improving your credit score after securing a bad credit loan.

2. Avoiding Refinancing Traps (and Knowing When It’s Smart)

Some lenders might offer to refinance your loan after a certain period. While refinancing can be beneficial if your credit score has significantly improved and you can secure a much lower interest rate, be wary of offers that don’t genuinely save you money or extend the loan term excessively.

Refinancing should aim to reduce your overall interest paid or lower your monthly payment without adding substantial cost in the long run. Always calculate the total cost of the new loan versus the remaining cost of your current loan before making a decision.

3. Strategies for Improving Your Credit Score Overall

Beyond your new car loan, take active steps to repair your credit. This small car loan can be the first positive entry on your credit report in a while, but other actions will amplify its effect:

- Pay Down Other Debts: Especially credit card balances. Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can quickly boost your score.

- Keep Old Accounts Open: Even if they have a zero balance, old accounts contribute to your credit history length, which positively impacts your score.

- Avoid New Debt: Limit taking on additional loans or credit cards while you’re focused on improving your score.

- Check Your Credit Report Regularly: Continue to monitor your reports for errors and to track your progress.

Dive deeper into credit repair with our article on .

4. The Power of a Small Loan: A Stepping Stone

View this $2500 car loan with bad credit not as a burden, but as an opportunity. Successfully managing this smaller loan demonstrates to future lenders that you are a responsible borrower. As your credit score improves, you’ll gain access to better financial products, lower interest rates on future loans, and more favorable terms. This initial small loan can be the catalyst for a complete financial turnaround, providing you with both reliable transportation and a fresh start for your credit profile.

Conclusion: Your Path to a $2500 Car Loan with Bad Credit is Clear

Securing a $2500 car loan with bad credit is not a myth; it’s a realistic goal that many people achieve every day. While your journey might require a bit more preparation and research than someone with pristine credit, the path is clear and achievable. By understanding your credit, preparing your finances, knowing where to look for lenders, and approaching the application process strategically, you significantly increase your chances of approval.

Remember, this loan is more than just a means to get a car; it’s an opportunity to rebuild your financial standing. Embrace the responsibility of making timely payments, and watch as your credit score begins to climb, opening doors to a more stable and prosperous financial future. You have the tools and the knowledge now – go forth and drive towards success!