How to Truly Beat Car Loans: Your Expert Guide to Smarter Auto Financing

How to Truly Beat Car Loans: Your Expert Guide to Smarter Auto Financing Carloan.Guidemechanic.com

Securing a car loan is a significant financial decision for most people. It can be a straightforward path to owning your dream vehicle, or it can become a burden that weighs on your budget for years. The good news? With the right knowledge and strategies, you don’t have to settle for just any car loan. You can absolutely beat car loans and secure terms that genuinely work in your favor.

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing. My mission here is to equip you with the insights and actionable steps needed to navigate the complexities of car loans, empowering you to make informed choices and save substantial money. This comprehensive guide will transform the way you approach car financing, ensuring you get the best possible deal every time.

How to Truly Beat Car Loans: Your Expert Guide to Smarter Auto Financing

Understanding the Foundation: What Makes a Car Loan Tick?

Before we can strategize to beat car loans, it’s crucial to understand their fundamental components. A car loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a set period. Grasping these core elements is the first step towards taking control.

The Principal: The Core of Your Loan

The principal is simply the actual amount of money you borrow to buy the car. If your car costs $30,000 and you put down a $5,000 down payment, your principal loan amount would be $25,000. This figure directly impacts your monthly payments and the total interest you’ll accrue over the loan’s life. A smaller principal means less to pay back.

The Interest Rate (APR): Your Cost of Borrowing

Perhaps the most critical factor in any loan is the interest rate, often expressed as an Annual Percentage Rate (APR). This is the percentage charged by the lender for the privilege of borrowing their money. A lower APR translates directly into lower monthly payments and significantly less money paid over the entire loan term. Understanding how to influence this rate is key to effectively beating car loans.

Based on my experience, many consumers mistakenly focus solely on the monthly payment. While crucial, the APR tells the true story of how expensive your loan will be. Always prioritize securing the lowest possible APR.

The Loan Term: How Long You’ll Be Paying

The loan term is the duration, usually expressed in months, over which you agree to repay the loan. Common terms range from 36 to 72 months, with some even extending to 84 months. A longer loan term generally results in lower monthly payments, which can seem attractive.

However, a longer term also means you’ll pay more in total interest over time. It can also mean that you might be "upside down" on your loan (owing more than the car is worth) for a longer period. Balancing affordability with total cost is a strategic move to beat car loans.

How Lenders Assess Your Risk

Lenders aren’t just handing out money; they’re assessing risk. Their primary concern is whether you will repay the loan. They look at several factors to determine your creditworthiness and, consequently, the interest rate they offer.

Your credit score, debt-to-income ratio (DTI), employment history, and even your residential stability all play a role. Understanding these assessment criteria allows you to proactively strengthen your position before applying for a loan.

Pre-Purchase Strategies to Beat the Loan Before You Even Shop

The most powerful strategies to beat car loans begin long before you step onto a dealership lot. These preparatory steps empower you with knowledge and leverage, putting you in the driver’s seat of your financial future.

Know Your Credit Score: Your Financial Report Card

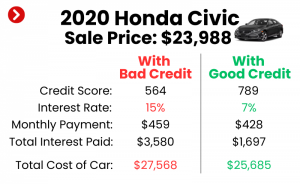

Your credit score is arguably the single most influential factor in determining the interest rate you’ll be offered. Lenders use it as a quick snapshot of your financial reliability. Scores generally range from 300 to 850, with higher scores indicating lower risk.

A good to excellent credit score (typically 700+) can unlock the lowest interest rates available, saving you thousands over the life of the loan. Conversely, a poor score can lead to significantly higher rates, making your car loan much more expensive.

Pro tips from us: Check your credit score and report well in advance of car shopping. You can get free copies from annualcreditreport.com. Review it for any errors and dispute them immediately. If your score isn’t where you want it, take steps to improve it, such as paying down existing debts or making all payments on time. You might want to read our article on for more detailed advice.

Budget Realistically: What Can You Truly Afford?

It’s tempting to focus solely on the car’s sticker price, but a smart budgeter considers the total cost of ownership. This includes not just the car loan payment, but also insurance, fuel, maintenance, and potential repairs. An informed budget helps you avoid overextending yourself.

Determine a comfortable monthly payment range that doesn’t strain your finances. Remember, your car payment shouldn’t consume more than 10-15% of your net monthly income. Sticking to a realistic budget is a fundamental way to beat car loans by ensuring they fit comfortably into your life.

Save for a Down Payment: The Power of Upfront Cash

Making a substantial down payment is one of the most effective ways to lower your monthly payments and reduce the total interest paid. A larger down payment reduces the principal amount you need to borrow, immediately decreasing your loan burden.

Furthermore, lenders view larger down payments as a sign of financial stability and commitment, which can sometimes lead to more favorable interest rates. Aim for at least 10-20% of the car’s purchase price, if possible. This upfront cash makes a huge difference in the long run.

Get Pre-Approved: Your Secret Weapon for Negotiation

This is perhaps the single most important pre-purchase strategy to beat car loans. Getting pre-approved for a loan before you visit a dealership provides you with a concrete offer from a lender. This offer includes a specific interest rate and loan amount, giving you a clear benchmark.

When you walk into a dealership with a pre-approval in hand, you’re no longer negotiating blindly. You know the best rate you can get elsewhere, which forces the dealership to either match or beat that offer if they want your business. It shifts the power dynamic entirely in your favor.

Navigating the Loan Application Process Like a Pro

With your groundwork laid, it’s time to engage with lenders. This stage is all about informed comparison and shrewd decision-making. Don’t rush into the first offer you receive; patience and thoroughness pay off.

Comparing Lenders: A World Beyond the Dealership

Many consumers make the mistake of only considering financing options presented by the car dealership. While dealership financing can sometimes be competitive, it’s rarely your only or best option. To truly beat car loans, you must cast a wider net.

Consider banks, credit unions, and online lenders. Credit unions, in particular, are known for offering very competitive rates because they are member-owned non-profits. Online lenders offer convenience and often quick approval processes. Always get multiple quotes.

Common mistakes to avoid are: Limiting your search to a single lender or assuming the dealership’s offer is the best you can get. Take the time to apply with 2-3 different institutions to compare their pre-approval offers. This comparison is your greatest asset.

Understanding Loan Offers: Beyond the Headline Number

When comparing loan offers, look beyond just the advertised interest rate. Scrutinize the APR, which includes not only the interest rate but also any lender fees. This gives you a more accurate picture of the total cost of borrowing.

Also, pay close attention to the loan term, any prepayment penalties (though these are rare on standard auto loans), and any additional fees. A seemingly low interest rate might be offset by hidden costs or unfavorable terms. Read every line of the loan agreement.

Negotiating Loan Terms: Every Point Counts

Remember that many aspects of a car loan can be negotiable, especially the interest rate and the loan term. Armed with your pre-approval offers, you have strong leverage. Don’t be afraid to ask for a better rate or a shorter term if it aligns with your budget.

If the dealership offers financing, present your pre-approval offer and challenge them to beat it. They often have access to multiple lenders and can sometimes find a slightly better deal to close the sale. Persistence here can save you hundreds, if not thousands, of dollars.

The Art of Negotiation: Getting the Best Deal

Negotiation is a skill, and when it comes to car loans, it’s a vital one. This is where your preparation truly shines, allowing you to secure terms that truly beat car loans.

Separate the Car Price from the Loan

One of the oldest tricks in the book is to bundle the car price negotiation with the loan negotiation. This makes it incredibly difficult to know if you’re getting a good deal on either. Always negotiate the car’s purchase price first. Agree on a final price for the vehicle before you even discuss financing.

Once you have a firm purchase price, then you can focus solely on the loan terms. This separation ensures clarity and prevents you from being manipulated into paying more for the car under the guise of a "great loan deal."

Leverage Your Pre-Approval

As mentioned, your pre-approval is your most potent negotiation tool. Don’t just mention you’re pre-approved; show them the offer. Let the finance manager know that you’re willing to walk away and finance through your pre-approved lender if they can’t match or beat it.

Based on my experience working with countless buyers, dealerships often have flexibility, especially if they know you have a strong alternative. They want to keep all aspects of the sale in-house, including financing, so use that to your advantage.

Be Patient and Willing to Walk Away

Never feel pressured to make a decision on the spot. If you’re not getting the terms you want, be prepared to walk away. There are always other dealerships and other lenders. This willingness to disengage is a powerful negotiating tactic.

The fear of losing a sale can often prompt a dealership to sweeten their offer. Your patience is a commodity that can translate directly into savings on your car loan.

Avoiding Unnecessary Add-Ons

Once you’ve agreed on a car price and loan terms, the finance department will often try to sell you additional products like extended warranties, GAP insurance, paint protection, or VIN etching. While some of these might have value, many are overpriced and can significantly inflate your loan amount.

Scrutinize each add-on. Ask yourself if you truly need it and if you could get it cheaper elsewhere. Politely decline anything that doesn’t offer clear, immediate value. Adding these to your loan means you’ll pay interest on them for the entire loan term, making them even more expensive.

Post-Purchase Strategies: Refinancing to Beat Existing Loans

The journey to beat car loans doesn’t necessarily end after you drive off the lot. If you’ve already financed a car, there’s still a powerful strategy you can employ: refinancing.

When is Refinancing a Good Idea?

Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can be an excellent strategy if:

- Interest Rates Have Dropped: If market interest rates have decreased since you took out your original loan, you might qualify for a lower rate now.

- Your Credit Score Has Improved: If you’ve worked to improve your credit score since your initial purchase, you’re now seen as a lower risk and can qualify for better rates.

- You Want a Shorter Term: You might refinance to a shorter term to pay off the loan faster and reduce total interest, accepting higher monthly payments.

- You Want Lower Monthly Payments: While not always recommended due to increased total interest, extending your loan term through refinancing can lower monthly payments if your financial situation has changed.

Pro tips from us: Check your current loan terms and compare them to new offers regularly. Even a percentage point or two difference in APR can save you hundreds, or even thousands, over the life of the loan. This is especially true if you initially got a high-interest loan.

The Refinancing Process

The refinancing process is similar to applying for an original car loan. You’ll gather your financial documents, get quotes from various lenders (banks, credit unions, online lenders), and compare their offers. Once approved, the new lender pays off your old loan, and you begin making payments to the new institution.

Ensure you understand any fees associated with the new loan, such as application fees or title transfer fees, to ensure the savings from a lower interest rate aren’t negated by these costs. A trusted external resource like the can offer further guidance on refinancing and understanding your rights.

Common Pitfalls and How to Avoid Them

Even with the best intentions, it’s easy to fall into common traps that undermine your efforts to beat car loans. Being aware of these pitfalls is crucial for navigating the process successfully.

Ignoring the APR

As discussed, focusing solely on the monthly payment without considering the APR is a major mistake. A low monthly payment achieved through a very long loan term and a high APR means you’ll pay significantly more in the long run. Always prioritize the lowest possible APR.

Focusing Only on Monthly Payments

Salespeople are expertly trained to discuss monthly payments because it makes expensive cars seem affordable. Don’t let them anchor you to this single number. Always consider the total cost of the loan over its entire term.

Falling for Extended Loan Terms

While an 84-month loan might offer incredibly low monthly payments, it’s often a trap. You’ll pay significantly more in interest, and you’ll likely be "upside down" on your loan (owing more than the car is worth) for much longer. This can create serious problems if you need to sell or trade in the car before the loan is paid off.

Not Reading the Fine Print

Loan documents can be lengthy and filled with legal jargon, but it’s imperative to read and understand every single clause. Look for prepayment penalties, late payment fees, and any other conditions that could impact you. If you don’t understand something, ask for clarification.

Impulse Buying

Making an emotional, spur-of-the-moment decision on a car purchase often leads to poor financial choices. Take your time, do your research, and stick to your budget and pre-approved loan terms. A little patience can save you a lot of money.

Future-Proofing Your Car Loan Strategy

Successfully beating car loans isn’t a one-time event; it’s a continuous commitment to smart financial practices. By adopting these long-term strategies, you can maintain control over your auto financing and ensure ongoing financial health.

Build and Maintain Good Credit

Your credit score is dynamic. Continuously making payments on time, keeping credit utilization low, and responsibly managing your credit accounts will ensure your score remains strong. This positions you for the best rates not just on car loans, but on all future borrowing. A good credit score is your most powerful tool in any financial negotiation.

Regularly Review Your Loan

Don’t just set and forget your car loan. Periodically review your interest rate, especially if market rates have shifted or your credit score has improved. As mentioned, refinancing could be an option that saves you money. Staying informed means you’re always ready to seize a better opportunity.

Making Extra Payments

If your budget allows, making extra payments towards your principal can dramatically reduce the total interest paid and shorten your loan term. Even small additional payments can add up significantly over time. Ensure your lender applies extra payments directly to the principal to maximize their impact.

Based on my experience, even paying an extra $50-$100 per month can cut months off your loan and save you hundreds of dollars in interest. It’s a simple, yet incredibly effective, strategy.

Conclusion: Empowering Your Journey to Smarter Car Financing

The journey to beat car loans might seem daunting, but it’s entirely achievable with the right approach. From meticulously preparing your finances and understanding your credit score to strategically comparing lenders and negotiating like a pro, every step contributes to a more favorable outcome. Remember, the power is truly in your hands when you are informed and prepared.

By adopting these expert strategies, you’re not just getting a car loan; you’re securing a financial product that aligns with your goals and respects your budget. Take control, leverage your knowledge, and confidently navigate the world of auto financing. Start your journey to smarter car financing today, and drive away with the best possible deal.