How to Unlock a Low APR on Your Car Loan: An Expert Guide to Saving Thousands

How to Unlock a Low APR on Your Car Loan: An Expert Guide to Saving Thousands Carloan.Guidemechanic.com

Securing a car loan is a significant financial decision, and one of the most critical elements dictating its overall cost is the Annual Percentage Rate (APR). A seemingly small difference in APR can translate into hundreds, or even thousands, of dollars saved or spent over the life of your loan. Understanding how to get a good APR on a car loan isn’t just about saving money; it’s about making an informed choice that supports your financial well-being.

As an expert blogger and professional SEO content writer, I’ve seen firsthand how a little preparation can lead to substantial savings. This comprehensive guide will equip you with the knowledge and strategies needed to navigate the car loan landscape confidently, ensuring you secure the most favorable terms possible. We’ll delve deep into every factor, offering actionable advice and pro tips based on years of experience in personal finance.

How to Unlock a Low APR on Your Car Loan: An Expert Guide to Saving Thousands

Understanding APR: Your Key to Financial Savings

Before we dive into strategies, let’s clarify what APR truly means and why it’s so pivotal. Many people confuse the interest rate with the APR, but they are distinct, though related, concepts.

What is APR (Annual Percentage Rate)?

The Annual Percentage Rate (APR) represents the total annual cost of borrowing money, expressed as a percentage. It includes not just the interest rate, but also any additional fees associated with the loan, such as administrative charges, loan origination fees, or closing costs. While the interest rate is the percentage charged by the lender for borrowing the principal amount, the APR provides a more complete picture of the true cost of your loan over a year.

For example, a loan might advertise a 5% interest rate, but with various fees factored in, the APR could be 5.5% or even higher. This distinction is crucial because the APR is what you’ll ultimately pay.

Why a Low APR Matters: Long-Term Savings Illustrated

The impact of APR on your car loan’s total cost cannot be overstated. A lower APR directly translates to less money paid in interest over the life of the loan. Even a difference of one or two percentage points can save you a substantial sum, especially on a multi-year loan for a significant amount.

Consider a $30,000 car loan over 60 months. At a 7% APR, your total interest paid would be approximately $5,600. However, if you manage to secure a 5% APR, that total interest drops to around $3,900. That’s a saving of $1,700 just from a 2% reduction in APR! Pro tips from us: Always focus on the total cost of the loan, not just the monthly payment. Lenders can manipulate loan terms to make monthly payments seem attractive while hiding a high APR.

The Core Factors Influencing Your Car Loan APR

Lenders assess several key factors when determining the APR they’ll offer you. Understanding these elements is the first step toward improving your chances of securing a good rate.

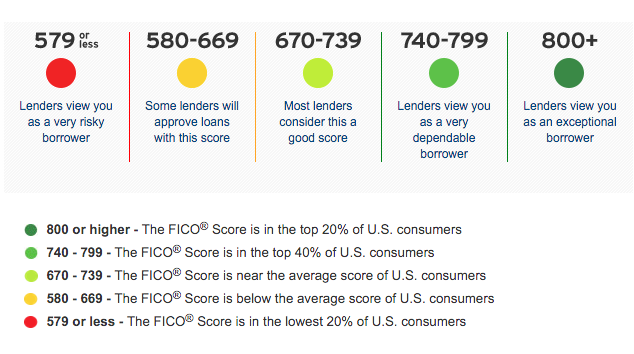

Your Credit Score: The Ultimate Deciding Factor

Without a doubt, your credit score is the single most influential factor in determining your car loan APR. It’s a numerical representation of your creditworthiness, indicating to lenders how likely you are to repay your debts on time. Higher scores signal lower risk, leading to lower APRs.

Lenders typically categorize borrowers into tiers based on their credit scores. Individuals with excellent credit (typically 780+) receive the most favorable rates, while those with good credit (670-739) will still get competitive offers. If your score falls into the fair (580-669) or poor (below 580) range, you can expect significantly higher APRs, as lenders perceive a greater risk of default. Based on my experience, lenders often use a tiered system, and even a few points can bump you into a better tier, saving you money.

Your Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is another critical metric lenders evaluate. It compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover new debt obligations, making you a less risky borrower.

To calculate your DTI, sum up all your monthly debt payments (car loans, student loans, mortgage/rent, credit card minimums) and divide that by your gross monthly income (before taxes). Lenders generally prefer a DTI of 36% or less, though some auto lenders may go up to 43-50% for well-qualified applicants. A high DTI can make lenders nervous, potentially leading to a higher APR or even a loan denial.

Loan Term Length

The length of your car loan, often referred to as the "term," significantly impacts your APR. Shorter loan terms (e.g., 36 or 48 months) typically come with lower APRs because lenders assume less risk over a shorter period. Conversely, longer loan terms (e.g., 72 or 84 months) usually carry higher APRs.

While a longer term means lower monthly payments, it also means you’ll pay more in interest over the life of the loan. Common mistakes to avoid are automatically opting for the longest term just to achieve the lowest possible monthly payment without considering the total cost. A longer term means the lender is exposed to the risk of you defaulting for a longer period, hence the higher rate.

Your Down Payment Amount

Making a substantial down payment on your car purchase is a powerful way to reduce your APR. A larger down payment lowers the amount you need to borrow, which reduces the lender’s risk. When you have more equity in the vehicle from day one, you’re less likely to default, and if you do, the lender is better protected.

Financial experts often recommend a down payment of at least 20% for new cars and 10% for used cars. This not only helps secure a lower APR but also reduces the likelihood of being "upside down" on your loan (owing more than the car is worth) early in the loan term.

Vehicle Age and Type (Collateral)

The car itself acts as collateral for the loan, and its characteristics influence your APR. Newer cars, being less prone to immediate depreciation and typically more reliable, are generally seen as less risky collateral than older, higher-mileage vehicles. As a result, new car loans often have slightly lower APRs than used car loans for similar borrowers.

Additionally, the type of vehicle can play a role. A niche, high-performance, or heavily modified vehicle might be harder for a lender to repossess and sell if you default, potentially leading to a higher APR. Lenders prefer vehicles that hold their value well and are easy to resell.

Current Interest Rate Environment

Beyond your personal financial profile, the broader economic landscape also influences car loan APRs. When the Federal Reserve raises interest rates, it generally becomes more expensive for all lenders to borrow money, and these increased costs are often passed on to consumers in the form of higher loan APRs.

Conversely, in periods of lower interest rates, you might find more attractive loan offers. While you can’t control the economic climate, being aware of it can help you understand why rates might be higher or lower than expected.

Strategic Steps to Secure the Best Possible APR

Now that you understand the factors at play, let’s explore the actionable steps you can take to significantly improve your chances of getting a good APR on a car loan.

Step 1: Know Your Credit Score (and Improve It!)

This is the cornerstone of securing a low APR. Before you even set foot in a dealership or apply for a loan, pull your credit reports and scores. You are entitled to a free credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) once every 12 months through AnnualCreditReport.com. (External link: For your free annual credit reports, visit www.AnnualCreditReport.com).

- Review for Accuracy: Scrutinize your reports for any errors, inaccuracies, or fraudulent activity. Dispute any discrepancies immediately, as these can negatively impact your score.

- Boost Your Score: If your score isn’t where you want it to be, take steps to improve it. Pay all your bills on time, reduce your credit card balances to below 30% of your credit limit, and avoid opening new lines of credit just before applying for a car loan. For an in-depth guide on boosting your credit score, read our article: (Hypothetical internal link).

Step 2: Get Pre-Approved from Multiple Lenders

One of the most powerful strategies to secure a good APR is to get pre-approved for a loan from several different lenders before you visit a dealership. This could include banks, credit unions, and online lenders.

- Why Pre-Approval is Powerful: Pre-approval gives you a firm loan offer, including an APR, that is valid for a certain period. It provides a baseline for comparison and gives you significant leverage at the dealership. You walk in as a cash buyer, knowing exactly what financing you qualify for.

- Shop Around: Don’t just accept the first offer. Apply to at least 3-5 lenders. Each inquiry will cause a slight dip in your credit score, but credit scoring models typically group multiple inquiries for the same type of loan within a short window (usually 14-45 days) as a single inquiry, minimizing the impact. Based on my experience, this competitive shopping is where most people miss out on significant savings. Having an offer in hand makes the dealership’s finance department work harder to beat it.

Step 3: Make a Substantial Down Payment

As discussed, a larger down payment directly correlates with a lower APR. Aim for at least 20% on new cars and 10% on used cars if your budget allows.

- Benefits Beyond APR: Beyond securing a better rate, a significant down payment reduces the total amount of interest you’ll pay, shortens the time it takes to build equity in your vehicle, and protects you from going upside down on your loan. It’s a wise financial move that signals responsibility to lenders.

Step 4: Choose a Shorter Loan Term (If Feasible)

While longer terms offer lower monthly payments, they nearly always result in a higher APR and more interest paid over time. If your budget allows, opt for the shortest loan term you can comfortably afford.

- Balance Monthly Payments with Total Cost: Pro tip: Use an online car loan calculator to compare different loan terms and their associated total costs (principal + interest) at various APRs. This will visually demonstrate the long-term savings of a shorter term. It’s about finding the sweet spot where your monthly payment is manageable without paying excessive interest.

Step 5: Negotiate the Car Price First, Then the Loan

This is a common mistake: people negotiate the car price and the loan terms simultaneously. This can lead to confusion and allow dealerships to make up for a low car price with a high APR, or vice-versa.

- Separate Negotiations: Always negotiate the vehicle’s purchase price as if you were paying cash. Once you’ve agreed on a final price, then discuss financing. This clear separation ensures you get the best deal on both the car and the loan. Your pre-approved loan offer will be invaluable here.

Step 6: Consider a Co-Signer (If Necessary and Carefully)

If your credit score is less than ideal, or your DTI ratio is high, adding a co-signer with excellent credit can help you secure a lower APR. A co-signer essentially guarantees the loan, taking on equal responsibility for repayment.

- When It Makes Sense: This strategy is best for individuals with limited credit history (e.g., young adults) or those actively rebuilding their credit.

- Risks for the Co-Signer: Understand that the co-signer is equally liable for the debt. If you miss payments, their credit score will also be negatively impacted, and they will be legally obligated to pay. It should only be considered with someone you trust implicitly and who understands the full implications.

Step 7: Revisit Your Loan Later (Refinancing)

Even if you don’t get the absolute best APR initially, your situation might improve over time. If your credit score improves significantly, interest rates drop, or your financial health stabilizes, you might be a candidate for refinancing your car loan.

- When Refinancing is a Good Option: Refinancing involves taking out a new loan to pay off your existing one, often at a lower interest rate or with different terms. It’s a smart move if you’ve made consistent payments, your credit score has risen, or market rates have fallen since you first financed your vehicle. Considering refinancing your existing loan? Our detailed guide on (Hypothetical internal link) can help you navigate the process.

Common Mistakes to Avoid When Seeking a Car Loan

Even with the best intentions, certain pitfalls can lead to a less favorable APR. Awareness is your best defense.

- Not Checking Your Credit Score Beforehand: Going into the process blind leaves you vulnerable. You won’t know if the rate offered is fair or if there are errors on your report.

- Accepting the First Offer from the Dealership: Dealerships often start with higher APRs. Without comparison offers, you have no leverage to negotiate.

- Focusing Only on Monthly Payments: This is a classic trick. Lenders can stretch out loan terms to lower monthly payments, but this significantly increases the total interest you pay and often comes with a higher APR.

- Extending the Loan Term Unnecessarily: While a longer term means lower monthly payments, it almost always means a higher overall cost due to increased interest and typically a higher APR. Avoid 72 or 84-month terms unless absolutely necessary.

- Falling for Add-Ons That Inflate the Loan: Dealerships may try to sell you extended warranties, GAP insurance, or other extras. While some may be valuable, buying them through your loan will increase your principal and, consequently, the total interest you pay. Consider purchasing these separately or declining them if they don’t offer real value.

Conclusion: Empowering Your Car Loan Journey

Securing a good APR on a car loan is not a matter of luck; it’s the result of thorough preparation, strategic planning, and informed decision-making. By understanding the factors that influence your rate, actively working to improve your financial standing, and diligently shopping around for the best offers, you put yourself in the driver’s seat.

Remember, every percentage point you shave off your APR translates directly into savings that stay in your pocket. You have the power to save thousands of dollars over the life of your loan simply by being proactive. Start your journey today by checking your credit, getting pre-approved, and empowering yourself with knowledge. This is how to get a good APR on a car loan and ensure your next vehicle purchase is a financially sound one.