How Trading In A Car With A Loan Works: Your Ultimate Guide to a Seamless Swap

How Trading In A Car With A Loan Works: Your Ultimate Guide to a Seamless Swap Carloan.Guidemechanic.com

Thinking about upgrading your ride but still have an outstanding loan on your current vehicle? You’re not alone. This is a remarkably common scenario, and for many, the idea of trading in a car with an existing loan feels like navigating a complex financial maze. Will the dealership take it? What happens to the old loan? Will it affect your credit?

As an expert blogger and professional SEO content writer who has witnessed countless car transactions, I can tell you that trading in a car with a loan is not only possible but also a routine part of the automotive sales process. The key, however, lies in understanding how it works, preparing yourself with the right information, and knowing what to expect. This comprehensive guide will demystify the entire process, providing you with the knowledge and confidence to make a smart financial decision.

How Trading In A Car With A Loan Works: Your Ultimate Guide to a Seamless Swap

Our ultimate goal here is to empower you, the reader, with real value and actionable insights. By the time you finish this article, you’ll be an expert on the subject, ready to approach your next car trade-in with clarity and control. Let’s dive in!

Demystifying the Core Concept: Trading In a Car with an Existing Loan

At its heart, trading in a car with a loan means that the dealership will facilitate the payoff of your existing loan when you purchase a new vehicle from them. They essentially act as an intermediary, handling the financial transfer to your current lender. This convenience is a major draw for many car owners.

The process isn’t just about handing over your keys; it’s a financial transaction involving multiple parties: you, your current lender, the dealership, and potentially a new lender. The outcome largely depends on the financial relationship between your car’s market value and your outstanding loan balance. Understanding this relationship is your first and most critical step.

Many people assume they must pay off their old loan before they can trade in their car. Based on my experience, this is a common misconception. While you can pay it off, it’s rarely necessary, and the dealership is fully equipped to manage this as part of the deal.

The Absolute First Step: Knowing Your Financial Standing

Before you even set foot on a dealership lot, the most crucial homework you can do involves assessing your current car’s worth and your outstanding loan balance. This information is your superpower in negotiations.

Calculate Your Current Car’s Value (Trade-In Value vs. Retail Value)

Your car’s value is not a fixed number; it varies based on several factors and who is buying it. When considering a trade-in, you’re primarily interested in its "trade-in value," which is typically lower than its "retail value" (what a private buyer might pay or what the dealership would sell it for after reconditioning).

- Online Valuation Tools: Start by using reputable online resources like Kelley Blue Book (KBB), Edmunds, and NADAguides. These platforms allow you to input your car’s specific details (make, model, year, mileage, condition, features) to get an estimated trade-in value.

- Condition Matters: Be honest about your car’s condition. A "fair" condition car will fetch less than one in "excellent" condition. Minor dents, scratches, tire wear, and interior blemishes all impact the value.

- Get Multiple Quotes: Pro tips from us: Don’t rely on just one source. Get estimates from at least two or three different online tools. You can even visit a few dealerships or online car buying services (like Carvana or Vroom) to get a preliminary appraisal or cash offer without committing to a purchase. This gives you a solid range to work with.

Understanding this value helps you set realistic expectations for your trade-in. It’s the starting point for all subsequent financial calculations.

Determine Your Loan Payoff Amount

This is perhaps the most critical piece of information you need. Your loan payoff amount is not simply your current balance shown on your monthly statement. It’s the exact amount your lender requires to close out your loan completely, including any accrued interest or fees up to a specific date.

- Contact Your Lender Directly: The most accurate way to get this number is to call your loan provider (bank, credit union, or financing company). Ask for your "10-day payoff amount." This figure is typically valid for a short period, giving you a window to complete the trade-in.

- Why it’s Different: The current balance on your statement might not account for interest that has accrued since your last payment or any per-diem interest. The payoff amount provides a definitive figure.

- Get it in Writing: Always ask your lender to send you the payoff quote in writing (email or fax) for your records. This documentation can be helpful during the dealership process.

Knowing your precise payoff amount prevents any last-minute surprises or miscalculations. It’s non-negotiable data that empowers your position.

Unveiling Your Equity: Positive, Negative, or Breaking Even

Once you have both your car’s estimated trade-in value and your loan payoff amount, you can determine your "equity." Equity is the difference between what your car is worth and what you owe on it. This calculation is the linchpin of your trade-in strategy.

- Positive Equity: Your car’s trade-in value is greater than your loan payoff amount. This is the ideal scenario. You have money left over after the loan is paid off.

- Negative Equity (Being "Upside Down"): Your car’s trade-in value is less than your loan payoff amount. This means you owe more on the car than it’s worth. This situation requires careful consideration.

- Breaking Even: Your car’s trade-in value is roughly equal to your loan payoff amount. There’s little to no money left over, nor is there a deficit.

Understanding your equity position dictates how the trade-in will impact your next vehicle purchase. It’s crucial for making informed decisions.

Navigating the Waters with Positive Equity

If you find yourself with positive equity, congratulations! This means your car has depreciated less than anticipated, or you’ve made significant extra payments. This equity can be a powerful asset.

When you have positive equity, the dealership will pay off your existing loan, and the remaining amount (your equity) can be used in one of two ways:

- As a Down Payment: Most commonly, the positive equity is applied directly as a down payment toward your new vehicle purchase. This reduces the amount you need to finance for the new car, leading to lower monthly payments or a shorter loan term.

- Cash Back: In some rare cases, if your equity is substantial and you don’t need it all for a down payment, you might be able to receive some of it as cash back. However, dealerships typically prefer to apply it to the new purchase.

Based on my experience, positive equity puts you in a strong negotiating position. It shows you’re a responsible borrower and can make you a more attractive customer for a new loan. You’re bringing value to the table beyond just the purchase of a new car.

Tackling Negative Equity (Being "Upside Down")

Negative equity, often referred to as being "upside down" or "underwater" on your loan, occurs when you owe more on your car than its current market value. This is a common situation, especially if you bought a new car recently, financed it for a long term, or put little to no money down. While it presents a challenge, it’s certainly not a deal-breaker for trading in your car.

Here are the primary options when dealing with negative equity:

Option 1: Rolling it into the New Loan

This is the most common approach dealerships offer. They will pay off your old loan, and the negative equity amount will be added to the financing of your new vehicle.

- Pros: It’s convenient, allowing you to get into a new car without paying out-of-pocket immediately.

- Cons: You will be financing more than the new car is actually worth. This increases your new loan amount, which means higher monthly payments and potentially a longer loan term. You’ll start your new car ownership with negative equity, making it harder to get out of the cycle in the future.

- Warning: Carefully consider the impact on your new loan. An already long loan term (e.g., 72 or 84 months) combined with rolled-over negative equity can lead to a never-ending cycle of being upside down.

Option 2: Paying the Difference Out-of-Pocket

If you have the financial means, you can pay the negative equity amount directly to the dealership or your old lender. This clears your old loan completely, allowing you to start fresh with your new car purchase without any carryover debt.

- Pros: This is the most financially sound option. You avoid rolling negative equity into a new loan, ensuring your new loan is only for the value of the new car. It helps you build equity faster in your new vehicle.

- Cons: Requires an immediate cash outlay, which might not be feasible for everyone.

Option 3: Selling the Car Privately

If your negative equity is substantial, selling your car privately might fetch a higher price than a dealership trade-in. This could reduce the amount of negative equity you need to cover.

- Benefits: Private sales often yield a higher selling price, potentially minimizing your negative equity burden.

- Challenges: Selling privately requires time, effort, and dealing with potential buyers. More importantly, you still have an outstanding loan. You’ll need to coordinate with your lender to ensure a smooth title transfer once the buyer pays you. You’ll likely need to pay the difference between the sale price and your payoff amount out of pocket to your lender to clear the lien before you can give the buyer a clean title.

- Common mistakes to avoid are: Not having a clear plan for paying off the loan balance after the private sale, or not understanding the title transfer process with a lienholder.

Option 4: Refinancing or Waiting it Out

If you’re upside down and not in a rush, consider these strategic alternatives:

- Refinance Your Current Loan: If interest rates have dropped or your credit score has improved, you might be able to refinance your current loan for a lower interest rate, which can help you pay it down faster and build equity.

- Wait and Pay Down Your Loan: Sometimes, the best strategy is to simply keep your current car, continue making payments (or even extra payments), and wait until you build positive equity. This might mean driving your current vehicle for another year or two, but it can save you significant money in the long run.

Deciding how to handle negative equity requires a careful evaluation of your finances and priorities. Don’t let a dealership pressure you into a deal that rolls over too much negative equity, especially if it stretches your budget.

The Dealership Process: What to Expect

Once you’ve done your homework and understand your equity position, you’re ready to engage with the dealership. Knowing the steps involved will help you remain confident and in control.

The Appraisal

When you bring your car to the dealership for a trade-in, they will conduct an appraisal. This is their assessment of your vehicle’s condition, mileage, features, and overall market desirability.

- What they look for: Appraisers examine the exterior for dents, scratches, and rust; the interior for wear and tear, stains, and odors; the tires for tread depth; and they’ll likely test drive the car to check mechanical components. They also consider service records and vehicle history reports (like CarFax).

- How to prepare your car: A clean car makes a better first impression. Wash it, vacuum the interior, remove personal belongings, and gather any service records you have. While you don’t need to fix major mechanical issues, addressing minor cosmetic flaws (if inexpensive) can sometimes help.

- Understanding their offer: The dealership’s trade-in offer is based on their internal valuation, potential reconditioning costs, and how quickly they believe they can resell your vehicle. It might be different from your online estimates, but your research provides a strong benchmark.

Negotiation Strategies for Your Trade-In

Negotiating a car deal involves two primary transactions: the purchase price of the new car and the trade-in value of your old car. Pro tips from us: Always try to negotiate these two aspects separately.

- Separate the Deals: Focus on getting the best possible price for the new car first. Once that’s settled, then discuss the trade-in value. If you combine them, it’s easier for the dealership to shuffle numbers around, giving you a good deal on one while shortchanging you on the other.

- Have Your Research Ready: Your online valuation estimates and your precise loan payoff amount are your strongest negotiating tools. If the dealership’s offer is significantly lower than your research, be prepared to present your findings and justify your car’s value.

- Be Prepared to Walk Away: This is the ultimate negotiation tactic. If the numbers don’t work for you, be ready to leave. There are other dealerships and other cars.

The Paperwork Trail: Closing the Deal

Once you’ve agreed on the price of the new car and the trade-in value, the finance department will handle the paperwork. This is where the old loan is officially taken care of.

- Old Loan Payoff: The dealership will typically generate a check or an electronic transfer for your loan payoff amount directly to your current lender. This ensures your old loan is fully settled. You will sign documents authorizing the dealership to do this on your behalf.

- New Loan Application: If you’re financing the new vehicle, you’ll complete a new loan application. This is where any positive equity will be applied as a down payment, or negative equity will be rolled into the new loan.

- Title Transfer: You’ll sign over the title of your trade-in to the dealership. Since your current lender holds the title until the loan is paid off, the dealership will handle the lien release process directly with your lender. You won’t receive the physical title until your loan is paid off.

Make sure you receive copies of all signed documents, especially those related to your old loan payoff. Keep them for your records until you confirm with your old lender that the loan has been closed.

Pro Tips for a Smooth and Successful Trade-In

Based on my experience helping countless individuals through this process, here are some actionable tips to ensure your trade-in experience is as smooth and financially beneficial as possible:

- Do Your Homework Before Visiting the Dealership: This cannot be stressed enough. Knowing your car’s value and loan payoff amount gives you immense power.

- Be Honest About Your Car’s Condition: While you want the best price, misleading an appraiser will only lead to disappointment and wasted time. Be realistic.

- Understand All Figures Before Signing: Don’t just look at the monthly payment. Scrutinize the total price of the new car, the trade-in allowance, any fees, and the interest rate on the new loan.

- Consider Getting Pre-Approved for a New Loan: Obtaining a pre-approval from your bank or credit union gives you a benchmark interest rate. The dealership’s finance department can then try to beat or match it, or you can use your pre-approval.

- Don’t Be Afraid to Walk Away: If the deal isn’t right, or you feel pressured, simply leave. A good deal often requires patience.

- Clean Your Car! A clean, well-maintained car gives the impression it’s been cared for, potentially leading to a better appraisal. Remove all personal items.

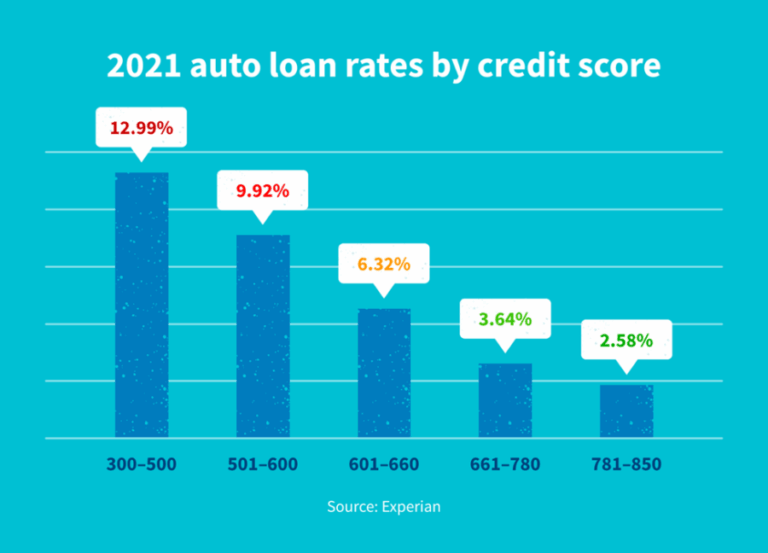

- Check Your Credit Score: Your credit score will significantly impact the interest rate on your new car loan, which in turn affects your monthly payments and overall cost. Knowing your score helps you understand your financing options.

Common Mistakes to Avoid When Trading In a Car with a Loan

Even with the best intentions, people often make mistakes that can cost them money or create unnecessary stress. Here are some common pitfalls to steer clear of:

- Not Knowing Your Payoff: As mentioned, this is foundational. Without it, you’re negotiating blind.

- Ignoring Negative Equity: Pretending negative equity doesn’t exist won’t make it go away. It will simply be rolled into your new loan, costing you more in the long run. Address it head-on.

- Focusing Only on Monthly Payments: Dealerships love to talk about low monthly payments. While important, a low payment might hide a higher overall price, a longer loan term, or a low trade-in value. Always look at the "out-the-door" price and the total cost of the loan.

- Not Shopping Around: This applies to both the new car and your trade-in. Different dealerships might offer varying trade-in values. Get multiple quotes.

- Getting Emotionally Attached: While you might love your old car, it’s now a financial asset. Approach the trade-in purely from a business perspective.

- Forgetting About Your Old Tags/Registration: In some states, you might need to transfer your license plates to your new vehicle or return them to the DMV. Clarify this with the dealership or your local DMV.

Frequently Asked Questions (FAQs)

Let’s address some of the most common questions people have about trading in a car with a loan.

Can I trade in a car with a lien?

Yes, absolutely! That’s precisely what this entire article is about. A lien simply means your lender holds the title until the loan is paid off. The dealership will handle the payoff and the lien release as part of the transaction.

What if my lender isn’t present at the dealership?

Your lender doesn’t need to be physically present. The dealership will contact your lender directly to get the payoff amount and then send the funds to them. This is a standard procedure.

Does my credit score affect the trade-in?

Your credit score doesn’t directly affect the value of your trade-in. However, it significantly impacts the interest rate you’ll qualify for on your new car loan. A lower credit score can lead to higher interest rates, making your new car more expensive and potentially making it harder to absorb any negative equity.

How long does the payoff take for my old loan?

Typically, the dealership will send the payoff amount to your lender within a few business days of you signing the new car purchase agreement. It might take your lender another 7-14 days to process the payment, close your account, and send you confirmation. It’s a good idea to follow up with your old lender a couple of weeks after the trade-in to ensure the loan has been fully closed.

Should I pay off my old loan before trading it in?

While you can pay off your old loan, it’s usually not necessary. The dealership is set up to handle the payoff for you. Paying it off yourself might be beneficial if you have significant negative equity and want to clear that debt before starting a new loan. Otherwise, let the dealership manage it for convenience.

For further reading on smart car financing decisions, consider exploring resources like the Consumer Financial Protection Bureau’s guide on car loans. This external source offers valuable insights into understanding financing terms and protecting your interests.

Conclusion: Drive Away with Confidence

Trading in a car with an outstanding loan doesn’t have to be a source of stress or confusion. By understanding the core mechanics – knowing your car’s value, your loan payoff amount, and your equity position – you equip yourself with the knowledge needed to navigate the process effectively. Whether you have positive equity, negative equity, or are breaking even, there’s a clear path forward.

Remember to do your homework, negotiate wisely, and read all paperwork carefully. With these strategies in hand, you’ll be able to make an informed decision, secure a fair deal, and drive away in your new vehicle with confidence, knowing you’ve managed your finances like a true pro. Happy driving!