How Will A Car Loan Affect My Credit? A Comprehensive Guide to Auto Financing & Your Financial Future

How Will A Car Loan Affect My Credit? A Comprehensive Guide to Auto Financing & Your Financial Future Carloan.Guidemechanic.com

Securing a car loan is a significant financial decision, one that extends far beyond simply getting keys to a new vehicle. For many, it represents a substantial commitment that will directly interact with one of their most vital financial assets: their credit score. Understanding how a car loan will affect your credit is not just smart, it’s essential for navigating your financial journey wisely.

This article delves deep into the multifaceted relationship between auto financing and your credit health. We’ll explore the initial impacts of applying, the long-term benefits of responsible repayment, and the potential pitfalls that could derail your financial progress. Our goal is to equip you with the knowledge to make informed decisions and leverage a car loan as a powerful tool for building a strong credit profile.

How Will A Car Loan Affect My Credit? A Comprehensive Guide to Auto Financing & Your Financial Future

Understanding Your Credit Score: The Foundation of Financial Health

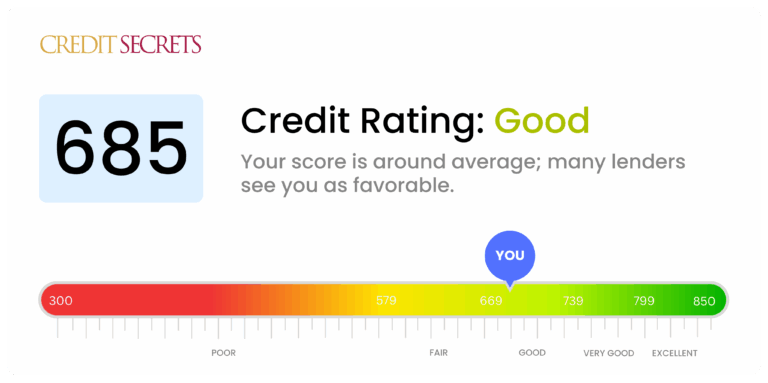

Before we dissect the specific impact of a car loan, it’s crucial to grasp the fundamentals of your credit score. This three-digit number, often ranging from 300 to 850, is a snapshot of your creditworthiness. Lenders use it to assess the risk of lending you money. A higher score typically unlocks better interest rates and more favorable loan terms.

Based on my experience, understanding these fundamentals is the first step toward strategically managing your finances. Your credit score is not static; it’s a dynamic reflection of your borrowing and repayment habits over time. It’s influenced by several key factors, each playing a role in how a car loan will interact with your overall credit profile.

These five primary components, according to widely used scoring models like FICO, dictate your credit score:

- Payment History (35%): This is the most critical factor. Consistent, on-time payments boost your score, while late or missed payments can cause significant damage.

- Amounts Owed (30%): This includes your total debt and, importantly, your credit utilization ratio for revolving accounts (how much credit you’re using versus how much is available). Lower utilization is generally better.

- Length of Credit History (15%): The longer your accounts have been open and in good standing, the better. This demonstrates a track record of responsible borrowing.

- New Credit (10%): Opening multiple new accounts in a short period can signal risk to lenders and may temporarily lower your score.

- Credit Mix (10%): Having a healthy variety of credit accounts, such as both installment loans (like a car loan or mortgage) and revolving credit (like credit cards), shows you can manage different types of debt responsibly.

The Initial Impact: Applying for a Car Loan

The journey of obtaining a car loan begins with the application process, and this initial step can have an immediate, albeit usually temporary, effect on your credit score. It’s important to understand these short-term impacts to avoid unnecessary anxiety or missteps.

When you apply for a car loan, lenders will typically perform what’s known as a "hard inquiry" or "hard pull" on your credit report. This allows them to view your detailed credit history and assess your risk profile. Each hard inquiry is recorded on your credit report and can cause a small, temporary dip in your credit score, usually by a few points.

This slight reduction is generally short-lived, with your score often recovering within a few months, provided you continue to manage your credit responsibly. However, multiple hard inquiries for different types of credit (e.g., a car loan, a credit card, and a personal loan) in a short period can be viewed negatively, suggesting a higher risk or a desperate need for credit.

Rate Shopping and Credit Score Impact: A Smart Approach

A crucial exception to the "multiple inquiries are bad" rule applies specifically to rate shopping for auto loans. Credit scoring models recognize that consumers often shop around for the best interest rates when buying a car. To accommodate this, most models treat multiple hard inquiries for the same type of loan (like an auto loan) within a specific timeframe as a single inquiry. This "rate shopping window" typically ranges from 14 to 45 days, depending on the scoring model.

Pro tips from us: To minimize the impact on your credit, aim to complete your car loan applications within this concentrated period. Research different lenders and get pre-approvals within a few weeks, rather than spreading out your applications over several months. This strategy allows you to compare offers effectively without unnecessarily penalizing your credit score.

The Positive Side: How a Car Loan Can Boost Your Credit

While the application process causes a minor, temporary dip, the real potential for a car loan to positively affect your credit score unfolds over the loan’s term. When managed responsibly, an auto loan can be an excellent credit-building tool, particularly for those looking to establish or improve their credit profile.

Payment History: The Cornerstone of Credit Building

The most significant way a car loan can boost your credit is through consistent, on-time payments. As we discussed, payment history accounts for 35% of your FICO score, making it the most influential factor. Each month you make your car payment on time, you’re building a positive credit history, demonstrating reliability and financial responsibility to future lenders.

From my perspective, this is where a car loan truly shines as a credit-building tool. Unlike credit cards, which offer revolving credit and the temptation to overspend, an installment loan like a car loan has a fixed payment and a clear end date. This structure can make it easier to manage and consistently make those crucial on-time payments. Over years of steady payments, this positive history accumulates, steadily pushing your credit score upward.

Diversifying Your Credit Mix: A Sign of Financial Maturity

Another way a car loan positively impacts your credit is by diversifying your "credit mix." Your credit mix, which accounts for 10% of your FICO score, refers to the different types of credit accounts you manage. Lenders prefer to see that you can handle both revolving credit (like credit cards) and installment loans (like auto loans, mortgages, or student loans).

If your credit history primarily consists of credit cards, adding an installment loan like a car loan demonstrates your ability to manage a different type of debt responsibly. This diversification signals financial maturity to credit bureaus and lenders, potentially leading to a higher credit score. It shows that you’re not solely reliant on one type of credit, making you a more attractive borrower.

Building Credit for "Credit Invisibles" or Thin Files

For individuals with little to no credit history, often referred to as "credit invisibles" or those with "thin files," a car loan can be a foundational step. It’s challenging to get credit without a credit history, creating a classic catch-22. A car loan, especially one with a co-signer or from a lender specializing in new credit, can be the first significant entry on your credit report.

By successfully managing and repaying this loan, you begin to establish a positive credit history, opening doors to future financial products like mortgages or personal loans. This initial positive entry is invaluable for building a robust credit profile from the ground up. You can learn more about establishing credit from scratch in our detailed guide: .

The Negative Side: When a Car Loan Can Hurt Your Credit

While a car loan offers significant credit-building potential, it’s a double-edged sword. Mismanagement can lead to severe negative consequences for your credit score, taking months or even years to recover. Understanding these pitfalls is as important as knowing the benefits.

Late Payments: The Credit Score Destroyer

The most damaging mistake you can make with a car loan is missing a payment or making it late. A single payment that is 30 days or more past due can cause a significant drop in your credit score, potentially by dozens of points. The longer the payment is delayed, and the more frequently it happens, the more severe the damage.

A common mistake many make is underestimating the ripple effect of a single late payment. This negative mark remains on your credit report for seven years, signaling to future lenders that you might be a high-risk borrower. Even if you catch up on payments, the initial late payment record continues to impact your score.

Defaulting or Repossession: Catastrophic Consequences

If you consistently fail to make your car payments, you risk defaulting on your loan. This can lead to the lender repossessing your vehicle. Both a loan default and a repossession are catastrophic events for your credit score. They are severe negative marks that will remain on your credit report for seven years, making it incredibly difficult to obtain new credit, secure favorable interest rates, or even rent an apartment.

Beyond the credit score impact, you may still owe the difference between the outstanding loan balance and the amount the lender sells the car for at auction, known as a "deficiency balance." This can lead to further financial strain and potential collection agency involvement, adding another layer of negative reporting to your credit.

Excessive Debt and High Debt-to-Income Ratio

Taking on a car loan that is too large for your income can also negatively impact your credit and overall financial health. While the car loan itself is an installment loan and doesn’t directly affect your credit utilization ratio (which applies to revolving credit), a high loan amount contributes to your overall debt burden. This can lead to a high debt-to-income (DTI) ratio, which lenders consider when assessing your ability to take on more debt.

A high DTI ratio signals that a significant portion of your income is already committed to debt payments, making you a riskier borrower for future loans, such as a mortgage. It can indirectly impact your ability to get approved for other credit products or secure competitive rates.

Loan Shopping Spree (Outside the Window)

As mentioned earlier, applying for multiple car loans within a short, concentrated window (the "rate shopping window") is generally fine. However, if you apply for numerous auto loans spread out over several months, or apply for different types of loans concurrently (e.g., a car loan, a credit card, and a personal loan), the cumulative effect of these hard inquiries can be detrimental. Each inquiry outside the rate shopping window could result in a small score drop, indicating to lenders that you are actively seeking credit, which can be perceived as a sign of financial distress.

Managing Your Car Loan for Optimal Credit Health

The key to leveraging a car loan as a credit-building asset lies in proactive and responsible management. By following a few best practices, you can ensure your auto financing journey has a positive impact on your financial future.

1. Budgeting and Affordability: Choose Wisely

Before you even apply for a car loan, it’s crucial to determine what you can genuinely afford. Don’t just consider the monthly payment; factor in insurance, fuel, maintenance, and registration costs. Taking on a loan that stretches your budget thin significantly increases the risk of late or missed payments.

Our pro tip for managing any loan is consistency and vigilance. Create a detailed budget and stick to it. Choose a car and a loan amount that leaves you with comfortable breathing room each month, even if unexpected expenses arise.

2. Prioritize On-Time Payments: Consistency is Key

This cannot be stressed enough: make every single payment on time, every single month. Set up automatic payments from your bank account to avoid accidental oversights. If automatic payments aren’t an option, set calendar reminders a few days before the due date.

Consider setting up reminders on your phone or using a budgeting app to keep track of payment due dates. Even paying a few days early, if possible, provides an extra buffer against unforeseen delays.

3. Monitor Your Credit Report Regularly: Spot Errors and Stay Informed

Regularly checking your credit report is a powerful habit for all aspects of credit management. You are entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months via AnnualCreditReport.com. Review your reports for any inaccuracies, especially regarding your car loan.

Errors such as incorrect payment dates or reporting of a late payment when you paid on time can unfairly damage your score. If you find an error, dispute it immediately with the credit bureau and the lender. This vigilance ensures your credit report accurately reflects your responsible financial behavior. .

4. Understand Your Loan Terms: No Surprises

Before signing any loan agreement, thoroughly understand all the terms and conditions. This includes the interest rate, the total amount you will pay over the loan’s life, the payment schedule, and any potential prepayment penalties. Knowing these details prevents surprises and helps you plan your payments effectively.

Some loans might have clauses that could penalize you for paying off the loan early. While this is less common with standard auto loans, it’s always worth confirming. Knowledge is power when it comes to financial agreements.

5. Communicate with Your Lender: Proactive Problem Solving

If you anticipate difficulty making a payment, don’t wait until it’s too late. Contact your lender immediately. Many lenders are willing to work with you, especially if you have a good payment history. They might offer options like deferring a payment, adjusting your payment schedule, or providing temporary hardship programs.

Being proactive and transparent with your lender demonstrates responsibility and can help you avoid a negative mark on your credit report. It’s always better to seek solutions than to ignore the problem.

The Long-Term Picture: After the Loan is Paid Off

Once you’ve made that final car loan payment, a significant milestone is reached. What happens to your credit score then? The good news is that the positive impact of your responsible payment history doesn’t vanish.

When the loan is fully paid off, the account will be marked as "paid in full" on your credit report. This is a very positive entry, demonstrating successful debt management. While the account is closed, the positive payment history for the duration of the loan will remain on your credit report for up to 10 years. This long-term record continues to contribute positively to your credit score, especially regarding the "Length of Credit History" factor. It shows a proven track record of managing an installment loan successfully.

Common Myths and Misconceptions About Car Loans and Credit

Based on countless conversations, these myths often lead to unnecessary anxiety or poor financial decisions. Let’s debunk a few common misconceptions about how car loans affect your credit.

- Myth 1: Paying off a car loan early always hurts your credit score. While paying off an installment loan might slightly reduce the "average age of accounts" on your credit report, which could have a minimal, temporary effect, the overall impact is overwhelmingly positive. You eliminate debt, save on interest, and the record of successful repayment remains on your report for years, boosting your payment history. The benefit of being debt-free and improving your debt-to-income ratio far outweighs any negligible score dip.

- Myth 2: Applying for multiple car loans instantly ruins your credit. As discussed, the "rate shopping window" allows you to apply with several lenders for the same type of loan within a short period (typically 14-45 days) without multiple hits to your score. Credit models are smart enough to recognize you’re looking for one car, not multiple loans.

- Myth 3: You need a perfect credit score to get a car loan. This is simply not true. While a higher score will qualify you for the best interest rates, lenders offer loans to individuals across a wide spectrum of credit scores. Those with lower scores may face higher interest rates or require a larger down payment, but getting approved is often still possible.

Conclusion: Navigating Your Car Loan for a Brighter Financial Future

Understanding how a car loan will affect your credit is paramount for anyone considering auto financing. It’s clear that a car loan is a powerful financial tool, capable of significantly boosting your credit score when managed responsibly, but also posing substantial risks if neglected. The journey from application to full repayment is a critical period that can define your creditworthiness for years to come.

By prioritizing on-time payments, choosing an affordable loan, understanding your terms, and diligently monitoring your credit report, you can harness the positive power of a car loan. It’s an opportunity to build a robust credit history, diversify your credit mix, and ultimately pave the way for future financial goals. Remember, informed decisions today lead to a stronger financial tomorrow. Take control of your financial future and make your car loan a testament to your credit-building success. For a deeper dive into managing your overall financial health, consider exploring our guide on .