I Got Pre Approved For A Car Loan, Now What? Your Ultimate Guide to Smart Car Buying

I Got Pre Approved For A Car Loan, Now What? Your Ultimate Guide to Smart Car Buying Carloan.Guidemechanic.com

Congratulations! Receiving a pre-approval for a car loan is an exciting milestone. It means a lender has assessed your financial standing and is ready to offer you financing, giving you a clear idea of how much you can borrow and at what interest rate. This isn’t just a pat on the back; it’s a powerful tool that puts you in a much stronger position when you walk into a dealership.

However, the journey doesn’t end with pre-approval; in many ways, it’s just beginning. Many buyers, fueled by the excitement, rush into the next steps without a clear strategy, potentially leaving money on the table or making less-than-ideal choices. This comprehensive guide is designed to transform that initial pre-approval into a smart, stress-free car buying experience. We’ll walk you through every critical step, ensuring you leverage your pre-approval to secure the best deal possible.

I Got Pre Approved For A Car Loan, Now What? Your Ultimate Guide to Smart Car Buying

Understanding Your Pre-Approval Letter: The Foundation of Your Power

When you get pre-approved for a car loan, it’s easy to feel a rush of excitement. This document, however, is far more than just a piece of paper; it’s your financial blueprint for car shopping. Before you even think about stepping onto a car lot, it’s crucial to thoroughly understand every detail of what your pre-approval actually means. This initial step sets the stage for all your subsequent decisions.

What Exactly Does "Pre-Approval" Mean?

A car loan pre-approval is essentially a conditional offer from a lender. It signifies that, based on a review of your credit history, income, and debt-to-income ratio, the lender is willing to lend you a specific amount of money at a particular interest rate and for a defined loan term. It’s not a final, binding contract for a specific car, but rather a strong indication of your borrowing power.

Think of it as having a "cash in hand" status. You’re entering the dealership with a clear understanding of your external financing options, which dramatically shifts the negotiation dynamic in your favor. This financial clarity allows you to focus on the car’s price, rather than getting caught up in the dealership’s financing maze.

Key Details to Scrutinize in Your Letter

Your pre-approval letter isn’t just a confirmation; it’s packed with vital information you must understand. Based on my experience, many buyers overlook these critical details, only to find surprises later on. Take the time to meticulously review each element.

First, identify the approved loan amount. This is the maximum sum the lender is willing to provide. It defines the upper limit of your car shopping budget, helping you avoid looking at vehicles that are financially out of reach. Remember, this amount doesn’t include your down payment or trade-in value, which can further extend your purchasing power.

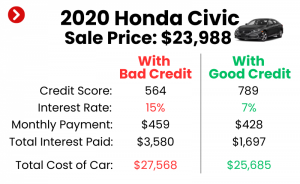

Next, pay close attention to the interest rate (APR). This is arguably the most crucial number, as it directly impacts the total cost of your loan over its lifetime. Even a small difference in the interest rate can translate into hundreds or even thousands of dollars in savings or additional costs. Compare this rate to general market rates for someone with your credit score to gauge its competitiveness.

The loan term, typically expressed in months (e.g., 60 months, 72 months), is another significant factor. A longer loan term usually means lower monthly payments, but it also means you’ll pay more in interest over time. Conversely, a shorter term has higher monthly payments but reduces the overall interest paid. Find a balance that fits your budget and financial goals.

Finally, check for any conditions or stipulations. Some pre-approvals might have specific requirements, such as a minimum down payment, a certain age limit for the vehicle, or a requirement for comprehensive insurance. Understanding these conditions upfront ensures there are no last-minute roadblocks when you’re ready to finalize your purchase.

How Your Pre-Approval Impacts Your Budget

Your pre-approval letter provides a solid foundation for your car buying budget. Knowing the maximum loan amount and your potential monthly payment allows you to narrow down your vehicle choices effectively. It prevents the common pitfall of falling in love with a car you can’t truly afford.

However, it’s essential to remember that the pre-approved amount is just one piece of the budget puzzle. It doesn’t account for other significant costs associated with car ownership. We’ll delve into those in the next section, but for now, recognize your pre-approval as a powerful starting point for responsible financial planning.

Setting Your Realistic Car Buying Budget: Beyond the Monthly Payment

While your pre-approval tells you how much a lender is willing to give you, it doesn’t automatically dictate how much you should spend. A common mistake buyers make is focusing solely on the monthly loan payment. This narrow view often leads to unexpected financial strain down the road. A truly smart car buying budget encompasses far more than just your loan repayment.

It’s More Than Just the Monthly Payment

When you consider a car, your financial planning needs to extend beyond the loan amount itself. There are numerous recurring and one-time expenses that contribute to the true cost of car ownership. Overlooking these can quickly turn the excitement of a new vehicle into a financial burden.

Your budget needs to be holistic, factoring in every penny that will go towards your new ride. This comprehensive approach ensures you’re prepared for the full financial commitment, not just the most visible one. By doing so, you maintain financial stability and genuinely enjoy your purchase without constant worry.

Hidden Costs: Insurance, Maintenance, Fuel, Registration, Taxes

Let’s break down these often-underestimated expenses. Pro tips from us: Always get quotes for these costs before you commit to a specific vehicle.

Car Insurance: This is non-negotiable and can vary wildly based on the car’s make, model, year, your driving record, age, and location. A high-performance car will almost always have higher insurance premiums than an economical sedan. Get multiple quotes for specific models you’re considering. We’ll discuss this in more detail later.

Maintenance and Repairs: All cars need maintenance. New cars come with warranties, but routine services (oil changes, tire rotations) are still your responsibility. Used cars, especially older ones, might require more frequent and costly repairs. Research the average maintenance costs for specific models. Websites like Edmunds or Kelley Blue Book often provide estimates.

Fuel: This cost fluctuates with gas prices and your driving habits. Consider the car’s fuel efficiency (MPG). A vehicle that gets 20 MPG will cost significantly more in fuel than one that gets 35 MPG over a year, especially if you have a long commute.

Registration and Taxes: These are typically one-time or annual costs. Sales tax on the purchase price can be substantial, depending on your state. Vehicle registration fees are recurring and vary by state and sometimes by vehicle type or value. Don’t forget potential property taxes on the vehicle in some areas.

Calculating Total Cost of Ownership

To get a complete picture, you need to calculate the Total Cost of Ownership (TCO). This involves adding up the projected costs for the loan, insurance, fuel, maintenance, and registration/taxes over a specific period, typically five years. Several online calculators can help you estimate this, but populating them with your specific data is key.

For example, if a car costs $25,000, but has high insurance, poor fuel economy, and known expensive maintenance issues, its TCO could easily outstrip a $28,000 car with better running costs. Pro Tip: Create a detailed spreadsheet. List potential vehicles and their estimated costs across all these categories. This visual comparison will highlight the true financial impact of each option.

Don’t Forget the Down Payment

Your down payment is a critical component of your car buying budget. While your pre-approval sets the maximum loan amount, a substantial down payment can significantly reduce your monthly payments and the total interest you pay over the loan term. It also builds equity faster and can make you a more attractive borrower.

Aim for at least 10-20% of the vehicle’s purchase price, if possible. If you have a trade-in, that value can contribute to your down payment. The larger your down payment, the less you need to borrow, which can be a huge financial advantage in the long run.

Researching the Right Vehicle: Matching Needs with Reality

With your budget firmly established thanks to your pre-approval and comprehensive cost analysis, the next exciting step is finding the perfect car. This isn’t just about aesthetics; it’s about matching your practical needs, lifestyle, and financial boundaries with a reliable vehicle. Smart research here prevents buyer’s remorse later.

Defining Your Needs vs. Wants

Before you get swayed by shiny exteriors or impressive horsepower, make a clear distinction between what you need in a car and what you want. Do you need space for a growing family, or is a compact sedan sufficient for your daily commute? Is fuel efficiency paramount, or do you prioritize towing capacity?

Needs are non-negotiable functionalities, while wants are desirable features that can be compromised if necessary. Prioritizing needs ensures the car serves its primary purpose effectively, while a realistic look at wants helps keep you within budget.

New vs. Used: Pros and Cons

This is a fundamental decision that significantly impacts cost, depreciation, and features. Both options have distinct advantages and disadvantages.

New Cars:

- Pros: Latest technology and safety features, full factory warranty, customizable options, that "new car smell."

- Cons: Rapid depreciation (especially in the first few years), higher purchase price, potentially higher insurance premiums.

Used Cars:

- Pros: Significant cost savings (depreciation has already occurred), lower insurance rates, wider selection of models within your budget.

- Cons: Shorter or no warranty, potential for unknown mechanical issues, older technology, less customization.

A pre-owned certified (CPO) vehicle can offer a good middle ground, providing some warranty coverage and inspection assurance for a used car price.

Reliability, Safety Ratings, Resale Value

These are crucial long-term considerations for any vehicle purchase. A cheap car that constantly needs repairs isn’t cheap in the long run.

Research reliability ratings from reputable sources like Consumer Reports, J.D. Power, or Edmunds. These reports provide insights into common issues and overall owner satisfaction. A reliable car means fewer unexpected expenses and less stress.

Always check safety ratings from organizations like the National Highway Traffic Safety Administration (NHTSA) and the Insurance Institute for Highway Safety (IIHS). These ratings assess crashworthiness and safety features, which are paramount for your peace of mind.

Consider the resale value of the vehicles you’re looking at. Some brands and models hold their value better than others. A strong resale value means you’ll recoup more of your investment when it’s time to sell or trade in the car in the future.

Reading Reviews and Test Driving (Crucial Step)

Online reviews from owners and professional automotive journalists offer invaluable insights into real-world performance, comfort, and common quirks. Pay attention to consistent complaints or praises across multiple reviews.

However, nothing replaces a thorough test drive. This isn’t just a quick spin around the block. Drive the car on various road conditions you’ll encounter regularly – city streets, highways, uneven roads. Test acceleration, braking, handling, and visibility. Check the comfort of the seats, the functionality of the infotainment system, and the ease of parking.

Common mistakes to avoid are falling in love with a car based solely on its looks or online reviews without experiencing it firsthand. The test drive is your opportunity to confirm if the car genuinely fits your driving style and comfort preferences. Bring a trusted friend or family member for a second opinion.

Leveraging Your Pre-Approval at the Dealership: Your Power Play

Armed with a clear budget and a shortlist of desired vehicles, you’re ready to engage with dealerships. This is where your pre-approval truly shines as a strategic advantage. It transforms your position from a hopeful buyer seeking financing into a strong, confident negotiator.

Why Pre-Approval Gives You an Edge

Entering a dealership with a pre-approval letter in hand immediately signals to the sales team that you are a serious, qualified buyer. You’ve already secured financing, which means the dealership doesn’t need to "qualify" you for a loan. This saves them time and effort, and crucially, it removes one of their primary negotiation levers.

You’re no longer dependent on the dealership’s finance department to get approved. This shifts the focus entirely to the price of the vehicle itself, rather than getting tangled in a bundled deal where financing terms might obscure the actual car price. You dictate the terms, not them.

Negotiating Power: You’re a Cash Buyer (in Essence)

With your pre-approval, you essentially walk in as a "cash buyer." While you’re not paying with physical cash, you have guaranteed funds from an external lender. This means the dealership’s primary goal becomes selling you the car at the best possible price for them, rather than also trying to profit heavily from the financing.

This position allows you to negotiate with confidence. You can insist on discussing the vehicle’s price independently of any financing offers the dealership might present. If they try to bundle, you can politely but firmly separate the conversations, knowing you have a solid backup financing option.

Comparing Dealership Financing Offers with Your Pre-Approval

Even though you have your pre-approval, it’s a pro tip from us to still allow the dealership to present their financing options. Why? Because they might, on occasion, be able to beat your pre-approved rate, especially if they have special manufacturer incentives or can access a lender with a slightly better offer.

Use your pre-approval as your baseline. If the dealership can offer a lower interest rate or better terms, great! You’ve just saved more money. If their offer is higher or less favorable, you simply stick with your pre-approved loan. This comparison ensures you’re always getting the most competitive financing available. From years of observing car transactions, buyers who compare always fare better.

The Dealership Dance: Mastering Negotiation Strategies

Negotiating at a car dealership can feel intimidating, but with your pre-approval in hand, you hold a significant advantage. The key is to approach the process strategically, separating different components of the deal to ensure you get the best value for each.

Negotiating the Car Price First, Separate from Financing

This is perhaps the most crucial negotiation strategy. Always focus on agreeing upon the out-the-door price of the vehicle before discussing financing options. Dealers often try to bundle everything together, making it difficult to discern if you’re getting a good deal on the car or if a seemingly low monthly payment is masking a higher vehicle price or unfavorable loan terms.

State clearly that you want to negotiate the vehicle’s price first, independent of your financing or trade-in. Your pre-approval allows you to do this effectively, as you’re not reliant on their financing to buy the car. Aim for a price that is competitive based on your market research.

The Trade-In: A Separate Negotiation

If you have a vehicle to trade in, treat it as a separate transaction. Many buyers make the mistake of discussing their trade-in value too early in the negotiation process. This allows the dealer to play with numbers, offering you a seemingly higher trade-in value while inflating the price of the new car, or vice-versa.

Once you have a firm, agreed-upon price for the new car, then introduce your trade-in. Negotiate its value as if you were selling it outright. Research your car’s value on sites like Kelley Blue Book (KBB) or Edmunds beforehand so you have a realistic expectation. If the dealership’s offer is too low, be prepared to sell your old car privately.

Add-Ons and Extras: Be Wary

Once the car price and trade-in are settled, you’ll likely be moved to the finance and insurance (F&I) office. This is where dealers often try to upsell you on various add-ons and extras, such as extended warranties, paint protection, fabric guard, VIN etching, or gap insurance.

While some of these might have value (e.g., gap insurance if you have a small down payment), many are highly profitable for the dealership and can be purchased for less elsewhere or might not be necessary at all. Politely decline anything you don’t want or haven’t thoroughly researched. Common mistakes to avoid are feeling pressured into these add-ons; you have the right to say no.

Walking Away Is Always an Option

Never underestimate the power of being willing to walk away from a deal. If you feel pressured, if the numbers aren’t right, or if the dealership isn’t being transparent, politely end the negotiation. There are always other dealerships and other cars. Your pre-approval gives you the freedom to do this without worrying about securing financing elsewhere.

Pro Tip: Don’t discuss your pre-approval rate until a price is agreed upon. Keep your pre-approval as your secret weapon until you’re ready to compare financing options. This strategy keeps the dealer focused on giving you the best price for the car itself. For more in-depth negotiation tactics, consider reading Mastering Car Dealership Negotiations.

The Importance of a Pre-Purchase Inspection (Don’t Skip This!)

Once you’ve settled on a specific vehicle and agreed on a price, there’s one critical step remaining before you sign on the dotted line, especially if you’re buying a used car: a pre-purchase inspection (PPI). This step is often overlooked by eager buyers, but it can save you thousands of dollars and countless headaches.

Especially for Used Cars

A PPI is absolutely essential when buying a used vehicle. While a dealership might perform their own inspection and offer a "certified pre-owned" vehicle, an independent third-party opinion is invaluable. Dealers have an incentive to sell the car, whereas an independent mechanic’s only incentive is to give you an honest assessment of the vehicle’s condition.

Even new cars can have minor issues from transport or manufacturing, but the risk of hidden problems is significantly higher with used vehicles. A PPI acts as your independent insurance policy against unforeseen mechanical or structural issues.

Why a Third-Party Mechanic Is Crucial

Taking the car to a mechanic of your choosing ensures an unbiased evaluation. This mechanic has no vested interest in the sale of the vehicle. They work for you, and their loyalty is to your best interests, not the dealership’s bottom line. They can identify problems that might not be visible during a test drive or that a dealership might try to downplay.

Ideally, choose a mechanic who specializes in the make and model of the car you’re considering. They’ll know common issues to look for and have the specialized tools and knowledge to spot potential problems quickly. Always make sure the dealership agrees to allow the PPI, which most reputable dealers will.

What They Look For

During a comprehensive PPI, the mechanic will perform a thorough inspection covering various aspects of the vehicle. This includes:

- Engine and Transmission: Checking for leaks, strange noises, fluid levels, and overall health.

- Brakes: Inspecting pads, rotors, lines, and fluid.

- Suspension and Steering: Looking for worn components, alignment issues, and smooth operation.

- Tires: Assessing tread depth, wear patterns, and overall condition.

- Electrical System: Testing lights, windows, infotainment, and other electronic components.

- Frame and Body: Checking for signs of previous accidents, rust, or shoddy repair work.

- Diagnostic Scan: Running computer diagnostics to check for any stored error codes.

They’ll also check for any outstanding recalls or service bulletins that might affect the vehicle.

Potential Savings from Identifying Issues

The cost of a PPI (typically $100-$200) is a small investment that can yield significant returns. If the mechanic uncovers major issues, you have several options:

- Negotiate Further: You can use the inspection report to negotiate a lower price for the vehicle, accounting for the cost of repairs.

- Request Repairs: You can ask the dealership to fix the identified issues before you purchase the car.

- Walk Away: If the problems are too extensive or costly, or if the dealership isn’t willing to budge, you can walk away from the deal entirely.

Identifying just one significant problem, like a failing transmission or extensive rust, could save you thousands of dollars that you would have otherwise spent on repairs shortly after purchase.

Understanding the Final Loan Documents: Read Everything!

You’ve found the perfect car, negotiated a great price, and secured excellent financing thanks to your pre-approval. Now comes the paperwork, the final hurdle before you drive off the lot. This stage is critical, and rushing through it can lead to costly mistakes. It’s imperative to read every single document carefully.

Interest Rate, APR (Annual Percentage Rate), Loan Term

When you’re presented with the final loan documents, double-check the interest rate and Annual Percentage Rate (APR). The interest rate is the cost of borrowing money, but the APR is the total cost, including any fees or additional charges, expressed as an annual rate. The APR is usually slightly higher than the interest rate and provides a more accurate representation of the total cost of your loan. Ensure these numbers match what you were promised and what your pre-approval specified (or the better rate the dealership offered).

Also, confirm the loan term (e.g., 60 months, 72 months) is exactly what you agreed upon. A longer term might seem appealing due to lower monthly payments, but it significantly increases the total interest paid over the life of the loan. Ensure there are no unexpected changes to the term that could impact your financial plan.

Fees and Charges

Scrutinize the breakdown of all fees and charges. These can include documentation fees, registration fees, title fees, and potentially other administrative charges. While some fees are standard and legally mandated, others can be negotiable or even questionable. Question any fee you don’t understand or that seems excessively high.

Common mistakes to avoid are signing without fully understanding each fee. Don’t be afraid to ask for a detailed explanation of every line item. Ensure there are no "mystery" charges or inflated figures. Your pre-approval allows you to be firm here, as you’re not desperate for their financing.

Reviewing the Fine Print

Beyond the numbers, read the fine print of the loan agreement. Look for clauses regarding early payment penalties (though less common now), late payment fees, and any conditions that could affect your loan. Understand your responsibilities as the borrower and the lender’s rights.

It’s also important to review the vehicle purchase agreement, ensuring the final negotiated price of the car, any trade-in value, and agreed-upon add-ons are correctly reflected. Compare these figures to your own notes and calculations.

Don’t Feel Rushed. Ask Questions.

Dealership finance managers often work quickly, presenting stacks of documents for signatures. Pro tips from us: Do not feel rushed. You have the right to take your time and read everything thoroughly. If you don’t understand something, ask for clarification. If the explanation isn’t satisfactory, ask again.

It’s your money and your long-term financial commitment. Bring a calculator, and if possible, a trusted friend or family member to review the documents with you. Ensure that the terms you’re signing match the terms you agreed to during the negotiation phase.

Protecting Your Investment: Car Insurance

Before you can legally drive your new car off the lot, you’ll need to secure proper car insurance. This isn’t just a legal requirement; it’s a vital step in protecting your investment and your financial well-being. Getting insurance sorted before the purchase is a smart move.

Mandatory Requirements

Almost every state mandates a minimum level of car insurance, primarily liability coverage. This covers damages and injuries you might cause to other people or their property in an accident. Driving without at least this minimum coverage can result in hefty fines, license suspension, or even jail time.

Furthermore, if you’re financing your car, your lender will almost certainly require you to carry full coverage, which includes collision and comprehensive insurance, to protect their financial interest in the vehicle. This is non-negotiable when you have a loan.

Types of Coverage: Liability, Comprehensive, Collision

Let’s briefly break down the main types of coverage:

- Liability Coverage: As mentioned, this pays for damages you cause to others. It usually has two components: bodily injury liability (for medical expenses) and property damage liability (for repairs to other vehicles or property).

- Collision Coverage: This pays for damages to your car resulting from a collision with another vehicle or object, regardless of who is at fault.

- Comprehensive Coverage: This covers damages to your car from non-collision events, such as theft, vandalism, fire, natural disasters (hail, floods), or hitting an animal.

Beyond these, you might consider other coverages like uninsured/underinsured motorist coverage, medical payments coverage, or roadside assistance.

Getting Quotes Before Buying the Car

This is a critical pro tip from us: obtain insurance quotes for the specific make, model, and year of the car you intend to buy before you finalize the purchase. Insurance premiums can vary significantly based on the vehicle’s value, safety ratings, repair costs, and even its popularity for theft.

Getting quotes beforehand allows you to factor the actual insurance cost into your overall budget. You don’t want to get a great deal on a car only to find out its insurance premiums are prohibitively expensive. Compare quotes from several different insurance providers to find the most competitive rates. A trusted external source like NerdWallet’s Car Insurance Guide can help you compare options.

How It Impacts Your Total Monthly Cost

Remember our discussion about the total cost of ownership? Car insurance is a significant recurring expense that directly impacts your monthly budget. When you’re calculating your affordable monthly payment, always include the estimated insurance premium alongside your loan payment, fuel, and potential maintenance savings.

Having your pre-approval in hand gives you the clarity to focus on these other costs without the added stress of securing financing. By getting insurance quotes early, you ensure that your new car purchase remains comfortably within your overall financial plan.

The Final Steps and Driving Away: Celebration and Responsibility

You’ve navigated the entire car buying process like a pro, leveraging your pre-approval to your advantage. Now, it’s time for the final touches and to enjoy the fruits of your smart decision-making. The last steps involve administrative details and embracing responsible car ownership.

Registration and Plates

Once the paperwork is signed and the financing is complete, the dealership will typically handle the initial vehicle registration and temporary plates. They’ll submit the necessary documents to your state’s Department of Motor Vehicles (DMV) or equivalent agency. You’ll usually receive permanent license plates and registration within a few weeks, either directly from the DMV or through the dealership.

Ensure you understand the process for your specific state and when you can expect your permanent documents. Keep your temporary registration and plates securely displayed as required by law.

Maintenance Schedule

A new car is a significant investment, and proper maintenance is key to protecting its value and ensuring its longevity. Familiarize yourself with the manufacturer’s recommended maintenance schedule, which you’ll find in your owner’s manual. Adhering to this schedule helps prevent major issues, keeps your warranty valid, and maintains the car’s performance.

Regular oil changes, tire rotations, fluid checks, and timely inspections are essential. Don’t defer maintenance, as small problems can quickly escalate into expensive repairs. Your proactive approach to car buying should extend to car ownership as well. For more on this, check out Maintaining Your New Car for Longevity.

Enjoying Your New Car Responsibly

Finally, it’s time to celebrate! You’ve made a well-informed, financially sound decision. Drive your new car with confidence, knowing you got a great deal and are fully prepared for the responsibilities of ownership. Enjoy the freedom and convenience it brings, whether it’s for daily commutes, weekend adventures, or family trips.

Remember the research, negotiation, and diligence that went into this purchase. That same level of care should continue as you maintain and drive your vehicle responsibly.

Conclusion: Your Smart Car Buying Journey Complete

Getting pre-approved for a car loan is a fantastic start, but as we’ve explored, it’s just the first step in a strategic car buying journey. From meticulously understanding your pre-approval letter and crafting a comprehensive budget to leveraging your power at the dealership and scrutinizing final documents, every stage offers an opportunity to save money and ensure a satisfying purchase.

By taking the time to research, negotiate wisely, and prepare for all associated costs, you’ve transformed a potentially stressful transaction into an empowering experience. You’ve avoided common pitfalls, secured the best possible financing, and driven away with a vehicle that truly meets your needs and budget. So, if you’ve been asking "I got pre approved for a car loan, now what?", the answer is clear: embark on this journey with knowledge, confidence, and a well-defined strategy. Happy driving!