I Need A Car Loan ASAP: Your Ultimate Guide to Fast Approval and Driving Away Sooner

I Need A Car Loan ASAP: Your Ultimate Guide to Fast Approval and Driving Away Sooner Carloan.Guidemechanic.com

Life often throws unexpected curveballs, and sometimes, those curveballs involve a sudden, urgent need for a car. Perhaps your old vehicle just gave up the ghost, a new job requires a reliable commute, or an emergency has made transportation essential. Whatever the reason, if you find yourself thinking, "I need a car loan ASAP," you’re not alone. The good news is that securing fast car financing is entirely possible with the right approach and preparation.

Navigating the world of auto loans, especially under pressure, can feel overwhelming. Many people believe that speed means sacrificing good terms or getting stuck with a bad deal. This doesn’t have to be the case. This comprehensive guide will arm you with the knowledge, strategies, and insider tips to secure an urgent car loan quickly, efficiently, and on favorable terms, helping you get back on the road sooner.

I Need A Car Loan ASAP: Your Ultimate Guide to Fast Approval and Driving Away Sooner

Understanding the "ASAP" Urgency: What Lenders Look For

When you need a car loan urgently, the primary goal is often speed. However, speed shouldn’t compromise thoroughness. Lenders, even those offering rapid approval, still need to assess your creditworthiness. They want to be confident that you can and will repay the loan.

The "ASAP" factor means minimizing delays at every step. This involves understanding what information lenders require and having it ready before you even apply. It’s about streamlining the process from your end to make their decision-making as straightforward and quick as possible.

Pillar 1: Assess Your Financial Readiness – The Foundation of Fast Approval

Before you even think about submitting an application, taking an honest look at your current financial standing is crucial. This self-assessment will not only help you understand your options but also prepare you for what lenders will scrutinize. Skipping this step is a common mistake that significantly slows down the approval process.

Your Credit Score: The Silent Narrator of Your Financial History

Your credit score is arguably the most significant factor lenders consider. It’s a three-digit number that summarizes your credit risk based on your payment history, debt levels, length of credit history, and more. A higher score generally translates to better loan terms and faster approval.

Based on my experience, many people underestimate the power of their credit score. Lenders use it as a quick snapshot to gauge your reliability. For an "ASAP" loan, a strong score can unlock instant pre-approvals and expedited processes. You can obtain a free copy of your credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) once a year. Reviewing this report helps you identify any errors and understand where you stand.

Income and Employment Stability: Proof You Can Pay

Lenders need assurance that you have a consistent source of income to make your monthly payments. They typically look for stable employment history, often preferring at least six months to a year at your current job. Your income amount will also determine how much you can realistically borrow.

Having proof of income readily available is vital for rapid approval. This usually includes recent pay stubs (the last two or three), W-2 forms from previous years, and sometimes even bank statements showing regular deposits. For self-employed individuals, tax returns and profit-and-loss statements will be essential.

Debt-to-Income Ratio (DTI): Balancing Your Books

Your Debt-to-Income (DTI) ratio is another critical metric. It’s calculated by dividing your total monthly debt payments by your gross monthly income. Lenders use DTI to assess your ability to take on additional debt. A lower DTI indicates you have more disposable income to cover new loan payments.

Pro tips from us: Aim for a DTI of 36% or lower, though some lenders may approve up to 43% for auto loans. If your DTI is on the higher side, consider paying down some smaller debts before applying, if time permits. This small step can make a big difference in speeding up your approval.

The Power of a Down Payment: Showing Commitment

While "no money down" car loans exist, making a significant down payment can dramatically speed up your approval and improve your loan terms. A down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows the lender your commitment to the purchase.

Even a modest down payment of 10-20% can make your application more attractive. If you have some savings, allocating a portion towards a down payment is a strategic move for getting a car loan ASAP. It can also help offset a less-than-perfect credit score.

Pillar 2: Gather Your Documents – Preparation is Key to Speed

The single biggest delay in securing a car loan quickly is often missing or incomplete documentation. Lenders cannot process your application without all the necessary paperwork. Having everything organized and accessible before you even apply is paramount for an "ASAP" approval.

Common mistakes to avoid are waiting until a lender asks for a specific document. Anticipate their needs. Based on my experience, preparing a digital folder with scans or photos of these documents can shave days off the approval process.

Here’s a checklist of essential documents you should have ready:

- Proof of Identity: Valid driver’s license or state-issued ID.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement (dated within the last 60 days).

- Proof of Income: Recent pay stubs (2-3), W-2 forms, tax returns (for self-employed), bank statements.

- Proof of Insurance: You’ll need to show proof of auto insurance before driving off the lot. Having a quote or understanding your options ready will expedite this final step.

- Bank Account Information: For setting up automatic payments.

- Trade-in Information (if applicable): Title, registration, and payoff amount for your current vehicle.

Organizing these documents beforehand allows you to complete online applications swiftly and respond to lender requests almost instantly. This level of preparedness signals to lenders that you are a serious and organized borrower.

Pillar 3: Explore Your Loan Options – Where to Find Fast Financing

Not all lenders are created equal when it comes to speed. Knowing where to look for an urgent car loan can save you valuable time. Different types of lenders offer varying application processes and approval timelines.

Online Lenders: The Speed Champions

For those thinking, "I need a car loan ASAP," online lenders are often the fastest route. Many specialized online platforms offer streamlined application processes, quick pre-qualifications, and sometimes even same-day approval and funding. Their digital-first approach means less paperwork and faster communication.

Online lenders are excellent for comparing rates from multiple providers without affecting your credit score with numerous hard inquiries. They cater to a wide range of credit scores, including those with less-than-perfect credit.

Credit Unions: Member Benefits and Competitive Rates

Credit unions are known for their member-focused approach and often offer competitive interest rates, sometimes lower than traditional banks. If you’re already a member of a credit union, or if you can quickly join one, they can be a great option for a fast car loan.

While they might not always be as lightning-fast as some online lenders, the application process is typically efficient, especially if you have an established relationship. Their personalized service can also be a benefit if you have unique circumstances.

Banks (Traditional): Familiarity and Existing Relationships

Your current bank or credit card company might offer auto loans. If you have a long-standing relationship with a bank, they may be able to process your application more quickly due to your existing financial history with them. However, traditional bank applications can sometimes take a bit longer than online alternatives.

It’s always worth checking with your primary financial institution first. They might offer preferred rates or a smoother process for loyal customers.

Dealership Financing: Convenience at a Cost?

Many dealerships offer on-site financing, which can be incredibly convenient, especially if you need to drive away with a car today. They act as intermediaries, working with various lenders to find you a loan. This "one-stop shop" approach is appealing when time is of the essence.

However, common mistakes to avoid are accepting the first offer from a dealership without comparing it to pre-approved offers you’ve secured elsewhere. Dealerships may mark up interest rates to profit from the financing. Always arrive at the dealership with a pre-approved loan offer in hand to use as leverage.

Pillar 4: Pre-Qualification vs. Pre-Approval – Know the Difference for Speed

Understanding the distinction between pre-qualification and pre-approval is crucial when you need a car loan ASAP. Both can speed up the process, but in different ways.

Pre-Qualification: A Soft Look

Pre-qualification involves a "soft inquiry" on your credit report, which doesn’t affect your credit score. It’s a quick estimate of what loan amount and interest rate you might qualify for based on basic information you provide. It gives you a general idea of your borrowing power.

This step is excellent for comparing multiple lenders without commitment. It allows you to shop around confidently, knowing roughly what you can afford.

Pre-Approval: A Game Changer for Urgency

Pre-approval is a more thorough process that involves a "hard inquiry" on your credit report. This means a lender has reviewed your financial information and has conditionally approved you for a specific loan amount at a particular interest rate. A pre-approval letter is essentially a promise from a lender to give you a loan, provided certain conditions are met (like the car meeting their criteria).

Getting pre-approved before you step foot on a dealership lot is a powerful strategy for securing a car loan quickly. It turns you into a cash buyer, giving you significant negotiating power on the vehicle price itself. It also eliminates the financing step at the dealership, allowing you to focus solely on the car.

Pillar 5: The Application Process – Streamlining for Rapid Results

Once you’ve assessed your finances, gathered documents, and identified potential lenders, it’s time to apply. The way you approach the application itself can significantly impact how quickly you get approved.

Online Applications: Your Fastest Route

Utilize online application portals whenever possible. They are designed for efficiency and can often provide instant decisions or very rapid responses. Ensure you fill out every field accurately and completely. Any missing information will cause delays as the lender will need to contact you for clarification.

Pro tips from us: When applying with multiple lenders, do so within a short window (typically 14-45 days, depending on the credit scoring model). This allows credit bureaus to count multiple hard inquiries for the same type of loan as a single inquiry, minimizing the impact on your credit score.

Honesty and Accuracy: Avoiding Red Flags

Always be completely honest and accurate in your application. Inconsistencies or false information can lead to immediate rejection or, worse, accusations of fraud. Lenders will verify your information, and any discrepancies will only cause delays. Providing clear, verifiable information from the outset is key to a swift approval.

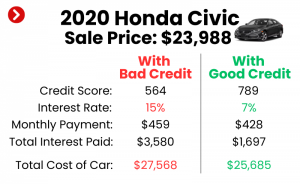

Pillar 6: What If You Have Bad Credit and Need a Car Loan ASAP?

Needing a car loan urgently with bad credit adds another layer of complexity, but it’s not an impossible situation. Many lenders specialize in subprime auto loans for individuals with less-than-perfect credit histories.

Subprime Lenders: Specialized Options

Subprime lenders are more willing to take on the risk associated with bad credit, though often at higher interest rates. They look beyond just your credit score, also considering your income, employment stability, and the amount of your down payment. These lenders can often provide rapid approvals because their processes are geared towards this specific market.

The Power of a Cosigner: A Helping Hand

If your credit score is a major hurdle, securing a cosigner with good credit can significantly improve your chances of rapid approval and potentially lower your interest rate. A cosigner agrees to be equally responsible for the loan if you default.

Based on my experience, finding a cosigner who understands the commitment and has a strong financial profile is crucial. This is a big ask, so approach this option with careful consideration and ensure both parties understand the implications.

Larger Down Payment: Reducing Lender Risk

For bad credit car loans, a larger down payment becomes even more critical. It directly reduces the lender’s risk and shows your financial commitment. If you can save up a more substantial down payment, it will greatly enhance your chances of getting an urgent car loan approved, even with a low credit score.

Pillar 7: Negotiating Your Loan Terms – Even When You’re in a Hurry

Even when you’re in a rush, it’s vital not to overlook the importance of negotiating your loan terms. The "ASAP" need shouldn’t mean you settle for unfavorable conditions. Focus on the Annual Percentage Rate (APR), the loan term, and the total cost of the loan.

Common mistakes to avoid are focusing solely on the monthly payment. A lower monthly payment might seem attractive but could be due to a longer loan term, meaning you pay significantly more in interest over time. Always ask for the total cost of the loan.

With a pre-approval in hand, you have leverage. You can use that offer to negotiate with the dealership’s finance department or even other lenders. Don’t be afraid to walk away if the terms are not competitive. Remember, you’re not just buying a car; you’re buying money to buy a car.

Post-Approval Steps: Getting on the Road

Once your loan is approved, the final steps are usually straightforward but still require attention to detail.

- Review the Loan Agreement: Read every line of the final loan agreement before signing. Ensure the interest rate, loan term, payment schedule, and any fees match what you were promised. Don’t be afraid to ask questions.

- Finalize the Purchase: With your financing secured, you can proceed with the vehicle purchase. Ensure all vehicle details (VIN, mileage, price) are accurate on the bill of sale.

- Insurance: You will need to have proof of auto insurance before you can drive the car off the lot. Have your insurance details or a binder ready.

- Understand Payment Schedules: Know your first payment date and how to make payments. Setting up automatic payments can help you avoid missing deadlines and further build your credit history.

Actionable Checklist for Your "ASAP" Car Loan

To make your urgent car loan journey as smooth as possible, follow this concise checklist:

- Check Your Credit Score & Report: Identify areas for improvement and correct errors.

- Gather All Documents: ID, proof of income, residence, insurance, bank info.

- Determine Your Budget: Know what you can realistically afford for a monthly payment and total loan cost.

- Consider a Down Payment: Even a small one can help.

- Explore Lenders: Start with online lenders for speed, then credit unions/banks.

- Get Pre-Approved: This is your strongest tool for speed and negotiation.

- Compare Offers: Look beyond monthly payments; focus on APR and total cost.

- Negotiate Wisely: Don’t let urgency compromise good terms.

- Read Before You Sign: Understand every detail of your loan agreement.

For a deeper dive into improving your credit score, check out our guide on . If you’re weighing the pros and cons of new vs. used, read our comprehensive article: .

Frequently Asked Questions About Urgent Car Loans

Q: Can I get a car loan with no money down quickly?

A: Yes, it’s possible, especially with excellent credit. However, a down payment generally improves your chances of fast approval and better terms, even for urgent loans. It also reduces your overall loan amount and interest paid.

Q: How long does "ASAP" really take for a car loan?

A: For prepared applicants with good credit, pre-qualification can be instant, and pre-approval can happen within hours to 24-48 hours. If all documents are ready, you could potentially drive away with a car in as little as one business day.

Q: What if I get rejected for an urgent car loan?

A: Don’t panic. Ask the lender why you were rejected. This feedback is invaluable. It might be due to a low credit score, high DTI, or insufficient income. You can then address these issues, consider a cosigner, a larger down payment, or explore lenders specializing in bad credit. For more general financial guidance, you can visit the Consumer Financial Protection Bureau (CFPB) website at consumerfinance.gov.

Conclusion: Drive Away with Confidence

Needing a car loan ASAP can be a stressful situation, but with the right strategy, it doesn’t have to be a nightmare. By understanding the key factors lenders consider, diligently preparing your documents, exploring the right loan options, and leveraging pre-approval, you can significantly streamline the process. Remember, even under pressure, informed decisions lead to better outcomes.

Take a deep breath, follow the steps outlined in this guide, and empower yourself to secure the fast car financing you need. With careful planning and proactive steps, you’ll be behind the wheel of your new vehicle sooner than you think, with a loan that fits your financial situation. Start your preparation today, and you’ll be well on your way to getting that car loan ASAP.