I Need A Car Loan With Bad Credit: Your Ultimate Guide to Approval and Affordable Driving

I Need A Car Loan With Bad Credit: Your Ultimate Guide to Approval and Affordable Driving Carloan.Guidemechanic.com

Hearing yourself say, "I need a car loan with bad credit," can feel like hitting a brick wall. It’s a common and often frustrating situation, leaving many wondering if securing reliable transportation is even possible. The good news? It absolutely is. While navigating the world of auto financing with a less-than-perfect credit score presents unique challenges, it’s far from an insurmountable obstacle.

This comprehensive guide is designed to empower you with the knowledge, strategies, and confidence needed to secure a car loan, even when your credit history isn’t sparkling. We’ll dive deep into understanding your situation, preparing for the application process, finding the right lenders, and making smart financial decisions that will benefit you for years to come. Let’s get you on the road!

I Need A Car Loan With Bad Credit: Your Ultimate Guide to Approval and Affordable Driving

Understanding "Bad Credit" in the Auto Loan World

Before we explore solutions, it’s vital to understand what "bad credit" means to a potential lender. Your credit score is a numerical representation of your creditworthiness, primarily based on your past payment behavior. Lenders use this score to assess the risk of lending money to you.

Generally, FICO scores range from 300 to 850. A score below 620-660 typically falls into the "subprime" or "bad credit" category. This isn’t just a number; it tells a story of late payments, defaults, bankruptcies, or high debt utilization. From a lender’s perspective, these indicate a higher risk of you defaulting on a new loan.

However, it’s crucial to remember that lenders are in the business of lending money. While they prefer low-risk borrowers, they also understand that life happens, and people need second chances. This is where specialized bad credit car financing options come into play. They acknowledge your past but look for indicators of your current ability and willingness to pay.

Dispelling Myths & Setting Realistic Expectations

When you’re searching for a car loan with bad credit, it’s easy to fall prey to misconceptions or unrealistic hopes. Based on my experience in the finance industry, setting clear expectations from the start is paramount to a successful outcome.

Myth 1: No One Will Lend to Me

Reality: This is simply untrue. While traditional banks might be hesitant, there’s a robust market of subprime auto lenders, credit unions, and dealerships specializing in helping individuals with bad credit. They understand the need for transportation and are structured to work with higher-risk profiles.

Myth 2: I’ll Get the Same Rates as Someone with Excellent Credit

Reality: Unfortunately, this is highly unlikely. Lenders compensate for the increased risk associated with bad credit by charging higher interest rates. This means your loan will cost more over its lifetime. Your goal isn’t necessarily the lowest rate overall, but the best rate available to you given your credit situation.

Myth 3: "Guaranteed Approval" Means a Great Deal

Reality: Be extremely cautious of any lender promising "guaranteed approval" without even looking at your financial situation. While some dealerships specialize in bad credit loans, "guaranteed" often comes with extremely high interest rates, unfavorable terms, or hidden fees. Always read the fine print and question anything that sounds too good to be true.

Pro tip from us: Focus on affordability and transparency. A legitimate lender will always assess your ability to repay, even with bad credit. Your primary goal is to find a loan you can comfortably afford, not just any loan.

Preparing for Your Bad Credit Car Loan Journey

Preparation is your most powerful tool when seeking car loan approval with poor credit. The more informed and organized you are, the stronger your position will be.

1. Know Your Credit Score & Report Inside Out

Before approaching any lender, pull your credit report from all three major bureaus: Experian, Equifax, and TransUnion. You can do this annually for free at AnnualCreditReport.com.

- Review for accuracy: Look for any errors, incorrect late payments, or accounts that aren’t yours. Disputing these can potentially boost your score.

- Understand your history: Identify the specific issues dragging your score down. This helps you explain your situation to lenders and shows you’re aware and proactive.

- See what lenders see: Your credit report provides a detailed history of your borrowing and repayment behavior. This transparency is crucial for your self-assessment.

2. Assess Your Financial Situation Thoroughly

Lenders care deeply about your ability to repay. Creating a realistic budget is non-negotiable.

- Calculate your income vs. expenses: What is your net monthly income? What are all your fixed and variable expenses? Be honest and thorough.

- Determine an affordable payment: Based on your budget, how much can you truly afford to pay each month for a car loan, insurance, and fuel? Don’t overextend yourself.

- Understand your debt-to-income (DTI) ratio: This is a key metric for lenders. It’s your total monthly debt payments divided by your gross monthly income. A lower DTI indicates you have more disposable income to manage new debt.

3. Save for a Significant Down Payment

This is arguably the single most impactful step you can take when seeking a car loan with bad credit. A substantial down payment offers multiple benefits:

- Reduces lender risk: By putting more money down, you reduce the amount the lender has to finance, lowering their risk.

- Lowers your loan amount: This means smaller monthly payments and less interest paid over the life of the loan.

- Shows commitment: A down payment demonstrates your financial responsibility and commitment to the loan.

- Offsets high interest rates: While your interest rate might still be higher, a lower principal balance means you’ll pay less in total interest. Aim for at least 10-20% of the car’s value, if possible.

4. Consider a Co-signer

If you have a trusted friend or family member with good credit, asking them to co-sign could significantly improve your chances of approval and potentially secure a better interest rate.

- Benefits: A co-signer’s strong credit history acts as a guarantee for the lender, mitigating their risk.

- Risks: Both you and the co-signer are equally responsible for the loan. If you miss payments, it impacts both your credit scores, and the co-signer is legally obligated to pay. This decision should never be taken lightly.

5. Gather All Necessary Documents

Being prepared with your paperwork streamlines the application process and shows lenders you’re serious.

- Proof of income: Recent pay stubs, bank statements, tax returns (if self-employed).

- Proof of residence: Utility bills, lease agreement.

- Proof of identity: Driver’s license, state ID.

- References: Sometimes required, especially for subprime loans.

Common mistakes to avoid are: applying without knowing your credit score, not budgeting realistically, and underestimating the power of a good down payment. These simple steps can make a huge difference in your success.

Where to Find Bad Credit Car Loans

Not all lenders are created equal, especially when it comes to bad credit car loan options. Knowing where to look will save you time and frustration.

1. Subprime Lenders and Special Finance Dealerships

These lenders specialize in working with individuals who have lower credit scores. Their business model is built around assessing higher risk.

- Their approach: They look beyond just your credit score, focusing on your current income, stability (job history, residence history), and ability to make a down payment.

- Dealerships with "special finance" teams: Many larger dealerships have dedicated departments or work with networks of subprime lenders to help customers with poor credit. They can often pre-qualify you with multiple lenders to find the best fit.

- Buy Here Pay Here (BHPH) lots: These dealerships are also lenders. You buy the car and make payments directly to them.

- Pros: Often very high approval rates, even with severely bad credit.

- Cons: Typically higher interest rates, limited car selection, and often no reporting to credit bureaus (meaning it won’t help rebuild your credit). Use BHPH as a last resort.

2. Credit Unions

Credit unions are member-owned financial institutions known for their more flexible lending criteria and often more competitive rates compared to traditional banks, even for those with bad credit.

- Member-focused: They prioritize their members’ financial well-being.

- Potential for better rates: Even if your credit isn’t perfect, your existing relationship with a credit union might give you an edge.

- How to apply: If you’re not already a member, consider joining one. Many have open membership requirements.

3. Online Loan Marketplaces

Websites that connect borrowers with multiple lenders can be incredibly efficient. You fill out one application, and they match you with lenders willing to work with your credit profile.

- Convenience: Apply from home and receive multiple offers.

- Comparison shopping: Easily compare terms, rates, and fees from different lenders.

- Streamlined process: These platforms often specialize in finding solutions for various credit situations, including subprime.

4. Traditional Banks (with caveats)

While major banks are generally stricter, if you have a long-standing relationship with your bank and can demonstrate significant financial improvement, it might be worth inquiring. However, don’t make this your primary focus with bad credit.

Pro tips from us: Start with online marketplaces or credit unions to get a sense of what’s available. Then, if you’re comfortable, explore special finance dealerships. Always get pre-qualified with a few lenders before stepping onto a car lot. This gives you leverage and a clear understanding of your budget.

The Application Process: What to Expect

Once you’ve identified potential lenders, the application process for an auto loan with bad credit generally involves a few key steps. Understanding these will help you navigate it smoothly.

1. The Application Form

You’ll provide detailed personal and financial information, including your employment history, income, residence history, and existing debts. Be prepared to be thorough and accurate.

2. Credit Checks

Lenders will perform a credit check, which will result in a "hard inquiry" on your credit report. While multiple hard inquiries within a short period (typically 14-45 days) for the same type of loan are often grouped as one for scoring purposes, it’s still wise to limit your applications to a few targeted lenders.

3. Beyond the Score: What Lenders Look At

Especially with bad credit, lenders assess more than just your FICO score. They look for:

- Stability: Consistent employment history, stable residence.

- Income: Sufficient disposable income to cover the loan payments.

- Debt-to-Income (DTI) ratio: As mentioned, a lower DTI is always better.

- Down payment: A significant down payment shows your commitment.

- References: Some subprime lenders may request personal or professional references.

Pro tip: Be honest and transparent about your financial history. Trying to hide issues will only prolong the process or lead to rejection. Explaining past challenges and demonstrating current stability can actually work in your favor.

Negotiating Your Bad Credit Car Loan

Securing approval is just the first step. The next crucial phase is negotiating the terms of your loan and the car purchase itself. This is where many people with bad credit make mistakes, often due to desperation.

1. Focus on the Total Cost, Not Just the Monthly Payment

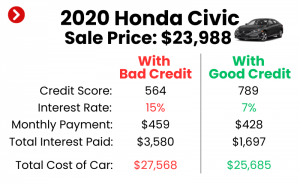

Dealerships often highlight only the monthly payment, which can be deceiving. A low monthly payment might mean a very long loan term (e.g., 72 or 84 months) and a high interest rate, leading to significantly more interest paid over time.

- Interest rates: This is your primary concern. Even a seemingly small difference in interest rates can save you hundreds or thousands of dollars.

- Loan term: Aim for the shortest term you can comfortably afford. This reduces the total interest paid and helps you build equity faster.

- Total cost: Always ask for the total amount you will pay over the life of the loan, including principal and interest.

2. Avoid Unnecessary Add-ons

Dealerships often try to sell extended warranties, GAP insurance, paint protection, and other services. While some, like GAP insurance, can be valuable (especially if you put little down and owe more than the car is worth), many are overpriced and can be purchased elsewhere for less, or are simply not needed.

- Question everything: Ask what each add-on costs and if it’s truly necessary.

- Know your rights: You are generally not required to purchase these add-ons to get the loan.

3. Don’t Settle for the First Offer

This is where your pre-approval from other lenders becomes invaluable. If you walk into a dealership with an existing loan offer, you have leverage.

- Shop around: Compare offers from different lenders and dealerships.

- "Based on my experience," many individuals with bad credit feel they have no choice but to accept the first offer. This is a costly mistake. Always negotiate.

- Separate negotiations: Try to negotiate the car price and the loan terms separately. Get a firm price on the vehicle before discussing financing.

Common mistakes to avoid are: Rushing into a decision, not reading the fine print of the loan agreement, letting emotions override financial logic, and focusing solely on the monthly payment. Remember, this is a significant financial commitment. Take your time.

Improving Your Credit for Future Opportunities

Securing a car loan with bad credit is a step forward, but it’s also an opportunity to start rebuilding your credit. This can lead to better financial opportunities down the road, including refinancing your current car loan at a lower rate.

1. Make All Payments On Time, Every Time

This is the single most important factor in improving your credit score. Payment history accounts for 35% of your FICO score. Even one late payment can set you back significantly.

2. Reduce Your Overall Debt

Focus on paying down high-interest credit card debt. A lower credit utilization ratio (amount of credit used vs. amount available) can positively impact your score.

3. Keep Old Accounts Open

The length of your credit history (15% of your FICO score) is important. Don’t close old, paid-off accounts, even if you don’t use them.

4. Avoid New Hard Inquiries Unless Necessary

Each time you apply for new credit, a hard inquiry appears on your report. While a few within a short period for a car loan are often grouped, excessive inquiries can temporarily lower your score.

5. Consider Secured Credit Cards or Credit Builder Loans

These tools are specifically designed to help people with bad credit rebuild their history. A secured credit card requires a deposit, which becomes your credit limit. A credit builder loan puts money into a savings account while you make payments, demonstrating your ability to pay.

For more in-depth strategies on credit repair, consider reading our article on How to Improve Your Credit Score Fast.

Life After Loan Approval: Responsible Ownership

Congratulations, you’ve secured your car loan! Now, the journey shifts to responsible ownership, which not only keeps you on the road but also helps you strengthen your financial standing.

1. Punctual Payments are Paramount

We cannot stress this enough. Your car loan can be a powerful tool for credit rebuilding. Consistent, on-time payments will gradually improve your credit score, opening doors to better rates on future loans and credit products. Set up automatic payments to avoid missing due dates.

2. Budget for All Car-Related Expenses

Your car loan payment is just one piece of the puzzle. Remember to budget for:

- Car insurance: Rates can be higher with bad credit.

- Fuel: A recurring cost that adds up.

- Maintenance: Oil changes, tire rotations, unexpected repairs. Don’t neglect these, as preventative maintenance saves money in the long run.

- Registration and taxes: Annual or biannual costs.

3. Explore Refinancing Opportunities

Once you’ve made 6-12 months of on-time payments and your credit score has shown improvement, you might be eligible to refinance your car loan at a lower interest rate.

- When to refinance: If your credit score has improved, interest rates have dropped, or you found a more competitive lender.

- Benefits: Lower monthly payments, less interest paid over the loan term, and financial relief.

- How to do it: Shop around with credit unions and online lenders. Be prepared to provide updated financial information.

Staying disciplined with your car loan payments can truly transform your financial outlook. It’s a tangible step towards proving your creditworthiness and securing a brighter financial future. For more insights into responsible vehicle ownership, you might find our guide on Maintaining Your Car on a Budget helpful.

Conclusion: Your Road to Approval is Clear

The statement, "I need a car loan with bad credit," is not a dead end. It’s a starting point for a journey that requires preparation, diligence, and informed decision-making. While the path may have a few more bumps than for someone with pristine credit, it is absolutely navigable.

By understanding your credit, preparing your finances, knowing where to find specialized lenders, and negotiating wisely, you can secure the car loan you need. Remember, this isn’t just about getting a car; it’s about taking control of your financial future and using this opportunity to rebuild your credit.

Don’t let past financial missteps define your present or future. Take the proactive steps outlined in this guide, and you’ll be well on your way to approval and enjoying the freedom of reliable transportation. Start preparing today, and empower yourself to drive towards a better tomorrow.

External Resource: For official information on your credit rights and managing debt, visit the Consumer Financial Protection Bureau (CFPB) website: ConsumerFinance.gov