I Want Out Of My Car Loan: Your Comprehensive Guide to Breaking Free

I Want Out Of My Car Loan: Your Comprehensive Guide to Breaking Free Carloan.Guidemechanic.com

The feeling is all too common. You signed on the dotted line, full of excitement for your new vehicle, but now, the thrill is gone. Perhaps your financial situation has shifted, your car no longer fits your lifestyle, or you simply have buyer’s remorse. Whatever the reason, you’re now thinking, "I want out of my car loan."

This sentiment can be incredibly stressful, but here’s the good news: you’re not alone, and there are almost always viable solutions. This isn’t a dead end; it’s a crossroads. As expert bloggers and professional SEO content writers, we understand the complexities of vehicle financing and the myriad reasons why people seek an escape. Our mission in this comprehensive guide is to empower you with the knowledge and actionable strategies to navigate your options, make informed decisions, and ultimately, find your way out of your car loan.

I Want Out Of My Car Loan: Your Comprehensive Guide to Breaking Free

We’ll delve deep into understanding your current situation, explore various exit strategies, highlight crucial considerations, and share pro tips gleaned from years of experience. By the end of this article, you’ll have a clear roadmap to address your "I want out of my car loan" dilemma effectively and responsibly.

Why Do People Want Out of Their Car Loan? Understanding the Common Scenarios

Before we dive into solutions, it’s helpful to acknowledge the root causes. Understanding why you want out can often guide you toward the most appropriate solution. Based on my experience, the reasons are diverse, often stemming from significant life changes or unexpected financial shifts.

One of the most frequent catalysts is financial hardship. A job loss, a reduction in income, unexpected medical bills, or other unforeseen expenses can quickly make a car payment that once felt manageable now feel like an insurmountable burden. Suddenly, every dollar counts, and that monthly car note becomes a source of anxiety.

Another common reason is simply that the car no longer meets your needs. Your family might have grown, requiring a larger vehicle, or perhaps your commute has changed, making your fuel-guzzling SUV impractical. Lifestyle changes, such as moving to a city with excellent public transport, can also render car ownership unnecessary or undesirable. This shift can lead to the realization that the vehicle you once loved is now a financial drain without providing adequate utility.

Negative equity is another significant driver of this desire to escape. This occurs when you owe more on your car loan than the car is currently worth. It’s a frustrating position to be in, making you feel trapped because selling the vehicle won’t cover the outstanding debt. This situation often arises from buying a new car that depreciates quickly, taking a long loan term, or rolling previous negative equity into the current loan.

Finally, plain old buyer’s remorse is a powerful motivator. You might have rushed into a purchase, fallen for high-pressure sales tactics, or simply realized the car isn’t what you truly wanted after all. This feeling of regret, coupled with a long-term financial commitment, can make you desperately wish for a way out.

Understanding Your Current Situation: The First Critical Step

Before exploring any solutions, you absolutely must have a clear picture of your financial standing and your car’s value. This initial assessment is non-negotiable and forms the bedrock of any successful strategy. Common mistakes to avoid include guessing these figures or, worse, ignoring them completely.

First, know your exact car loan payoff amount. This isn’t just your current balance; it’s the total amount required to fully satisfy the loan today, including any accrued interest or fees. Contact your lender directly and request a "10-day payoff quote." This figure is crucial for every option we’ll discuss.

Second, determine your car’s current market value. This involves getting realistic estimates for both trade-in value and private sale value. Websites like Kelley Blue Book (KBB.com), Edmunds, and NADAguides are excellent resources for this. Be honest about your car’s condition, mileage, and features to get the most accurate appraisal. Pro tips from us: get multiple valuations from different sources, and consider an in-person appraisal from a dealership if you’re serious about selling or trading in.

Third, calculate your equity. This is the difference between your car’s market value and your loan payoff amount.

- Positive equity: Your car is worth more than you owe. This is the ideal scenario, as you’ll have money left over after paying off the loan.

- Negative equity (also known as "being upside down"): You owe more than your car is worth. This is a common and challenging situation that requires careful planning.

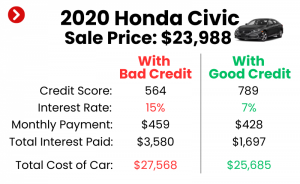

Finally, check your credit score. Your credit score will play a significant role if you plan to refinance, secure a personal loan, or lease a new vehicle. A higher score generally translates to better interest rates and more favorable terms. You can get free credit reports and scores from sites like AnnualCreditReport.com or through many credit card providers.

Strategies to Get Out of Your Car Loan: Your Roadmap to Freedom

Once you have a firm grasp of your current financial and equity position, you can start exploring viable strategies to address your "I want out of my car loan" predicament. Each option has its own set of pros, cons, and specific circumstances under which it makes the most sense.

1. Refinancing Your Car Loan

Refinancing means replacing your current car loan with a new one, often with different terms. This is a popular option when you want to lower your monthly payments, reduce your interest rate, or shorten your loan term.

When it’s a good option:

- Interest rates have dropped: If current rates are lower than your original loan’s rate, you could save a substantial amount over time.

- Your credit score has improved: A better credit score since you took out the initial loan makes you eligible for more favorable terms.

- You want to lower your monthly payment: Extending the loan term can reduce your monthly outlay, though it might increase the total interest paid over the life of the loan.

- You want to pay off the loan faster: Shortening the loan term can help you become debt-free sooner, though it will increase your monthly payment.

How it works: You apply for a new loan with a different lender (or sometimes your existing one). If approved, the new loan pays off your old loan, and you begin making payments to the new lender under the new terms. This process can often be completed online and is relatively straightforward.

Pros:

- Can significantly lower your monthly payment.

- Can reduce the total interest paid over the loan’s life.

- Potentially frees up cash flow.

- Doesn’t require selling your car.

Cons:

- Might extend your loan term, leading to more interest paid overall.

- Not an option if you have significant negative equity or a very low credit score.

- Application fees or closing costs may apply.

Pro tips from us: Shop around aggressively. Don’t just go with the first offer. Check credit unions, online lenders, and traditional banks. Compare interest rates, loan terms, and any associated fees. Even a slight reduction in your interest rate can save you hundreds, if not thousands, of dollars over the life of the loan. Also, ensure there are no prepayment penalties on your current loan that would negate the benefits of refinancing.

Common mistakes to avoid: Refinancing simply to extend the loan term without securing a better interest rate. While it lowers monthly payments, it can lead to paying much more in interest over time and can prolong negative equity. Also, don’t forget to factor in any fees associated with the new loan.

2. Selling Your Car Privately

Selling your car to a private party can often yield a higher price than trading it into a dealership, especially if you have positive equity or can cover a small amount of negative equity. This is a direct approach to getting out of your car loan entirely.

When it’s viable:

- You have positive equity: This means the sale price will cover your loan payoff, leaving you with cash in hand.

- You have minor negative equity and can cover the difference: If you can pay the gap between the sale price and your loan amount out of pocket, this is a strong option.

- You’re willing to put in the effort: Private sales require time for marketing, showing the car, and handling paperwork.

Process:

- Get your car professionally detailed: A clean car sells faster and for more money.

- Take high-quality photos: Showcase your car from multiple angles.

- Determine a competitive asking price: Use market value guides and comparable listings.

- List your car: Utilize online marketplaces (e.g., Craigslist, Facebook Marketplace, AutoTrader).

- Manage inquiries and show the car: Be prepared for questions and test drives.

- Handle the payoff and title transfer: This is the most critical step when there’s a lien. The buyer’s funds will go directly to your lender to pay off the loan, and then the lender will release the title, which you can then sign over to the buyer. Sometimes, a three-way transaction at the bank is best to ensure all parties are protected.

Pros:

- Potentially the highest sale price compared to trade-in.

- Complete freedom from the car loan.

- You control the selling process.

Cons:

- Requires significant time and effort.

- Dealing with potential buyers can be challenging.

- Navigating the lien payoff and title transfer process can be complex.

- You’ll need alternative transportation after the sale.

Based on my experience: Be transparent with potential buyers about the lien. Explain the process clearly. Many buyers are wary of purchasing a car with a lien, so having a plan to facilitate a smooth transaction at your bank or credit union can build trust. If you have negative equity, you must be prepared to pay that difference at the time of sale.

3. Trading In Your Car

Trading in your vehicle to a dealership is a convenient option, especially if you plan to purchase another car immediately. The dealership handles the payoff of your existing loan and deducts the trade-in value from the price of your new car.

When it’s viable:

- You’re buying another vehicle: This is the primary reason for a trade-in.

- You prefer convenience over maximum profit: Dealerships streamline the process.

- You have positive equity: This will reduce the cost of your new vehicle.

- You have negative equity and are prepared to roll it into a new loan: This is a common, but potentially risky, scenario.

How negative equity is rolled into a new loan: If your trade-in value is less than your loan payoff, the dealership will add that difference to the purchase price of your new car. For example, if you owe $15,000, your car is worth $12,000, and you buy a new car for $25,000, your new loan will be for $25,000 + $3,000 (negative equity) = $28,000 (plus taxes and fees).

Pros:

- Extremely convenient; the dealership handles all paperwork and loan payoff.

- Can simplify the process of getting a new car.

- Potential tax savings in some states (you only pay sales tax on the difference between the new car’s price and your trade-in value).

Cons:

- Typically yields a lower value for your car than a private sale.

- Rolling negative equity into a new loan can put you further underwater and extend your debt.

- Can obscure the true cost of your new vehicle if you don’t negotiate properly.

Common mistakes to avoid: Focusing solely on the monthly payment of the new car without understanding how much negative equity you’re rolling over. Always negotiate the trade-in value and the new car’s price separately. Don’t let the dealership combine these figures into one "monthly payment" discussion until you’ve agreed on the individual components.

Pro tips from us: Get pre-approved for a loan on the new car before you go to the dealership. This gives you leverage. Also, get multiple trade-in offers from different dealerships. Don’t be afraid to walk away if the numbers don’t make sense.

4. Voluntary Repossession (A Last Resort)

Voluntary repossession involves returning your car to the lender because you can no longer afford the payments. This is a severe step with significant long-term consequences and should almost always be avoided.

What it is: You contact your lender and arrange to surrender the vehicle. While it seems like a way to avoid the stress of collections, it doesn’t absolve you of the debt.

Impact on credit: A voluntary repossession will severely damage your credit score, remaining on your credit report for up to seven years. This makes it incredibly difficult to obtain future loans (car, mortgage, personal) at reasonable rates.

Still owing money (deficiency balance): After the car is repossessed, the lender will sell it at auction, usually for much less than its market value. The difference between the sale price and your outstanding loan balance (plus repossession and auction fees) is called the "deficiency balance." You will still be legally obligated to pay this amount, and the lender can pursue you for it, even taking you to court.

Why it should almost always be avoided: The financial and credit ramifications are devastating. It’s often better to explore every other option, including selling the car privately (even if you have to pay the negative equity), refinancing, or even exploring bankruptcy if your financial situation is truly dire.

5. Loan Assumption (Rare)

In very rare cases, some car loans allow for assumption, meaning another qualified individual can take over your existing loan. This is highly uncommon for standard auto loans but might be an option for certain types of loans or with specific lenders. It requires the new borrower to meet the lender’s credit criteria.

6. Early Payoff

If your financial situation has improved significantly and you have the funds, paying off your car loan early is a fantastic way to get out of debt quickly.

Benefits:

- Saves you money on interest.

- Frees up monthly cash flow.

- Removes the debt from your credit report sooner.

Check for prepayment penalties: Some loan agreements include penalties for paying off the loan before its scheduled term. Always review your loan documents or contact your lender to confirm if such penalties apply. Most modern auto loans do not have these, but it’s essential to verify.

Dealing with Negative Equity: The Elephant in the Room

Negative equity is perhaps the biggest hurdle for those who say, "I want out of my car loan." It means you owe more than your car is worth, and it often feels like being trapped. But even with negative equity, you have options beyond voluntary repossession.

What it is and why it happens: As mentioned, it’s the gap between your loan balance and your car’s market value. It often results from rapid depreciation (especially with new cars), making a small down payment, taking a very long loan term, or rolling previous negative equity into the current loan.

Strategies for managing negative equity:

- Pay the difference out of pocket: If you sell your car privately or trade it in, and you have negative equity, the simplest solution is to pay the difference yourself. This requires having the cash available, but it’s the cleanest break from the old loan.

- Roll it into a new loan (with caution): When trading in, dealerships will often offer to roll your negative equity into the financing for your new car. While this sounds convenient, it means you’re starting a new loan already "upside down." This increases your new loan amount, leading to higher payments and a longer time to build positive equity. Only consider this if the new car is absolutely necessary, and you can afford the increased payment comfortably.

- Personal loan: In some cases, you might be able to secure a personal loan to cover the negative equity difference if you’re selling your car. This effectively converts your secured auto loan debt into an unsecured personal loan. Evaluate the interest rates carefully, as personal loans often have higher rates than auto loans.

- Wait it out: If your financial situation allows, sometimes the best strategy is to continue making payments until you build up positive equity. Over time, your car depreciates less rapidly, and your loan balance decreases, eventually putting you in a better position. This requires patience and discipline.

Based on my experience: Don’t ignore negative equity. It won’t disappear on its own. Actively working to address it, whether by paying it down or strategically managing it, is crucial for your financial well-being. Avoiding it often leads to a cycle of being perpetually upside down on vehicle loans.

Crucial Considerations Before Making a Move

Before you finalize any decision to get out of your car loan, take a moment to consider these vital factors. Rushing into a choice without thorough consideration can lead to new problems.

- Impact on your credit score: Every action, from refinancing to voluntary repossession, will affect your credit. Understand whether the impact will be positive (e.g., lower debt load) or negative (e.g., missed payments, repossession). Your credit score is a long-term asset.

- Financial implications: Calculate the total cost of each option. Does it genuinely save you money in the long run, or are you just shifting debt around? Consider interest rates, fees, potential taxes, and the total amount you’ll pay.

- Future transportation needs: What will you drive after getting out of this loan? Do you have alternative transportation, or will you need to buy another vehicle? Factor in the costs and logistics of your next mode of transport.

- Reading your loan agreement carefully: Your existing loan contract is a critical document. It outlines prepayment penalties, late fees, and specific terms regarding payoff. Always refer to it or contact your lender directly for clarification.

- Consulting a financial advisor: For complex situations, especially involving significant negative equity or other debts, a certified financial advisor can provide personalized guidance tailored to your unique circumstances. This can be an invaluable step.

Pro Tips from Us: Navigating the Process

Having guided many through similar situations, we’ve gathered some invaluable pro tips to help you effectively address your "I want out of my car loan" dilemma:

- Do your research thoroughly: Knowledge is power. Understand your car’s value, your loan terms, and all available options before making any commitments. Don’t rely solely on what a dealership or lender tells you.

- Negotiate everything: Whether you’re refinancing, selling, or trading in, always negotiate. Don’t accept the first offer. There’s often room for improvement.

- Understand all fees: Be aware of any application fees, closing costs, early payoff penalties, or dealership documentation fees. These can add up and affect the true cost of your chosen solution.

- Don’t rush into decisions: This is a significant financial move. Take your time, weigh all your options, and avoid making impulsive choices driven by frustration or pressure.

- Seek professional advice when needed: For complicated scenarios, especially if you’re dealing with substantial negative equity or broader financial difficulties, consulting a financial advisor or credit counselor can provide clarity and expert guidance.

Common Mistakes to Avoid

As an expert, I’ve seen these pitfalls trap many people. Steering clear of them is as important as knowing your options.

- Ignoring the problem: Hoping your car loan will magically resolve itself is a recipe for disaster. Late payments accrue fees, damage your credit, and make finding solutions harder. Address the issue head-on as soon as you feel that "I want out of my car loan" anxiety.

- Not knowing your car’s true value: Going into a negotiation without an accurate understanding of your car’s worth puts you at a severe disadvantage. Dealerships will always try to buy low and sell high.

- Rolling negative equity without understanding the full impact: While convenient, this can bury you deeper in debt. Always calculate the total additional cost and how it impacts your new monthly payment and loan term.

- Falling for predatory refinancing offers: Be wary of lenders offering extremely long terms (e.g., 84+ months) or high-interest rates, especially if your credit isn’t stellar. Always compare the Annual Percentage Rate (APR) and total cost.

- Considering voluntary repossession without exploring all other options: As discussed, this is a nuclear option that will severely impact your financial future. Exhaust every single alternative before even considering this path.

Conclusion: Your Path to Freedom Starts Now

The feeling of being trapped by a car loan can be overwhelming, but as this comprehensive guide illustrates, you have a range of options available. Whether you’re looking to lower your payments, get rid of a vehicle that no longer suits you, or simply escape a bad financial decision, there’s a path forward.

Remember, the journey begins with understanding your current situation: knowing your loan payoff, your car’s market value, and your equity position. From there, you can explore refinancing, private sales, trade-ins, and other strategies, always keeping an eye on the impact on your credit and your overall financial health.

Don’t let the thought, "I want out of my car loan," fester into deeper financial distress. Take proactive steps, arm yourself with knowledge, and make an informed decision. Your financial freedom is within reach. Start by assessing your situation today, and take the first confident step towards breaking free.