Is a 15-Year Car Loan Right for You? Unpacking the Pros, Cons, and Hidden Costs of Extended Auto Financing

Is a 15-Year Car Loan Right for You? Unpacking the Pros, Cons, and Hidden Costs of Extended Auto Financing Carloan.Guidemechanic.com

The allure of a new car is undeniable, a gleaming promise of freedom and convenience. As vehicles become more technologically advanced and, consequently, more expensive, the idea of owning one can feel out of reach for many. This is where extended car financing options, like the increasingly discussed 15-year car loan, enter the conversation. Promising incredibly low monthly payments, these long-term auto loans seem to offer an accessible path to car ownership.

However, beneath the surface of apparent affordability lies a complex financial landscape. As an expert blogger and professional SEO content writer, my mission is to peel back the layers and provide you with a super comprehensive, in-depth look at 15-year car loans. This article will equip you with the knowledge to make an informed decision, examining everything from the initial appeal to the significant long-term financial implications. We’ll explore the pros, the considerable cons, and crucial factors to consider, ensuring you understand the true cost of such an extended commitment.

Is a 15-Year Car Loan Right for You? Unpacking the Pros, Cons, and Hidden Costs of Extended Auto Financing

Understanding the 15-Year Car Loan Landscape

A 15-year car loan, often referred to as a 180-month auto loan, is an extended vehicle financing agreement designed to stretch your payments over a significantly longer period than traditional options. While 5-year (60-month) and 7-year (84-month) loans are common, a 15-year term takes this concept to an extreme. This extended duration is typically offered to make high-value vehicles, such as luxury cars, high-end SUVs, or even RVs, appear more affordable on a month-to-month basis.

Lenders are increasingly offering these ultra long-term car loans to broaden their customer base and attract buyers who might otherwise be priced out of the market. By reducing the monthly payment, they create an illusion of affordability, making a larger loan amount seem manageable within a tight budget. However, this seemingly attractive offer often comes with substantial hidden costs that borrowers must fully understand.

Based on my experience, individuals considering such an extended auto loan are typically those who prioritize the lowest possible monthly payment above all else. They might be looking to acquire a more expensive vehicle than their budget would traditionally allow, or they may have other significant financial obligations that limit their immediate cash flow. While the immediate relief of a small monthly payment is tempting, it’s crucial to look beyond the superficial numbers and evaluate the entire financial commitment.

The Allure of Lower Monthly Payments: The Primary Benefit

The most significant and often the only perceived benefit of a 15-year car loan is the dramatically reduced monthly payment. By spreading the total cost of the vehicle over 180 months, the amount you pay each month can be substantially lower compared to a standard 5 or 7-year loan. This reduction can make luxury vehicles or higher-priced models seem within reach for a wider range of budgets.

For some, this lower monthly obligation might free up cash flow for other essential expenses or savings goals in the short term. It can provide a sense of budgeting flexibility, allowing them to manage their finances without feeling overwhelmed by a hefty car payment. This is often the primary driver for individuals opting for such extended car loan terms, as it provides immediate relief to their monthly financial commitments.

Moreover, if you have a specific, high-value vehicle in mind that you genuinely need or desire, and your budget is extremely constrained, a 15-year car loan might appear to be the only viable path to ownership. It allows access to more expensive vehicles that would otherwise be completely unattainable with shorter financing periods. However, this immediate gratification comes at a significant long-term cost, which we will explore in detail.

The Significant Drawbacks and Hidden Costs

While the lower monthly payment is enticing, the disadvantages of a 15-year car loan are numerous and often far outweigh the perceived benefits. Understanding these drawbacks is critical to making a truly informed financial decision.

A. Astronomical Total Interest Paid

This is arguably the most significant financial pitfall of extended car financing. While your monthly payment is low, the sheer length of a 180-month loan means you will pay a staggering amount of interest over the life of the loan. Even a seemingly small interest rate will compound significantly over 15 years, leading to a total cost of ownership that is dramatically higher than with a shorter term.

For example, a car costing $30,000 at a 6% interest rate over 5 years would result in roughly $4,700 in total interest. The same car and interest rate over 15 years could see you paying well over $15,000 in interest – more than triple the amount. This means you’re paying thousands, if not tens of thousands, more for the exact same vehicle simply by extending the loan term. Pro tips from us: Always focus on the "total cost" of the loan, not just the monthly payment.

B. Rapid Depreciation vs. Loan Balance

Vehicles begin to depreciate the moment they are driven off the lot, losing a significant portion of their value within the first few years. With a 15-year car loan, your car will depreciate much faster than you pay down the principal balance. This creates a high risk of being "upside down" or "underwater" on your loan, meaning you owe more on the car than it is worth.

Being upside down has serious implications. If you need to sell or trade in your car early, you’ll likely find yourself in a position where the sale price doesn’t cover your remaining loan balance. You would then have to pay the difference out of pocket or roll the negative equity into a new loan, further exacerbating your financial burden. Common mistakes to avoid are underestimating the impact of depreciation and assuming you can easily sell or trade in your car in a few years.

C. Increased Risk of Mechanical Failure and Maintenance Costs

A 15-year loan implies you will own and be responsible for the car for a very long time. Most manufacturer warranties expire long before a 15-year term is up, typically after 3-5 years. This means that for the vast majority of your loan term, you will be solely responsible for all maintenance, repairs, and unexpected breakdowns.

As a car ages, the likelihood of mechanical failures increases, and so do the costs associated with keeping it running. You could be making payments on a vehicle that constantly requires expensive repairs, draining your financial resources even further. The idea of making car payments on a car that spends more time in the shop than on the road is a real and often overlooked risk.

D. Limited Flexibility and Future Financial Burden

Committing to a 15-year car loan ties up a significant portion of your monthly budget for an extremely long duration. This long-term obligation severely limits your financial flexibility. It can make it difficult to save for other important life goals, such as a down payment on a house, retirement, or your children’s education.

Imagine being burdened with a car payment when you’re trying to start a family, change careers, or face unexpected financial challenges. This extended commitment can hinder your ability to adapt to life changes and pursue new opportunities. Based on my experience, many people regret long-term loans when their life circumstances inevitably change.

E. Higher Interest Rates (Often)

While not always the case, lenders typically charge higher interest rates for longer loan terms. This is because a longer loan period represents a greater risk for the lender. The longer the loan, the more variables can affect your ability to repay, such as job loss, economic downturns, or the car becoming a total loss.

Even a slight increase in the interest rate, when compounded over 15 years, can add thousands of dollars to the total cost of the loan. It’s crucial to compare the Annual Percentage Rate (APR) across different loan terms, not just the monthly payment, to understand the true cost.

When Might a 15-Year Car Loan Potentially Make Sense? (Rare Scenarios)

In almost all standard situations, a 15-year car loan is not advisable due to the astronomical interest paid and the risks involved. However, there are extremely niche and rare scenarios where it might be considered, though even then, caution is paramount.

One highly specific instance could be for a very high-value, collectible, or vintage vehicle that is expected to appreciate in value over time, or at least hold its value exceptionally well. In such a scenario, the car is viewed more as an investment rather than just transportation. Even then, alternative financing options like personal loans or specialized asset-backed loans might be more suitable.

Another incredibly risky scenario might be using a 15-year loan as a very temporary bridge, with an aggressive and concrete plan to refinance into a much shorter term within a year or two, once your financial situation improves. This strategy requires immense financial discipline and a guaranteed income increase or windfall. Pro tips from us: This approach is fraught with peril and should only be considered by those with a robust financial plan and emergency fund. For the vast majority of car buyers, these scenarios are exceptions that prove the rule: avoid 15-year car loans.

Crucial Factors to Consider Before Committing

Before you even consider signing on the dotted line for a 15-year car loan, several critical factors demand your thorough evaluation. Overlooking any of these could lead to severe financial distress down the road.

A. Your Credit Score

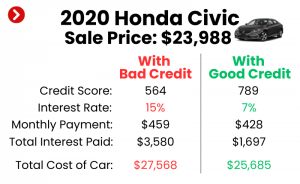

Your credit score is a fundamental determinant of the interest rate you’ll be offered. A higher credit score signals lower risk to lenders, potentially qualifying you for the best available rates. With a 15-year car loan, where interest costs are already sky-high, even a slightly higher interest rate due to a mediocre credit score can add thousands more to your total cost. Ensure your credit is in the best possible shape before applying for any long-term vehicle financing.

B. Down Payment

A substantial down payment is crucial, especially with extended car loans. A larger down payment reduces the principal amount you need to borrow, which in turn lowers your monthly payments and, more importantly, the total interest paid over the loan’s lifetime. Furthermore, a significant down payment helps to mitigate the risk of being upside down on your loan, as it immediately reduces the gap between the car’s value and your loan balance. Aim for at least 20% if considering any car loan, and even more for a 15-year term.

C. Car’s Reliability and Resale Value

If you’re committing to owning a car for 15 years, its long-term reliability is paramount. Research models known for their durability and low maintenance costs. A car that constantly breaks down will not only be a financial drain but also a source of immense frustration. Similarly, while depreciation is inevitable, some cars hold their value better than others. Choose a vehicle with a solid reputation for longevity and a decent resale value, should you ever need to sell it before the loan term is up. You can check trusted sources like Kelley Blue Book (KBB.com) for insights into resale value and Consumer Reports for reliability ratings.

D. Your Financial Stability and Future Plans

Honestly assess your current and projected financial stability. Do you have a secure job? Is your income likely to remain stable or increase over the next 15 years? What are your future life plans? Are you considering a family, buying a house, or changing careers? A 15-year car loan can be a rigid financial commitment that might conflict with significant life events. Pro tips from us: Project your finances 5-10 years out to understand the long-term impact of such a loan.

E. Insurance Costs

Lenders typically require comprehensive collision and liability insurance on financed vehicles to protect their investment. For a 15-year loan, you will be paying for this comprehensive coverage for a very long time, adding significantly to your total cost of ownership. As the car ages, while its market value decreases, you’ll still be required to maintain often expensive coverage for a vehicle that might be worth far less than your remaining loan balance.

F. The "Opportunity Cost"

Consider what else that money could be doing. The thousands of dollars you’ll pay in extra interest on a 15-year car loan could instead be invested, saved, or used to pay down higher-interest debt. This concept, known as "opportunity cost," highlights the lost potential of your money. By choosing to finance a car over an excessively long period, you are sacrificing potential wealth growth elsewhere.

Alternatives to a 15-Year Car Loan (Pro Tips from Us)

Given the significant drawbacks, it’s almost always advisable to explore alternatives to a 15-year car loan. Here are some much more financially sound options:

A. Shorter Term Loans

Opting for a 3, 5, or 7-year car loan will result in higher monthly payments, but the total interest paid will be dramatically lower. This is the most straightforward and financially responsible alternative. If the monthly payments for a shorter term seem too high, it’s a clear indicator that you might be looking at a car that is beyond your affordable price range. (For a deeper dive into different loan terms, consider reading our article on "Understanding Different Car Loan Terms: 3-Year vs. 5-Year vs. 7-Year").

B. Buying a Used Car

One of the smartest financial moves you can make is to buy a reliable used car. Let someone else absorb the massive initial depreciation hit. A well-maintained used car can provide excellent value and significantly reduce the total amount you need to finance. This allows for shorter loan terms and much lower overall costs.

C. Saving Up for a Larger Down Payment

If a new car is a must, commit to saving a larger down payment. The more you put down upfront, the less you need to borrow, which directly translates to lower monthly payments and less interest over the life of the loan. This financial discipline will pay dividends in the long run.

D. Budgeting and Reducing Car Expectations

Perhaps the car you desire is simply too expensive for your current financial situation. Re-evaluate your needs versus your wants. Can you comfortably afford a less expensive model, a different trim level, or a slightly older used vehicle? Adjusting your expectations to fit a realistic budget is a sign of financial maturity.

E. Refinancing (Strategically)

If you already have a long-term car loan and your financial situation has improved (e.g., better credit score, higher income), strategically refinancing into a shorter term can save you a significant amount in interest. Common mistakes to avoid are refinancing without a substantial reduction in the loan term or interest rate, which often just extends the pain. Make sure the new loan genuinely benefits you.

F. Leasing

For those who love driving new cars every few years and don’t drive excessive miles, leasing might be a better option than a long-term purchase. With a lease, you essentially pay for the depreciation of the vehicle during the lease term, typically 2-4 years. While you don’t own the car, it can offer lower monthly payments than purchasing and allows you to drive a new vehicle more frequently without the burden of long-term ownership.

Making an Informed Decision: A Step-by-Step Guide

Deciding on vehicle financing, especially for a significant term like 15 years, requires careful thought and a structured approach.

- Calculate Everything: Don’t just look at the monthly payment. Use an online loan calculator to determine the total amount of interest you will pay over the entire 15-year term. Compare this total cost to shorter loan terms to grasp the true financial impact.

- Compare Loan Offers: Shop around. Get quotes from multiple lenders – banks, credit unions, and online auto loan providers. Don’t just accept the first offer, and always scrutinize the APR, not just the monthly payment.

- Assess Your "Worst Case" Scenario: What if you lose your job, face an unexpected expense, or need to sell the car early? How would being upside down on a 15-year loan impact your financial recovery? Planning for contingencies is a hallmark of smart financial planning.

- Seek Financial Advice: If you’re unsure, consult a trusted financial advisor. They can help you assess your overall financial picture and determine if a long-term car loan aligns with your broader financial goals. (For tips on improving your financial standing, you might find our article "Boosting Your Credit Score for Better Loan Rates" helpful).

- Read the Fine Print: Thoroughly understand all terms and conditions of any loan agreement. Look for prepayment penalties, late fees, and any other clauses that could impact you. Never sign a document you haven’t fully read and comprehended.

Conclusion

The appeal of a 15-year car loan, with its incredibly low monthly payments, is understandable in today’s expensive vehicle market. It presents an immediate solution to the desire for a new car without a burdensome upfront cost. However, as we’ve explored in depth, this apparent affordability comes at a significant and often prohibitive price. The astronomical total interest paid, the high risk of being upside down on your loan, increased maintenance costs over an extended ownership period, and the long-term financial inflexibility make 15-year auto loans a financially risky proposition for most individuals.

Based on my experience as a financial content specialist, prioritizing short-term payment relief over long-term financial health is a common pitfall. While such loans might exist for niche situations, the overwhelming consensus is that they are generally not a wise financial decision for the average car buyer.

Before committing to such a prolonged financial obligation, I strongly encourage you to prioritize smart auto financing strategies. Research alternatives, save for a larger down payment, consider a reliable used car, and always choose a loan term that minimizes your total interest paid. Your financial well-being is paramount. Make an informed decision that aligns with your long-term goals, ensuring your car ownership journey is a source of joy, not financial stress.