Is A 7-Year Car Loan Bad? A Deep Dive into the 84-Month Auto Financing Dilemma

Is A 7-Year Car Loan Bad? A Deep Dive into the 84-Month Auto Financing Dilemma Carloan.Guidemechanic.com

The dream of a new car often comes with the reality of financing. In today’s competitive automotive market, one option that frequently pops up is the 7-year car loan, also known as an 84-month auto loan. On the surface, it promises lower monthly payments, making that shiny new (or newer used) vehicle seem much more attainable. But is this extended repayment period a smart financial move, or a subtle trap designed to cost you more in the long run?

As an expert in financial literacy and automotive trends, I’ve seen countless individuals navigate the complexities of car financing. Based on my experience, the question "Is a 7-year car loan bad?" isn’t a simple yes or no. It’s a nuanced discussion with significant implications for your financial health. This comprehensive guide will break down the pros, cons, hidden costs, and crucial considerations surrounding extended car loans, empowering you to make an informed decision.

Is A 7-Year Car Loan Bad? A Deep Dive into the 84-Month Auto Financing Dilemma

Understanding the Allure: Why 7-Year Car Loans Seem So Attractive

It’s easy to see why 84-month car loans have grown in popularity. The primary appeal lies in one simple, powerful benefit: significantly lower monthly payments. When you stretch out the repayment period over seven years instead of the traditional three, four, or five, your monthly financial obligation shrinks.

This reduction in monthly outflow can be incredibly enticing. For many, it’s the only way to fit a desired vehicle into their budget, especially as car prices continue to climb. An extended car loan can make a more expensive car, or one with more features, feel affordable by easing the immediate strain on your cash flow.

Furthermore, in an economic landscape where every dollar counts, a lower monthly payment offers a sense of financial flexibility. It leaves more money available for other expenses, savings, or unexpected costs. This perceived affordability is a powerful psychological draw, but it often masks the true long-term financial implications.

The Hidden Costs & Major Disadvantages: Why a 7-Year Car Loan Can Be Bad

While the allure of lower monthly payments is strong, the disadvantages of an extended car loan can be substantial and far-reaching. From a financial perspective, an 84-month term often proves to be a more expensive and riskier path. Understanding these drawbacks is critical before you commit.

Significantly More Interest Paid Over Time

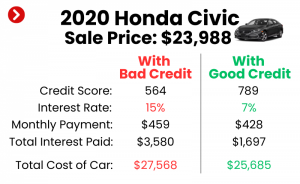

This is arguably the most significant drawback of a long-term car loan. When you extend your repayment period to seven years, you are borrowing money for a much longer duration. This means the lender has more time to charge you interest on the outstanding principal. Even if you secure a competitive interest rate, the sheer length of the loan term compounds the total amount of interest you will pay.

Let’s consider a hypothetical scenario: a $30,000 car loan at 6% APR. Over a 5-year (60-month) term, your monthly payment might be around $580, and you’d pay approximately $4,800 in total interest. Extend that to a 7-year (84-month) term, and your monthly payment drops to about $435, but your total interest paid skyrockets to roughly $6,500. That’s an extra $1,700 out of your pocket, simply for the convenience of a lower monthly payment.

Based on my experience, many buyers focus solely on the monthly payment without calculating the total cost of the loan. This oversight can lead to significant overspending. Always ask your lender for the total cost of the loan, including all interest, before signing any agreement.

Rapid Depreciation and the Risk of Negative Equity (Being Upside Down)

Cars, especially new ones, are depreciating assets. They lose value the moment you drive them off the lot, and this decline continues rapidly during the first few years of ownership. With a 7-year car loan, your car’s value often depreciates faster than you pay down the loan principal, leading to a situation known as negative equity, or being "upside down" on your loan.

Negative equity means you owe more on your car than it’s currently worth. This becomes a serious problem if your vehicle is totaled in an accident, as your insurance payout might not cover the full loan amount, leaving you to pay the difference out of pocket. It also makes it incredibly difficult to sell or trade in your car, as you’d need to come up with cash to cover the gap between the trade-in value and your outstanding loan balance.

Pro tips from us: To mitigate the risk of negative equity, always aim for a substantial down payment. This reduces the initial loan amount and helps you build equity faster. Also, consider gap insurance, which covers the difference between your car’s actual cash value and the amount you still owe on your loan if your vehicle is declared a total loss.

Extended Period of Indebtedness

Committing to an 84-month car loan means you will be in debt for a very long time – seven years! This prolonged financial obligation can feel like a heavy burden, especially as the car ages. It ties up a portion of your monthly income for an extended period, limiting your financial flexibility and ability to pursue other goals.

Think about what can happen in seven years: job changes, family growth, homeownership plans, or other major life events. Having a significant car payment hanging over your head can hinder your ability to save for a down payment on a house, invest for retirement, or even afford an unexpected emergency. It postpones financial freedom and keeps you beholden to a creditor for a substantial portion of your life.

Higher Total Cost of Ownership

Beyond the increased interest, an extended car loan often contributes to a higher total cost of ownership in other ways. While your loan term is seven years, most new car warranties typically expire after three to five years. This means you could be paying off your car for several years after its factory warranty has run out.

As cars age, they inevitably require more maintenance and repairs. If you’re still making loan payments while simultaneously facing costly repairs for an aging vehicle, your overall monthly automotive expenses can become quite burdensome. This scenario is a common mistake to avoid: underestimating the long-term costs beyond just the loan payment.

Limited Financial Flexibility and Vehicle Turnover

Life is unpredictable. You might find yourself needing a different vehicle sooner than seven years – perhaps your family grows, your commute changes, or you simply want an upgrade. With a long-term loan, trading in or selling your car prematurely can be financially challenging due to the negative equity trap we discussed.

You might be forced to roll the negative equity from your current car into a new loan, creating an even larger debt burden. This cycle of rolling over debt can be incredibly difficult to break and often leads to an endless loop of expensive car payments. It restricts your ability to adapt to changing needs without incurring significant financial penalties.

Higher Risk of Mechanical Issues Post-Warranty

As mentioned, an 84-month loan stretches well beyond the typical manufacturer’s warranty. This means that for a significant portion of your loan term, you’ll be solely responsible for any mechanical breakdowns or repairs. Modern vehicles, while reliable, can still encounter expensive issues as they accumulate mileage and age.

Imagine paying a substantial car loan every month while simultaneously footing the bill for a new transmission or engine repair. This dual financial strain can be overwhelming and completely negate the perceived savings from lower monthly payments. It’s crucial to consider the vehicle’s expected lifespan and reliability against the loan term.

When a 7-Year Car Loan Might Make Sense (Rare Scenarios)

While generally not recommended, there are a few very specific and rare circumstances where an 84-month car loan might be considered, though even then, extreme caution is advised. These scenarios typically apply to individuals with excellent credit and a clear, disciplined financial strategy.

One such scenario could involve an exceptionally low, promotional interest rate – sometimes even 0% APR – offered for a limited time on specific models. If you have a stellar credit score and can secure such a rate, the argument about paying more interest over time becomes moot. However, these offers are exceedingly rare for terms as long as 84 months and often come with strict eligibility requirements.

Another niche situation might be if you are purchasing a vehicle known for its exceptional longevity and slow depreciation, often a luxury brand or a classic model that holds its value well. Even then, you would need a very large down payment and a clear plan to pay it off faster than the full term. For the average consumer buying a typical daily driver, this is rarely the case.

Finally, some might use an extended loan as a temporary measure to manage a specific, short-term cash flow issue, with a concrete plan to refinance to a shorter term or pay off the loan aggressively once their financial situation improves. This requires immense discipline and a strong commitment to accelerated payments. Pro tips from us: If you find yourself in this situation, ensure your loan has no prepayment penalties and immediately begin making extra payments.

Crucial Factors to Consider Before Committing to an 84-Month Loan

Before you even think about signing on the dotted line for a long-term car loan, there are several critical factors you must meticulously evaluate. These considerations will help you determine if an 84-month term aligns with your personal financial reality.

First and foremost, your credit score plays a pivotal role. A higher credit score generally qualifies you for lower interest rates, which can somewhat mitigate the increased interest paid over a longer term. Conversely, if your credit score is average or poor, an extended loan will come with a much higher APR, making it an even more expensive proposition. For tips on improving your credit, you might find our guide on How to Improve Your Credit Score for Better Loan Rates helpful.

The interest rate offered is another non-negotiable point of scrutiny. Don’t just accept the first offer. Shop around with multiple lenders – banks, credit unions, and online lenders – to compare APRs. A difference of even one percentage point can save you thousands over a seven-year term. Always look at the total interest amount, not just the monthly payment.

Your down payment amount is incredibly impactful. A larger down payment directly reduces the amount you need to finance, thereby lowering your monthly payments and the total interest paid. It also helps you build equity faster, reducing the risk of negative equity. Aim for at least 20% down, if possible, especially on a new car.

Consider the vehicle’s reliability and expected lifespan. Is the car you’re buying known for its durability and low maintenance costs? Will it realistically last seven years (or more) without significant, costly repairs? Research reliability ratings from trusted sources like Consumer Reports or J.D. Power before making a decision.

Finally, take a hard look at your personal financial stability and future goals. Can you comfortably afford this payment for seven years? Are there any major life events on the horizon that might impact your income or expenses? An 84-month commitment is a long-term anchor on your budget, so ensure it aligns with your broader financial plan. Don’t let the allure of a lower monthly payment overshadow the total cost of ownership.

Pro Tips for Smart Car Financing (Even if Considering Longer Terms)

Even if you’re exploring the possibility of a longer car loan, there are smart strategies you can employ to minimize risks and secure the best possible terms. These pro tips are applicable to any car buying scenario, but they become even more crucial with extended financing.

Shop for Loans Before the Car: Get pre-approved for a loan from your bank or credit union before you even step foot on a dealership lot. This gives you a benchmark interest rate and empowers you to negotiate better with the dealer’s financing department. Having your own financing ready puts you in a stronger negotiating position.

Always Negotiate the Car Price First: Do not discuss financing until you have agreed on the final purchase price of the vehicle. Dealerships often try to combine these negotiations, which can obscure the true cost and allow them to make up for a lower car price with a less favorable loan term. Separate these two crucial steps.

Make the Largest Down Payment You Can Afford: We’ve stressed this already, but it bears repeating. A substantial down payment reduces your principal, lowers interest paid, and builds equity. It’s the single best way to improve your financial standing in a car loan.

Consider Used Cars: Used cars have already undergone their most significant depreciation. Opting for a well-maintained, slightly used vehicle can save you thousands on the purchase price and result in a smaller loan amount, which is easier to pay off over a shorter term.

Run the Numbers Yourself: Don’t rely solely on what the dealership tells you. Use online car loan calculators to crunch the numbers for different loan terms, interest rates, and down payments. Understand the total cost of the loan and how much interest you’ll pay. The Consumer Financial Protection Bureau (CFPB) offers excellent resources and calculators to help you understand car loan costs. You can find helpful tools and advice on their website www.consumerfinance.gov.

Read the Fine Print: Before signing anything, thoroughly review the loan agreement. Understand all terms and conditions, including the APR, total interest, any fees, and whether there are prepayment penalties. Some loans charge a fee if you pay them off early, which could negate your efforts to save interest.

Plan for Early Payoff: If you absolutely must take an 84-month car loan, make it a priority to pay it off faster. Even making an extra payment each year, or adding a small amount to your monthly payment, can significantly reduce the total interest paid and shorten your loan term. This requires discipline but can save you a substantial amount of money.

Common Mistakes to Avoid When Buying a Car

Beyond the specific pitfalls of 7-year car loans, there are several common mistakes that car buyers often make, regardless of the loan term. Being aware of these can save you a lot of headache and money.

One of the biggest blunders is focusing only on the monthly payment. While important for budgeting, fixating solely on this number can blind you to a higher purchase price or an unfavorable interest rate, ultimately leading to a more expensive car overall. Always consider the total cost.

Another common error is not understanding the true total cost of the loan. This includes not just the principal and interest, but also any fees, taxes, and add-ons like extended warranties or protection plans that get rolled into the loan. These can significantly inflate your debt.

Rolling negative equity from a previous car into a new loan is a dangerous practice that can trap you in a cycle of debt. Try to pay off any remaining balance on your trade-in before getting a new loan, or make a large enough down payment to cover the negative equity.

Skipping a thorough test drive or vehicle inspection is also a mistake. A car is a major purchase; ensure it meets your needs and is in good mechanical condition, especially if buying used. A pre-purchase inspection by an independent mechanic is always a wise investment.

Finally, buying more car than you truly need or can comfortably afford is a pervasive issue. It’s easy to get swept up in the excitement of new features or a prestigious badge, but always align your vehicle choice with your actual budget and lifestyle, not just your aspirations. Don’t forget to budget for the true cost of vehicle ownership, including insurance, fuel, and maintenance. We have a detailed article on The True Cost of Vehicle Ownership: Beyond the Sticker Price that can provide further insights.

The Verdict: Is A 7-Year Car Loan Bad?

After dissecting the complexities of 84-month car loans, the verdict leans heavily towards the negative for most consumers. While the allure of lower monthly payments is undeniable, the increased total interest paid, the high risk of negative equity, the extended period of indebtedness, and the potential for costly repairs post-warranty collectively make a 7-year car loan a financially disadvantageous choice in the vast majority of situations.

For the average car buyer, these long-term loans represent a subtle but significant drain on personal finances, trapping individuals in debt for far longer than necessary and limiting their financial flexibility. They often lead to paying thousands more than the vehicle is truly worth and can create significant stress when unforeseen circumstances arise.

There are indeed rare exceptions where such a loan might be justifiable – primarily with exceptionally low or 0% APR offers for individuals with impeccable credit and a rock-solid plan for early repayment. However, these scenarios are far from the norm and require a level of financial discipline that most people do not possess or cannot maintain over such a long period.

Conclusion

When asking "Is a 7-year car loan bad?", the answer for most people is a resounding yes. It’s a financial decision that prioritizes short-term payment relief over long-term financial health, often leading to greater overall expense and increased risk.

Our advice is to always prioritize a shorter loan term – ideally 36 to 60 months – and make the largest down payment you can reasonably afford. Focus on the total cost of the loan, not just the monthly payment. By understanding the true implications of extended financing, you can avoid common pitfalls and make a financially sound decision that serves your best interests for years to come. Drive smart, not just with a low monthly payment.