Is Financing a Car Truly a Loan? Unpacking the Auto Loan Landscape

Is Financing a Car Truly a Loan? Unpacking the Auto Loan Landscape Carloan.Guidemechanic.com

Navigating the world of car ownership can feel like deciphering a complex financial puzzle. For many, the dream of driving a new or pre-owned vehicle often hinges on one crucial question: Is financing a car a loan? The short answer is a resounding yes, but the intricacies behind this simple affirmation are vast and profoundly impact your financial well-being.

As an expert blogger and professional SEO content writer, I’m here to peel back the layers of vehicle financing. This comprehensive guide will explore every facet of auto loans, from their fundamental definition to the nitty-gritty of securing the best terms. Our goal is to equip you with the knowledge to make informed decisions, ensuring your car financing journey is as smooth and cost-effective as possible.

Is Financing a Car Truly a Loan? Unpacking the Auto Loan Landscape

The Core Question: Is Financing a Car a Loan? Absolutely, Here’s Why

Let’s cut straight to the chase: yes, financing a car is unequivocally a loan. When you finance a vehicle, you are essentially borrowing money from a lender – be it a bank, credit union, online lender, or the dealership itself – to cover the cost of the car. This borrowed money, known as the principal, is then repaid over a predetermined period, typically with added interest.

This entire arrangement fits the classic definition of a loan. A loan is a sum of money that an individual or entity borrows from another individual or entity, with the understanding that it will be paid back, often with interest. Car financing adheres perfectly to this principle, establishing a clear debtor-creditor relationship.

What makes car financing distinct from, say, a personal loan, is its secured nature. The vehicle you’re purchasing acts as collateral for the loan. This means that if you fail to make your agreed-upon payments, the lender has the legal right to repossess the car to recover their losses. This secured aspect significantly influences how these loans are structured and the terms offered to borrowers.

Understanding this fundamental concept is your first step towards mastering car financing. It’s not just an agreement to pay monthly; it’s a legally binding contract that makes you responsible for a significant debt, backed by a tangible asset.

Deconstructing the Auto Loan: What Exactly Is It?

Now that we’ve firmly established that financing a car is a loan, let’s delve deeper into what constitutes an auto loan. It’s a specialized type of installment loan, meaning you borrow a lump sum and repay it in fixed monthly installments over a set period. Each payment typically includes a portion of the principal balance and the interest accrued.

Secured vs. Unsecured Loans: The Car as Collateral

The most defining characteristic of an auto loan is its status as a secured loan. Unlike an unsecured personal loan, which is granted based solely on your creditworthiness, a secured loan requires collateral. In the context of car financing, the vehicle itself serves as this collateral.

This setup significantly reduces the risk for the lender. Should you default on your payments, they have a tangible asset – your car – they can seize and sell to recoup their investment. This reduced risk often translates to lower interest rates for borrowers compared to unsecured loan options.

It’s crucial to understand this collateral aspect. Until the loan is fully repaid, the lender typically holds the car’s title or a lien on it, indicating their ownership stake. Only once your final payment is made is the title fully transferred into your name, signifying complete ownership.

Key Components of an Auto Loan: Decoding the Terms

Every auto loan comes with several critical components that dictate the total cost and your monthly obligations. Understanding these elements is vital for making an informed decision.

- Principal Amount: This is the initial sum of money you borrow to buy the car, minus any down payment or trade-in value. It’s the base amount upon which interest is calculated.

- Interest Rate (APR): The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage. It includes not only the interest rate but also any additional fees charged by the lender. A lower APR means less money paid over the life of the loan.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer term usually results in lower monthly payments but can lead to paying more interest over time.

- Monthly Payments: This is the fixed amount you pay each month until the loan is satisfied. It’s calculated based on the principal, interest rate, and loan term.

- Down Payment: This is the upfront cash amount you pay towards the car’s purchase price. A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid overall.

The Journey of an Auto Loan: How It Works from Start to Finish

Understanding the mechanics of how financing a car as a loan plays out from application to repayment is crucial. This journey involves several distinct stages, each with its own considerations.

Pre-Approval: Your Strategic Advantage

Based on my experience, one of the most powerful steps you can take is getting pre-approved for a car loan before you even step foot on a dealership lot. Pre-approval involves applying for a loan with a bank, credit union, or online lender before you’ve chosen a specific vehicle.

This process gives you a clear understanding of how much you can afford, what interest rate you qualify for, and what your monthly payments will look like. Armed with a pre-approval letter, you transform from a casual shopper into a cash buyer in the eyes of the dealership, giving you significant leverage in negotiations. It helps you separate the car price negotiation from the financing negotiation.

Applying for the Loan: Documentation and Credit Check

Once you’ve found the perfect vehicle, or if you’re skipping pre-approval and going straight to the dealership for financing, you’ll complete a loan application. This typically requires providing personal information, employment details, income verification, and a social security number.

The lender will then perform a hard inquiry on your credit report. This credit check allows them to assess your creditworthiness, including your payment history, outstanding debts, and overall credit score. Your credit profile is a primary determinant of the interest rate and loan terms you’ll be offered.

Loan Approval & Negotiation: Understanding Offers

If your application is approved, you’ll receive a loan offer outlining the principal amount, interest rate, and loan term. If you have multiple offers, perhaps from your pre-approval and the dealership, you can compare them side-by-side.

Pro tips from us: Never accept the first offer, especially from a dealership. Use any pre-approval offers as a benchmark to negotiate for a better rate. Don’t be afraid to walk away if the terms aren’t favorable; there are always other options available.

Making Payments: Staying on Track

Once the loan is finalized and you drive off the lot, your monthly payments begin. It’s vital to make these payments on time and in full. Late payments can result in fees, negatively impact your credit score, and in severe cases, lead to repossession of your vehicle.

Common mistakes to avoid are underestimating the total cost of ownership, including insurance, fuel, and maintenance, which can strain your budget and make loan payments challenging. Always factor these into your overall financial planning.

Paying Off the Loan: The Title Transfer

Congratulations! Once you’ve made your final payment, the loan is officially satisfied. The lender will then release their lien on the vehicle and send you the clear title. This document proves that you now own the car outright, free and clear of any financial obligations. Keep this title in a safe place.

Types of Auto Loans and Where to Find Them

When financing a car as a loan, you have several avenues to explore. Each option comes with its own set of advantages and disadvantages.

Dealership Financing

This is perhaps the most common route. Dealerships often have relationships with multiple lenders and can offer convenient one-stop shopping. They might even offer special promotional rates, sometimes referred to as "captive financing" through the manufacturer’s own finance arm.

- Pros: Convenience, potential for special rates (especially for new cars), ability to bundle the loan with the purchase.

- Cons: Less transparency, limited negotiation power on rates, may prioritize their profit margins over your best interest.

Bank Loans

Traditional banks are a reliable source for auto loans. If you have an existing relationship with a bank, they might offer you competitive rates and a streamlined application process.

- Pros: Established reputation, potentially competitive rates, good customer service.

- Cons: Stricter eligibility requirements, less flexibility than some other lenders, application process might be slower.

Credit Union Loans

Credit unions are non-profit financial institutions owned by their members. They are renowned for offering some of the most competitive interest rates on auto loans, often beating banks.

- Pros: Generally lower interest rates, personalized service, often more flexible with borrowers who have less-than-perfect credit.

- Cons: Requires membership (often easy to join), might have fewer branches or online tools than large banks.

Online Lenders

The digital age has brought forth a plethora of online lenders specializing in auto financing. These platforms offer quick approvals and can be a great way to compare multiple offers from the comfort of your home.

- Pros: Convenience, fast application and approval, ability to compare multiple offers quickly.

- Cons: Less personal interaction, can be overwhelming with too many options, need to vet the lender’s reputation.

Factors Influencing Your Car Loan Approval & Terms

Understanding that financing a car is a loan means acknowledging that lenders will assess your risk profile. Several key factors weigh heavily on whether your loan is approved and what terms you’re offered.

Credit Score: Your Financial Report Card

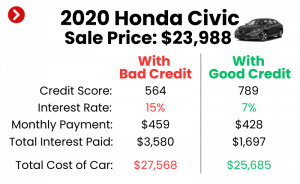

Your credit score is arguably the most significant factor. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt.

- High Credit Score (e.g., 700+): Indicates a low-risk borrower, leading to the best interest rates and most favorable terms.

- Average Credit Score (e.g., 600-699): You’ll likely qualify, but with slightly higher interest rates.

- Low Credit Score (e.g., below 600): You might still get approved, but expect significantly higher interest rates and potentially stricter terms, or you might need a co-signer.

Based on my experience, improving your credit score before applying for an auto loan can save you thousands of dollars in interest over the life of the loan.

Debt-to-Income Ratio (DTI): Can You Afford It?

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to take on additional debt. A lower DTI (typically below 36-43%) indicates you have more disposable income to cover new loan payments.

A high DTI might signal to lenders that you’re already stretched thin financially, making you a higher risk. This could result in loan denial or less favorable terms.

Down Payment: Showing Your Commitment

A substantial down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. It also signals to lenders that you’re committed to the purchase and have some skin in the game.

Common mistakes to avoid are putting down too little, or even nothing. While zero-down payment options exist, they often come with higher interest rates and leave you "upside down" on your loan (owing more than the car is worth) sooner.

Loan Term: The Balancing Act

The loan term, or repayment period, directly impacts your monthly payment and the total interest paid.

- Shorter Terms (e.g., 36-48 months): Higher monthly payments but significantly less interest paid overall. You own the car outright faster.

- Longer Terms (e.g., 72-84 months): Lower monthly payments, making the car seem more affordable. However, you’ll pay substantially more interest over the loan’s life, and the car will depreciate faster than you pay off the loan.

Pro tips from us: While longer terms offer lower payments, always calculate the total cost of the loan. Often, a slightly higher monthly payment for a shorter term is the more financially prudent choice.

Vehicle Age & Value: Collateral Considerations

The age and market value of the car you’re financing also play a role. Lenders are more willing to finance newer, lower-mileage vehicles because they hold their value better, making them more reliable collateral.

Financing an older, high-mileage vehicle can be more challenging, potentially leading to higher interest rates or shorter loan terms due to the increased risk of depreciation and mechanical issues.

Income Stability: Proof of Ability to Repay

Lenders want assurance that you have a stable and sufficient income to consistently make your loan payments. They will typically ask for proof of income, such as pay stubs, tax returns, or bank statements. Steady employment history is often viewed favorably.

Pros and Cons of Financing a Car

Deciding whether to take out a loan for a vehicle is a significant financial decision. Understanding that financing a car is a loan with specific benefits and drawbacks is key to making the right choice for your situation.

Advantages of Financing a Car

- Affordability: Financing makes car ownership accessible to a wider range of people who might not have the cash to buy a vehicle outright. You can drive the car you need or want without depleting your savings.

- Building Credit: Consistently making on-time payments on an auto loan is an excellent way to build or improve your credit history. A strong credit history opens doors to better rates on future loans, mortgages, and even insurance.

- Immediate Ownership (Eventually): While the lender holds a lien, you are the registered owner and have full use of the vehicle from day one. Once the loan is paid off, the car is entirely yours, with no mileage restrictions or wear-and-tear penalties like with a lease.

- Freedom to Customize: As the owner (even with a loan), you have the freedom to customize your vehicle as you see fit, without worrying about lease-end penalties for modifications.

- Potential for Equity: Over time, especially if you make a good down payment and choose a shorter loan term, you can build equity in your car. This equity can be used as a trade-in or as collateral for future loans.

Disadvantages of Financing a Car

- Interest Costs: The most significant drawback is the additional money you pay in interest over the life of the loan. This can add thousands of dollars to the total cost of the vehicle, especially with higher interest rates or longer loan terms.

- Depreciation: Cars are depreciating assets, meaning they lose value rapidly, especially in the first few years. You might find yourself "upside down" on your loan, owing more than the car is worth, particularly with little or no down payment and a long loan term.

- Debt Burden: An auto loan adds to your overall debt obligations, impacting your debt-to-income ratio and potentially limiting your ability to take on other loans (like a mortgage) in the future.

- Risk of Repossession: As a secured loan, failure to make payments can result in the loss of your vehicle, along with any money you’ve already paid towards it.

- Long-Term Commitment: Auto loans often span several years, locking you into monthly payments for a significant period. This can be restrictive if your financial situation changes unexpectedly.

Common Mistakes to Avoid When Financing a Car

Based on my experience helping countless individuals navigate vehicle purchases, certain pitfalls appear repeatedly. Understanding that financing a car is a loan is just the first step; avoiding these common mistakes will save you stress and money.

- Not Getting Pre-Approved: This is a cardinal sin in car buying. Without pre-approval, you walk into the dealership blind, unaware of your true borrowing power or the best interest rate you qualify for. You lose valuable negotiation leverage.

- Focusing Only on Monthly Payments: Dealerships love to talk about low monthly payments. While important, fixating solely on this figure can obscure a longer loan term or a higher interest rate, ultimately leading to paying much more over time. Always ask for the total cost of the loan.

- Ignoring the Total Cost: Beyond the monthly payment, consider the total amount you’ll pay for the car, including the purchase price, interest, taxes, and fees. A lower monthly payment doesn’t always mean a cheaper car.

- Skipping the Down Payment: While tempting, a zero-down payment can be a trap. It increases your principal, raises your monthly payments, and puts you at a higher risk of being upside down on your loan, especially given rapid depreciation.

- Not Checking Your Credit Report: Errors on your credit report can negatively impact your score, leading to higher interest rates. Always review your report for accuracy before applying for any loan. You can get a free copy from AnnualCreditReport.com.

- Falling for Unnecessary Add-ons: Dealerships often push extended warranties, paint protection, or undercoating. While some might offer value, many are overpriced or unnecessary. Evaluate each add-on carefully before agreeing to finance it.

- Not Shopping Around for Rates: Just as you’d compare car prices, compare loan offers from multiple lenders (banks, credit unions, online lenders) to secure the most competitive interest rate. This simple step can save you hundreds, if not thousands, of dollars.

Pro Tips for Securing the Best Car Loan

Now that we’ve covered the pitfalls, let’s focus on proactive strategies. Here are some pro tips from us to help you secure the most favorable terms when financing a car as a loan.

- Improve Your Credit Score: This is your strongest asset. Pay bills on time, reduce existing debt, and avoid opening new credit accounts in the months leading up to your car purchase. A higher score translates directly to lower interest rates.

- Save for a Substantial Down Payment: Aim for at least 10-20% of the car’s purchase price, if possible. A larger down payment reduces the loan amount, lowers your monthly payments, and mitigates the risk of being upside down on your loan.

- Shop Around for Rates Aggressively: Don’t just rely on the dealership’s financing. Get pre-approved by several banks, credit unions, and online lenders. Use these competing offers to negotiate for the best possible rate. Remember, a difference of even half a percentage point can save you hundreds over the loan term.

- Understand the Full Loan Agreement: Before signing anything, read every line of the loan contract. Ensure you understand the APR, loan term, total interest paid, any prepayment penalties, and all fees. Ask questions until everything is crystal clear.

- Consider Refinancing: If you’ve already financed a car but your credit score has improved, or interest rates have dropped, consider refinancing your auto loan. This could lead to a lower interest rate, reduced monthly payments, or a shorter loan term, saving you money in the long run. For a deeper dive into managing your debt, check out our guide on .

- Maintain a Low Debt-to-Income Ratio: Before applying, try to pay down other debts. A lower DTI ratio makes you a more attractive borrower and can help you qualify for better loan terms.

- Know Your Budget: Go beyond the monthly payment. Calculate your total budget for car ownership, including insurance, fuel, maintenance, and potential repairs. Don’t let a "low" monthly payment push you into a car you can’t truly afford.

Alternatives to Financing: Leasing vs. Buying Outright

While financing a car is a loan and a popular choice, it’s not the only way to acquire a vehicle. Briefly, let’s touch upon the primary alternatives: leasing and buying outright.

Leasing a Car

Leasing is essentially renting a car for a fixed period, typically 2-4 years, with specific mileage limits. You pay for the depreciation of the vehicle during that time, plus fees and interest.

- Pros: Lower monthly payments than financing, always driving a new car with the latest features, often covered by warranty, no trade-in hassle at the end of the lease.

- Cons: No ownership equity, mileage restrictions, wear-and-tear penalties, higher long-term cost if you always lease, less flexibility.

Buying a Car Outright

This means paying the full purchase price of the car with cash, avoiding any loans or interest payments.

- Pros: No monthly payments, no interest costs, full ownership from day one, complete freedom to modify, no mileage restrictions.

- Cons: Requires a significant upfront cash outlay, ties up a large sum of money, rapid depreciation of the asset.

Each option has its merits, but for most people, financing strikes a balance between immediate access to a vehicle and manageable payments.

Conclusion: Driving Forward with Confidence

By now, it should be crystal clear: financing a car is a loan – a secured installment loan that enables you to acquire a vehicle by borrowing money and repaying it over time with interest. This comprehensive understanding is your most valuable tool as you navigate the car buying process.

From grasping the core components of an auto loan to strategically shopping for the best rates and avoiding common financial pitfalls, you now possess the insights needed to make informed decisions. Remember, knowledge is power, especially when it comes to significant financial commitments like vehicle financing.

Don’t rush the process. Do your homework, compare offers, and understand every detail of your loan agreement. By approaching car financing with confidence and a well-informed strategy, you can secure a great deal and enjoy your new ride without unnecessary financial stress.

What has been your experience with car financing? Share your insights and questions in the comments below – we love hearing from our readers!