Is It Smart to Pay Your Car Loan with a Credit Card? A Comprehensive Guide

Is It Smart to Pay Your Car Loan with a Credit Card? A Comprehensive Guide Carloan.Guidemechanic.com

The idea of using a credit card to pay off a significant expense like a car loan can be incredibly appealing. Imagine earning a stack of rewards points, consolidating debt, or simply buying yourself some breathing room during a tight financial month. While the thought might spark a sense of financial savviness, the reality is far more complex, riddled with potential pitfalls that could turn a seemingly clever move into a costly mistake.

As an expert blogger and professional SEO content writer, I’ve delved deep into the intricacies of personal finance. Based on my experience, navigating the world of credit cards and loans requires a clear understanding of the rules, fees, and potential consequences. This comprehensive guide will unravel everything you need to know about paying your car loan with a credit card, offering insights, strategies, and crucial warnings to help you make an informed decision. Our ultimate goal is to equip you with the knowledge to manage your finances wisely, ensuring you avoid common mistakes and leverage financial tools effectively.

Is It Smart to Pay Your Car Loan with a Credit Card? A Comprehensive Guide

Why Direct Payments Are Almost Always a No-Go: Understanding Lender Restrictions

Before we explore the indirect methods, it’s crucial to understand why most car loan lenders don’t allow direct credit card payments. This isn’t just about inconvenience; it’s rooted in fundamental financial principles and operational costs.

Firstly, when a customer uses a credit card, the merchant (in this case, the car loan lender) is charged a transaction fee by the credit card processing network. These "interchange fees" can range from 1.5% to 3.5% or even more of the transaction amount. For a large payment like a car loan, these fees can quickly add up, significantly eroding the lender’s profit margin. Most lenders simply aren’t willing to absorb these costs for car loan payments.

Secondly, from a risk management perspective, lenders prefer to keep car loans as secured debt, separate from the often higher-interest, unsecured nature of credit card debt. Allowing direct payments could blur these lines, creating administrative complexities and potentially increasing their exposure to default risk. It’s simply not how the system is designed to operate.

The Indirect Route: How You Might Pay Your Car Loan with a Credit Card

Since direct payments are largely off the table, the strategies involve indirect methods. Each comes with its own set of rules, fees, and risks. It’s essential to understand these nuances before proceeding.

Method 1: The Balance Transfer Strategy (Often Misunderstood)

A balance transfer involves moving existing debt from one credit card to another, usually to take advantage of a lower interest rate or a 0% introductory APR offer. While you generally cannot directly balance transfer a car loan (which is a different type of loan, not credit card debt), this method can still play a strategic role.

How it works (indirectly): Instead of transferring your car loan, you could use a balance transfer to consolidate other high-interest credit card debt onto a new card with a 0% APR promotional period. By doing so, you free up cash flow that would have gone towards those credit card payments, allowing you to direct that freed-up money towards your car loan. This strategy effectively helps you manage your overall debt burden.

Pros:

- 0% APR Promotional Periods: Many cards offer 0% interest for 12-21 months, allowing you to pay down transferred debt without accruing interest during that period.

- Debt Consolidation: Simplifies your payments by combining multiple credit card balances into one.

- Potential for Savings: If you can pay off the transferred balance before the promotional period ends, you save significantly on interest.

Cons:

- Balance Transfer Fees: Most balance transfers come with a fee, typically 3-5% of the transferred amount. You must factor this into your calculations.

- New Interest Rate After Promo: Once the promotional period expires, the interest rate can jump significantly, sometimes higher than your original cards.

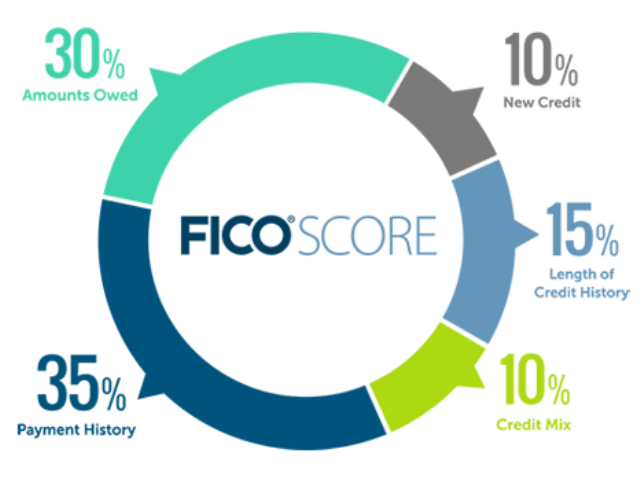

- Impact on Credit Score: A new credit inquiry and increased credit utilization can temporarily ding your score.

- Not a Direct Car Loan Payment: Remember, you’re not directly paying your car loan; you’re just optimizing other debt to free up cash.

Pro tips from us: Always look for cards with the lowest (or ideally, no) balance transfer fees. Ensure you have a solid plan to pay off the transferred balance before the 0% APR period ends. Based on my experience, direct balance transfers for car loans are extremely rare and typically not permitted by lenders.

Method 2: Cash Advances (Proceed with Extreme Caution)

A cash advance is essentially borrowing cash against your credit card’s line of credit. You can get a cash advance by withdrawing money from an ATM using your credit card or by visiting a bank branch.

How it works: You take out a cash advance from your credit card, deposit the cash into your checking account, and then use that money to pay your car loan lender directly.

Pros:

- Immediate Cash Access: Provides quick access to funds when you need them most.

- No Lender Restrictions: Since you’re paying with cash from your checking account, your car loan lender won’t know or care about the source of the funds.

Cons:

- High Fees: Cash advance fees are notoriously high, typically 3-5% of the advanced amount, with a minimum fee often around $10.

- Immediate High Interest: Unlike regular purchases, cash advances do not have a grace period. Interest starts accruing immediately, often at a higher APR than your standard purchase rate.

- No Rewards: You typically don’t earn any rewards points or cashback on cash advances.

- Impact on Credit Score: High credit utilization and a cash advance on your report can signal higher risk to lenders, potentially lowering your credit score.

Common mistakes to avoid are thinking cash advances are a cheap or easy solution. The fees and immediate interest make them one of the most expensive ways to access funds. Based on my experience, this method should only be considered in absolute emergencies where the alternative is defaulting on a loan, and you have an immediate, guaranteed plan to repay the credit card.

Method 3: Convenience Checks (Similar to Cash Advances)

Convenience checks are pre-printed checks linked to your credit card account, allowing you to write a check against your credit line. They are often sent by credit card companies as promotional offers.

How it works: You write a convenience check directly to your car loan lender. Since it’s a check, many lenders will accept it, as they won’t differentiate it from a personal check drawn from your bank account.

Pros:

- Accepted by More Lenders: Can be used for payments where credit cards are not directly accepted.

- No Direct Credit Card Processing: The car loan lender isn’t processing a credit card transaction.

Cons:

- High Fees and Interest: Convenience checks are treated very much like cash advances. They typically come with high transaction fees (3-5%) and immediate, high-interest rates with no grace period.

- No Rewards: Generally, you won’t earn rewards points on convenience check transactions.

- Risk of Overspending: It can be easy to write a check for more than you can afford to repay quickly.

Based on my experience, convenience checks are often misunderstood as a simple alternative. In reality, they carry the same heavy financial burden as cash advances. Use them only if you fully understand the costs and have a rapid repayment strategy.

Method 4: Third-Party Payment Services

Several third-party payment platforms allow you to pay bills that typically don’t accept credit cards directly. These services act as an intermediary.

How it works: You pay the third-party service with your credit card, and the service then remits payment to your car loan lender via ACH transfer or physical check. Popular examples include Plastiq (though always check their current offerings and fees).

Pros:

- Earn Rewards: You can potentially earn credit card rewards points on your car loan payments, which is a major draw for many.

- Convenience: Allows you to consolidate various bill payments onto your credit card.

- Bridging the Gap: Solves the problem of lenders not directly accepting credit cards.

Cons:

- Service Fees: These platforms charge a fee for their service, typically ranging from 2.5% to 3% of the payment amount. You need to calculate if your rewards outweigh this fee.

- Potential Delays: Payments might take a few business days to process and reach your lender, so plan accordingly to avoid late fees.

- Credit Utilization: Large payments will increase your credit utilization, which can temporarily affect your credit score.

Pro tips from us: Always calculate the fee versus the rewards earned. For example, if you pay a 2.85% fee and earn 2% cashback, you’re still losing money. This method is most effective when you have a high-value rewards card (e.g., travel points worth more than 3 cents per point) and you’re confident you can pay off the credit card balance immediately.

Method 5: Paying Other Bills with Your Credit Card to Free Up Cash

This is an indirect but often the safest and most strategic method. It doesn’t involve directly paying your car loan with a credit card, but rather optimizing your cash flow.

How it works: You use your credit card for everyday expenses that you would typically pay with cash or your debit card (e.g., groceries, utilities, fuel). You then ensure you pay off your credit card balance in full and on time each month. The cash you "saved" by using your credit card for these other expenses can then be directed towards your car loan payment.

Pros:

- Earn Rewards: You earn rewards on your everyday spending.

- No Direct Fees: There are no additional fees (like cash advance or balance transfer fees) for making regular purchases.

- Improved Cash Flow: Frees up liquid cash in your bank account for your car loan.

- Credit Building: Responsible use of a credit card (paying in full) can improve your credit score.

Cons:

- Requires Discipline: You must pay off your credit card balance in full every month to avoid interest charges, which would negate any benefits.

- Risk of Overspending: It’s easy to overspend if you don’t stick to a strict budget.

Based on my experience, this is often the safest and most strategic indirect method. It allows you to leverage credit card benefits without incurring the high fees and immediate interest associated with direct payment methods.

The "Why": Potential Benefits of Using a Credit Card for Car Loan Payments (When Done Right)

Despite the hurdles and risks, there are specific, carefully managed scenarios where using a credit card to facilitate a car loan payment might offer some advantages.

- Earning Rewards Points or Cashback: For those with premium rewards cards, using a third-party service or the "free up cash" strategy could yield valuable points, miles, or cashback that can offset the cost of fees or simply provide a bonus. The key is ensuring the value of the rewards outweighs any fees incurred.

- Temporary Financial Relief in an Emergency: In a genuine, short-term cash crunch, using a cash advance or convenience check (as a last resort) might prevent a late payment fee or even default on your car loan. This is a high-cost solution and should only be considered if you have an immediate and guaranteed plan to repay the credit card.

- Leveraging 0% APR Offers (Indirectly): As discussed with balance transfers, if you can use a 0% APR offer to pay off other high-interest debt, it frees up your cash flow to tackle your car loan more aggressively without incurring new interest on the consolidated debt for a period.

- Avoiding a Late Payment/Default: A late payment on a car loan can significantly damage your credit score, incur hefty fees, and potentially lead to repossession. If a credit card is your only option to make a payment on time, the cost of the credit card transaction might be less damaging than the consequences of a late car loan payment. This is a very specific, last-ditch scenario.

The "Why Not": Significant Risks and Drawbacks to Consider

While the potential benefits can be enticing, the risks associated with paying your car loan with a credit card are substantial and often outweigh the advantages.

- High Interest Rates: Credit card APRs are notoriously high, often ranging from 15% to 25% or even more. Car loan interest rates are typically much lower (e.g., 3-8%). Transferring a lower-interest debt to a higher-interest credit card is almost always a financially unsound decision unless a 0% APR promotional period is perfectly managed.

- Accumulation of Fees: As detailed earlier, cash advance fees, balance transfer fees, and third-party service fees can quickly add up, making the transaction more expensive than the benefits derived. These fees are typically non-refundable and instantly increase your debt.

- Falling into a Debt Cycle: The most significant risk is transferring one debt only to accrue more debt on your credit card. If you cannot pay off the credit card balance quickly, you’ll end up owing more overall due to higher interest and fees, effectively digging yourself into a deeper financial hole.

- Negative Impact on Credit Score:

- Increased Credit Utilization: Using a large portion of your credit limit for a car loan payment significantly increases your credit utilization ratio, which can negatively impact your credit score.

- New Credit Inquiries: Applying for a new balance transfer card leads to a hard inquiry, temporarily lowering your score.

- Missed Payments: If you struggle to pay off the credit card, missed payments will severely damage your credit.

- Loss of Car as Collateral: It’s important to remember that even if you use a credit card to pay your car loan, your car loan is still a secured debt. If you default on your car loan (e.g., you used the credit card for one payment but then couldn’t continue making payments), the car lender can still repossess your vehicle. You would then be left with no car and high-interest credit card debt.

- No Grace Period for Cash Advances/Convenience Checks: Interest starts accruing immediately, making these methods particularly expensive.

When Does It Make Sense? Specific Scenarios Where It Might Be Considered

Given the risks, there are very few scenarios where paying your car loan with a credit card is advisable. Here are the limited situations where it might be considered, always with extreme caution and a robust repayment plan:

- To Avoid an Imminent Late Payment or Default on Your Car Loan: If you are facing a late payment fee, a significant credit score drop, or even repossession, and you have absolutely no other funds available, a cash advance or convenience check might be a last-resort option. However, this is only viable if you have an immediate and guaranteed source of funds to pay off the credit card within days or weeks, preventing high interest from accumulating.

- To Leverage a 0% APR Balance Transfer for Other Debt (Indirectly): As discussed, if you have high-interest credit card debt, a 0% APR balance transfer can free up cash flow. This freed-up cash can then be used for your car loan. This is a strategic move to optimize your overall debt, not a direct car loan payment.

- To Maximize Rewards with a Third-Party Service (When Rewards Outweigh Fees): If you have a premium credit card that offers rewards valued higher than the 2.5-3% fee charged by a third-party service, and you can pay off the entire credit card balance before interest accrues, this can be a calculated move. For example, if you get 5% back on a certain category that includes your car payment via a third-party, and the fee is 2.5%, you net 2.5%. This requires careful math and financial discipline.

Pro tips from us: Before considering any of these, always have a solid repayment plan. Ask yourself: "How exactly will I pay off this credit card balance before interest kicks in or fees become prohibitive?" If you don’t have a clear, guaranteed answer, do not proceed.

Step-by-Step Guide: How to Proceed Safely (If You Choose To)

If, after weighing all the pros and cons, you decide to use a credit card indirectly for your car loan payment, here’s a step-by-step guide to doing so as safely as possible:

Step 1: Understand Your Car Loan Terms

- Check your current interest rate: This is your baseline. You don’t want to replace this with a higher rate.

- Review late payment policies: Know the fees and credit score implications of missing a payment.

- Payment due date: Be aware of deadlines, especially if using a third-party service with processing delays.

Step 2: Review Your Credit Card Offers

- Current APR: Know the standard purchase APR, cash advance APR, and any balance transfer APRs.

- Fees: Identify cash advance fees, balance transfer fees, and annual fees.

- Credit Limit: Ensure you have enough available credit for the payment without maxing out your card.

- Rewards Program: Understand how rewards are earned and their actual value.

Step 3: Calculate All Costs and Benefits

- Total Fees: Sum up all transaction fees (cash advance, balance transfer, third-party service).

- Interest Charges: Calculate potential interest if you cannot pay off the credit card immediately.

- Rewards Value: Estimate the monetary value of any rewards earned.

- Net Cost/Benefit: Compare the total cost (fees + potential interest) against any benefits (rewards, avoiding late fees).

Step 4: Choose the Right Method

- If freeing up cash flow: Consider a 0% APR balance transfer for other high-interest debt.

- If maximizing rewards: Evaluate third-party payment services, ensuring rewards outweigh fees.

- If in an absolute emergency: A cash advance or convenience check might be a last resort, but only with an immediate repayment plan.

Step 5: Execute and Monitor

- Make the payment: Follow the steps for your chosen method carefully.

- Track processing times: Especially with third-party services, ensure the payment reaches your car loan lender on time.

- Monitor your credit card statement: Verify the payment, fees, and interest charges are accurate.

Step 6: Prioritize Credit Card Repayment

- Pay off the credit card balance immediately: This is the most critical step to avoid high-interest charges.

- Set reminders: Ensure you don’t miss the credit card payment due date.

- Adjust your budget: Allocate funds specifically to pay down the credit card debt as quickly as possible.

Common Mistakes to Avoid

Based on my experience, many people fall into common traps when attempting to use credit cards for loan payments. Avoiding these pitfalls is crucial for your financial health.

- Not Calculating All Fees: Many overlook cash advance fees, convenience check fees, or third-party service charges, leading to an unexpected increase in the overall cost.

- Forgetting About Immediate Interest: Cash advances and convenience checks typically incur interest from day one, with no grace period, making them far more expensive than expected.

- Assuming All Credit Cards Are the Same: Different cards have varying APRs, fees, and rewards structures. What works for one card might be disastrous for another.

- Accumulating More Debt: The most significant mistake is transferring debt from a car loan to a credit card only to accumulate more high-interest credit card debt because you can’t pay it off.

- Not Having a Repayment Plan: Going into this without a clear, guaranteed strategy to pay off the credit card balance immediately is a recipe for financial trouble.

- Ignoring Credit Utilization: A large payment on a credit card can dramatically increase your utilization ratio, negatively impacting your credit score.

Expert Recommendations & Final Thoughts

In conclusion, while the allure of using a credit card for a car loan payment is strong, it’s generally not recommended for the average consumer. The high fees, immediate interest accrual, and risk of falling into a debt cycle often outweigh any perceived benefits.

Pro tips from us: Always prioritize paying down high-interest debt first. Your car loan typically has a much lower interest rate than your credit card. Transferring that debt is usually a step backward.

If you are struggling to make your car loan payments, consider these alternatives before resorting to a credit card:

- Contact your lender: Many lenders are willing to work with you on payment plans, deferrals, or other hardship options.

- Refinance your car loan: If you have improved credit or current interest rates are lower, refinancing could reduce your monthly payments or total interest. For a deeper dive into managing credit card debt, check out our guide on Smart Strategies for Credit Card Debt Management. If you’re considering refinancing your car loan, our article on Understanding Car Loan Refinancing: A Complete Guide offers valuable insights.

- Adjust your budget: Look for areas to cut expenses to free up cash for your car payment.

- Seek financial counseling: A certified financial advisor can help you create a sustainable budget and debt repayment plan. You can find more detailed information on credit card terms and conditions from reputable sources like the Consumer Financial Protection Bureau (CFPB).

Ultimately, responsible financial management means understanding the tools at your disposal and using them strategically. While a credit card can be a powerful tool for building credit and earning rewards, using it to pay a car loan often comes with a steep price. Always choose the path that protects your financial future and minimizes your debt burden.