Keesler Federal Credit Union Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

Keesler Federal Credit Union Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is exciting, but navigating the world of auto loans can often feel like a complex maze. For many, finding competitive interest rates and a trustworthy lender is paramount. This is where Keesler Federal Credit Union (KFCU) shines, offering a member-centric approach to financing your next car.

As an expert blogger and professional SEO content writer, I understand the importance of not just finding a loan, but securing the best possible terms. In this comprehensive guide, we’ll dive deep into everything you need to know about Keesler Federal Credit Union car loan rates, how they work, and most importantly, how you can position yourself to get the most favorable deal. Our goal is to equip you with the knowledge to make informed decisions and confidently drive away in your dream car.

Keesler Federal Credit Union Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

Understanding Keesler Federal Credit Union (KFCU): More Than Just a Bank

Before we delve into the specifics of Keesler Federal Credit Union car loan rates, it’s crucial to understand what makes KFCU, and credit unions in general, different from traditional banks. This foundational knowledge helps explain why credit unions often offer more attractive loan products.

What is a Credit Union?

Unlike banks, which are typically for-profit entities owned by shareholders, credit unions are not-for-profit financial cooperatives. They are owned by their members, which means any profits generated are usually returned to members in the form of lower loan rates, higher savings rates, and fewer fees. This member-first philosophy is a core distinction.

KFCU operates with this very principle, prioritizing the financial well-being of its members. They are focused on community and personalized service, which can be a significant advantage when applying for something as important as a car loan.

Who Can Join Keesler Federal Credit Union?

A common question people have is, "Can I even join a credit union?" For Keesler Federal Credit Union, membership is open to a broad community. Historically tied to Keesler Air Force Base, their field of membership has expanded significantly.

Generally, you can join KFCU if you live, work, worship, or attend school in specific counties across Mississippi and Louisiana. Membership is also open to active duty and retired military personnel, Department of Defense employees, and their families. Always check their official website for the most current and specific eligibility requirements.

Becoming a member is a straightforward process, usually involving opening a savings account with a small initial deposit. This small step unlocks a world of financial services, including access to their competitive auto loan rates.

Demystifying KFCU Car Loan Rates: What Drives Them?

When you apply for a car loan at Keesler Federal Credit Union, the rate you receive isn’t pulled out of thin air. Several key factors come into play, influencing the specific interest rate you’ll be offered. Understanding these elements empowers you to improve your position before even applying.

The Core Factors Influencing Your Rate

Based on my experience in personal finance, these are the primary drivers behind any auto loan rate, including those at KFCU:

-

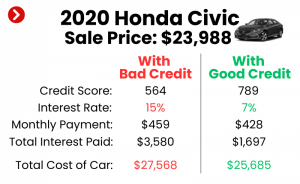

Your Credit Score: This is arguably the most significant factor. Your credit score, typically a FICO or VantageScore, is a numerical representation of your creditworthiness. It tells lenders how reliably you’ve managed debt in the past.

- A higher credit score (generally above 700) indicates lower risk to the lender, resulting in more favorable Keesler Federal Credit Union car loan rates. Conversely, a lower score suggests higher risk, leading to higher interest rates to compensate the lender.

- Pro Tip from us: Always check your credit score and report before applying for any loan. This allows you to identify and dispute any errors, and gives you time to improve your score if needed. Websites like AnnualCreditReport.com provide free access to your reports.

-

The Loan Term (Length): This refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months).

- Shorter loan terms often come with lower interest rates because the lender’s risk exposure is reduced. However, shorter terms mean higher monthly payments.

- Longer loan terms (e.g., 72 or 84 months) result in lower monthly payments, making the car more "affordable" on a month-to-month basis. The trade-off is usually a higher interest rate and significantly more total interest paid over the life of the loan.

-

Vehicle Type and Age: Lenders assess the risk associated with the collateral – in this case, the car itself.

- New cars typically qualify for lower rates than used cars. This is because new cars have a predictable value and are less likely to require immediate costly repairs.

- Used cars, especially older models or those with high mileage, are seen as higher risk. Their value can depreciate faster, and they may be more prone to mechanical issues, leading to slightly higher rates.

-

Your Down Payment: The amount of money you put down upfront towards the purchase of the vehicle.

- A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. This can often translate into a lower interest rate on your Keesler Federal Credit Union car loan.

- Beyond the rate, a substantial down payment also means lower monthly payments and less interest paid overall.

-

Your Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to manage additional debt.

- A lower DTI ratio indicates that you have more disposable income to cover your loan payments, making you a more attractive borrower. KFCU, like other lenders, wants to ensure you can comfortably afford the loan without overextending your finances.

-

Your Relationship with KFCU: As a member-owned institution, credit unions often reward loyalty.

- If you’re an existing member with a good standing history (e.g., other accounts, previous loans paid on time), KFCU might offer you slightly more favorable rates or terms. This is part of the credit union advantage.

KFCU’s Competitive Edge

The not-for-profit structure of Keesler Federal Credit Union often allows them to offer more competitive car loan rates compared to larger, for-profit banks. Their focus is on serving members, not maximizing shareholder profits. This means they can pass on savings directly to you in the form of lower interest rates and potentially more flexible loan terms.

Types of Car Loans Offered by Keesler Federal Credit Union

KFCU understands that car buying needs are diverse. They offer a range of auto loan products designed to fit various situations, from purchasing a brand-new vehicle to refinancing an existing loan.

New Car Loans

If you’re eyeing a vehicle straight off the dealership lot, KFCU offers competitive new car loans. These loans are typically for vehicles that are current model year or up to one or two years old, with very low mileage.

- Key Benefit: New car loans often come with the lowest interest rates due to the predictable value and lower risk associated with brand-new collateral.

- Consideration: While rates are lower, the total loan amount will be higher, leading to larger monthly payments or longer terms.

Used Car Loans

For those who prefer the value and cost savings of a pre-owned vehicle, Keesler Federal Credit Union also provides used car loans. These loans are designed for vehicles that are several years old or have accumulated a certain amount of mileage.

- Key Benefit: Used car loans make quality pre-owned vehicles accessible, often with more affordable price tags than new cars.

- Considerations: Rates for used car loans might be slightly higher than new car loans, and there might be restrictions on the maximum age or mileage of the vehicle KFCU will finance. Always check their specific criteria.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for a better deal. KFCU’s auto loan refinancing option can be a game-changer. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms.

- When to Consider Refinancing:

- Your credit score has significantly improved since you took out your original loan.

- Interest rates have dropped since your original purchase.

- You want to lower your monthly payment by extending the loan term (though this means more interest overall).

- You want to shorten your loan term to pay it off faster and reduce total interest.

- Pro tips from us: Refinancing can save you hundreds, even thousands, over the life of your loan. It’s particularly beneficial if your current loan has a high-interest rate from a dealership or a subprime lender. KFCU’s competitive rates make them an excellent option for this.

Other Vehicle Loans

Beyond traditional cars, KFCU often extends financing to other types of vehicles. This can include:

- Motorcycle Loans: For those who prefer two wheels over four.

- RV Loans: For adventurers looking for a home on wheels.

- Boat Loans: For marine enthusiasts ready to hit the water.

Each of these loan types will have its own specific rates and terms, which are typically influenced by the same factors as car loans (credit score, loan term, collateral value).

The Application Process: A Step-by-Step Guide to Securing Your KFCU Car Loan

Applying for a car loan at Keesler Federal Credit Union doesn’t have to be intimidating. By following a structured approach, you can streamline the process and increase your chances of approval for the best possible Keesler Federal Credit Union car loan rates.

Phase 1: Preparation is Key

Thorough preparation is the bedrock of a successful loan application. This stage empowers you with knowledge and helps avoid common pitfalls.

- Check Your Credit Score and Report: As mentioned earlier, this is your first and most critical step. Understand where you stand. If there are errors, dispute them immediately. If your score needs improvement, consider delaying your application slightly to implement strategies to boost it.

- Determine Your Budget: Before you even look at cars, figure out how much you can truly afford. This isn’t just about the monthly loan payment; it includes insurance, fuel, maintenance, and potential registration fees. A good rule of thumb is that your total car expenses shouldn’t exceed 10-15% of your net income.

- Gather Necessary Documents: Having your paperwork ready saves time and hassle. You’ll typically need:

- Proof of identity (Driver’s License, Social Security Card).

- Proof of residence (Utility bill, lease agreement).

- Proof of income (Pay stubs, W-2s, tax returns for self-employed).

- Vehicle information (if you’ve already chosen a car, including VIN, make, model, year).

Phase 2: The Application Itself

KFCU offers convenient ways to apply, catering to your preference.

- Online Application: This is often the quickest and easiest method. You can typically complete the entire application from the comfort of your home, submitting documents electronically.

- In-Person or Phone Application: If you prefer a more personal touch or have questions, you can visit a KFCU branch or speak with a loan officer over the phone. This allows for direct interaction and immediate clarification of any concerns.

- Pre-Approval: Your Secret Weapon: Common mistakes to avoid are skipping the pre-approval process. Getting pre-approved for a loan before you visit the dealership is incredibly powerful.

- What is Pre-Approval? KFCU will review your financial information and, if approved, will provide you with a conditional loan offer, including a maximum loan amount and an estimated interest rate.

- Benefits:

- Know Your Budget: You’ll know exactly how much you can spend, preventing you from falling in love with a car outside your financial reach.

- Bargaining Power: You walk into the dealership as a cash buyer, negotiating the price of the car rather than the monthly payment. This puts you in a much stronger position to get a better deal on the vehicle itself.

- Confidence: You can shop with peace of mind, knowing your financing is secured.

Phase 3: Approval and Closing

Once you’ve submitted your application, the waiting game begins, but it’s usually not a long one with credit unions.

- What to Expect After Applying: KFCU’s loan officers will review your application and credit profile. They may contact you for additional information or clarification.

- Reviewing the Loan Offer: If approved, you’ll receive a loan offer outlining the interest rate, term, monthly payment, and any associated fees. Carefully read every detail. Ensure you understand all the terms and conditions. Don’t hesitate to ask questions if anything is unclear.

- Finalizing the Loan: Once you accept the offer and have selected your vehicle, KFCU will work with you to finalize the paperwork. This usually involves signing the loan agreement and setting up your payment schedule.

Maximizing Your Savings: Tips for Getting the Best Keesler Federal Credit Union Car Loan Rates

While your credit score is a major determinant, there are proactive steps you can take to influence your Keesler Federal Credit Union car loan rates and secure the most advantageous terms.

-

Improve Your Credit Score: This cannot be emphasized enough.

- Pay all your bills on time, every time. Payment history is the biggest factor in your score.

- Reduce your outstanding debt, especially on credit cards, to lower your credit utilization ratio.

- Avoid opening new credit accounts unnecessarily before applying for the car loan.

- Keep old accounts open, even if unused, as this contributes to a longer credit history.

- If you’re looking to improve your financial health before applying, check out our guide on .

-

Make a Larger Down Payment: As discussed, putting more money down upfront reduces the loan amount and the lender’s risk.

- This often results in a lower interest rate, a smaller monthly payment, and less interest paid over the life of the loan.

- Aim for at least 10-20% of the vehicle’s purchase price if possible.

-

Choose a Shorter Loan Term: While a longer term offers lower monthly payments, a shorter term almost always comes with a lower interest rate.

- If your budget allows for a higher monthly payment, opting for a 36- or 48-month loan instead of a 60- or 72-month loan can save you a significant amount in interest.

- Carefully weigh your monthly budget against the total cost of the loan.

-

Consider a Co-signer (Wisely): If your credit isn’t stellar, or you’re a young borrower with limited credit history, a co-signer with excellent credit can help you qualify for better rates.

- Important Note: A co-signer is equally responsible for the loan. If you miss payments, it negatively impacts their credit, and they are legally obligated to repay the debt. Only pursue this option with someone you trust implicitly and who understands the full implications.

-

Bundle Your Services: As a member-focused institution, KFCU might offer rate discounts if you have multiple accounts or services with them (e.g., checking account, savings account, direct deposit).

- Always ask a loan officer if there are any member-exclusive discounts or promotions you qualify for.

-

Maintain a Low Debt-to-Income Ratio: Before applying, try to pay down other debts. A lower DTI shows KFCU that you have plenty of room in your budget for a new car payment.

Common Mistakes to Avoid When Applying for a Car Loan

Even with the best intentions, applicants can fall into common traps. Being aware of these can save you money and stress.

- Not Checking Your Credit Score: As reiterated, this is foundational. Surprises on your credit report can derail your application or lead to higher rates.

- Applying to Too Many Lenders: Each hard inquiry on your credit report can slightly lower your score. While multiple auto loan inquiries within a short window (typically 14-45 days) are often grouped as one for scoring purposes, excessive, scattered applications can be detrimental. Focus on 2-3 strong contenders like KFCU.

- Focusing Only on the Monthly Payment: Dealerships often try to negotiate based solely on the monthly payment. This can hide a longer loan term or a higher interest rate, leading to you paying significantly more overall. Always look at the total loan amount and interest rate.

- Not Understanding the Full Loan Terms: Read the fine print! Ensure you know the APR (Annual Percentage Rate), any fees, pre-payment penalties (rare for auto loans but possible), and the total cost of the loan.

- Skipping Pre-Approval: Going to the dealership without pre-approval from KFCU means you’re negotiating from a weaker position. Get pre-approved first!

- Not Factoring in Additional Costs: Remember to budget for car insurance, registration fees, taxes, and potential maintenance. These add significantly to the true cost of car ownership. For advice on managing these costs, you might find our article on helpful.

FAQs about Keesler Federal Credit Union Car Loans

Let’s address some frequently asked questions that often arise when considering a KFCU auto loan.

Q: What are the minimum credit score requirements for a KFCU car loan?

A: While KFCU doesn’t publicly disclose a strict minimum, like most lenders, a higher score will always yield better rates. Generally, a score in the "good" to "excellent" range (670+) will give you the best chance for the most competitive Keesler Federal Credit Union car loan rates. However, they do consider members with less-than-perfect credit, so it’s always worth applying or speaking with a loan officer.

Q: How long does the approval process take?

A: Many applicants report quick decisions, sometimes within hours, especially if applying online and all necessary documentation is readily available. Pre-approvals can also be very fast. The final funding process will depend on how quickly you finalize your vehicle choice and paperwork.

Q: Can I get a loan if I’m not a member yet?

A: You will need to become a member of Keesler Federal Credit Union to obtain a loan. The good news is that membership is typically an easy process and can often be completed simultaneously with your loan application.

Q: What if my credit isn’t perfect? Can I still get a loan?

A: Yes, credit unions like KFCU are often more flexible and willing to work with members who have varied credit histories compared to traditional banks. They may offer solutions or advice to help you improve your creditworthiness. Don’t be discouraged; apply and discuss your situation with a loan officer. They may have specific programs or options tailored for you.

Q: Does KFCU offer gap insurance or extended warranties?

A: Many credit unions, including KFCU, offer optional products like Guaranteed Asset Protection (GAP) insurance and extended warranties. These can provide valuable peace of mind. Discuss these options with your loan officer to understand their benefits and costs.

Conclusion: Drive Smarter with Keesler Federal Credit Union

Securing a car loan doesn’t have to be a stressful ordeal. By choosing a reputable, member-focused institution like Keesler Federal Credit Union, you’re already on the right track. Their commitment to competitive Keesler Federal Credit Union car loan rates, personalized service, and a diverse range of loan products makes them an excellent choice for financing your next vehicle.

Remember, the key to unlocking the best rates lies in preparation: understanding your credit, budgeting wisely, and utilizing the power of pre-approval. By following the advice in this comprehensive guide, you’ll be well-equipped to navigate the auto loan process with confidence and drive away not just in a new car, but with a smart financial decision.

Ready to take the next step towards your new vehicle? Visit the official Keesler Federal Credit Union website today to explore their current car loan rates, check your membership eligibility, and begin your application process. Your journey to a great car loan starts here!