Low Credit Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence

Low Credit Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Finding reliable transportation can be a challenge, and that challenge often feels insurmountable when you’re dealing with low credit. The dream of owning a car can seem distant, especially when you’re worried about loan rejections or sky-high interest rates. But here’s the reassuring truth: low credit doesn’t have to be a permanent roadblock to getting the car you need.

Based on my experience in the automotive and finance industry, countless individuals with less-than-perfect credit successfully secure car loans every single day. The key isn’t magic; it’s understanding your options, knowing where to look, and preparing effectively. This comprehensive guide will illuminate the path to low credit car loans near me, offering actionable advice and insights to help you navigate the process with confidence and ultimately drive away in your new vehicle.

Low Credit Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence

Understanding "Low Credit" in the Auto Loan World

Before diving into solutions, it’s crucial to understand what "low credit" actually means to a car lender. Your credit score, typically a FICO score ranging from 300 to 850, is a numerical representation of your creditworthiness. Lenders use this score, along with your credit report, to assess the risk of lending you money.

Generally, a FICO score below 600-620 is considered "subprime" or "low credit" in the auto lending world. Scores in the 300-579 range are typically classified as "very poor," while 580-669 falls into the "fair" category. These lower scores signal to lenders that you may have had difficulties managing credit in the past, such as late payments, defaults, or bankruptcies.

The primary reason lenders are hesitant with low credit scores is the perceived higher risk of default. They want assurance that you will repay the loan as agreed. However, it’s important to remember that a low score doesn’t automatically disqualify you from getting a car loan. It simply means you’ll need to approach the process strategically and understand that the terms might differ from someone with excellent credit.

Why Finding a Car Loan with Low Credit is Crucial (and Possible)

For many people, a car isn’t a luxury; it’s a necessity. Reliable transportation is often essential for getting to work, taking children to school, running errands, and maintaining independence. Without it, daily life can become incredibly difficult and stressful.

The good news is that the auto lending industry recognizes this widespread need. There’s a significant market for "subprime auto loans" specifically designed for individuals with low credit scores. These lenders understand that life happens, and past financial difficulties shouldn’t permanently prevent someone from obtaining essential transportation.

What we’ve learned working with countless clients is that while the journey might require a bit more effort and research, securing a car loan with low credit is absolutely possible. It’s about finding the right lender, understanding their requirements, and presenting yourself as a responsible borrower despite your credit history. This market exists because lenders want to help you, provided you can demonstrate a clear ability to repay.

Strategies for Securing Low Credit Car Loans Near You

When your credit score isn’t ideal, knowing where to turn for a car loan makes all the difference. Fortunately, several avenues specialize in helping individuals just like you. Let’s explore the most effective strategies for finding low credit car loans near me.

Local Dealerships: Buy Here, Pay Here & Subprime Specialists

Local dealerships are often the first stop for many car buyers, and they can be particularly helpful for those with low credit. There are two main types to consider:

1. Buy Here, Pay Here (BHPH) Dealerships:

These dealerships are unique because they act as both the car seller and the lender. Instead of arranging financing through a third-party bank, you make your payments directly to the dealership. This direct lending model often allows for more flexible approval criteria, making them a viable option for individuals with very low or no credit.

- Pros: Easier approval, especially for those with severe credit challenges. The application process is often quicker and less stringent.

- Cons: Interest rates are typically much higher than traditional loans, and the selection of vehicles might be limited to older, higher-mileage cars. Furthermore, not all BHPH dealerships report payments to credit bureaus, which means it might not help rebuild your credit unless they explicitly state they do.

2. Dealerships with Subprime Specialists:

Many traditional new and used car dealerships have finance departments that specialize in working with a wide range of credit scores, including subprime. These dealerships often have relationships with multiple lenders—banks, credit unions, and finance companies—that specifically cater to borrowers with low credit.

- How they work: The finance manager acts as an intermediary, submitting your application to several lenders to find one willing to approve you. They understand the nuances of low credit financing and can often match you with a program suitable for your situation.

- Based on my experience, many local dealerships actively seek to assist buyers with low credit. They understand that this demographic represents a significant portion of the market and have dedicated resources to serve them. Don’t be shy about discussing your credit situation upfront; transparency helps them find the best solution.

Online Lenders Specializing in Bad Credit

In today’s digital age, online lenders have become a powerful resource for low credit car loans near me. These platforms often have vast networks of lenders, many of whom specialize exclusively in subprime auto financing.

The application process is typically quick and convenient, allowing you to get pre-qualified from the comfort of your home. You can often receive multiple offers, enabling you to compare terms and choose the best fit without visiting several physical locations.

Pro tips from us: When using online lenders, always compare interest rates, loan terms, and any associated fees. Read reviews and ensure the lender is reputable. Look for platforms that offer pre-qualification with a soft credit inquiry, which won’t impact your credit score.

Credit Unions

Credit unions are member-owned financial institutions known for their community focus and often more lenient lending practices compared to large banks. If you’re already a member of a credit union, or if you qualify for membership (often based on location, employer, or association), they can be an excellent option for low credit car loans.

Credit unions are sometimes more willing to look beyond just your credit score and consider your overall financial situation, your relationship with them, and your ability to repay. Their interest rates can also be more competitive than those offered by subprime finance companies.

Banks (with conditions)

While traditional banks often have stricter lending criteria, they shouldn’t be entirely ruled out. If you have an existing relationship with a bank (e.g., checking or savings account), they might be more inclined to work with you.

It’s worth inquiring about their auto loan options, especially if you can offer a substantial down payment or have a co-signer. Banks typically offer competitive rates for those who qualify, so it’s always worth a conversation.

The Power of a Co-Signer

A co-signer can significantly improve your chances of approval for a low credit car loan. A co-signer is someone with good credit who agrees to take on the responsibility of the loan if you fail to make payments. Their strong credit profile provides an additional layer of security for the lender, reducing their risk.

- Benefits: A co-signer can help you secure approval, potentially at a lower interest rate than you’d get on your own. This can save you a substantial amount of money over the life of the loan.

- Common mistakes to avoid are not fully understanding the co-signer’s liability. The co-signer is equally responsible for the loan, and any missed payments will negatively affect their credit score as well as yours. Ensure both parties are fully aware of the commitment and have a clear agreement in place.

Leveraging a Down Payment

Making a significant down payment is one of the most powerful tools you have when seeking a low credit car loan. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk.

- Why it helps: Lenders see a down payment as a sign of your commitment and financial responsibility. It shows you have some skin in the game. It can lead to better loan terms, a lower monthly payment, and a higher chance of approval.

- Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment if possible. Even a smaller down payment is better than none. Every dollar you put down reduces your loan principal and the total interest you’ll pay.

Preparing for Your Low Credit Car Loan Application

Preparation is key to a smooth and successful car loan application, especially when dealing with low credit. Taking these steps beforehand will not only increase your chances of approval but also help you secure better terms.

Know Your Credit Score and Report

Before you even step foot in a dealership or fill out an online application, obtain copies of your credit report from all three major bureaus (Equifax, Experian, and TransUnion). You are entitled to a free report from each once every 12 months via AnnualCreditReport.com. This is a crucial first step.

Review your reports meticulously for any errors or inaccuracies. Mistakes are common, and disputing and correcting them can potentially boost your score. Understanding your score gives you a realistic expectation of the loan terms you might qualify for and helps you identify areas for improvement.

Budgeting Realistically

A car loan isn’t just about the monthly payment. You need to consider the total cost of car ownership. This includes:

- Monthly loan payment: Ensure it fits comfortably within your budget.

- Car insurance: Rates can be higher for newer cars or for drivers with a low credit score.

- Fuel costs: Factor in your daily commute and other driving habits.

- Maintenance and repairs: Even a reliable used car will eventually need service.

- Registration and taxes: These are often annual expenses.

Pro tips from us: Create a detailed monthly budget that accounts for all your income and expenses. Be honest with yourself about what you can truly afford. Overextending yourself on a car loan can lead to financial strain and potentially more credit issues down the road. Lenders will also look at your debt-to-income ratio, so knowing this beforehand helps you set realistic expectations.

Gathering Necessary Documents

Having all your documents ready before you apply can significantly speed up the approval process and demonstrate your preparedness to lenders. Here’s a list of commonly requested items:

- Proof of Income: Recent pay stubs (typically the last 2-3 months), bank statements, or tax returns if you’re self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement with your current address.

- Identification: Valid driver’s license or state ID.

- Social Security Number: For credit checks.

- References: Sometimes required, especially for subprime lenders.

- Proof of Insurance: You’ll need this before driving off the lot.

Pro tips from us: Organize these documents in a folder or digitally so they are easily accessible. This shows lenders you are serious and organized, which can be a small but positive signal.

Navigating the Application and Approval Process

Once you’ve prepared, it’s time to engage with lenders. Understanding the nuances of the application process can help you make informed decisions and avoid potential pitfalls.

Pre-Qualification vs. Pre-Approval

These terms are often used interchangeably, but there’s a crucial difference:

- Pre-Qualification: This is a preliminary assessment based on basic financial information you provide. It usually involves a "soft" credit inquiry, which doesn’t affect your credit score. Pre-qualification gives you an estimate of what you might be approved for and helps you understand your options without committing.

- Pre-Approval: This is a more definitive offer from a lender. It involves a "hard" credit inquiry, which will temporarily impact your credit score by a few points. With pre-approval, the lender has reviewed your full credit report and financial details, giving you a concrete loan amount and terms.

Pro tips from us: Always aim for pre-approval from a few different lenders before you start serious car shopping. Having a pre-approval in hand gives you significant leverage at the dealership, allowing you to focus on negotiating the car’s price rather than worrying about financing.

Understanding Loan Terms

When reviewing loan offers, pay close attention to these key terms:

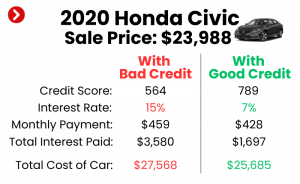

- Interest Rate (APR): This is the cost of borrowing money, expressed as a percentage. For low credit car loans, APRs will typically be higher. Even a small difference in the APR can save you hundreds or thousands of dollars over the life of the loan.

- Loan Term: This is the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term means lower monthly payments, but you’ll pay more in total interest over time. A shorter term means higher monthly payments but less overall interest.

- Total Cost of the Loan: Always calculate the total amount you will pay over the life of the loan, including principal and interest. Sometimes a lower monthly payment on a longer term can result in a much higher total cost.

Avoiding Predatory Lenders

From my years in the industry, I’ve seen that while many lenders genuinely want to help, some unfortunately target vulnerable individuals with low credit. Common mistakes to avoid are falling for "guaranteed approval" scams or high-pressure sales tactics. Be wary of:

- Guaranteed Approval: No legitimate lender can guarantee approval without first reviewing your financial information.

- Excessively High Interest Rates: While higher rates are expected with low credit, rates above 25-30% should raise a red flag unless your credit is extremely poor and you have no other options.

- Hidden Fees or Unclear Terms: Always read the fine print. If a lender is reluctant to explain terms or pushes you to sign quickly, walk away.

- "Packing" the Loan: Adding unnecessary products like extended warranties or GAP insurance without clear explanation, especially if they inflate your loan significantly.

Pro tips from us: Trust your gut. If an offer seems too good to be true, it probably is. Don’t be afraid to ask questions, take the paperwork home to review, or get a second opinion.

Rebuilding Your Credit Through a Car Loan

One of the most significant long-term benefits of successfully securing and managing a low credit car loan is the opportunity it provides to rebuild your credit. This isn’t just about getting a car now; it’s about paving the way for better financial opportunities in the future.

When you make your car loan payments on time, every month, the lender reports this positive activity to the credit bureaus. This consistent, responsible payment history is a powerful factor in improving your credit score over time. A higher credit score will eventually open doors to lower interest rates on future loans, better credit card offers, and even better rates on insurance and housing.

View your car loan as an investment in your financial future. It’s a chance to demonstrate your reliability and commitment to managing debt responsibly, proving to future lenders that you are a worthy borrower.

Pro Tips for Success with Low Credit Car Loans

To maximize your chances of success and secure the best possible terms for your low credit car loan, keep these expert tips in mind:

- Don’t Settle for the First Offer: Just because you have low credit doesn’t mean you should accept the very first loan offer you receive. Shop around with multiple lenders – online, credit unions, and dealerships – to compare interest rates and terms. This due diligence can save you a lot of money.

- Negotiate the Car Price, Not Just the Loan: Remember that the car’s price directly impacts the loan amount. Focus on negotiating the best possible price for the vehicle first. A lower purchase price means you borrow less, which is always advantageous, especially with higher interest rates.

- Consider a Less Expensive, Reliable Used Car: While a new car is appealing, a reliable used car is often a more practical choice for those with low credit. The lower purchase price means a smaller loan, potentially making it easier to get approved and keeping your monthly payments manageable. You can find excellent value in the used car market.

- Understand the Full Cost of Ownership: Beyond the loan payment, factor in insurance, fuel, and maintenance. Don’t let a seemingly affordable monthly payment overshadow the overall financial commitment. Ensure the total cost aligns with your budget.

- Be Honest About Your Financial Situation: Transparency with lenders is crucial. While it might feel uncomfortable to discuss past credit issues, being upfront allows lenders to better understand your situation and find appropriate financing solutions. Trying to hide information can lead to complications or even rejection.

- Understand Car Loan Interest Rates: Education is power. Take the time to understand how interest rates are calculated and what factors influence them. This knowledge will empower you to identify fair offers and question anything that seems out of place.

Conclusion: Drive Away with Confidence

Securing a car loan when you have low credit can seem daunting, but as this guide illustrates, it’s far from impossible. By understanding the landscape of low credit car loans near me, preparing diligently, and approaching the process strategically, you can absolutely find the right financing and drive away in a vehicle that meets your needs.

Remember, your low credit score is a snapshot of your past, not a life sentence. With careful planning, thorough research, and a commitment to responsible repayment, a car loan can not only provide you with essential transportation but also serve as a powerful tool to rebuild and strengthen your credit for a brighter financial future. Don’t let past financial challenges hold you back from the freedom and independence that a reliable car can offer. Start your search today, armed with knowledge and confidence!