Low Down Payment Bad Credit Car Loans: Your Comprehensive Guide to Getting Approved

Low Down Payment Bad Credit Car Loans: Your Comprehensive Guide to Getting Approved Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a labyrinth, especially when you’re dealing with bad credit and hoping for a low down payment. Many people assume that having a less-than-perfect credit score automatically disqualifies them from purchasing a reliable vehicle without a hefty upfront cost. However, this isn’t necessarily true.

The reality is, securing low down payment bad credit car loans is not just a pipe dream; it’s a viable path for many. It requires understanding the process, knowing where to look, and presenting yourself as a responsible borrower. This comprehensive guide will break down everything you need to know, from understanding your credit situation to driving away in your new car.

Low Down Payment Bad Credit Car Loans: Your Comprehensive Guide to Getting Approved

Understanding the Landscape: Bad Credit and Car Loans

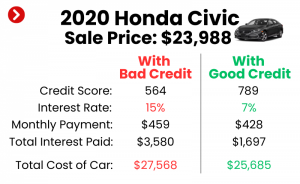

Before diving into strategies, let’s clarify what "bad credit" typically means in the eyes of an auto lender. Credit scores, primarily FICO and VantageScore, range from 300 to 850. Generally, a score below 600-620 is considered "subprime" or "bad credit."

Lenders use these scores to assess your creditworthiness. A lower score suggests a higher risk of default, making them more hesitant to lend money. This hesitation often translates into higher interest rates or a requirement for a larger down payment to mitigate their risk.

Based on my experience, many people with bad credit feel trapped, believing their only options are exorbitant interest rates or saving for years. While the terms might not be as favorable as for someone with excellent credit, there are indeed specialized avenues for bad credit car financing that consider your current financial stability over your past credit mishaps.

The Reality of Low Down Payment Bad Credit Car Loans

So, what exactly constitutes a "low down payment" in this context? For prime borrowers, 10-20% of the car’s value is typical. For those with bad credit, lenders often ask for 20% or more. Therefore, a "low" down payment could be anything from 0% (which is rare and comes with significant caveats) to 5-10% of the vehicle’s purchase price.

It’s crucial to manage expectations. While possible, a zero-down payment with bad credit is exceptionally challenging to obtain and usually comes with the highest interest rates. The goal here is to understand that even a small down payment can significantly improve your chances and reduce your overall costs.

Lenders offering subprime auto loans understand that life happens. They are willing to work with individuals who have experienced financial difficulties but are now in a stable position to make consistent payments. Their business model revolves around assessing current income, employment stability, and debt-to-income ratio, often more than just your credit score.

Strategies for Securing a Low Down Payment Bad Credit Car Loan

Securing an auto loan with bad credit and a low down payment requires a strategic approach. It’s not about magic, but about preparation and knowing the right steps. Here are some proven strategies:

1. Improve Your Credit Score (Even Slightly)

While you might be in urgent need of a car, even a small improvement in your credit score can make a difference. Every point counts when lenders are evaluating risk.

- Check Your Credit Report for Errors: Based on my experience, a surprising number of credit reports contain errors that can unfairly drag down your score. Obtain free copies of your credit report from AnnualCreditReport.com and dispute any inaccuracies immediately.

- Pay Down Small Debts: If you have any outstanding small debts, like a past-due utility bill or a minor credit card balance, paying them off can give your score a quick boost. It shows lenders you are taking proactive steps to manage your finances.

- Become an Authorized User: If a trusted family member has excellent credit, ask them to add you as an authorized user on one of their credit cards. Their positive payment history can reflect on your report, though this requires trust and open communication. For a deeper dive into improving your credit score, read our detailed guide on .

2. Save for Any Down Payment

Even if your goal is a "low" down payment, having some money to put down is always better than none. A down payment, no matter how small, offers several advantages:

- Reduces Lender Risk: It shows the lender you have "skin in the game" and are committed to the purchase.

- Lowers Loan Amount: A smaller loan means less risk for the lender and potentially better terms for you.

- Combats Negative Equity: Cars depreciate quickly. A down payment helps prevent you from owing more than the car is worth, a common problem with no money down car loans.

- Decreases Monthly Payments: Even a few hundred dollars down can make your monthly payments more manageable.

Pro tips from us: Even if you only have $500, put it down. It demonstrates responsibility and can open doors that might otherwise remain closed.

3. Find the Right Lender

Not all lenders are created equal, especially when it comes to car loans for poor credit. Targeting the right institutions is crucial.

- Special Finance Dealerships: Many dealerships have "special finance" departments or work with a network of subprime lenders. These dealerships are equipped to handle applicants with challenging credit histories. They understand the nuances of auto loans for low credit scores and often have more flexible criteria.

- Credit Unions: Credit unions are member-owned and often have more lenient lending requirements compared to traditional banks. They may be more willing to look beyond your credit score and consider you as an individual member.

- Online Lenders Specializing in Subprime: Several online platforms connect borrowers with lenders who specialize in bad credit auto loans. These platforms can offer a streamlined application process and a wider range of options.

- Avoid Buy-Here-Pay-Here (BHPH) as a First Resort: While BHPH dealerships can be a last resort for those who can’t get approved elsewhere, they typically come with very high interest rates and often report only to one credit bureau (or none), limiting your ability to rebuild credit. Their car selections might also be less reliable.

4. Consider a Co-signer

If you have a trusted friend or family member with good credit, asking them to co-sign your loan can significantly improve your chances of approval and potentially secure a lower interest rate.

- Pros: A co-signer’s strong credit score can offset your bad credit, making you a more attractive borrower. This can lead to better loan terms.

- Cons: The co-signer becomes equally responsible for the loan. If you miss payments, their credit will suffer, and they could be on the hook for the entire debt. This decision should not be taken lightly and requires open communication.

5. Choose the Right Car

The type of car you choose plays a huge role in the approval process. Lenders are more likely to approve a loan for a lower-priced, reliable vehicle.

- Affordable, Reliable Used Car: Focus on used cars that are known for their longevity and lower maintenance costs. A less expensive car means a smaller loan amount, which is less risky for the lender. To understand the nuances of buying a used car, explore our article on .

- Avoid Luxury or Brand New Vehicles: These vehicles depreciate rapidly and carry a higher price tag, making them a much riskier investment for lenders when dealing with a bad credit applicant. Aim for practical, not aspirational, in this situation.

6. Gather Necessary Documentation

Being prepared with all required documents can speed up the application process and demonstrate your readiness.

- Proof of Income: Pay stubs, tax returns, bank statements.

- Proof of Residency: Utility bills, lease agreement.

- Proof of Identity: Driver’s license, state ID.

- References: Sometimes required.

- Proof of Insurance: You’ll need this before driving off the lot.

The Application Process: What to Expect

Once you’ve done your homework and chosen a potential lender or dealership, it’s time to apply. The process for low down payment bad credit car loans can differ slightly from standard applications.

Most lenders will offer a pre-qualification option. This involves a "soft pull" on your credit, which doesn’t affect your score, and gives you an idea of what you might be approved for. It’s an excellent way to gauge your options without commitment.

The full application, however, will involve a "hard pull" on your credit, which can temporarily ding your score by a few points. During this stage, lenders will scrutinize several factors beyond your credit score:

- Income Stability: They want to see consistent employment and sufficient income to cover monthly payments.

- Debt-to-Income (DTI) Ratio: This measures how much of your gross monthly income goes towards debt payments. A lower DTI indicates you have more disposable income to handle a new car payment.

- Job History: Lenders prefer to see a stable work history, often looking for at least six months to a year at your current job.

- Residency Stability: Demonstrating a stable living situation also adds to your profile as a reliable borrower.

Common mistakes to avoid are applying to too many places at once within a short period, which can lower your score further, or not being transparent about your financial situation. Be honest and provide accurate information.

Navigating the Loan Terms and Conditions

Once approved, carefully review the loan terms. This is where understanding the true cost of your bad credit car financing comes into play.

- Annual Percentage Rate (APR): This is the most critical number. It represents the total cost of borrowing, including the interest rate and any fees. For borrowers with bad credit, expect a higher APR. Even with a low down payment, a high APR can significantly increase your total repayment amount.

- Loan Term: This is the length of time you have to repay the loan, typically 36 to 72 months. A longer term means lower monthly payments but significantly more interest paid over the life of the loan.

- Monthly Payments: While it’s tempting to focus solely on the monthly payment, always consider it in conjunction with the APR and loan term. A low monthly payment might come at the cost of a very long term and excessive interest.

Pro tips from us: Don’t just focus on the monthly payment. Understand the total amount you will pay over the life of the loan. Ask about any prepayment penalties, as paying off your loan early could save you interest. You can learn more about understanding loan terms on reliable financial education sites like Investopedia. .

Pro Tips for Success and Rebuilding Credit

Getting approved for a low down payment bad credit car loan is just the first step. The ultimate goal should be to use this opportunity to rebuild your credit and improve your financial standing.

- Make Payments On Time, Every Time: This is the single most important action you can take. Consistent on-time payments will positively impact your credit score over time, demonstrating your reliability to future lenders.

- Consider Refinancing Later: Once you’ve made 6-12 months of on-time payments, and if your credit score has improved, consider refinancing your car loan. Refinancing can allow you to secure a lower interest rate, reducing your monthly payments or the total amount of interest paid.

- Budgeting for Car Ownership: Remember that a car involves more than just the loan payment. Factor in insurance, fuel, maintenance, and potential repairs. A common mistake to avoid is underestimating these additional costs, which can lead to financial strain and missed payments.

- Avoid Taking on More Debt: While you’re working to improve your credit, try to avoid opening new credit lines or taking on additional debt. This helps keep your DTI ratio low and demonstrates financial prudence.

Common mistakes to avoid are missing payments, extending the loan term for too long just to get a lower monthly payment (which costs more in the long run), and buying a car that is beyond your means. A reliable vehicle that fits your budget is far more beneficial than an expensive one that jeopardizes your financial recovery.

Real-Life Scenarios and Common Questions

Many individuals with bad credit have unique situations. Let’s address some common questions:

- Can I get a loan with a bankruptcy? Yes, it’s possible, especially if the bankruptcy has been discharged. Lenders will want to see that you’ve re-established some credit and are on a path to financial recovery. The longer it’s been since discharge, the better your chances.

- What if I have no credit history? This is different from bad credit. Some lenders offer "first-time buyer" programs. You might still need a co-signer or a slightly larger down payment, but it’s often easier than overcoming severe bad credit, as there are no negative marks.

- Is "guaranteed approval" real? Be extremely wary of any lender promising "guaranteed approval" for guaranteed approval car loans without any credit check. While some dealerships advertise this, it usually means you’ll be subjected to very high interest rates, unfavorable terms, or directed to a buy-here-pay-here lot. Always read the fine print and understand the true cost.

Conclusion

Securing low down payment bad credit car loans is a challenging but achievable goal. It requires diligent research, strategic planning, and a commitment to responsible financial behavior. By understanding your credit situation, exploring specialized lenders, preparing a down payment (however small), and carefully reviewing loan terms, you can navigate this process successfully.

Remember, this isn’t just about getting a car; it’s an opportunity to rebuild your financial standing. Make your payments on time, manage your budget wisely, and you’ll not only enjoy the convenience of your new vehicle but also pave the way for a healthier credit future. Start your research today and take the first step towards driving the car you need, responsibly.