Master Your Car Loan Repayments: The Ultimate Guide to Financial Freedom on Wheels

Master Your Car Loan Repayments: The Ultimate Guide to Financial Freedom on Wheels Carloan.Guidemechanic.com

For many of us, a car isn’t just a mode of transport; it’s a vital part of daily life, connecting us to work, family, and opportunities. And for most, securing that vehicle involves a car loan. But getting the loan is just the first step. The true journey, and often the most critical, lies in understanding and effectively managing your car loan repayments. This isn’t just about making monthly payments; it’s about smart financial strategy, saving money, and ultimately achieving financial peace of mind.

Based on my extensive experience in personal finance and helping countless individuals navigate their automotive financing, mastering your car loan is a cornerstone of responsible debt management. This comprehensive guide will equip you with the knowledge, strategies, and insights you need to take control of your auto loan payments, ensuring you drive towards financial success, not stress.

Master Your Car Loan Repayments: The Ultimate Guide to Financial Freedom on Wheels

Understanding the Anatomy of Your Car Loan Repayments

Before you can effectively manage something, you must first understand its core components. Your monthly car loan payment isn’t just a number; it’s a carefully calculated sum derived from several key factors. Let’s break down what truly makes up your car loan repayments.

What Makes Up Your Monthly Payment?

Every payment you make towards your car loan is typically split into two primary components: principal and interest. Understanding this split is fundamental to smart repayment strategies.

The Principal: Your Original Loan Amount

The principal is the actual amount of money you borrowed to purchase your vehicle. Think of it as the base cost of your car, minus any down payment you made. Each payment you make reduces this principal amount, bringing you closer to owning your car outright.

Initially, a smaller portion of your payment might go towards the principal, especially in longer loan terms. As the loan matures, a larger share typically shifts to reducing the principal balance. This gradual reduction of the principal is what allows you to build equity in your vehicle over time.

The Interest: The Cost of Borrowing

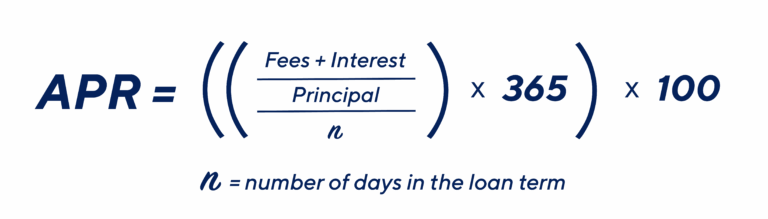

Interest is essentially the fee your lender charges you for borrowing their money. It’s the profit margin for the financial institution. This cost is usually expressed as an Annual Percentage Rate (APR). The higher your APR, the more you pay in interest over the life of the loan.

Interest can be calculated in different ways. Most car loans use a simple interest method, meaning interest is calculated daily on the outstanding principal balance. This is why making extra payments specifically towards the principal can be so powerful – it immediately reduces the balance on which future interest is calculated.

Additional Fees (If Any)

While not always a standard part of every monthly payment, some car loans may include or have associated fees. These could range from origination fees at the start of the loan to late payment fees if you miss a due date. It’s crucial to review your loan agreement carefully to understand all potential costs.

Common mistakes to avoid are overlooking these fees in the initial excitement of getting a new car. Always ask your lender for a full breakdown of all charges. Transparency is key when signing any financial document.

Key Factors Influencing Your Car Loan Repayments

Several variables play a significant role in determining the size of your monthly payment and the total cost of your loan. Being aware of these factors empowers you to make informed decisions.

The Loan Amount: How Much You Borrowed

This is perhaps the most straightforward factor. The more money you borrow, the higher your monthly car loan payments will generally be, assuming all other factors remain constant. A larger loan amount means more principal to repay and more interest to accrue.

This highlights the importance of making a substantial down payment. A larger down payment reduces the principal amount you need to finance, leading to lower monthly payments and less interest paid overall.

The Interest Rate (APR): Your Cost of Credit

Your interest rate is arguably the most impactful factor on the total cost of your loan. A lower interest rate means you pay less for the privilege of borrowing, significantly reducing your overall expenses. This rate is heavily influenced by your credit score, the current market conditions, and the loan term.

Even a small difference in the APR can translate to hundreds or thousands of dollars saved over the life of the loan. Always shop around for the best rates and don’t settle for the first offer.

The Loan Term: How Long You’ll Pay

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term will result in lower monthly payments, which might seem attractive. However, this often comes at a significant cost.

With a longer term, you’re paying interest for a longer period, meaning the total interest paid over the life of the loan will be considerably higher. Conversely, a shorter loan term means higher monthly payments but less total interest paid and faster debt freedom. It’s a balance between affordability and total cost. .

Your Credit Score: The Foundation of Your Rate

Your credit score is a numerical representation of your creditworthiness. Lenders use it to assess the risk of lending to you. A higher credit score signals to lenders that you are a reliable borrower, often qualifying you for the lowest interest rates available.

Conversely, a lower credit score typically results in higher interest rates, as lenders perceive a greater risk. Building and maintaining a strong credit score is paramount for securing favorable car loan repayment terms.

Strategies for Smart Car Loan Repayment Management

Now that you understand the mechanics, let’s explore actionable strategies to manage your car loan repayments effectively. These tips are designed to save you money, reduce stress, and accelerate your path to car ownership.

Budgeting for Success: Your Financial Roadmap

Effective budgeting is the cornerstone of responsible financial management, especially when it comes to recurring debts like car loans. Without a clear budget, it’s easy to fall behind or miss opportunities to save.

Creating a Realistic Budget

Start by creating a detailed budget that tracks all your income and expenses. Understand exactly how much disposable income you have each month after essential bills are paid. Your car loan payment should fit comfortably within this budget, without stretching your finances too thin.

Pro tips from us: Use a spreadsheet, a budgeting app, or even pen and paper. The key is consistency and accuracy. Account for both fixed expenses (rent, utilities) and variable expenses (groceries, entertainment).

Automating Your Payments

One of the simplest yet most effective strategies is to automate your monthly car loan payments. Set up an automatic transfer from your checking account to your lender on or before the due date. This ensures you never miss a payment, protecting your credit score and avoiding late fees.

Automation provides peace of mind and frees up mental energy. Just make sure you always have sufficient funds in your account to cover the payment.

Building an Emergency Fund

Life is unpredictable. Unexpected expenses like medical emergencies or job loss can quickly derail your ability to make car loan repayments. That’s where an emergency fund comes in. Aim to save at least 3-6 months’ worth of living expenses in a readily accessible savings account.

This fund acts as a financial safety net, allowing you to cover your car payments and other essential bills during unforeseen circumstances. It’s a critical component of any robust financial plan.

Making Extra Payments: The Power of Principal Reduction

This is where you can truly accelerate your debt payoff and save a significant amount on interest. Every extra dollar you pay towards your loan, specifically marked for principal, works wonders.

How Extra Payments Reduce Interest and Shorten the Term

When you make an extra payment, and instruct your lender to apply it directly to the principal, you immediately reduce the balance on which future interest is calculated. This has a compounding effect: less principal means less interest, which means more of your regular payments go towards principal, snowballing your progress.

Even small, consistent extra payments can shave months off your loan term and save you hundreds or thousands in interest. It’s one of the most powerful strategies for managing car loan repayments.

The Bi-Weekly Payment Strategy

Consider switching to a bi-weekly payment schedule. Instead of one monthly payment, you make half of your monthly payment every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments annually instead of 12.

This "extra" payment each year goes directly towards the principal, significantly shortening your loan term and reducing total interest. Always confirm with your lender if they support bi-weekly payments and how to ensure the extra payment is applied to the principal.

Lump-Sum Payments

If you receive a bonus, a tax refund, or any unexpected windfall, consider making a lump-sum payment towards your car loan principal. This can provide a substantial boost to your repayment efforts, dramatically cutting down the remaining balance and future interest.

Even a few hundred dollars can make a noticeable difference, especially early in the loan term when the interest component of your payments is higher. Always specify that the extra payment should go to the principal.

Refinancing Your Car Loan: A Fresh Start

Refinancing involves taking out a new loan to pay off your existing car loan, ideally with better terms. This can be a game-changer for your car loan repayments.

When Refinancing is a Good Idea

Refinancing is particularly beneficial if:

- Interest Rates Have Dropped: If market rates are lower than when you originated your loan.

- Your Credit Score Has Improved: A higher score can qualify you for a much better rate.

- You Want a Shorter Term: To pay off the loan faster and save on interest (though monthly payments will increase).

- You Want a Lower Monthly Payment: By extending the loan term, but be wary of the increased total interest.

Based on my experience, many people overlook refinancing opportunities. It’s always worth checking if you can secure a better deal, especially if a year or two has passed since your original loan.

The Refinancing Process

The process typically involves applying to new lenders, providing financial information, and getting approved for a new loan. The new lender then pays off your old loan, and you start making payments to them under the new terms.

Pro tips from us: Shop around with multiple lenders (banks, credit unions, online lenders) to compare offers. Look not just at the interest rate but also any fees associated with the new loan.

Things to Watch Out For

While beneficial, refinancing isn’t without its potential pitfalls. Avoid extending your loan term too much just to lower your monthly payment, as this will lead to paying significantly more interest over time. Also, be aware of any prepayment penalties on your existing loan, which could offset the benefits of refinancing.

Ensure the new loan doesn’t come with high fees that negate the interest savings. Always do the math to ensure it’s truly a beneficial move for your specific situation.

Dealing with Balloon Payments (If Applicable)

Some car loans, particularly in certain regions or for specific types of vehicles, might include a balloon payment. This is a large, lump-sum payment due at the very end of the loan term.

Explanation of What They Are

A balloon payment loan structure allows for lower monthly payments throughout the loan term, as a significant portion of the principal is deferred until the end. It can make expensive cars seem more affordable on a monthly basis.

However, the catch is that you must be prepared for that substantial final payment. If you’re not ready, it can lead to financial strain.

Planning for the Final Lump Sum

If your loan includes a balloon payment, start saving for it from day one. Treat it like a separate savings goal. You might consider setting up a dedicated savings account and making regular contributions.

Alternatively, you could plan to sell or trade in the vehicle before the balloon payment is due, using the proceeds to cover the outstanding balance. Or, you might plan to refinance the balloon payment into a new, traditional loan. Understand your options well in advance.

Common Pitfalls and How to Avoid Them

Even with the best intentions, it’s easy to stumble when it comes to car loan repayments. Being aware of common mistakes can help you steer clear of financial trouble.

Ignoring the Fine Print: Your Loan Agreement

The loan agreement is a legally binding contract, yet many borrowers don’t read it thoroughly. This oversight can lead to unpleasant surprises down the road.

Prepayment Penalties

Some lenders impose prepayment penalties if you pay off your loan early, either in full or by making significant extra payments. This is less common with car loans than with mortgages, but it does exist. Always check your loan agreement for any such clauses before accelerating your payments.

If a penalty exists, calculate if the interest savings from early repayment still outweigh the penalty fee. Sometimes, it still makes financial sense to pay early.

Late Payment Fees

Missing a payment or paying late will almost certainly incur a late fee, adding to your debt. These fees can vary but are an unnecessary expense that can be easily avoided through diligent budgeting and automated payments.

More importantly, late payments are reported to credit bureaus and can significantly damage your credit score, impacting your ability to secure favorable rates for future loans.

Default Clauses

Your loan agreement will outline what constitutes a default (e.g., missing multiple payments). Defaulting can lead to severe consequences, including vehicle repossession and significant damage to your credit history. Understand these terms clearly.

If you anticipate difficulty making a payment, proactively contact your lender. They may be willing to work with you on a temporary solution, such as deferring a payment, rather than resorting to default.

Borrowing More Than You Can Afford

It’s tempting to get the newest, most feature-rich car, but borrowing beyond your means is a common and dangerous trap. This often happens when focusing solely on the monthly payment.

The Trap of Extending Loan Terms

Lenders might offer very long loan terms (e.g., 72 or 84 months) to make expensive cars seem affordable with low monthly payments. While the monthly payment might fit your budget, the total cost of the loan due to accumulated interest will be substantially higher. You could end up paying far more for the car than its actual value.

You also risk being "upside down" on your loan (owing more than the car is worth) for a longer period, making it difficult to sell or trade in the vehicle.

Focus on Total Cost, Not Just Monthly Payment

Always look at the total amount you will pay over the life of the loan, not just the monthly installment. A lower monthly payment over a longer term almost always means a higher total cost. Use online loan calculators to compare different loan terms and interest rates to see the full financial picture.

Pro tips from us: Aim for the shortest loan term you can comfortably afford. This minimizes interest paid and gets you to debt freedom faster.

Skipping Payments: A Costly Mistake

Skipping payments, even for one month, can have a ripple effect on your finances and credit. It’s a critical error that should be avoided at all costs.

Consequences for Credit Score and Potential Repossession

A missed payment can be reported to credit bureaus, dropping your credit score significantly. This makes it harder and more expensive to borrow money for mortgages, future car loans, or even credit cards. Repeated missed payments can lead to your lender repossessing your vehicle.

Repossession not only means losing your car but also leaves a major negative mark on your credit report for years, potentially making it very difficult to obtain credit in the future.

Communicating with Your Lender

If you anticipate difficulty making a payment, do not wait until you miss it. Contact your lender immediately. Explain your situation and explore options. Many lenders have hardship programs or can offer a temporary deferment (though interest may still accrue).

Open communication is always better than silence and can help you avoid the severe consequences of missed payments.

Advanced Strategies and Future Planning

Once you’ve mastered the basics, consider these advanced strategies to optimize your car loan repayments and integrate them into your broader financial goals.

Impact of Your Credit Score Beyond the Loan

Your credit score’s influence doesn’t end once you’ve secured your car loan. It continues to play a vital role in your financial life.

Maintaining and Improving Your Score

Consistently making on-time auto loan payments is an excellent way to build and maintain a strong credit score. Your payment history is the most significant factor in calculating your score. As you diligently pay down your car loan, you demonstrate responsible credit behavior.

To further improve your score, keep your credit utilization low on credit cards and address any errors on your credit report. .

How It Affects Future Loans

A high credit score ensures you’ll qualify for the best interest rates on future loans, whether it’s another car, a mortgage, or a personal loan. This translates directly into significant savings over your lifetime. Your car loan is a stepping stone to a stronger financial future.

Conversely, a poor payment history on your car loan can make future borrowing difficult and more expensive, trapping you in a cycle of high-interest debt.

Selling Your Car with an Outstanding Loan

Life circumstances change, and you might need to sell your car before the loan is fully paid off. This is a common situation with specific considerations.

Process and Considerations

If you decide to sell your car with an outstanding loan, the first step is to determine your loan payoff amount from your lender. This is the exact sum needed to clear your debt. You’ll then need to sell the car for at least that amount.

The process usually involves the buyer paying the lender directly for the payoff amount, and any remaining balance (if you sell for more than you owe) going to you. If you sell for less than you owe, you’ll need to pay the difference out of pocket.

Positive vs. Negative Equity

- Positive Equity: This means your car is worth more than the outstanding loan balance. You can sell the car, pay off the loan, and pocket the difference. This is the ideal scenario.

- Negative Equity (Upside Down): This means you owe more on the car than it’s currently worth. If you sell, you’ll have to pay the lender the difference out of your own funds, or roll that negative equity into a new car loan, which is generally not recommended.

Managing your car loan repayments effectively, especially by making extra payments, helps build positive equity faster, giving you more flexibility if you decide to sell.

The Long-Term View: Financial Freedom Beyond Car Loans

Think of your car loan repayment journey as a valuable training ground for broader financial success. The discipline and strategies you learn here are transferable.

Applying Lessons Learned to Other Debts

The principles of budgeting, making extra principal payments, and avoiding high-interest debt are applicable to mortgages, student loans, and credit card debt. Mastering your car loan can give you the confidence and experience to tackle larger financial challenges.

It’s about cultivating responsible borrowing habits and understanding the true cost of debt.

Building Wealth

Every dollar you save on interest or accelerate in debt payoff is a dollar that can be invested, saved, or used to pursue other financial goals. By efficiently managing your car loan, you free up cash flow that can contribute to your retirement fund, a down payment on a home, or other wealth-building endeavors.

This holistic approach to finance is what truly leads to long-term financial freedom.

Conclusion: Drive Towards Financial Empowerment

Navigating car loan repayments might seem daunting, but armed with the right knowledge and strategies, it becomes a powerful tool for financial empowerment. From understanding the core components of your payment to implementing smart budgeting and acceleration techniques, every step you take brings you closer to full car ownership and overall financial health.

Remember, consistent effort and proactive management are key. Don’t be afraid to revisit your budget, explore refinancing options, or make those extra payments that can save you significant money over time. By taking control of your auto loan payments, you’re not just paying for a car; you’re investing in your financial future.

Start implementing these strategies today, and drive confidently towards a future where your car is a source of joy and convenience, not financial burden. Your journey to financial freedom on wheels begins now!