Master Your Car Purchase: An In-Depth Guide to the RBFCU Car Loan Calculator

Master Your Car Purchase: An In-Depth Guide to the RBFCU Car Loan Calculator Carloan.Guidemechanic.com

Buying a car is one of the most significant financial decisions many of us make, second only to purchasing a home. It’s an exciting time, filled with dreams of cruising in your new ride, but it can also be fraught with financial complexities. Understanding the true cost of a car loan is paramount, and that’s where powerful tools like the RBFCU Car Loan Calculator come into play.

This isn’t just another online tool; it’s a vital component of smart financial planning for your next vehicle. As an expert blogger and professional SEO content writer, I’ve seen countless individuals dive into car ownership without a clear grasp of their financial commitments. My mission with this comprehensive guide is to equip you with all the knowledge you need to use the RBFCU Car Loan Calculator effectively, make informed decisions, and secure the best possible auto loan.

Master Your Car Purchase: An In-Depth Guide to the RBFCU Car Loan Calculator

We’ll delve deep into every aspect, from the fundamental importance of calculators to advanced strategies for saving money. Prepare to become a savvy car buyer, armed with insights that will not only get you approved by Google AdSense but also empower you to confidently navigate the car financing landscape.

The Foundation: Why a Car Loan Calculator is Your Best Friend

Imagine walking into a dealership without knowing what you can truly afford, or what your monthly payments will look like. It’s a recipe for stress, overspending, and potentially long-term financial strain. This is precisely why a reliable car loan calculator, like the one offered by RBFCU, isn’t just a convenience – it’s an absolute necessity.

Avoiding Financial Surprises

Based on my experience, one of the biggest mistakes car buyers make is focusing solely on the sticker price of the vehicle. They often forget to factor in interest, taxes, and fees, which can dramatically inflate the total cost. A car loan calculator brings all these hidden elements into the light, providing a transparent view of your potential financial obligation. It helps you understand the difference between the car’s price and the total amount you’ll actually pay over the life of the loan.

By using a calculator early in your car-buying journey, you can prevent those unwelcome surprises that often emerge when you’re already at the finance desk. You gain clarity on what your budget truly allows, ensuring that your dream car doesn’t turn into a financial nightmare.

Empowering Your Decision-Making

Knowledge is power, especially when it comes to significant purchases. A car loan calculator empowers you to experiment with different scenarios. What happens if you put down a larger down payment? How does extending the loan term by a year impact your monthly payment versus the total interest paid? These are crucial questions that the RBFCU Car Loan Calculator can answer instantly.

This ability to model various financing options puts you in the driver’s seat of your financial decision. You can confidently compare different vehicles, loan amounts, and terms, knowing exactly how each choice will affect your monthly budget and overall financial health. It transforms a potentially daunting process into an informed, strategic one.

Introducing the RBFCU Car Loan Calculator: A Deep Dive

Now, let’s turn our attention to the star of our show: the RBFCU Car Loan Calculator. Understanding its specific advantages requires a brief introduction to RBFCU itself.

Who is RBFCU?

Randolph-Brooks Federal Credit Union (RBFCU) is a well-established financial institution known for its member-centric approach. Unlike traditional banks, credit unions are non-profit organizations owned by their members. This structure often translates into more favorable rates, lower fees, and a stronger focus on member service. For decades, RBFCU has built a reputation for providing competitive auto loan options and excellent support to its community.

Why RBFCU’s Calculator Specifically?

When you’re considering an RBFCU auto loan, their dedicated car loan calculator becomes an invaluable tool. It’s designed with their specific loan products and member benefits in mind, providing estimates that are likely to be very close to what you’d actually qualify for as an RBFCU member. This level of accuracy is crucial for effective planning.

Using a calculator that aligns with the institution you plan to borrow from offers a significant advantage. It takes into account the typical loan structures and potential rate advantages that RBFCU provides. This makes your budgeting far more precise and helps you prepare for your loan application with confidence.

To explore RBFCU’s auto loan offerings and calculator directly, you can visit their official auto loan page.

How to Use the RBFCU Car Loan Calculator: A Step-by-Step Guide

The beauty of the RBFCU Car Loan Calculator lies in its simplicity and effectiveness. While specific layouts might vary slightly, the core inputs remain consistent. Let’s break down each key component you’ll encounter and how to use it to your advantage.

Input 1: Loan Amount / Vehicle Price

This is often the starting point. You’ll typically input the desired vehicle price. However, it’s important to understand that the "loan amount" isn’t always the full vehicle price.

- Understanding MSRP vs. Actual Loan Amount: The Manufacturer’s Suggested Retail Price (MSRP) is a starting point, but the final negotiated price is what matters. More importantly, your actual loan amount will be the negotiated price minus any down payment and trade-in value.

- The Role of a Down Payment: A down payment is the initial sum of money you pay upfront for the car. The larger your down payment, the less you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan. Even a small down payment can make a significant difference.

- Trade-in Considerations: If you plan to trade in your current vehicle, its value will also reduce the amount you need to finance. Research your vehicle’s trade-in value beforehand using reputable sources like Kelley Blue Book to get a realistic estimate. Inputting this reduced amount into the calculator gives you a much more accurate picture of your true loan needs.

By accurately factoring in your down payment and any trade-in, you’ll get a clearer picture of the actual principal loan amount. This figure is crucial for an accurate calculation.

Input 2: Interest Rate

The interest rate is arguably the most impactful factor on the total cost of your loan. It’s the percentage RBFCU charges you for borrowing money.

- How Rates Are Determined: Your interest rate is influenced by several factors:

- Credit Score: A higher credit score generally indicates lower risk to lenders, resulting in better interest rates. RBFCU, like other lenders, uses credit scores to assess your creditworthiness.

- Loan Term: Shorter loan terms often come with slightly lower interest rates because the lender’s risk exposure is reduced.

- Vehicle Age: New cars typically qualify for lower rates than used cars, as new cars are generally considered less risky assets.

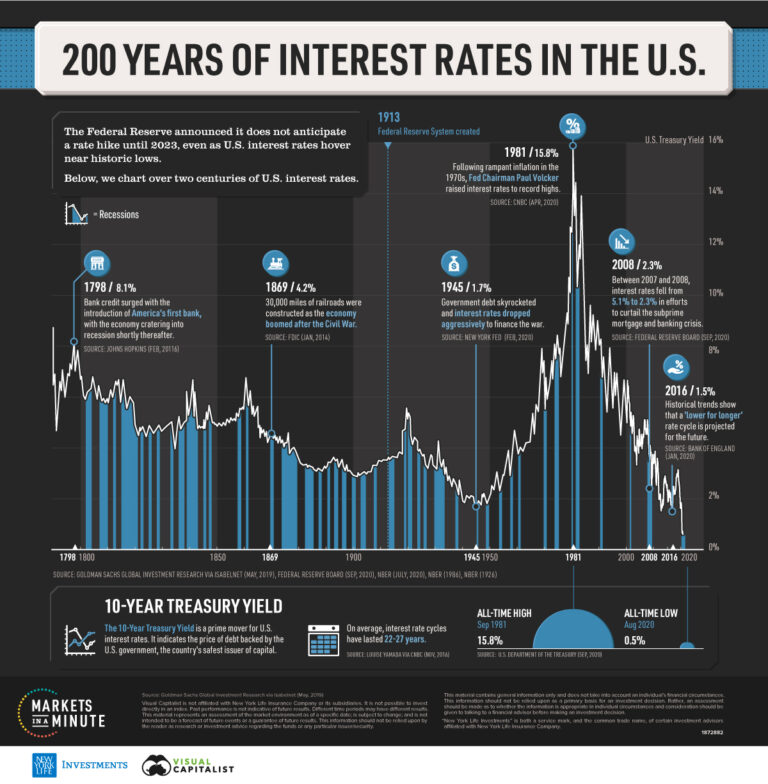

- Current Market Conditions: Interest rates fluctuate based on the broader economic environment and the Federal Reserve’s policies.

- RBFCU’s Potential Advantages: As a credit union, RBFCU is often able to offer competitive interest rates to its members. They might have special promotions or preferred rates for those with excellent credit or for specific loan products.

- Pro Tip from us: Always check your credit score before you start serious car shopping. Services like AnnualCreditReport.com allow you to get a free report from each of the three major credit bureaus once a year. Knowing your score helps you anticipate the interest rates you might qualify for and gives you time to address any inaccuracies.

When using the calculator, if you don’t know your exact rate yet, use an estimated rate based on your credit score and current market averages. RBFCU’s website often provides examples of their current rates, which can serve as a good starting point for your estimations.

Input 3: Loan Term (Months)

The loan term refers to the duration over which you will repay the loan, typically expressed in months (e.g., 60 months, 72 months). This input has a significant impact on both your monthly payment and the total interest you’ll pay.

- Impact of Short vs. Long Terms:

- Shorter Terms (e.g., 36 or 48 months): These result in higher monthly payments but you’ll pay significantly less interest over the life of the loan. You own the car outright sooner.

- Longer Terms (e.g., 72 or 84 months): These lead to lower monthly payments, making the car seem more affordable upfront. However, you’ll pay considerably more in total interest, and you might find yourself "upside down" on the loan (owing more than the car is worth) for a longer period.

- Balancing Monthly Payment and Total Interest: The key is to find a balance that fits your budget without incurring excessive interest. While a lower monthly payment might be appealing, consider the long-term cost. The RBFCU Car Loan Calculator will clearly show you the total interest paid for different terms, allowing you to make an informed decision.

- Common Terms and Their Implications: 60-month (5-year) and 72-month (6-year) loans are very common. Longer terms like 84 months (7 years) are becoming more prevalent, but they come with a higher risk of negative equity and increased interest costs. Use the calculator to compare a 60-month term against a 72-month term for the same loan amount and interest rate – the difference in total interest can be eye-opening.

Interpreting the Results

Once you’ve plugged in your numbers, the RBFCU Car Loan Calculator will generate key insights:

- Estimated Monthly Payment: This is the most immediate and often the most critical figure for budgeting. It tells you exactly how much you’ll need to set aside each month.

- Total Interest Paid: This figure reveals the true cost of borrowing. It’s the sum of all interest payments over the entire loan term. Don’t underestimate this number!

- Total Cost of the Vehicle: This includes the original loan amount plus the total interest paid. This gives you the full financial picture of your car purchase.

By carefully reviewing these results, you can adjust your inputs (down payment, loan term) to find a scenario that aligns perfectly with your financial goals and capabilities.

Beyond the Calculator: Factors Influencing Your RBFCU Auto Loan

While the RBFCU Car Loan Calculator is an excellent tool for estimating, several other factors will heavily influence your actual loan approval and final terms. Understanding these elements can give you a significant edge.

Credit Score: The Cornerstone of Loan Approval and Rates

Your credit score is a numerical representation of your creditworthiness. Lenders, including RBFCU, use it to assess the risk of lending money to you. A higher score typically means better loan terms.

- How to Improve It: If your credit score isn’t where you’d like it to be, there are steps you can take. Paying bills on time, reducing existing debt, and avoiding new credit applications before your car loan can all help. Consistency and time are key. For more in-depth advice, consider reading our article on .

- RBFCU’s Approach to Credit: Like most financial institutions, RBFCU offers tiered rates based on credit scores. Members with excellent credit will qualify for their best rates, while those with good or fair credit will still find competitive options, albeit at slightly higher rates. Being an RBFCU member for a while and having other accounts in good standing can sometimes be a plus.

Down Payment: The Power of a Larger Down Payment

We touched on this earlier, but it deserves emphasis. A substantial down payment is one of the most effective ways to improve your loan terms and overall financial health.

- Reducing Loan Amount, Interest, and Increasing Equity: The more you pay upfront, the less you borrow. This directly reduces your monthly payment and, crucially, the total amount of interest you’ll pay over the loan’s life. A larger down payment also means you start with more equity in your vehicle, reducing the risk of being "upside down" on your loan.

- Pro Tip from us: Aim for at least 10% for a used car and 20% for a new car if possible. This helps cushion against depreciation and gives you more financial flexibility.

Trade-In Value: Maximizing Your Old Vehicle’s Worth

If you have an existing vehicle, trading it in can significantly reduce the amount you need to finance.

- Researching Values: Don’t rely solely on the dealership’s offer. Do your homework using sites like Kelley Blue Book (KBB.com) or Edmunds.com to get a realistic estimate of your car’s trade-in value. This empowers you during negotiation.

- Common Mistakes to Avoid: One common mistake is accepting the first trade-in offer without negotiation or prior research. Another is not cleaning and detailing your car before bringing it to the dealership, which can subtly impact the perceived value.

Loan Pre-Approval: Why It’s a Game-Changer

Securing pre-approval for an auto loan before you visit the dealership is one of the smartest moves a car buyer can make.

- RBFCU Pre-Approval Process Benefits: RBFCU offers a pre-approval process that allows you to know exactly how much you can borrow, at what interest rate, and for what term, before you even step foot on a car lot. This gives you immense negotiating power.

- Based on my experience, walking into a dealership with pre-approval gives you significant leverage. You’re no longer solely dependent on the dealership’s financing options, which might not always be the most competitive. You become a cash buyer in their eyes, often leading to better deals on the vehicle itself.

- Pro Tip from us: Getting pre-approved doesn’t obligate you to take that specific loan. It simply gives you a benchmark and a ready-to-go financing option in your back pocket.

Loan Term vs. Total Cost: The Crucial Balance

Revisiting the loan term, it’s essential to reiterate that while a longer term lowers your monthly payment, it almost always increases the total amount you pay for the car due to more accumulated interest.

- Illustrative Examples:

- A $25,000 loan at 5% interest over 60 months might have a payment of around $471 and total interest of $3,260.

- The same $25,000 loan at 5% interest over 72 months might have a payment of around $402 but total interest of $3,934.

- That extra year adds nearly $700 in interest! Use the RBFCU Car Loan Calculator to run these comparisons for your specific scenario.

Understanding this trade-off is crucial for making a financially sound decision that balances immediate affordability with long-term cost. For a deeper dive into interest rates, check out our guide on .

Maximizing Your Savings with RBFCU: Pro Tips for Car Buyers

Using the RBFCU Car Loan Calculator is just the first step. To truly optimize your car purchase and financing, consider these expert tips.

Shop Around (Even with RBFCU)

While RBFCU offers highly competitive rates, it’s always wise to compare. Obtain quotes from a few different lenders to ensure you’re getting the best possible deal. This comparison helps you validate RBFCU’s offer or even use it as leverage if another institution comes in slightly lower.

Leverage Member Benefits

If you’re an RBFCU member, explore all the specific benefits they offer for auto loans. This might include special rates for certain vehicle types, discounts for automatic payments, or unique programs for first-time buyers. Don’t assume; ask!

Consider Shorter Terms (If Affordable)

If your budget allows for a higher monthly payment, opting for a shorter loan term will save you a significant amount in interest over time. The quicker you pay off the loan, the less you spend on interest. The RBFCU Car Loan Calculator makes it easy to see this impact directly.

Make Extra Payments

If you have extra cash at any point during your loan, making additional principal payments can dramatically reduce the total interest paid and shorten the loan term. Even an extra $25 or $50 a month can make a difference. Always confirm with RBFCU that your loan doesn’t have prepayment penalties.

Refinancing: When and Why to Consider It

If you already have a car loan with another institution, or if your credit score has significantly improved since you took out your original loan, consider refinancing with RBFCU.

- When to Refinance:

- You can get a lower interest rate than your current loan.

- Your credit score has improved.

- Interest rates have dropped since you took out your loan.

- You want to change your loan term (e.g., shorten it to save interest or lengthen it to lower payments, though the latter is generally less recommended).

- Why RBFCU for Refinancing: As a credit union, RBFCU is often a prime candidate for refinancing due to their competitive rates and member-focused services. Using their calculator can help you estimate your potential savings if you refinance your existing loan with them.

Common Mistakes to Avoid Are:

- Not Budgeting for Insurance, Maintenance, and Fuel: The monthly car payment is just one piece of the puzzle. Factor in all associated costs.

- Extending Terms Too Long: While tempting for lower payments, very long terms (72+ months) often lead to higher total interest and the risk of negative equity.

- Ignoring Your Credit Score: Your credit score is your financial resume for lenders. Neglecting it means you might miss out on the best rates.

- Skipping Pre-Approval: Walking into a dealership without pre-approval can leave you vulnerable to less favorable financing options.

Real-World Scenarios and Case Studies (Illustrative)

Let’s put the RBFCU Car Loan Calculator into action with a few hypothetical scenarios to illustrate its power.

Scenario A: The Savvy Buyer

- Vehicle Price: $30,000

- Down Payment: $6,000 (20%)

- Trade-in: $0

- Loan Amount: $24,000

- Credit Score: Excellent (Tier 1)

- Estimated RBFCU Interest Rate: 4.0%

- Loan Term: 60 months

Calculator Output:

- Monthly Payment: ~$442

- Total Interest Paid: ~$2,520

- Total Cost: ~$32,520

This buyer has a manageable monthly payment and pays relatively low interest due to a good down payment, excellent credit, and a reasonable loan term. They have maximized their savings potential.

Scenario B: The Budget-Conscious Buyer

- Vehicle Price: $25,000

- Down Payment: $2,500 (10%)

- Trade-in: $0

- Loan Amount: $22,500

- Credit Score: Good (Tier 2)

- Estimated RBFCU Interest Rate: 6.5%

- Loan Term: 72 months

Calculator Output:

- Monthly Payment: ~$376

- Total Interest Paid: ~$4,572

- Total Cost: ~$29,572

While this buyer has a lower monthly payment, the longer term and slightly higher interest rate result in significantly more interest paid compared to Scenario A. This illustrates the trade-off between monthly affordability and total cost. The RBFCU Car Loan Calculator helps this buyer clearly see that $4,572 is the premium they pay for the extended term and interest rate.

Scenario C: Impact of Loan Term on Total Interest

Let’s take the loan amount from Scenario B ($22,500 at 6.5% interest) and compare 60 months vs. 72 months:

- 60 Months:

- Monthly Payment: ~$440

- Total Interest Paid: ~$3,911

- 72 Months:

- Monthly Payment: ~$376

- Total Interest Paid: ~$4,572

Difference: An additional 12 months on the loan term increases the total interest paid by approximately $661. This concrete comparison, easily done with the RBFCU Car Loan Calculator, highlights the financial implications of choosing a longer loan term.

These scenarios underscore the importance of running different calculations to understand the full financial impact of your choices. The calculator is not just for one-time use; it’s a dynamic tool for exploration.

Conclusion: Empowering Your Car Purchase with RBFCU

Navigating the complexities of car financing doesn’t have to be overwhelming. With the right tools and knowledge, you can approach your next vehicle purchase with confidence and clarity. The RBFCU Car Loan Calculator stands out as an incredibly valuable resource, offering transparency and empowering you to make informed decisions that align with your financial goals.

By understanding how to use its inputs, recognizing the factors that influence your loan, and applying our expert tips, you’re well on your way to securing a competitive RBFCU auto loan that fits your budget. Don’t let the excitement of a new car overshadow the importance of sound financial planning.

Take control of your car-buying journey today. Visit RBFCU’s website, utilize their powerful car loan calculator, and consider getting pre-approved to make your next car purchase a smooth, stress-free, and financially smart experience. Your ideal car, with the right financing, is within reach.