Master Your Car Purchase: The Ultimate Car Loan Worksheet Guide

Master Your Car Purchase: The Ultimate Car Loan Worksheet Guide Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, but it can also feel like navigating a complex maze of numbers, jargon, and high-pressure sales tactics. Without a clear strategy, you might find yourself agreeing to terms that don’t truly serve your financial best interest. This is where a meticulously designed Car Loan Worksheet becomes your most powerful tool.

Imagine walking into a dealership or comparing online loan offers with absolute clarity and confidence. You know your budget inside and out, understand every single cost component, and can identify a good deal from a bad one instantly. This isn’t just wishful thinking; it’s the reality a comprehensive car loan worksheet creates.

Master Your Car Purchase: The Ultimate Car Loan Worksheet Guide

In this exhaustive guide, we’ll peel back every layer of the car financing process. We’ll empower you with the knowledge and the practical framework to build and utilize a car loan worksheet that ensures you make smart, informed decisions. Our ultimate goal is to transform you from a hopeful buyer into a savvy negotiator, saving you potentially thousands of dollars and countless headaches.

Why You Absolutely Need a Car Loan Worksheet

Many car buyers make decisions based on emotion or a single number: the monthly payment. This approach is a common pitfall that can lead to overspending, unexpected costs, and buyer’s remorse. A dedicated car loan worksheet prevents these issues by bringing structure and transparency to the entire process.

Based on my experience, rushing into a car purchase without proper planning is one of the biggest financial mistakes people make. A worksheet forces you to slow down, consider all variables, and think critically. It acts as your personal financial compass in the often-turbulent waters of auto financing.

Ultimately, this simple yet powerful document transforms an intimidating transaction into a manageable one. It shifts the power dynamic, putting you in control. You move from reacting to offers to proactively defining your ideal scenario.

Here’s why it’s non-negotiable for a smart car purchase:

- Avoid Common Pitfalls: Without a clear financial picture, it’s easy to fall for extended loan terms that lower monthly payments but dramatically increase total interest paid. A worksheet highlights these long-term costs.

- Gain Clarity and Control: It demystifies the entire car buying process by breaking down complex financial figures into digestible components. You see exactly where your money is going and what you’re committing to.

- Save Money in the Long Run: By comparing different scenarios – varying down payments, loan terms, and interest rates – you can identify the most cost-effective path. This proactive approach directly translates into significant savings.

- Negotiate with Confidence: Armed with concrete numbers and your predefined budget, you can confidently negotiate with dealers and lenders. You won’t be swayed by persuasive sales tactics when your worksheet clearly outlines your limits and preferences.

Deconstructing the Car Loan Worksheet: Essential Components

A truly comprehensive car loan worksheet isn’t just about the car’s price; it’s about your entire financial ecosystem surrounding the purchase. Let’s break down each crucial section you need to include.

Section 1: Your Financial Snapshot

Before you even look at a car, you need to look at your own finances. This self-assessment is the bedrock of responsible car buying.

-

Net Monthly Income:

Your net monthly income is your take-home pay after taxes, insurance, and other deductions. This figure is critical because it represents the actual money you have available to cover expenses, including a car payment. Don’t use your gross income; that leads to an inflated sense of affordability.

Pro tips from us: Be realistic and even a little conservative with this number. Account for any variable income or bonuses separately, and don’t rely on them for your core car payment calculation. Your car payment, along with insurance and fuel, should ideally not exceed 10-15% of your net monthly income. -

Existing Debts (Debt-to-Income Ratio – DTI):

List all your current monthly debt payments: credit cards, student loans, mortgage/rent, personal loans, etc. Your debt-to-income (DTI) ratio is a key metric lenders use to assess your ability to take on new debt. It’s calculated by dividing your total monthly debt payments (including the potential new car payment) by your gross monthly income.

A DTI of 36% or lower is generally considered healthy, though some lenders might approve higher ratios. A high DTI indicates you might be overextended, making lenders hesitant or offering less favorable terms. Understanding this helps you manage expectations. -

Savings/Emergency Fund:

Assess how much you have in your savings and emergency fund. While a portion might go towards a down payment, it’s crucial not to deplete your emergency savings entirely for a car. Life happens, and having a financial cushion provides security.

Common mistakes to avoid are using every last penny for a down payment. You need accessible funds for unexpected repairs or other emergencies that might arise shortly after your purchase. Prioritize your financial stability first. -

Credit Score:

Your credit score is perhaps the single most important factor determining the interest rate you’ll be offered on a car loan. Lenders use it to assess your creditworthiness – how likely you are to repay your loan. A higher score (generally 700+) indicates lower risk and typically qualifies you for the best rates.

Based on my experience, many buyers only check their score right before applying, which is too late to make significant improvements. Get your score well in advance, understand what’s on your credit report, and address any inaccuracies. can provide more in-depth guidance.

Section 2: The Car Itself (Target Vehicle Information)

Once you understand your financial limits, you can start focusing on the actual vehicle. This section helps you define the true cost of your desired car.

-

Target Price (MSRP, Invoice, Negotiated Price):

Don’t just look at the Manufacturer’s Suggested Retail Price (MSRP). Research the invoice price (what the dealer paid) and typical selling prices in your area for the specific make and model. Sites like Edmunds or Kelley Blue Book are invaluable here. Your worksheet should have a space for your negotiated price, which should be your target.

This research empowers you to approach negotiations with realistic expectations. Knowing the market value helps you avoid overpaying and sets a solid baseline for your budget. -

Trade-in Value (Realistic Assessment):

If you have a car to trade in, get multiple appraisals before heading to the dealership. Use online tools, visit other dealerships, or even get an offer from a service like CarMax. Dealers often offer less for trade-ins to maximize their profit, so knowing its true market value is vital.

Pro tips from us: Always negotiate the price of the new car before discussing your trade-in. This separates the two transactions, preventing the dealer from playing with numbers to make it seem like you’re getting a great deal on one while losing out on the other. -

Down Payment Amount (Strategy, Benefits):

The down payment is the initial amount of cash you put towards the car purchase. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. It also provides immediate equity in the vehicle.

Common mistakes to avoid are making a minimal down payment if you can afford more. While 0% down loans are attractive, they often lead to higher monthly payments and a longer period of being "upside down" (owing more than the car is worth), especially in the early years of the loan.

Section 3: Loan Details

This is where the rubber meets the road, calculating the actual financial commitment of the loan itself.

-

Loan Amount Needed:

This is straightforward: (Negotiated Car Price) – (Trade-in Value) – (Down Payment). This final figure is the amount you will need to finance. Having this number clearly defined prevents confusion and helps you quickly compare loan offers.

Ensuring this calculation is accurate is paramount. Any misstep here will throw off all subsequent calculations, leading to an inaccurate budget. Double-check your figures. -

Interest Rate (APR):

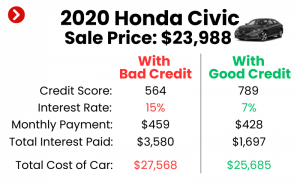

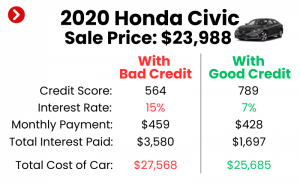

The Annual Percentage Rate (APR) is the true cost of borrowing money, expressed as a yearly percentage. It includes the interest rate plus certain fees. Your credit score, the loan term, and the lender’s policies all influence your APR. Even a percentage point difference can save you hundreds, if not thousands, over the loan’s life.

Based on my experience, shopping around for the best APR is non-negotiable. Don’t just accept the first offer, especially from the dealership. Get quotes from banks, credit unions, and online lenders before you go to the dealership. -

Loan Term (Duration):

The loan term is the length of time (in months) you have to repay the loan. Common terms are 36, 48, 60, 72, or even 84 months. A longer term means lower monthly payments, but you’ll pay significantly more in total interest over time. A shorter term means higher monthly payments but less overall interest.

Pro tips from us: Aim for the shortest loan term you can comfortably afford. While a 72-month loan might seem appealing for its low monthly payment, it often means you’ll be paying for the car long after its prime value and could be "upside down" for an extended period. -

Monthly Payment Calculation:

This is the figure most buyers focus on. While there are complex formulas, online car loan calculators make this simple. Input your loan amount, APR, and loan term, and it will instantly show your estimated monthly payment. Your worksheet should include a section to calculate and compare this for different scenarios.

Understanding how changes in any of the variables (loan amount, APR, term) impact this payment is crucial. Play around with different numbers to see the direct effect. -

Total Interest Paid:

This is the hidden cost that often shocks buyers. Your worksheet should clearly show the total amount of interest you will pay over the entire life of the loan. This is calculated as (Monthly Payment * Loan Term) – Loan Amount Needed.

Seeing this number in black and white can be a powerful motivator to make a larger down payment or opt for a shorter loan term. It truly highlights the "cost of convenience" for longer terms. -

Total Cost of Loan:

This is the grand total you’ll pay for the car and its financing. It includes the Negotiated Car Price + Sales Tax + Registration/Fees + Total Interest Paid. This comprehensive figure gives you the complete financial picture, allowing for a true apples-to-apples comparison between different financing options.

Many people only focus on the car price or the monthly payment. This "Total Cost" is the figure you should be laser-focused on to ensure you’re getting the best overall deal.

Section 4: Additional Costs & Fees (Often Overlooked)

This section is where many budgets go awry. These "hidden" costs can add thousands to your overall expense if not accounted for.

-

Sales Tax:

Most states charge sales tax on vehicle purchases, which can be a significant amount depending on the car’s price and your state’s tax rate. This is typically added to the purchase price before financing, or you may pay it separately.

Always factor this into your total cost, as it’s not negotiable and can easily be overlooked in the initial excitement. -

Registration and Licensing Fees:

These are fees paid to your state’s Department of Motor Vehicles (DMV) for registering the vehicle and obtaining license plates. They vary by state and often depend on the car’s value or weight.

These are mandatory costs that must be included in your worksheet. They can range from a few hundred to over a thousand dollars, depending on your location and vehicle. -

Documentation Fees (Doc Fees):

Dealers charge a "doc fee" for processing paperwork related to the sale. These fees vary widely by state and even by dealership and are often negotiable, though some states cap them.

Common mistakes to avoid are simply accepting this fee without question. While some amount is legitimate, excessive doc fees are profit centers for dealers. Research the typical doc fee in your state and negotiate if it seems too high. -

Extended Warranties/Service Contracts:

These are often pushed by finance managers but are entirely optional. They cover repairs beyond the manufacturer’s warranty. While they can provide peace of mind, they are often expensive and may duplicate existing coverage.

Pro tips from us: Research third-party warranty providers if you truly want one, as they are often more affordable than dealership offerings. Never feel pressured to buy one on the spot; you can always purchase them later. -

Gap Insurance:

Guaranteed Asset Protection (GAP) insurance covers the "gap" between what you owe on your car loan and what your car is worth if it’s totaled or stolen. This is particularly important if you make a small down payment, have a long loan term, or are financing a rapidly depreciating vehicle.

Based on my experience, if you’re "upside down" on your loan (owe more than the car is worth), GAP insurance is a wise investment. However, you can often get it cheaper from your auto insurance provider or a third-party insurer than from the dealership. -

Car Insurance (Estimate Monthly Premium):

Before buying, get insurance quotes for the specific make and model you’re considering. Different cars have different insurance costs based on factors like safety ratings, theft rates, and repair costs. This is an ongoing monthly expense that dramatically impacts your total cost of ownership.

can help you delve deeper into this critical aspect. Do not wait until after you’ve bought the car to get quotes; the monthly premium might be a deal-breaker. -

Fuel Costs (Ongoing):

Consider the fuel efficiency (MPG) of the vehicle you’re looking at. A car with poor MPG will cost you significantly more in fuel over its lifetime, especially with fluctuating gas prices. Estimate your average monthly mileage and calculate this ongoing expense.

This might seem obvious, but it’s often overlooked in the initial excitement. A "cheap" car to buy might be an expensive car to own if it’s a gas guzzler. -

Maintenance & Repairs (Budgeting for the Unexpected):

All cars require maintenance, and older or higher-mileage vehicles will inevitably need repairs. Research the typical maintenance costs for your desired model. Set aside a monthly amount for this. Sites like RepairPal can provide estimates.

Common mistakes to avoid are ignoring this category, especially for used cars. A healthy emergency fund helps cover major unexpected repairs without derailing your finances.

Step-by-Step Guide to Using Your Car Loan Worksheet

Now that you understand all the components, let’s put it into practice.

- Gathering Information: Collect all your financial documents: pay stubs, bank statements, credit report, current debt statements. Research target car prices, trade-in values, and insurance quotes.

- Filling It Out Diligently: Systematically fill in each section of your worksheet. Be honest and realistic with your numbers. Don’t skip any sections, even the "minor" fees.

- Analyzing the Results: Review your total cost of loan, monthly payment, and overall budget impact. Does it align with your financial goals and comfort level?

- Adjusting Your Expectations/Budget: If the numbers are too high, what can you adjust? A smaller down payment? A different car model? A longer loan term (with caution)? This is an iterative process.

- Using It for Negotiation: Bring your completed worksheet with you when talking to dealers or lenders. It’s your reference point and a powerful tool to stick to your budget and compare offers objectively.

Pro Tips from Us for Maximizing Your Worksheet’s Power

Leveraging your car loan worksheet effectively goes beyond just filling it out. These strategies will elevate your car buying game.

-

Get Pre-Approved First:

Always secure pre-approval for a car loan from your bank, credit union, or an online lender before stepping foot in a dealership. This gives you a concrete interest rate and loan amount you qualify for. It acts as a powerful negotiating chip, as the dealer knows you’re serious and already have financing secured.

Based on my experience, this step is non-negotiable. It separates the car price negotiation from the financing negotiation, giving you clearer focus and preventing dealers from manipulating numbers. -

Separate Negotiation Tactics (Car price vs. Loan terms):

Never discuss your trade-in or financing options until you have agreed on the final purchase price of the new car. Negotiate the car price as if you’re paying cash. Once that’s settled, then you can discuss your trade-in and compare the dealer’s financing offer against your pre-approval.

This strategy ensures you’re getting the best deal on each component independently. Otherwise, dealers can "pack" the deal, making you think you’re getting a good price on one aspect while overpaying on another. -

Don’t Forget the "Total Cost of Ownership":

Your car loan worksheet helps you calculate the purchase cost, but true car ownership involves more. Factor in depreciation, regular maintenance, potential repairs, fuel, and insurance. A car that’s cheap to buy might be expensive to own.

Pro tips from us: Websites like Edmunds or AAA often provide estimated "True Cost to Own" figures for various vehicles. Incorporating these into your broader financial planning ensures there are no surprises down the road. -

Review Annually (Refinancing Possibilities):

Even after you’ve purchased the car, your financial situation can change. Your credit score might improve, or interest rates might drop. Review your loan terms annually and explore refinancing options if you can secure a lower APR or better terms.

This proactive approach can save you a significant amount of money over the remaining life of the loan. It’s an ongoing process, not a one-time event. -

Consider the "Future You":

Think about your long-term financial goals. Will this car payment hinder your ability to save for a house, retirement, or other important milestones? A car is a depreciating asset, and while necessary, it shouldn’t derail your broader financial health.

Common mistakes to avoid are getting caught up in the "new car smell" and making a decision that you’ll regret years down the line when you’re still paying for a car that’s lost much of its value.

Common Mistakes to Avoid When Using a Car Loan Worksheet

Even with a great tool, missteps can happen. Be aware of these common pitfalls.

-

Underestimating Hidden Costs:

As we detailed, sales tax, registration, doc fees, and especially ongoing insurance and maintenance are often underestimated or completely forgotten. These costs can easily add thousands to your overall expense.

Always give these categories ample consideration and research. Don’t let them blindside you after the purchase. -

Focusing Only on Monthly Payment:

This is perhaps the biggest mistake car buyers make. A low monthly payment often comes at the cost of a very long loan term and significantly more total interest paid. It obscures the true cost of the vehicle.

Your worksheet should clearly highlight the "Total Cost of Loan" and "Total Interest Paid" as primary decision-making factors, not just the monthly payment. -

Not Shopping Around for Loans:

Accepting the first loan offer, especially from the dealership, is a common error. Dealerships often mark up interest rates to profit from financing.

Always get multiple loan quotes from various financial institutions. This competitive shopping can yield substantially better interest rates and save you hundreds or thousands of dollars. -

Ignoring Your Credit Score:

Your credit score directly impacts your interest rate. Neglecting to check it, understand it, or improve it before applying for a loan can cost you dearly in higher interest payments.

Take the time to pull your credit report, identify any errors, and work on improving your score if needed, well in advance of your car purchase. -

Being Swayed by Emotions:

Buying a car is an emotional experience, but emotional decisions often lead to financial regrets. Stick to the numbers on your worksheet, even if you fall in love with a car outside your budget.

Your car loan worksheet provides an objective, data-driven framework. Let it guide your decisions, not the excitement of a test drive or a salesperson’s pitch.

Beyond the Worksheet: What to Do After It’s Complete

Your completed car loan worksheet is a powerful guide, but the journey doesn’t end there. Here’s what to do next.

-

Compare Offers Systematically:

With your worksheet in hand, you can now compare different car models, dealership offers, and lender proposals side-by-side. Fill out a separate column or worksheet for each option you’re considering. This allows for a clear, objective comparison of total costs.

Don’t just look at the monthly payment; scrutinize the APR, loan term, total interest paid, and all associated fees for each offer. -

Read the Fine Print:

Before signing any documents, read everything thoroughly. Understand all terms and conditions, including any prepayment penalties, late fees, or clauses about defaulting on the loan. If something is unclear, ask for clarification.

Common mistakes to avoid are rushing through this step. A few minutes of careful reading can prevent major headaches later. If possible, ask for a copy of the loan documents to review at home before you sign. -

Final Decision:

Armed with all the information and your comprehensive worksheet analysis, make your final, informed decision. Choose the car and financing option that best fits your budget, lifestyle, and long-term financial goals.

Remember, the goal is not just to get a car, but to get a car that you can afford comfortably and without financial strain.

Conclusion: Drive Smart, Finance Smarter

The process of buying a car doesn’t have to be overwhelming or financially draining. By dedicating the time and effort to create and utilize a comprehensive Car Loan Worksheet, you transform a potentially stressful experience into an empowering one. This isn’t just a piece of paper; it’s your personal financial bodyguard, protecting you from common pitfalls and ensuring you make a truly informed decision.

From understanding your financial capacity to dissecting every cost associated with the vehicle and its financing, your worksheet will be your unwavering guide. It allows you to approach dealers and lenders with confidence, negotiate from a position of strength, and ultimately, drive away knowing you’ve secured the best possible deal.

Don’t let the excitement of a new car overshadow smart financial planning. Start building your car loan worksheet today, and embark on your next vehicle purchase with clarity, control, and peace of mind. Your wallet will thank you.