Master Your Car Purchase: The Ultimate Guide to the Loan To Value Ratio Car Calculator

Master Your Car Purchase: The Ultimate Guide to the Loan To Value Ratio Car Calculator Carloan.Guidemechanic.com

Embarking on the journey to buy a new or used car is exciting, but it often comes with a maze of financial terms and calculations. One crucial concept that can significantly impact your car loan’s approval, interest rate, and overall affordability is the Loan-to-Value (LTV) ratio. Understanding this metric isn’t just for financial experts; it’s a vital tool for any savvy car buyer.

This comprehensive guide will demystify the LTV ratio, explain its profound importance in car financing, and show you exactly how a Loan To Value Ratio Car Calculator can empower your purchasing decisions. We’ll delve deep into every aspect, providing you with the knowledge to secure the best possible deal and avoid common pitfalls.

Master Your Car Purchase: The Ultimate Guide to the Loan To Value Ratio Car Calculator

What Exactly is the Loan-to-Value (LTV) Ratio?

At its core, the Loan-to-Value (LTV) ratio is a financial metric that compares the amount of money you borrow to the appraised value of the asset you’re purchasing. In the context of car loans, it’s the percentage of the car’s market value that the lender is willing to finance. Think of it as a risk assessment tool for lenders.

A lower LTV ratio signifies less risk for the lender because you, the borrower, have more equity in the vehicle from the start. Conversely, a higher LTV ratio indicates greater risk, as the loan amount is closer to, or even exceeds, the car’s value. This fundamental principle dictates much of the lending world.

Understanding this ratio is paramount because it directly influences whether your loan gets approved, the interest rate you’re offered, and even the length of your loan term. It’s not just a number; it’s a window into the financial health of your car purchase.

The Simple Math: How to Calculate Your Car’s LTV

Calculating your car’s LTV ratio is straightforward once you have the necessary figures. You only need two key pieces of information: the total loan amount and the car’s actual cash value (ACV).

The formula is as follows:

LTV Ratio = (Total Loan Amount / Car’s Actual Cash Value) x 100

Let’s break down these components. The "Total Loan Amount" includes the principal amount you’re borrowing, often combined with any taxes, fees, and sometimes even extended warranties rolled into the loan. The "Car’s Actual Cash Value" refers to what the car is worth in the current market, usually determined by resources like Kelley Blue Book (KBB), Edmunds, or NADA guides.

For instance, if you’re looking to borrow $20,000 for a car that has an appraised value of $25,000, your LTV ratio would be ($20,000 / $25,000) x 100 = 80%. This means the loan covers 80% of the car’s value, and you’re covering the remaining 20% through a down payment or trade-in equity.

Why Your Car’s LTV Ratio Matters to Lenders (And You!)

The LTV ratio is a critical factor for lenders when evaluating your car loan application. It serves as a primary indicator of their potential exposure should you default on the loan. If the LTV is too high, the lender stands to lose more money if they have to repossess and sell the vehicle.

From the lender’s perspective, a lower LTV means greater security. They know that if the car needs to be repossessed, its sale will likely cover the outstanding loan balance. This reduced risk often translates into more favorable loan terms for you, the borrower.

For you, understanding LTV means greater transparency and control over your financing. A high LTV could lead to higher interest rates, stricter approval criteria, or even outright denial of the loan. Conversely, optimizing your LTV can unlock lower monthly payments, less interest paid over the loan’s life, and a smoother approval process.

Decoding the "Good" LTV: What Do Lenders Look For?

There isn’t a universally "perfect" LTV ratio, as it can vary slightly between lenders and based on current market conditions. However, based on my experience in the financial industry, most lenders prefer an LTV ratio of 80% or lower for the most competitive rates and terms.

An 80% LTV means you’re putting down at least 20% of the car’s value, either through a cash down payment or trade-in equity. This significant upfront investment demonstrates your financial commitment and reduces the lender’s risk considerably. Some lenders might approve loans with LTVs up to 100% or even 110-120% (often called "upside down" or "negative equity" loans), but these typically come with higher interest rates and more stringent requirements.

Pro tips from us: Aiming for an LTV of 80% or below should be your primary goal. This will not only improve your chances of approval but also qualify you for the most attractive interest rates, saving you substantial money over the life of the loan. It’s a clear signal to lenders that you’re a responsible and low-risk borrower.

The Power of the Loan To Value Ratio Car Calculator

While calculating LTV manually is simple, a Loan To Value Ratio Car Calculator automates this process, making it incredibly easy and efficient. These online tools are designed to help you quickly determine your potential LTV ratio before you even step foot into a dealership.

The primary benefit of using such a calculator is the ability to plan and strategize. You can input different scenarios—varying down payments, different car prices, or trade-in values—to see how each impacts your LTV. This foresight allows you to adjust your budget or expectations proactively.

Common mistakes to avoid are going into a dealership without this crucial information. Without knowing your LTV, you’re at a disadvantage, potentially accepting less favorable terms simply because you don’t understand the underlying numbers. A calculator empowers you to negotiate from a position of strength.

How to Use an LTV Car Calculator:

- Enter the Car’s Market Value: This is the appraised value of the vehicle you intend to purchase.

- Input Your Down Payment: The cash amount you plan to pay upfront.

- Add Your Trade-in Value (if any): If you’re trading in your current car, include its agreed-upon value.

- Specify Any Additional Costs: Include taxes, registration fees, and any other items you plan to roll into the loan.

- Calculate: The tool will instantly display your LTV ratio and often the total loan amount.

By playing with these numbers, you can easily determine what down payment or trade-in value you’d need to reach your target LTV, such as 80%.

Key Factors That Influence Your Car’s LTV

Several elements directly impact your car’s LTV ratio. Understanding these can help you manipulate the ratio in your favor.

1. The Car’s Actual Cash Value (ACV)

This is the baseline for your LTV calculation. The ACV is determined by market conditions, the vehicle’s make, model, year, mileage, and overall condition. A newer, low-mileage car in excellent condition will have a higher ACV, potentially allowing for a larger loan amount while maintaining a healthy LTV.

2. Your Down Payment

This is arguably the most direct way to influence your LTV. The more cash you put down upfront, the lower your loan amount will be, and consequently, the lower your LTV ratio. A substantial down payment instantly reduces the lender’s risk.

3. Trade-in Value

If you’re trading in an old vehicle, its equity acts much like a down payment. The higher the value of your trade-in (and the less you owe on it), the more it contributes to reducing the total loan amount for your new car, thus lowering your LTV. Make sure to research your trade-in’s value beforehand!

4. Additional Costs Rolled into the Loan

Sales tax, registration fees, extended warranties, and GAP insurance are often rolled into the total loan amount. While convenient, this increases your "Total Loan Amount" figure, which in turn raises your LTV ratio. Consider paying these costs out of pocket if you want to keep your LTV as low as possible.

Strategies to Optimize Your LTV for a Better Car Loan

Now that you know what influences your LTV, here’s how you can actively work to improve it:

1. Increase Your Down Payment

This is the most straightforward and effective strategy. The more cash you can put down, the smaller the loan amount needed, and the lower your LTV will be. Aim for 20% or more if possible.

2. Boost Your Trade-in Equity

Before heading to the dealership, get multiple quotes for your trade-in from different sources, not just the dealer. A higher trade-in value directly reduces the amount you need to borrow. Ensure your current vehicle is clean and well-maintained to maximize its value.

3. Choose a More Affordable Vehicle

It might sound obvious, but opting for a slightly less expensive car automatically lowers the "Car’s Actual Cash Value" component, making it easier to achieve a lower LTV with the same down payment. Sometimes, adjusting your expectations by a few thousand dollars can make a big difference in your financing terms.

4. Pay Additional Costs Out of Pocket

Instead of rolling sales tax, registration fees, or an extended warranty into your loan, pay for them separately. This keeps your "Total Loan Amount" lower, directly benefiting your LTV ratio.

Common LTV Mistakes to Steer Clear Of

Navigating car financing can be tricky, and several common missteps related to LTV can lead to less favorable outcomes.

One frequent mistake is not knowing your car’s true market value. Relying solely on the dealer’s valuation without cross-referencing independent sources like KBB or Edmunds can lead to overestimating the car’s value or underestimating your trade-in’s worth, resulting in a higher LTV than necessary. Always do your homework!

Another pitfall is rolling too many extra costs into the loan. While convenient, adding warranties, GAP insurance, and other fees to your principal loan amount inflates it, pushing your LTV higher and costing you more in interest over time. Carefully consider which extras are truly essential and whether they can be paid separately.

Finally, many buyers fail to use an LTV calculator beforehand. This proactive step can reveal potential issues and allow you to adjust your strategy. Going into negotiations blind leaves you vulnerable to unfavorable terms.

LTV Beyond Purchase: Refinancing Your Car Loan

The LTV ratio isn’t just relevant when you’re initially buying a car; it plays a significant role if you decide to refinance your existing auto loan. Refinancing involves taking out a new loan to pay off your current one, often to secure a lower interest rate or different terms.

When you apply for a refinance, lenders will again assess your LTV. They’ll compare your outstanding loan balance to the current market value of your car. If your car has depreciated significantly, or if you still owe a lot, your LTV might be high, making refinancing more challenging or less beneficial.

A low LTV, on the other hand, makes you a more attractive refinancing candidate. It shows that you have substantial equity in the vehicle, reducing the lender’s risk. If you’ve been consistently paying down your principal and your car has held its value well, you’re in a strong position to secure a better rate through refinancing.

Beyond LTV: A Holistic View of Car Loan Approval

While the LTV ratio is undeniably crucial, it’s just one piece of the puzzle. Lenders consider a range of factors when deciding whether to approve your car loan and what terms to offer.

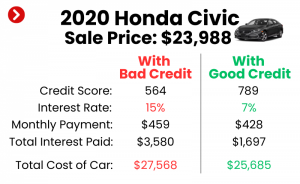

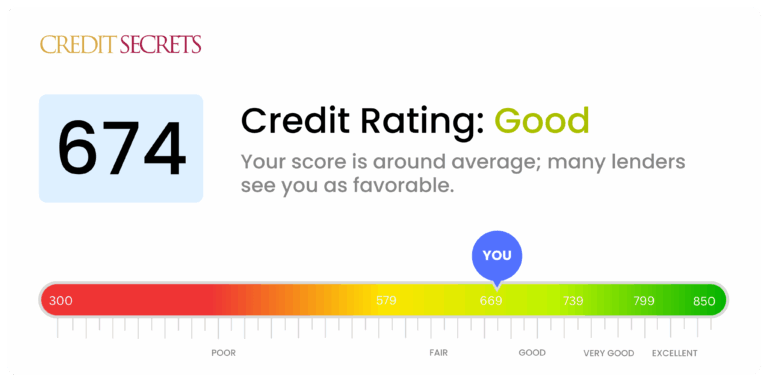

Your credit score is paramount. A higher credit score indicates a history of responsible borrowing and timely payments, making you a less risky borrower. It directly influences the interest rate you’ll receive. Lenders also look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A low DTI signals that you have enough disposable income to comfortably manage new loan payments.

Finally, your income stability and employment history also play a role. Lenders want to see consistent income that demonstrates your ability to make payments reliably over the loan term. It’s a comprehensive evaluation, where LTV is a significant, but not exclusive, determinant.

Pro Tips for Navigating Car Financing with LTV in Mind

Based on my experience guiding countless individuals through car financing, here are some invaluable pro tips:

- Pre-approval is Your Superpower: Get pre-approved for a car loan before you even step into a dealership. This gives you a clear understanding of your borrowing power, interest rate, and, crucially, allows you to determine a realistic LTV target. It shifts the negotiation power to you.

- Research Car Values Diligently: Use multiple reputable sources like Kelley Blue Book, Edmunds, and NADA guides to determine the fair market value of the car you’re interested in, as well as your trade-in. This knowledge prevents you from overpaying or accepting a lowball offer for your trade. You can even check listings on sites like AutoTrader or Cars.com to see what similar vehicles are selling for in your area.

- Don’t Forget Depreciation: Cars begin to depreciate the moment they leave the lot. A high LTV initially can quickly turn into negative equity as the car’s value drops. Aim for an LTV that gives you some buffer against this inevitable depreciation.

- Consider GAP Insurance Wisely: If your LTV is high (e.g., 100% or more), consider Guaranteed Asset Protection (GAP) insurance. This covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. It’s especially useful if you’re upside down on your loan.

- Negotiate Separately: When buying a car and trading one in, always negotiate the purchase price of the new car and the value of your trade-in separately. This prevents dealers from manipulating figures to make it seem like you’re getting a good deal on one, while losing out on the other.

Conclusion: Empower Your Car Purchase with LTV Knowledge

The Loan-to-Value (LTV) ratio is far more than just a financial term; it’s a powerful indicator of risk for lenders and a crucial tool for you, the car buyer. By understanding how LTV is calculated, its impact on your loan terms, and how to use a Loan To Value Ratio Car Calculator, you gain a significant advantage in the car buying process.

Taking the time to optimize your LTV through a solid down payment, a valuable trade-in, and wise purchasing choices will not only improve your chances of loan approval but also secure you better interest rates, lower monthly payments, and ultimately, save you thousands over the life of your car loan. Don’t let complex financial jargon deter you. Empower yourself with knowledge, leverage the tools available, and drive away with confidence, knowing you’ve secured the best possible deal.