Master Your Money: The Ultimate Guide to Calculate Payoff Amount On Car Loan

Master Your Money: The Ultimate Guide to Calculate Payoff Amount On Car Loan Carloan.Guidemechanic.com

Navigating the world of car loans can sometimes feel like deciphering a complex financial puzzle. You make your monthly payments diligently, but then a question arises: "What if I want to pay off my car loan early?" or "How much do I actually owe if I want to sell my car today?" This is where understanding how to calculate payoff amount on car loan becomes not just useful, but absolutely essential.

As an expert in personal finance and auto lending, I’ve seen firsthand how crucial this knowledge is for making smart financial decisions. Knowing your exact payoff figure empowers you, whether you’re looking to sell, trade-in, refinance, or simply achieve the satisfying milestone of debt-free car ownership. This comprehensive guide will demystify the process, providing you with all the insights and steps you need to take control of your car loan.

Master Your Money: The Ultimate Guide to Calculate Payoff Amount On Car Loan

What Exactly is a Car Loan Payoff Amount?

When you look at your car loan statement online, you’ll often see a "current balance." While this figure is helpful, it’s rarely the precise amount you’d need to pay today to fully satisfy your loan. The car loan payoff amount is the exact sum, including principal and all accrued interest up to a specific future date, that will completely close your loan account.

This distinction is vital because auto loans accrue interest daily. Your "current balance" typically reflects the principal balance as of your last payment or statement date. However, interest continues to build up every single day until the loan is paid off in full.

Think of it like this: your current balance is a snapshot from the past, while the payoff amount is a forward-looking calculation. It accounts for all the interest that will accumulate between today and the specific date you intend to make your final payment. This difference, often subtle but significant, is why getting an official payoff quote from your lender is almost always the best approach.

Why Would You Need Your Car Loan Payoff Amount?

There are several common scenarios where knowing your precise car loan payoff amount is not just recommended, but absolutely necessary. Failing to get this exact figure can lead to delays, unexpected costs, or even issues with your car’s title.

Let’s explore the key situations where this number becomes your financial compass. Understanding these will highlight why it’s so important to properly calculate payoff amount on car loan.

1. Selling Your Car Privately

If you decide to sell your car to another individual, you’ll need to know exactly how much is owed to the lender. This figure is crucial for setting an accurate selling price and ensuring you can transfer a clear title to the buyer. Any discrepancy can complicate the sale and title transfer process.

Based on my experience, many private sellers underestimate this amount, leading to awkward situations at the point of sale. You need to be able to pay off your lender immediately upon sale to release the lien and provide the buyer with a clean title.

2. Trading In Your Car at a Dealership

When you trade in your vehicle, the dealership will factor your car’s value and your remaining loan balance into the deal. They will contact your lender to obtain the official payoff amount. Knowing this number beforehand puts you in a stronger negotiating position.

You’ll be able to quickly assess if you have positive equity (your car is worth more than you owe) or negative equity (you owe more than your car is worth). This information is powerful leverage in any negotiation.

3. Refinancing Your Current Loan

Considering a new, lower interest rate or a more favorable loan term? When you refinance your car loan, your new lender will pay off your old loan directly. They will require an official payoff amount from your current lender to finalize the new loan.

Pro tips from us: always compare the official payoff amount with the principal balance on your statements. This ensures the new loan covers everything and avoids any lingering debt from the old lender.

4. Making Extra Payments or Paying Off Early

Perhaps your financial situation has improved, and you want to eliminate your car payment ahead of schedule. Making extra payments or paying off the entire loan early can save you a significant amount in interest over the life of the loan.

To confirm that your final payment truly closes the account, you’ll need the exact payoff amount for your chosen payment date. This prevents leaving a small, lingering balance that could still accrue interest or impact your credit.

5. Budgeting and Financial Planning

For those who are meticulous about their financial planning, knowing the precise payoff amount provides clarity. It allows you to accurately project when you’ll be debt-free and how much cash flow will be freed up. This aids in setting future financial goals, such as saving for a down payment on a home or investing.

The Core Components of Your Car Loan Payoff

To truly understand how to calculate payoff amount on car loan, it’s helpful to break down what makes up this figure. It’s more than just the number you see on your last statement.

Here are the key elements:

1. Outstanding Principal Balance

This is the original amount of money you borrowed, minus all the principal payments you’ve made so far. It represents the actual capital you still owe to the lender. Each monthly payment you make typically includes both interest and a portion that goes towards reducing this principal.

Over time, as you pay down your loan, this principal balance decreases. It’s the foundation upon which all other calculations for your payoff amount are built.

2. Accrued Interest (Per Diem)

This is perhaps the most critical component that differentiates your current balance from your payoff amount. Auto loans accrue interest daily, meaning a small amount of interest is added to your balance every single day. The "per diem" interest is the interest that has accumulated from your last payment date up to the specific date you request the payoff.

Common mistakes to avoid are assuming your online balance includes this daily accrual. It almost never does. This is why a payoff quote has an expiration date; the daily interest changes the total amount due as each day passes.

3. Any Outstanding Fees

While less common for car loans than for other types of debt, you might have outstanding fees that need to be settled. These could include:

- Late payment fees: If you’ve missed a payment or paid late, these fees would be added.

- Administrative fees: Some lenders might have small processing fees, though these are less frequent for early payoffs.

- Prepayment penalties: Extremely rare for car loans, but always worth checking your loan agreement. Most consumer car loans do not have these.

Always check your loan agreement or ask your lender if any additional fees would be included in your payoff amount. Transparency is key.

Step-by-Step Guide: How to Calculate Your Car Loan Payoff Amount

While understanding the components is important, actually getting the number is what matters most. There are two primary methods to calculate payoff amount on car loan, one highly recommended for accuracy, and another for conceptual understanding.

Method 1: The Easiest and Most Accurate Way – Requesting a Payoff Quote

This is by far the most reliable and recommended method. Your lender is the only entity that can give you the precise, legally binding payoff amount.

-

Contact Your Lender Directly:

- Phone: Call their customer service number. This is often the quickest way to get a quote and ask any questions. Be prepared to provide your account number and possibly your Vehicle Identification Number (VIN).

- Online Portal/App: Many lenders offer a self-service option through their online banking portal or mobile app. Look for sections like "Payoff Quote," "Loan Details," or "Early Payoff."

- In Person: If you have a local branch for your bank or credit union, you can visit them.

-

Specify Your Desired Payoff Date:

- When you request the quote, you’ll need to provide a specific date by which you intend to make the payoff payment. This is crucial because of the daily accruing interest. The lender will calculate the interest up to this exact date.

- Choose a date that gives you enough time for your payment to be processed and received by the lender, typically 7-10 business days out.

-

Understand the Payoff Quote:

- Your lender will provide a written (or sometimes verbal, followed by written confirmation) payoff quote. This document will clearly state the total amount due, usually broken down into principal, accrued interest, and any fees.

- Crucially, it will also specify the expiration date of that quote. The amount is only valid until that date. If your payment arrives after the expiration, the amount will be different, and you might still owe a small balance.

Pro tips from us: Always get the payoff quote in writing. An email or a downloadable document from their portal serves as official documentation. This protects you in case of any future disputes. Double-check the account number and the vehicle details on the quote to ensure it’s for the correct loan.

Method 2: Manual Calculation (For Understanding, Not Practical Use)

While not recommended for obtaining an official payoff amount, understanding how to manually estimate it can be enlightening. This helps you grasp the mechanics of daily interest.

-

Find Your Current Principal Balance:

- This can usually be found on your most recent loan statement or by logging into your online account. Remember, this is the principal after your last payment.

-

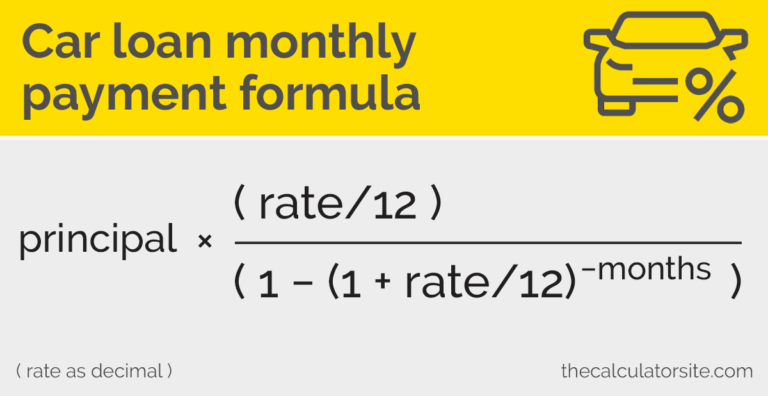

Determine Your Daily Interest Rate:

- Your Annual Percentage Rate (APR) is listed in your loan agreement. To get the daily rate, divide your APR by 365 (or 360, depending on your lender’s calculation method, though 365 is more common for auto loans).

- Example: If your APR is 6% (0.06), your daily rate is 0.06 / 365 = 0.00016438.

-

Calculate Per Diem Interest:

- Multiply your current principal balance by your daily interest rate. This gives you the amount of interest that accrues each day.

- Example: If your principal is $10,000 and your daily rate is 0.00016438, your daily interest is $10,000 * 0.00016438 = $1.64.

-

Count the Days to Payoff:

- Count the number of days from your last payment date up to your intended payoff date.

-

Calculate Total Accrued Interest:

- Multiply your daily interest amount by the number of days you counted.

- Example: If it’s 15 days, $1.64 * 15 = $24.60.

-

Add Any Outstanding Fees:

- Include any late fees or other charges not already part of your principal.

-

Sum It All Up:

- Your estimated payoff amount = Current Principal Balance + Total Accrued Interest + Outstanding Fees.

- Example: $10,000 (Principal) + $24.60 (Accrued Interest) = $10,024.60.

Based on my experience, this manual method is excellent for financial literacy but carries a risk of error. Lenders sometimes use slightly different day counts (360 vs. 365), and fees can be easily overlooked. Always rely on the official lender quote for accuracy.

Understanding the "Per Diem" Interest: The Hidden Variable

The concept of "per diem" interest is perhaps the most misunderstood aspect of calculating a car loan payoff. Per diem simply means "per day." This daily interest accrual is the reason your payoff amount isn’t just your principal balance.

Every day, a small amount of interest is added to your loan balance. This amount is calculated based on your outstanding principal balance and your loan’s annual interest rate. Even if you’re not making a payment, the interest clock is still ticking.

This continuous accrual explains why a payoff quote always has an expiration date. If you request a payoff for May 15th, the lender calculates interest up to that date. If your payment doesn’t arrive until May 20th, five additional days of interest would have accrued. This would leave a small, unpaid balance, and your loan wouldn’t be fully satisfied.

Always aim to send your payoff payment to arrive on or before the quoted payoff date. This ensures your payment covers the full amount of principal and interest the lender expects.

The Benefits of Paying Off Your Car Loan Early

Paying off a car loan early is a significant financial achievement that offers numerous advantages. It’s a strategy I frequently recommend for those who have the means.

Here’s why many people strive to eliminate their car debt ahead of schedule:

1. Saving on Interest Costs

This is arguably the most compelling benefit. By paying off your loan sooner, you reduce the total number of days over which interest can accrue. This directly translates into paying less money to the lender over the life of the loan. The higher your interest rate, the more substantial these savings can be.

Even small extra payments each month can shave off months or even years from your loan term and save you hundreds or thousands of dollars in interest.

2. Achieving Financial Freedom and Reducing Debt

Imagine one less monthly bill to worry about! Eliminating your car payment frees up a significant portion of your monthly budget. This extra cash flow can be redirected towards other financial goals, like building an emergency fund, investing, or tackling higher-interest debts like credit cards.

It provides a powerful sense of accomplishment and reduces financial stress. For more strategies on accelerating debt repayment, check out our guide on .

3. Improved Credit Score (Indirectly)

While paying off a loan closes that account, which can have a minor, temporary dip in your score due to a shorter average credit age, the long-term benefits are positive. Reducing your overall debt load improves your debt-to-income ratio, a key factor lenders consider. This signals to future lenders that you are a responsible borrower with less financial strain.

It demonstrates your ability to manage and eliminate debt, which is a strong positive for your credit profile.

4. Eliminating a Monthly Payment

The psychological and practical benefit of removing a recurring expense from your budget cannot be overstated. It provides greater flexibility and resilience in your personal finances. Should unexpected expenses arise, you have one less fixed cost to manage.

This newfound breathing room can be a game-changer for many households.

5. Full Ownership and Equity

Once your car loan is paid off, you officially own your vehicle outright. The lender’s lien is removed, and you receive the clear title. This means you have full equity in your car, which is an asset you can sell, trade, or use as collateral without any lender involvement.

This complete ownership provides peace of mind and simplifies future transactions involving your vehicle.

Potential Drawbacks or Considerations of Early Payoff

While paying off a car loan early offers many advantages, it’s not always the best financial move for everyone in every situation. It’s important to consider the potential downsides or alternative uses for that money.

Here are a few points to ponder before making a large early payoff:

1. Opportunity Cost

This is the most significant consideration. If you have extra cash, is paying off your car loan the best use of that money? For example, if you have high-interest credit card debt (e.g., 18-25% APR), paying that off should generally take precedence over a car loan with a much lower interest rate (e.g., 5-7% APR).

Similarly, if you haven’t built an emergency fund, that money might be better allocated to creating a financial safety net. The opportunity cost is what you give up by choosing one financial action over another.

2. Prepayment Penalties (Rare)

As mentioned, prepayment penalties are extremely uncommon for consumer auto loans in the United States. However, it’s always wise to double-check your original loan agreement. Some specialized or older loan contracts might have a clause that charges a fee for paying off the loan ahead of schedule.

If your loan does have such a penalty, you’ll need to weigh the penalty against the interest you would save by paying off early.

3. Impact on Credit Mix (Minor)

While paying off debt is generally good for your credit, closing a loan account can sometimes slightly impact your credit score. This is usually due to a change in your "credit mix" (the different types of credit you have) and potentially reducing the average age of your open accounts. However, this impact is typically minor and temporary, especially if you have other established credit accounts.

The benefits of reducing debt and improving your debt-to-income ratio usually outweigh this small, short-term effect.

Practical Scenarios: When to Use Your Payoff Amount

Understanding how to calculate payoff amount on car loan is one thing; knowing how to effectively use that information in real-world scenarios is another.

Let’s look at how your payoff amount plays a critical role in common car-related transactions:

1. Selling Your Car

When selling your car privately, the payoff amount is the non-negotiable figure you need to clear with your lender. Once you agree on a selling price with the buyer, you typically have two options:

- Buyer pays you, you pay the lender: The buyer pays you the agreed-upon price. You then immediately use a portion of that money (or all of it, if you have negative equity) to pay off your lender. Once the lender confirms receipt, they release the lien and send you the title. You then sign the title over to the buyer.

- Buyer pays the lender directly: Sometimes, the buyer may agree to pay the payoff amount directly to your lender, and the remaining balance (if any) to you. This streamlines the process but requires careful coordination.

Pro Tip: Always ensure the lender has received and processed the payoff before releasing the vehicle or signing over any documents.

2. Trading In Your Car

At a dealership, the process is usually more seamless. When you trade in your car, the dealer will typically:

- Appraise your vehicle: They determine its trade-in value.

- Request a payoff quote: The dealer will contact your lender to get the official payoff amount for your car loan.

- Calculate your equity: They compare the trade-in value to the payoff amount.

- Positive Equity: If your trade-in value is higher than your payoff, the difference is applied towards your new car purchase or given to you as cash.

- Negative Equity: If your payoff is higher than your trade-in value, you’ll have "negative equity" or be "upside down" on your loan. This difference is usually rolled into your new car loan, increasing the amount you borrow.

Knowing your payoff amount before stepping onto the lot gives you a huge advantage in negotiations.

3. Refinancing Your Loan

When you refinance, a new lender takes over your existing car loan. The process typically involves:

- Applying for a new loan: You apply with a new bank or credit union.

- New lender requests payoff: Once approved, your new lender will contact your current lender for an official payoff quote. This ensures they pay the exact amount needed to close your old account.

- New lender pays off old loan: The funds from your new loan are sent directly to your old lender.

- Lien transfer: Your old lender releases their lien, and the new lender places their lien on your vehicle.

Considering refinancing? Our article on can help you navigate the process. This ensures a smooth transition and that your old loan is fully settled.

Pro Tips for a Smooth Car Loan Payoff Process

Having advised countless individuals on their auto loan journeys, I’ve compiled some essential tips to ensure your car loan payoff process is as smooth and stress-free as possible.

-

Always Get a Written Payoff Quote: As stressed earlier, verbal quotes can be misremembered or misinterpreted. Demand a written quote (email, PDF download, or physical mail) that clearly states the payoff amount, the specific valid-until date, and your account information. This is your legal proof.

-

Send Funds Promptly and Strategically: Aim to send your payment several business days before the payoff quote’s expiration date. This allows for processing time and ensures the funds arrive and are posted by the lender before additional interest accrues. Use a traceable payment method, like a cashier’s check or wire transfer, for large sums.

-

Confirm the Payoff: Don’t assume the loan is closed once you send the money. A few days after your payment should have arrived, call your lender to confirm that the loan has been paid in full and the account is closed. Request a "Paid in Full" letter for your records.

-

Track Your Once the loan is paid off, the lender will release their lien on your vehicle. Depending on your state, they will either mail you the physical title or send an electronic release to your Department of Motor Vehicles (DMV). Follow up if you don’t receive it within a few weeks. A clear title is essential for selling or trading your car in the future.

-

Keep Meticulous Records: Save copies of your payoff quote, proof of payment, the "Paid in Full" letter, and your clear title. These documents are vital for future reference and can resolve any potential discrepancies.

For further reading on understanding consumer auto loans and managing debt, a trusted external source like the Consumer Financial Protection Bureau (CFPB) offers excellent resources. You can learn more about auto loans and your rights at https://www.consumerfinance.gov/consumer-tools/auto-loans/.

Conclusion: Empower Yourself by Knowing Your Payoff Amount

Understanding how to calculate payoff amount on car loan is more than just a financial exercise; it’s a critical skill that empowers you to make informed decisions about one of your most significant assets. Whether you’re planning to sell, trade, refinance, or simply enjoy the freedom of debt-free car ownership, having this exact figure at your fingertips is invaluable.

From years of observing financial trends and helping individuals manage their debt, I can confidently say that proactively engaging with your loan details, especially the payoff amount, positions you for greater financial control and peace of mind. Don’t rely on estimates or outdated balances. Take the simple steps to get an official quote from your lender, and you’ll be well on your way to mastering your automotive finances. Your journey to smart money management starts here.