Mastering Car Loan Computation: Your Ultimate Guide to Smart Auto Financing

Mastering Car Loan Computation: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

The thrill of buying a new car is undeniable. Whether it’s the sleek design, the latest technology, or the promise of new adventures, a vehicle represents freedom and possibility. However, beneath the excitement lies a crucial financial decision: how to finance your purchase. For most people, this means navigating the complexities of a car loan.

Understanding car loan computation isn’t just about crunching numbers; it’s about empowering yourself to make smart financial choices. A car loan is often one of the largest debts a person undertakes, second only to a mortgage. Misunderstanding its components can lead to paying thousands more than necessary or struggling with unaffordable monthly payments. This comprehensive guide will demystify the entire process, providing you with the knowledge and tools to compute, compare, and conquer your car loan.

Mastering Car Loan Computation: Your Ultimate Guide to Smart Auto Financing

The Core Elements of Your Car Loan – What You Need to Know

Before diving into formulas, it’s essential to grasp the fundamental components that make up any car loan. These elements are the building blocks upon which all computations are based. Ignoring any of them can lead to significant surprises down the road.

1.1 The Principal Amount: What You’re Actually Borrowing

The principal amount is simply the total sum of money you borrow from the lender. It’s not necessarily the sticker price of the car. This figure is derived by taking the vehicle’s selling price and then subtracting any down payment you make and the value of any trade-in vehicle.

Furthermore, it’s crucial to factor in sales tax, registration fees, and any other associated charges the dealer might roll into the loan. While these might seem minor individually, they can quickly add up, increasing the amount you need to borrow and, consequently, your overall monthly payments. Always ensure you have a clear breakdown of the "out-the-door" price before agreeing to a loan.

1.2 The Interest Rate (APR): The True Cost of Borrowing

The interest rate, often expressed as an Annual Percentage Rate (APR), is perhaps the most critical factor in car loan computation. It represents the cost of borrowing money, expressed as a percentage of the principal amount over a year. A higher APR means you’ll pay more in interest over the life of the loan, significantly increasing the total cost of your vehicle.

Several factors influence the interest rate you’re offered. Your credit score is paramount; a strong credit history typically qualifies you for lower rates, while a lower score can mean higher rates to offset the lender’s perceived risk. Market conditions, the specific lender, and even the loan term itself can also play a role. Based on my experience, shopping around for the best interest rate before you step into the dealership can save you thousands. Don’t just accept the first offer; compare rates from multiple banks, credit unions, and online lenders.

1.3 The Loan Term: How Long You’ll Be Paying

The loan term refers to the duration over which you agree to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This element has a direct and significant impact on both your monthly payment and the total amount of interest you’ll pay.

A shorter loan term, such as 36 or 48 months, will result in higher monthly payments because you’re paying off the principal over a shorter period. However, the trade-off is a lower total interest paid over the life of the loan. Conversely, a longer loan term (e.g., 72 or 84 months) will lead to lower monthly payments, making the car seem more affordable in the short term. The common mistake to avoid here is stretching the term too long, as this dramatically increases the total interest you’ll pay, making the car significantly more expensive in the long run.

1.4 Down Payment & Trade-In: Reducing Your Principal

A down payment is an initial sum of money you pay upfront toward the purchase of the car, reducing the amount you need to borrow. Similarly, if you have an existing vehicle, its trade-in value can also be applied to reduce the principal. Both of these are powerful tools in your car loan computation strategy.

The power of a significant down payment cannot be overstated. By reducing your principal, you immediately lower your monthly payments and, crucially, the total amount of interest you’ll accrue over the loan term. Pro tips from us suggest aiming for at least a 20% down payment if possible. This not only minimizes your loan amount but also helps prevent you from being "upside down" on your loan, which means owing more on the car than it’s worth. Even a small down payment can make a noticeable difference in your overall financial commitment.

Unveiling the Car Loan Computation Formula

While various online calculators make car loan computation easy, understanding the underlying formula provides invaluable insight. It allows you to see how each variable truly impacts your payments and total cost. This knowledge empowers you to manipulate the variables to your advantage.

2.1 The Amortization Formula Explained (Simplified)

The standard formula used to calculate monthly loan payments for an amortizing loan, like a car loan, is as follows:

Monthly Payment = P /

Let’s break down each variable and understand its role:

- P = Principal Loan Amount: This is the total amount of money you are borrowing after your down payment and trade-in are applied. As discussed, it includes the car’s price, sales tax, and any fees rolled into the loan.

- i = Monthly Interest Rate: This is not your APR. To use it in the monthly payment formula, you must convert your annual interest rate (APR) into a monthly rate. You do this by dividing your APR by 12 (for 12 months in a year). For example, if your APR is 6%, your monthly interest rate ‘i’ would be 0.06 / 12 = 0.005.

- n = Total Number of Payments: This represents the total number of monthly payments you will make over the life of the loan. You calculate this by multiplying your loan term in years by 12. So, a 5-year loan term would mean n = 5 * 12 = 60 payments.

This formula ensures that with each payment, a portion goes towards reducing the principal, and a portion covers the interest accrued since the last payment. Early in the loan, a larger portion of your payment goes towards interest, gradually shifting to more principal as the loan matures.

2.2 A Step-by-Step Walkthrough with an Example

Let’s put the formula into action with a practical scenario to illustrate car loan computation.

Scenario:

- Car Price: $30,000

- Down Payment: $5,000

- APR: 5%

- Loan Term: 60 months (5 years)

Step 1: Calculate the Principal Loan Amount (P)

- P = Car Price – Down Payment = $30,000 – $5,000 = $25,000

- Note: For simplicity, we’re excluding sales tax and fees in this example, but in a real scenario, they would be added to the principal.

Step 2: Calculate the Monthly Interest Rate (i)

- APR = 5% = 0.05

- i = APR / 12 = 0.05 / 12 = 0.00416667

Step 3: Calculate the Total Number of Payments (n)

- Loan Term = 60 months

Step 4: Plug the values into the formula

- Monthly Payment = $25,000 /

- Let’s break down the parts:

- (1 + i)^n = (1.00416667)^60 ≈ 1.283358

- i (1 + i)^n = 0.00416667 1.283358 ≈ 0.0053473

- (1 + i)^n – 1 = 1.283358 – 1 = 0.283358

- Monthly Payment = $25,000 * (0.0053473 / 0.283358)

- Monthly Payment = $25,000 * 0.018878

- Monthly Payment ≈ $471.95

Step 5: Calculate the Total Cost of the Loan and Total Interest Paid

- Total Payments = Monthly Payment n = $471.95 60 = $28,317.00

- Total Interest Paid = Total Payments – Principal Loan Amount = $28,317.00 – $25,000 = $3,317.00

As you can see, even with a relatively low interest rate, the interest payments add up over time. This calculation highlights the importance of understanding not just your monthly payment, but also the total cost of borrowing.

Beyond the Formula – Practical Tools and Considerations

While the formula is powerful, practical tools and strategic considerations are equally vital for effective car loan computation. These elements bridge the gap between theoretical knowledge and real-world application.

3.1 Car Loan Calculators: Your Best Friend

In today’s digital age, you don’t always need to manually compute your car loan. Online car loan calculators are incredibly powerful and user-friendly tools that can perform these complex computations in seconds. They are your best friend for quick comparisons and scenario planning.

To use them effectively, you’ll need the same inputs as our formula: the principal loan amount (or car price, down payment, trade-in), the interest rate (APR), and the loan term. Most calculators also allow you to factor in sales tax and other fees directly. You can find reliable car loan calculators on major financial websites or even on lender websites. For a great example of a robust and easy-to-use tool, check out the Bankrate Auto Loan Calculator. Using these tools lets you quickly compare how different interest rates, down payments, or loan terms will affect your monthly payment and total interest paid.

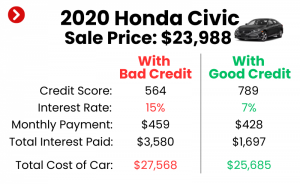

3.2 The Impact of Your Credit Score: A Financial Superpower

Your credit score is arguably the single most influential factor in determining the interest rate you’ll receive on a car loan. Lenders use it as a primary indicator of your creditworthiness – essentially, how likely you are to repay the loan on time. A high credit score (generally 700+) signals to lenders that you are a low-risk borrower, leading to more favorable interest rates and better loan terms.

Conversely, a low credit score can result in significantly higher interest rates, costing you thousands more over the life of the loan. Pro tips from us include checking your credit report and score well in advance of car shopping. If your score isn’t where you’d like it to be, take steps to improve it, such as paying down existing debt, making all payments on time, and disputing any errors on your report. Common mistakes include not checking your credit report at all, or worse, applying for multiple loans in a short period, which can temporarily ding your score.

3.3 Understanding the Total Cost of Ownership (TCO)

When budgeting for a car, it’s a common mistake to focus solely on the monthly car payment. However, the true financial commitment extends far beyond that single number. Understanding the Total Cost of Ownership (TCO) is crucial for a realistic assessment of affordability.

TCO includes not only your car loan payment but also a host of other expenses: auto insurance premiums, fuel costs, routine maintenance (oil changes, tire rotations), unexpected repairs, registration fees, and even potential parking fees. Based on my experience, many first-time car buyers overlook these critical ongoing costs. A car that seems affordable based on its monthly payment might quickly become a financial burden when all these other expenses are factored in. Budgeting holistically ensures you’re prepared for the full financial reality of car ownership.

Advanced Strategies and Common Pitfalls

Moving beyond the basics, there are several advanced strategies you can employ to optimize your car loan and common pitfalls to actively avoid. These insights can further enhance your car loan computation skills.

4.1 Pre-Approval vs. Dealer Financing: Which is Better?

One of the most powerful strategies when buying a car is to secure pre-approval for a loan from your bank, credit union, or an online lender before you visit the dealership. This means you know exactly how much you can borrow and at what interest rate before you even start negotiating.

The benefits of pre-approval are immense. It gives you significant negotiating power, allowing you to focus on the car’s price rather than getting distracted by loan terms. You walk into the dealership as a cash buyer, in effect. While the dealer might offer their own financing, often they can only beat your pre-approved rate if they’re willing to cut into their profit margins. Common mistakes include only looking at the monthly payment offered by the dealer without scrutinizing the APR or loan term, potentially leading to a less favorable deal.

4.2 The Power of Paying Extra: Accelerating Your Loan

Once you have a car loan, you don’t have to be passively bound by the amortization schedule. Making extra payments, even small ones, can significantly reduce the total interest you pay and shorten the life of your loan. This is because every extra dollar goes directly towards reducing your principal balance.

When you reduce the principal, less interest accrues in subsequent periods. Consider strategies like rounding up your monthly payment, making an extra payment whenever you have a windfall (tax refund, bonus), or adopting a bi-weekly payment schedule (paying half your monthly payment every two weeks, effectively making one extra full payment per year). This proactive approach, based on my experience, is one of the most effective ways to save money on your car loan.

4.3 Refinancing Your Car Loan: When and Why?

Refinancing involves taking out a new loan to pay off your existing car loan. This can be a smart financial move under specific circumstances, potentially saving you a substantial amount of money.

You might consider refinancing if interest rates have dropped since you initially took out your loan, or if your credit score has significantly improved. A lower interest rate means lower monthly payments and less total interest paid. Another reason might be to adjust your loan term – perhaps to lower your monthly payments if your financial situation has changed, though be mindful of increasing total interest. Based on my experience, it’s always worth revisiting your loan after 1-2 years, especially if your credit has improved or market rates have fallen. For a deeper dive into this, you might find our article, Guide to Refinancing Your Auto Loan, particularly helpful.

4.4 Gap Insurance & Extended Warranties: Are They Worth It?

When finalizing your car loan, you’ll likely be presented with optional add-ons like Gap Insurance and Extended Warranties. Understanding their purpose and necessity is key to avoiding unnecessary expenses.

- Gap Insurance: This covers the "gap" between what you owe on your loan and what your car’s actual cash value is, in case it’s totaled or stolen. If you make a small down payment, have a long loan term, or buy a car that depreciates quickly, you might owe more than the car is worth. In such cases, Gap Insurance can be a wise investment.

- Extended Warranties: These are service contracts that cover certain repairs after the manufacturer’s warranty expires. Their value depends heavily on the specific vehicle (some are more prone to issues), your risk tolerance, and the cost/coverage of the warranty itself. Common mistakes include rolling these high-cost items into your loan without fully understanding their terms, often paying interest on them for years. Always weigh the pros and cons carefully.

Budgeting for Your Car Loan – A Realistic Approach

Effective car loan computation extends beyond just the numbers; it integrates into your broader financial plan. A realistic budgeting approach ensures that your car ownership is a joy, not a burden.

5.1 The 20/4/10 Rule (or similar rule of thumb)

While not a strict law, rules of thumb can provide a helpful framework for car loan affordability. One popular guideline is the "20/4/10 Rule":

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price. This reduces your principal, lowers monthly payments, and helps you avoid being upside down on the loan.

- 4-Year Loan Term: Try to keep your loan term to no more than four years (48 months). This minimizes the total interest paid and ensures you build equity faster. While longer terms offer lower monthly payments, they dramatically increase total costs.

- 10% of Gross Income: Your total monthly car expenses (loan payment + insurance + maintenance/fuel) should not exceed 10% of your gross monthly income. This ensures your car costs remain manageable within your overall budget, leaving room for other financial goals.

Adhering to such guidelines can significantly improve your financial health and prevent you from becoming "car poor."

5.2 Creating a Comprehensive Car Budget

A robust budget goes beyond simple rules. It requires you to sit down and meticulously account for all potential car-related expenses. Don’t just consider the monthly car payment calculation. Think about:

- Insurance: Get quotes before buying the car, as premiums vary widely by vehicle and driver.

- Fuel: Estimate your weekly or monthly fuel consumption based on your driving habits and current gas prices.

- Maintenance: Set aside a monthly amount for routine maintenance (oil changes, tire rotations, brake pads, etc.) and a buffer for unexpected repairs.

- Registration & Fees: Annual costs that can add up.

- Parking/Tolls: If applicable in your area.

By creating a comprehensive car budget, you gain a clear picture of the true financial commitment. This allows you to select a vehicle and a loan that genuinely fits your lifestyle and financial capacity. For more detailed guidance on setting up your initial car budget, our article, Budgeting for Your First Car: A Complete Guide, offers extensive tips and worksheets.

Conclusion

Mastering car loan computation is an essential skill for anyone considering a vehicle purchase. By understanding the core elements – principal, interest rate, and loan term – and utilizing the amortization formula or online calculators, you transform what can seem like a daunting financial task into an empowering exercise. Remember that your credit score is a powerful lever, a substantial down payment is your ally, and a shorter loan term is often your friend against excessive interest.

Beyond the numbers, adopting practical strategies like pre-approval, understanding total cost of ownership, and budgeting comprehensively will safeguard your financial well-being. Don’t just drive, drive smart! With the insights provided in this guide, you are now well-equipped to navigate the world of auto financing with confidence, ensuring your car ownership journey is both exciting and financially sound.