Mastering the Charge: Your Ultimate Guide to Securing the Best EV Car Loan

Mastering the Charge: Your Ultimate Guide to Securing the Best EV Car Loan Carloan.Guidemechanic.com

The automotive world is undergoing a silent revolution, shifting gears from fossil fuels to electric power. Electric Vehicles (EVs) are no longer a niche fantasy; they’re a tangible, exciting reality that offers environmental benefits, reduced running costs, and a thrilling driving experience. As more drivers consider making the switch, a critical question often arises: how do I finance this future-forward investment?

Securing an EV car loan isn’t just about buying a car; it’s about investing in a sustainable lifestyle and often a smarter financial future. While the core principles of vehicle financing remain, EV loans come with unique considerations, opportunities, and even specialized products designed to get you behind the wheel of your dream electric ride. This comprehensive guide will illuminate every facet of EV financing, empowering you to navigate the loan landscape with confidence and make the most informed decisions.

Mastering the Charge: Your Ultimate Guide to Securing the Best EV Car Loan

The Electric Revolution and the Unique Nature of EV Loans

The transition to an electric vehicle is a significant decision, marked by environmental consciousness and often a desire for long-term savings. EVs, with their instant torque and quiet operation, offer a distinctly different driving experience. However, their upfront purchase price can sometimes be higher than comparable gasoline-powered cars, making financing a crucial part of the ownership journey.

This is where understanding the specifics of an EV car loan becomes paramount. Unlike traditional internal combustion engine (ICE) vehicle loans, EV financing often takes into account factors like government incentives, lower operating costs, and sometimes even specialized "green loan" products. These unique elements can significantly alter the total cost of ownership and the most advantageous financing path.

Why EVs Demand a Different Loan Perspective

Electric vehicles present a unique financial profile compared to their gasoline counterparts. While the initial sticker price might seem higher, the long-term cost savings are substantial. This includes significantly reduced fuel costs, lower maintenance needs due to fewer moving parts, and often attractive government incentives designed to encourage adoption.

Lenders are increasingly recognizing these differences. Some financial institutions now offer specialized EV loan products with slightly better interest rates or more flexible terms, acknowledging the lower environmental impact and the potentially more stable financial profile of EV owners. Understanding these nuances is key to securing the most favorable financing.

The Rise of "Green Loans" for Electric Vehicles

The concept of a "green loan" has emerged as a direct response to the growing demand for sustainable products, including electric vehicles. These are specific financial products offered by banks and credit unions that aim to incentivize environmentally friendly purchases. For an EV car loan, this might translate into a lower Annual Percentage Rate (APR) compared to a standard auto loan.

Based on my experience, these green loan offerings are becoming more prevalent, driven by both consumer demand and financial institutions’ commitments to sustainability. It’s always worth asking your potential lender if they have any such specialized programs for electric vehicle purchases. These small reductions in interest can add up to significant savings over the life of your loan.

Decoding EV Loan Options: What’s Available?

When it comes to financing your electric vehicle, you have a broad spectrum of options, each with its own advantages and considerations. Exploring these avenues thoroughly can help you pinpoint the best fit for your financial situation and your desired EV. It’s not a one-size-fits-all scenario, so careful comparison is essential.

Understanding the different types of lenders and their typical offerings will empower you to shop strategically for your EV car loan. Don’t limit yourself to the first option you encounter; a little research can yield substantial benefits.

Traditional Bank Loans

Many drivers begin their financing search with traditional banks, and for good reason. Large banks offer a wide array of auto loan products, including those for electric vehicles. They often have competitive rates, a robust online presence, and the convenience of existing relationships if you’re already a customer.

The process for an EV car loan through a traditional bank is generally straightforward, mirroring that of a conventional vehicle loan. You’ll apply, provide financial documentation, and receive an offer based on your creditworthiness. While they may not always offer specialized "green" rates, their sheer volume and stability make them a reliable choice.

Credit Union Loans

Credit unions are member-owned financial cooperatives known for their customer-centric approach and often highly competitive interest rates. Because they are not-for-profit, they can sometimes pass savings onto their members in the form of lower loan rates and fees. This makes them a particularly attractive option for an EV car loan.

Pro tips from us: Always check with local and national credit unions, even if you’re not currently a member. Joining a credit union is often easier than you think, and the potential savings on your EV loan could be well worth the effort. They also tend to be more flexible and understanding in their lending practices.

Manufacturer Financing Programs

Many EV manufacturers, especially luxury and high-volume brands, offer their own financing programs. These programs can come with enticing incentives such as very low APRs, cash rebates, or special lease deals specifically designed for their electric models. These are often seasonal or promotional, so timing can be everything.

It’s crucial to compare these manufacturer offers against what you can get from banks or credit unions. Sometimes, the manufacturer might offer a better rate, but other times, an independent lender could be more competitive. Always get quotes from multiple sources before committing.

Online Lenders

The digital age has brought forth a host of online lenders specializing in auto loans. These platforms offer unparalleled convenience, allowing you to apply for an EV car loan from the comfort of your home and often receive rapid approval decisions. Their business model can sometimes lead to very competitive rates, as they have lower overheads than brick-and-mortar institutions.

While convenient, it’s important to research online lenders thoroughly. Check reviews, understand their terms, and ensure they are reputable. They can be an excellent source for comparing rates quickly, but due diligence is key to a positive experience.

Specialized Green Loans and EV Loans

As mentioned earlier, some financial institutions are now explicitly offering "green loans" or dedicated EV car loan products. These loans are specifically tailored for eco-friendly purchases, and their terms might reflect the long-term benefits of EV ownership. This could include slightly lower interest rates, extended loan terms, or even specific incentives tied to energy efficiency.

When discussing your financing options, explicitly ask lenders if they have any specialized programs for electric vehicles. This proactive approach can unlock savings that might not be advertised upfront. These specialized products represent a growing trend in the financial sector to support sustainable living.

Government Incentives and Rebates: A Game Changer for EV Loans

One of the most significant differentiators for an EV car loan compared to a traditional vehicle loan is the availability of substantial government incentives and rebates. These programs, offered at federal, state, and even local levels, are designed to make electric vehicles more accessible and affordable. Understanding how they work is crucial, as they can directly impact the effective purchase price and, consequently, the amount you need to borrow.

These incentives aren’t just a bonus; they are a fundamental part of the EV financial equation. Factoring them into your calculations can significantly reduce your overall financial outlay, making an EV car loan much more manageable.

Federal Tax Credits

In many countries, governments offer federal tax credits for the purchase of new clean vehicles. In the United States, for example, the IRS provides tax credits that can amount to several thousand dollars for eligible new and sometimes used EVs. These credits are not instant rebates but rather a reduction in your federal tax liability.

Pro Tip: Eligibility for federal tax credits can be complex, involving factors like the vehicle’s battery capacity, manufacturing location, critical mineral and battery component sourcing, and the buyer’s income level. It’s absolutely essential to research the latest eligibility requirements for the specific EV model you are considering before you apply for an EV car loan. This credit can significantly reduce the amount you effectively pay for the vehicle. For the latest information on federal tax credits for clean vehicles, visit the IRS website.

State and Local Incentives

Beyond federal programs, many states and local municipalities offer their own set of incentives to encourage EV adoption. These can include direct rebates at the point of sale, tax exemptions, discounted vehicle registration fees, or even access to HOV (High-Occupancy Vehicle) lanes with a single occupant. Some local utilities also offer rebates for installing home charging equipment.

These regional incentives can vary widely, so a thorough investigation into what’s available in your specific area is highly recommended. Combining federal and state incentives can create a powerful financial advantage, substantially lowering the overall cost of your EV and thus reducing the principal amount of your EV car loan.

How Incentives Impact Your Loan Amount

The key takeaway here is that these incentives directly reduce the net cost of your EV. If you know you’re eligible for a $7,500 federal tax credit and a $2,000 state rebate, you can factor that $9,500 into your budget planning. This means you might need to borrow less, leading to lower monthly payments and less interest paid over the life of your EV car loan.

Common mistakes to avoid are neglecting to research incentives or assuming you’re automatically eligible. Always verify the most current programs and their specific criteria. Integrating these potential savings into your financial plan from the outset can dramatically improve the affordability of your electric vehicle purchase.

Key Factors Influencing Your EV Loan Approval and Rates

Securing the best EV car loan isn’t just about finding the right lender; it’s also about presenting yourself as a low-risk borrower. Several critical financial factors play a significant role in determining whether your loan is approved and, more importantly, the interest rate you’ll be offered. Understanding and optimizing these elements can lead to substantial long-term savings.

Lenders evaluate your financial health comprehensively. By being proactive and addressing any potential weaknesses, you can significantly strengthen your application for an EV car loan.

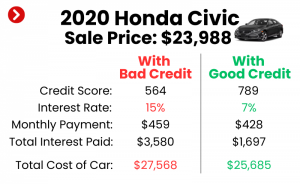

Your Credit Score: The Cornerstone

Your credit score is arguably the most important factor in securing any loan, and an EV car loan is no exception. It’s a three-digit number that represents your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score signals to lenders that you are a responsible borrower, making them more willing to offer you favorable interest rates.

Based on my experience, a credit score above 700 is generally considered "good," while scores above 760 often unlock the absolute best rates. If your score is lower, it’s worth taking steps to improve it before applying, such as paying down existing debts, disputing errors on your credit report, and making all payments on time. Read our detailed guide on boosting your credit score here!

Debt-to-Income Ratio (DTI)

Lenders also closely examine your debt-to-income (DTI) ratio. This percentage compares your total monthly debt payments (including the prospective EV loan) to your gross monthly income. A lower DTI ratio indicates that you have sufficient income to comfortably manage your existing debts and take on a new EV car loan.

A DTI ratio typically below 36% is often preferred by lenders, though some may go higher depending on other factors. If your DTI is high, consider paying down other debts or increasing your income before applying. This demonstrates financial stability and reduces perceived risk.

Down Payment Amount

Making a substantial down payment on your EV can significantly influence your loan terms. A larger down payment reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the EV car loan. It also signals financial stability to lenders, potentially leading to better rates.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment if possible. This not only lowers your loan amount but can also help offset any immediate depreciation and reduce the risk of being "underwater" on your loan (owing more than the car is worth).

Loan Term Length

The loan term, or the duration over which you agree to repay the loan, has a direct impact on your monthly payments and the total interest you’ll pay. Shorter terms (e.g., 36 or 48 months) result in higher monthly payments but significantly less interest over time. Longer terms (e.g., 72 or 84 months) offer lower monthly payments but accumulate more interest, making the car more expensive overall.

Carefully consider your budget and financial goals when choosing a loan term for your EV car loan. While lower monthly payments can be appealing, always calculate the total cost of the loan to ensure you’re making a financially sound decision.

Income Stability and Employment History

Lenders want assurance that you have a stable source of income to make your monthly payments consistently. They will typically ask for proof of employment, income statements (pay stubs, tax returns), and sometimes bank statements. A consistent employment history and a steady income stream are strong indicators of your ability to repay the EV car loan.

If you’ve recently changed jobs or have an irregular income, be prepared to provide additional documentation or explanations. Transparency and solid evidence of your financial capacity will always work in your favor.

The Application Process: A Step-by-Step Guide

Navigating the application process for an EV car loan can seem daunting, but by breaking it down into manageable steps, you can approach it systematically and confidently. A well-prepared applicant is more likely to secure favorable terms and avoid common pitfalls.

This section will walk you through the journey, from initial preparation to signing on the dotted line, ensuring you’re equipped for success.

Step 1: Get Pre-Approved

Before you even step foot in an EV dealership, obtaining pre-approval for an EV car loan is a game-changer. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate, pending a final vehicle choice. This crucial step provides several benefits.

It gives you a clear budget, prevents you from falling in love with a car you can’t afford, and empowers you to negotiate with dealerships on price, rather than just monthly payments. With a pre-approval in hand, you’re essentially a cash buyer, giving you significant leverage.

Step 2: Gather Your Documentation

Once you’re ready to formally apply for your EV car loan, having all your essential documents readily accessible will streamline the process. Lenders will require verification of your identity, income, and residency.

Typically, you’ll need:

- Government-issued photo identification (driver’s license, passport).

- Proof of income (recent pay stubs, W-2 forms, tax returns for self-employed individuals).

- Proof of residency (utility bill, lease agreement).

- Social Security Number.

- Details of the EV you intend to purchase (once decided).

Having these documents organized saves time and prevents delays in your EV car loan approval.

Step 3: Compare Multiple Offers

Common mistakes to avoid are accepting the first loan offer you receive. Just as you would compare different EV models, you should compare different loan offers. Apply to several lenders – banks, credit unions, and online providers – to get a range of interest rates and terms. This comparison shopping can reveal significant differences in APRs and fees, potentially saving you thousands over the life of your EV car loan.

Pay close attention not only to the interest rate but also to any origination fees, prepayment penalties, and other charges. A slightly higher interest rate with no fees might be better than a lower rate with substantial upfront costs.

Step 4: Read the Fine Print

Before you sign any loan agreement for your EV, meticulously read and understand all the terms and conditions. Don’t hesitate to ask questions about anything that isn’t clear. This includes understanding the Annual Percentage Rate (APR), the total amount of interest you’ll pay, any late payment fees, and whether there are penalties for paying off the loan early.

Ensuring complete transparency and understanding prevents future surprises and confirms that the EV car loan aligns with your financial expectations. It’s your money, and you have the right to know exactly where it’s going.

Beyond the Loan: Understanding the Total Cost of EV Ownership

While securing the best EV car loan is a major component of acquiring your electric vehicle, it’s crucial to look beyond the monthly payment. The true financial picture of EV ownership encompasses a range of ongoing costs and potential savings that can significantly alter the overall value proposition.

Adopting an EV is a holistic financial decision. By considering all aspects of ownership, you can make a truly informed choice and budget effectively for your new electric lifestyle.

Charging Costs vs. Fuel Costs

One of the most appealing aspects of EV ownership is the dramatic reduction in "fuel" costs. Electricity is generally much cheaper per mile than gasoline. However, charging costs can vary widely depending on whether you charge at home, at public stations, or at fast chargers. Home charging, especially during off-peak hours, is typically the most economical.

Pro tips from us: Calculate your estimated annual charging costs based on your driving habits and local electricity rates. This will give you a clearer picture of your ongoing expenses, which are likely to be significantly lower than what you’d spend at the gas pump, effectively reducing your overall transportation budget.

Maintenance and Repairs

EVs are renowned for their simpler powertrains, which translates to fewer moving parts and, generally, lower maintenance requirements compared to ICE vehicles. There’s no oil to change, no spark plugs to replace, and no complex exhaust systems to worry about. This inherent simplicity often results in substantial savings on routine maintenance.

While brakes may last longer due to regenerative braking, and tires will still need replacing, the overall maintenance burden is typically lighter. Factor these potential savings into your total cost of ownership analysis; they can make your EV car loan feel even more affordable in the long run.

Insurance Premiums

EV insurance premiums can sometimes be higher than those for comparable gasoline cars. This is often due to the advanced technology, higher repair costs for specialized components, and the relative newness of the market. However, as EVs become more common and repair networks expand, these costs may stabilize.

It’s wise to get insurance quotes for your specific EV model before committing to the purchase. Compare rates from multiple providers, as premiums can vary significantly. Some insurers may even offer discounts for eco-friendly vehicles or for drivers who utilize telematics devices.

Resale Value Considerations

Historically, electric vehicles have shown strong resale values, particularly as demand continues to grow and battery technology improves. However, like any vehicle, depreciation will occur. Factors such as battery degradation, technological advancements in newer models, and market demand will influence future resale value.

While difficult to predict with absolute certainty, the general trend suggests EVs hold their value well, especially premium models. This strong resale potential can be a positive factor when considering the long-term financial implications of your EV car loan. Discover how to pick the perfect EV that fits your needs in our comprehensive guide!

Future Trends in EV Financing

The landscape of EV financing is dynamic, constantly evolving to meet consumer needs and technological advancements. As electric vehicles become more mainstream, we can expect to see innovative financing solutions emerge, further simplifying and diversifying the path to EV ownership. Staying aware of these trends can provide a competitive edge.

The future of EV car loans is likely to be even more tailored and flexible, reflecting the unique attributes of electric mobility.

Growing Availability of Specialized EV Loan Products

As mentioned earlier, the trend towards dedicated "green loans" and specialized EV car loan products is only expected to grow. More banks, credit unions, and even fintech companies will likely offer financing options with preferential rates or terms for electric vehicles, recognizing their environmental and long-term economic benefits. This competition will ultimately benefit consumers, driving down rates and increasing accessibility.

Battery Leasing and Subscription Models

Some manufacturers are exploring or already offering battery leasing options, where you purchase the EV but lease the battery pack separately. This can significantly reduce the upfront purchase price of the vehicle, making it more affordable and potentially impacting the structure of your EV car loan. Similarly, all-inclusive EV subscription models are gaining traction, bundling the vehicle, insurance, maintenance, and charging into a single monthly fee.

These alternative ownership models present interesting alternatives to traditional EV car loans, catering to different financial preferences and usage patterns. They offer flexibility and reduce the commitment associated with outright ownership.

Integration with Smart Home and Energy Systems

As EVs become more integrated with smart home energy systems and potentially vehicle-to-grid (V2G) technology, their financial value proposition could further expand. An EV that can power your home during an outage or even sell electricity back to the grid might be seen as a more valuable asset by lenders and owners alike. This could influence future appraisals and, indirectly, loan terms.

The evolving role of the EV from a mere mode of transport to a mobile power bank will undoubtedly reshape how its value is perceived and financed. These innovations promise to make EV ownership even more attractive and financially integrated into our daily lives.

Conclusion: Powering Your EV Journey with Smart Financing

Embarking on the journey of electric vehicle ownership is an exciting prospect, promising a blend of cutting-edge technology, environmental responsibility, and significant long-term savings. While the initial investment might seem substantial, understanding the intricacies of an EV car loan is your key to unlocking this future-forward mode of transportation efficiently and affordably.

From leveraging government incentives to meticulously comparing loan offers and understanding the total cost of ownership, every step you take contributes to a smarter financial decision. Remember that your credit score, down payment, and chosen loan term are powerful levers in securing the most favorable rates. By being proactive, informed, and diligent, you can confidently navigate the financing landscape.

The world of EV financing is ripe with opportunities for the discerning buyer. Don’t just settle for any loan; seek out the best EV car loan that aligns with your financial health and supports your sustainable lifestyle goals. The road to electric driving is smoother and more accessible than ever before – go forth and charge ahead with confidence!