Mastering the Loan Application From A Car Dealership: Your Ultimate Guide to Approval and Savvy Financing

Mastering the Loan Application From A Car Dealership: Your Ultimate Guide to Approval and Savvy Financing Carloan.Guidemechanic.com

The dream of a new car – that fresh scent, the sleek lines, the promise of new adventures – is often shadowed by the daunting process of securing financing. For many, the loan application from a car dealership is a mysterious and intimidating step. It’s a moment filled with questions, anxieties, and the fear of making a costly mistake.

But what if you could approach this process with complete confidence, armed with knowledge and strategies that empower you to secure the best possible terms? This comprehensive guide is designed to demystify the car dealership loan application, transforming a potential stressor into a clear, manageable path toward driving away in your dream vehicle. We’ll delve deep into every aspect, ensuring you’re not just approved, but approved on your terms.

Mastering the Loan Application From A Car Dealership: Your Ultimate Guide to Approval and Savvy Financing

Why Consider Financing Through a Car Dealership?

Before we dive into the nitty-gritty of the application itself, it’s worth understanding why many choose to pursue a loan application from a car dealership in the first place. While you always have the option of securing outside financing, dealerships offer a unique set of advantages.

Firstly, convenience is a major draw. A dealership acts as a one-stop shop, allowing you to select your vehicle, apply for financing, and complete all paperwork under one roof. This integrated approach saves valuable time and simplifies what could otherwise be a fragmented process.

Secondly, dealerships often have established relationships with a wide network of lenders. This means they can shop your application around to various banks, credit unions, and even manufacturer-specific finance companies. This broad reach can sometimes result in competitive interest rates and flexible terms that you might not find by approaching a single lender on your own.

Finally, dealerships occasionally offer special financing incentives directly from manufacturers, such as low-APR deals or cash-back offers that are tied to using their financing partners. These promotions can be incredibly attractive, potentially leading to significant savings over the life of the loan. However, it’s crucial to always compare these offers with what you could secure independently.

The Pre-Application Checklist: Preparing for Success

The key to a successful loan application from a car dealership isn’t just filling out forms; it’s about preparation. Walking into a dealership without understanding your financial standing is like going to battle without armor. Based on my experience in the automotive and finance sectors, many buyers make this critical error, putting them at a significant disadvantage.

1. Know Your Credit Score Inside and Out

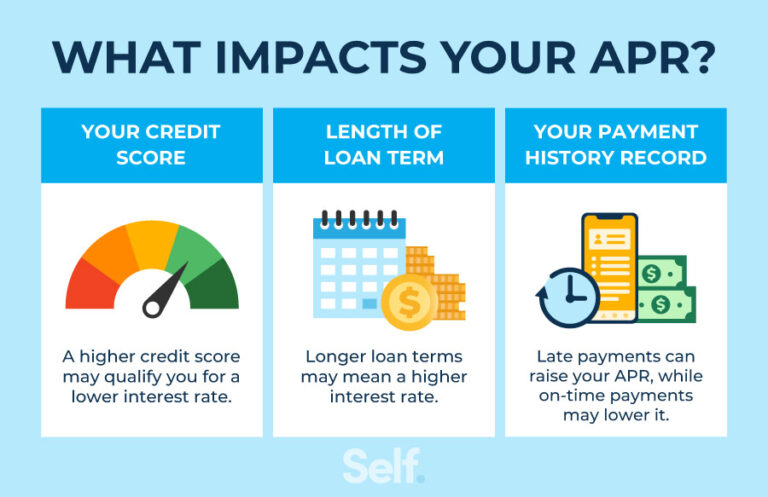

Your credit score is arguably the most influential factor in your loan approval and the interest rate you’ll receive. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay your debt. A higher score signifies lower risk to the lender.

Before you even step foot on a lot, pull your credit report and score. You’re entitled to a free credit report from each of the three major bureaus (Equifax, Experian, TransUnion) once a year through AnnualCreditReport.com. Review it for any errors or inaccuracies, which could negatively impact your score. Knowing your score range (e.g., excellent: 800+, good: 700-799, fair: 600-699, poor: below 600) gives you a realistic expectation of the rates you might qualify for.

2. Establish a Realistic Budget

Beyond the car’s sticker price, a responsible budget considers the total cost of ownership. This includes not just the monthly loan payment, but also insurance premiums, fuel costs, maintenance, and potential registration fees. It’s easy to get fixated on a low monthly payment, but this can mask a longer loan term or a higher overall cost.

Determine how much you can comfortably afford each month without straining your finances. This involves looking at your income, existing debts, and regular expenses. Having a clear budget in mind prevents you from falling in love with a car you genuinely can’t afford, protecting your financial well-being in the long run.

3. Save for a Healthy Down Payment

A significant down payment is one of your strongest allies when applying for an auto loan. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. From a lender’s perspective, a larger down payment also reduces their risk.

When you put more money down, your loan-to-value (LTV) ratio improves, making you a more attractive borrower. Aim for at least 10-20% of the vehicle’s purchase price, if possible. Even a small down payment is better than none, especially for those with less-than-perfect credit.

4. Understand Your Trade-In Value

If you plan to trade in your current vehicle, research its market value before you visit the dealership. Websites like Kelley Blue Book (KBB.com) and Edmunds.com provide excellent estimates based on your car’s condition, mileage, and features. Knowing this value gives you leverage during negotiations.

Your trade-in acts essentially as an additional down payment, reducing the amount you need to finance. Don’t let the dealership undervalue your trade; be prepared to negotiate or even sell it privately if the offer isn’t satisfactory.

5. Gather Essential Documents

Streamline the loan application from a car dealership by having all necessary documents ready. This proactive step demonstrates your seriousness and preparedness, making the process smoother for everyone involved.

Typically, you’ll need:

- Valid Driver’s License: For identification and proof of driving eligibility.

- Proof of Income: Recent pay stubs (2-3 months), W-2 forms, or tax returns (for self-employed individuals).

- Proof of Residence: A utility bill (gas, electric, water) or bank statement with your current address.

- Proof of Insurance: While you might not have the policy for the new car yet, showing proof of current insurance indicates you’re a responsible driver.

- References: Sometimes, personal or professional references are requested.

The Loan Application Process at the Dealership: Step-by-Step Guide

Once you’ve done your homework, you’re ready to navigate the actual loan application from a car dealership. Understanding each step will help you maintain control and make informed decisions.

1. Initial Discussion with the Salesperson

Your journey typically begins with a salesperson. They’ll discuss your vehicle preferences, budget, and financing needs. While they’ll ask about your desired monthly payment, it’s often wise to discuss the total purchase price first. Focusing solely on monthly payments can lead to longer loan terms and higher overall interest.

Be honest about your financial situation, but don’t overshare. Remember, your goal is to secure the best deal, not just any deal.

2. Filling Out the Application Form

The finance manager (sometimes called the F&I manager) will guide you through the official credit application. This form will request detailed personal and financial information, including your full name, address, Social Security Number, employment history, income, and existing debts.

Accuracy is paramount here. Providing false information on a credit application is a serious offense and can lead to loan denial, or worse, legal repercussions. Take your time to ensure all details are correct.

3. Authorizing a Credit Check

By signing the application, you grant the dealership permission to pull your credit report. This results in a "hard inquiry" on your credit file, which can temporarily lower your score by a few points. However, multiple hard inquiries for auto loans within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry. This allows you to shop around for rates without significant cumulative damage to your score.

4. Dealer Submits to Lenders

Once your application is complete, the finance manager will submit it to various lenders within their network. These lenders will review your credit history, income, and debt-to-income ratio to assess your risk and determine what loan terms they can offer.

This process can take anywhere from a few minutes to a few hours, depending on the complexity of your application and the responsiveness of the lenders. The finance manager acts as an intermediary, negotiating with lenders on your behalf to find the most favorable terms.

5. Receiving Offers and Negotiation

After receiving offers from multiple lenders, the finance manager will present you with the best options. This is a critical juncture where your preparedness truly pays off. Don’t simply accept the first offer.

Carefully review the annual percentage rate (APR), the loan term (number of months), and the total monthly payment. Compare these offers with any pre-approvals you secured independently. Be ready to negotiate the APR, especially if you have a strong credit score.

6. Understanding the Terms

It’s crucial to understand every aspect of the loan agreement before signing.

- APR (Annual Percentage Rate): This is the true cost of borrowing, expressed as a yearly rate, including interest and certain fees. A lower APR means less money paid over the life of the loan.

- Loan Term: This is the duration of the loan, typically ranging from 36 to 84 months. A longer term means lower monthly payments but more interest paid overall. A shorter term means higher monthly payments but less total interest.

- Monthly Payment: Ensure this fits comfortably within your budget.

Also, be aware of any additional products the dealership might offer, such as extended warranties, GAP insurance, or paint protection. While some of these might be beneficial, they add to the total loan amount and should be considered carefully. For more insights on this, you might find our article on Understanding Car Loan Interest Rates helpful.

Factors That Influence Your Loan Approval

Beyond your credit score, several other elements weigh heavily on the lender’s decision when you submit a loan application from a car dealership. Understanding these can help you position yourself as a more attractive borrower.

1. Credit History and Score

As mentioned, your credit score is foundational. Lenders scrutinize your payment history for any late payments, defaults, or bankruptcies. They also look at your credit utilization (how much credit you’re using compared to your available credit) and the length of your credit history. A consistent history of on-time payments and responsible credit use signals reliability.

2. Debt-to-Income (DTI) Ratio

Your DTI ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to manage additional debt. Generally, a DTI ratio below 36% is considered good, while anything above 43% might make lenders hesitant. A lower DTI shows that you have more disposable income available to cover a new car payment.

3. Employment Stability

Lenders prefer borrowers with stable employment histories. A consistent job, especially one you’ve held for several years, demonstrates a reliable income stream. Frequent job changes or gaps in employment can raise red flags about your ability to make consistent payments.

4. Down Payment Amount

We’ve discussed this, but its importance can’t be overstated. A substantial down payment reduces the loan amount, lowers the lender’s risk, and often results in better loan terms. Pro tips from us: Even if you don’t have a large sum, any down payment helps, especially if your credit isn’t stellar.

5. Vehicle Choice

The type of vehicle you choose also plays a role. Lenders are often more comfortable financing newer, lower-mileage vehicles that hold their value well. These cars pose less risk because if you default, the lender can recoup more of their losses by repossessing and selling the vehicle. Financing an older, high-mileage car can be more challenging.

Common Mistakes to Avoid During Your Loan Application

Navigating the loan application from a car dealership can be tricky, and certain pitfalls are common. Being aware of these can save you money, time, and stress.

1. Not Knowing Your Credit Score

Walking into a dealership blind to your credit score is a significant mistake. Without this knowledge, you can’t accurately gauge the fairness of the interest rates offered. You’re also susceptible to accepting higher rates than you qualify for. Always check your score first.

2. Skipping Pre-Approval

Securing a pre-approval from your bank or credit union before visiting the dealership provides you with a powerful negotiation tool. It gives you a benchmark rate to compare against the dealership’s offers. If the dealership can’t beat your pre-approval, you always have a fallback option.

3. Focusing Only on Monthly Payments

While monthly payments are important for budgeting, fixating solely on them can lead to being upsold on a longer loan term, which means paying more interest over time. Always consider the total cost of the loan, including the APR and the overall amount of interest you’ll pay.

4. Lying on the Application

Never falsify information on your credit application. This is considered loan fraud and carries severe consequences, including immediate loan denial, legal action, and a severely damaged credit history. Honesty is always the best policy.

5. Ignoring the Fine Print

Common mistakes to avoid are signing without fully understanding the APR, loan term, any additional fees, and the conditions of the loan. Rush is the enemy of good decision-making. Take your time to read every document thoroughly, ask questions, and don’t hesitate to seek clarification on anything you don’t understand.

Improving Your Chances of Approval (Even with Less-Than-Perfect Credit)

Even if your credit history isn’t pristine, there are strategies you can employ to strengthen your loan application from a car dealership and increase your likelihood of approval.

1. Bring a Co-signer

A co-signer with good credit can significantly boost your chances of approval. A co-signer agrees to be equally responsible for the loan, meaning if you default, they are obligated to make the payments. This reduces the risk for the lender, making them more willing to approve your application or offer better terms.

2. Increase Your Down Payment

As highlighted before, a larger down payment directly reduces the loan amount and the lender’s risk. If you have less-than-perfect credit, saving up for a substantial down payment can be a game-changer. It shows the lender you have a vested interest and are serious about repayment.

3. Opt for a Cheaper Car

Choosing a more affordable vehicle lessens the financial burden on both you and the lender. A smaller loan amount is inherently less risky. Consider a used car in good condition or a new, entry-level model if your budget and credit history are concerns.

4. Work on Your Credit Beforehand

If you’re not in a rush, take some time to improve your credit score before applying. Pay down existing debts, especially those with high interest rates. Make all your payments on time. Dispute any errors on your credit report. Even a few months of diligent credit management can make a difference.

Pre-Approval vs. Dealership Financing: A Comparison

A crucial step in smart car buying is understanding the difference between getting pre-approved by an external lender and seeking financing directly through the dealership. Both have their merits, and the best strategy often involves leveraging both.

Pre-approval means you’ve applied for a loan with a bank or credit union before visiting the dealership and have received a conditional offer. This offer specifies the maximum loan amount, the interest rate, and the loan term you qualify for. It gives you a solid offer in hand, effectively making you a cash buyer in the dealership’s eyes, as you already have secured funding.

Dealership financing, as we’ve discussed, involves the dealership submitting your application to multiple lenders in their network. Their goal is to find you an attractive offer, often competing with your pre-approval rate.

The best approach? Get pre-approved first. This arms you with a baseline interest rate. Then, when you’re at the dealership, allow them to try and beat that rate. If they can, fantastic! If not, you have your pre-approval to fall back on. This dual strategy ensures you’re getting the most competitive terms available. For more detailed information on car loan options, a trusted resource like the Consumer Financial Protection Bureau (CFPB) offers excellent guides on how to shop for a car loan.

Navigating the Negotiation Phase

The loan application from a car dealership isn’t just about getting approved; it’s about getting the best deal. This involves active negotiation, not just on the car’s price, but on the financing terms as well.

Don’t feel pressured to accept the first offer presented. Compare the APR, loan term, and monthly payment from various lenders. If you have a pre-approval, use it as leverage. Politely ask the finance manager if they can beat your existing offer. Be prepared to walk away if the terms aren’t favorable, as there are always other dealerships and lenders.

Remember, every percentage point off your APR can save you hundreds, if not thousands, of dollars over the life of the loan. Focus on the total cost of the loan, not just the monthly payment.

The Final Steps: Signing the Papers and Driving Away

Once you’ve agreed on the vehicle price and secured favorable loan terms through your loan application from a car dealership, you’ll move to the signing phase. This is where all the agreed-upon details are formalized.

Take your time reading every document carefully before signing. This includes the purchase agreement, the loan contract, and any additional product agreements. Ensure that the APR, loan term, and total purchase price match what you negotiated. Ask questions about anything unclear, and don’t feel rushed. Once everything aligns with your understanding, you can confidently sign the papers, get your keys, and drive away in your new vehicle!

Conclusion: Drive Away with Confidence

The loan application from a car dealership doesn’t have to be a source of stress. By understanding the process, preparing thoroughly, and knowing what to expect, you can approach it with confidence and clarity. From checking your credit score and setting a realistic budget to understanding loan terms and negotiating effectively, every step contributes to a successful and financially savvy outcome.

Remember, knowledge is power. Arm yourself with the insights shared in this guide, and you’ll be well-equipped to secure the best possible auto loan, allowing you to focus on the joy of your new ride. What was your experience like applying for a car loan? Share your tips and questions in the comments below – we’d love to hear from you!