Mastering the Road Ahead: Your Ultimate Guide to Getting a Car Loan and Driving Away Smart

Mastering the Road Ahead: Your Ultimate Guide to Getting a Car Loan and Driving Away Smart Carloan.Guidemechanic.com

The dream of owning a car is a powerful one for many. It represents freedom, independence, and convenience. But for most of us, turning that dream into a reality involves navigating the often complex world of car loans. This isn’t just about getting a loan to buy a car; it’s about making an informed financial decision that empowers you, rather than burdens you, for years to come.

As an expert blogger and professional in personal finance, I understand the nuances of vehicle financing. Based on my experience, approaching the process with knowledge and strategy can save you thousands of dollars and countless headaches. This comprehensive guide will break down everything you need to know about securing an auto loan, ensuring you drive away not just with a new set of wheels, but with peace of mind.

Mastering the Road Ahead: Your Ultimate Guide to Getting a Car Loan and Driving Away Smart

Understanding the Fundamentals of a Car Loan

Before you even step foot on a dealership lot or browse online listings, it’s crucial to grasp what a car loan truly is and how it functions. At its core, a car loan is a sum of money borrowed from a lender to purchase a vehicle, with the agreement to repay that amount, plus interest, over a predetermined period.

What Exactly is an Auto Loan?

Think of a car loan as a specialized installment loan. The car itself often serves as collateral, making it a secured loan. This means if you fail to make your payments, the lender has the legal right to repossess the vehicle to recover their losses. This distinction is vital because it affects the interest rates you might qualify for compared to unsecured loans.

The primary purpose of a vehicle loan is to make car ownership accessible. Instead of paying the full purchase price upfront, which is rarely feasible for most individuals, you make manageable monthly payments over several years. This allows you to spread the cost and fit it into your regular budget.

Key Terms You Need to Know

Navigating the world of car financing requires familiarity with certain terminology. Understanding these terms will empower you during discussions with lenders and help you compare offers effectively.

- Principal: This is the original amount of money you borrow to purchase the car. It does not include interest or fees.

- Interest Rate: Expressed as a percentage, this is the cost of borrowing money from the lender. A lower interest rate means you’ll pay less over the life of the loan.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically measured in months (e.g., 36, 48, 60, 72, or even 84 months). A longer term usually means lower monthly payments but more interest paid overall.

- Annual Percentage Rate (APR): The APR is a more comprehensive measure of the cost of borrowing. It includes not only the interest rate but also any additional fees associated with the loan, expressed as a single annual percentage. This is the figure you should use for direct comparisons between different loan offers.

- Down Payment: This is the initial amount of money you pay towards the car’s purchase price from your own savings. A larger down payment reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest you’ll pay.

- Collateral: In the case of a car loan, the vehicle itself acts as collateral. This means the lender can seize the car if you default on your payments.

Based on my experience, many first-time car buyers focus solely on the monthly payment without fully understanding these underlying terms. This can lead to unexpected costs and a less favorable financial outcome. Always ask for the APR to get a clear picture of the total borrowing cost.

Where to Find Your Car Loan: Exploring Your Options

When you’re ready to get a loan to buy a car, you’ll discover there are several avenues available, each with its own set of advantages and disadvantages. Exploring all your options before committing is a pro tip that can significantly impact your financial well-being.

Dealership Financing

Most car dealerships offer in-house financing or work with a network of lenders. This can be a convenient "one-stop shop" approach, as you can often complete the purchase and financing paperwork in a single location. Dealerships sometimes offer special promotions, low-interest rates, or incentives on specific models.

However, convenience shouldn’t override diligence. The rates offered by dealerships might not always be the most competitive, as they often mark up the interest rate to earn a profit. Always compare their offer with pre-approvals you’ve secured elsewhere.

Banks and Credit Unions

Traditional banks and credit unions are popular choices for auto loans. They often offer competitive interest rates, especially if you have a strong banking relationship or excellent credit. Credit unions, in particular, are known for having member-friendly rates and terms, as they are non-profit organizations.

Applying directly to a bank or credit union before visiting a dealership allows you to get pre-approved for a specific loan amount. This gives you a clear budget and negotiating power, as you walk into the dealership already knowing your financing terms.

Online Lenders

The digital age has brought forth a plethora of online lenders specializing in vehicle loans. These platforms often provide quick application processes, fast approvals, and competitive rates, as they have lower overhead costs than traditional brick-and-mortar institutions. They can be particularly useful for comparing multiple offers simultaneously from the comfort of your home.

However, always ensure the online lender is reputable and secure. Read reviews and check for proper licensing before sharing your personal financial information.

Manufacturer Financing Programs

Some car manufacturers offer their own financing arms, like Ford Credit or Toyota Financial Services. These programs frequently provide very attractive rates, sometimes even 0% APR, especially on new vehicles or during promotional periods. These offers are usually reserved for buyers with excellent credit scores.

It’s always worth checking if the manufacturer of the car you’re interested in has any special financing deals. These can be incredibly cost-effective if you qualify.

Pro tips from us: Always get pre-approved for a car loan from at least one outside lender (a bank or credit union) before you even set foot in a dealership. This gives you a baseline interest rate and a clear understanding of your budget, making you a more confident and informed negotiator.

The Car Loan Application Process: A Step-by-Step Guide

Securing a car loan might seem daunting, but breaking it down into manageable steps makes the journey much smoother. Based on my experience guiding countless individuals through this process, following a structured approach is key to a successful outcome.

Step 1: Assess Your Financial Health and Set a Budget

Before you even dream about specific car models, take a realistic look at your finances. This involves reviewing your credit score, income, existing debts, and monthly expenses. Understand what you can comfortably afford in terms of a monthly payment, insurance, fuel, and maintenance. Don’t forget to factor in a potential down payment.

A critical part of this step is checking your credit report. This allows you to identify any errors and get a clear picture of your creditworthiness. You can obtain a free credit report annually from each of the three major credit bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com.

Step 2: Get Pre-Approved for a Loan

This is arguably the most crucial step for securing a favorable auto loan. Applying for pre-approval from banks, credit unions, or online lenders before you start car shopping offers immense benefits. It gives you:

- A clear budget: You’ll know exactly how much you can borrow.

- Negotiating power: You become a cash buyer in the eyes of the dealership, allowing you to focus solely on the car’s price rather than being swayed by monthly payment tricks.

- A benchmark: You’ll have an interest rate to compare against any offers from the dealership.

Pre-approval involves a "soft" credit inquiry, which won’t impact your credit score. Once you’re ready to proceed with a specific lender, they’ll conduct a "hard" inquiry.

Step 3: Gather Necessary Documents

Lenders will require various documents to process your car loan application. Having these ready in advance can expedite the approval process. Typical documents include:

- Proof of identity (driver’s license, passport).

- Proof of income (pay stubs, tax returns, bank statements).

- Proof of residence (utility bill, lease agreement).

- Social Security number.

- Information about the vehicle you intend to purchase (if known).

The more prepared you are, the smoother your application will go.

Step 4: Shop for Your Car and Negotiate the Price

With your pre-approval in hand, you can now confidently shop for a car. Focus on negotiating the vehicle’s purchase price, knowing your financing is already secured. Don’t mention your pre-approval until you’ve agreed on a price for the car itself. This prevents the dealership from potentially inflating the price, knowing you have financing.

Common mistakes to avoid are applying to too many lenders at once within a short period, which can negatively impact your credit score. Instead, aim to get pre-approved by 2-3 lenders within a 14-day window; credit bureaus typically count these as a single inquiry. Also, never let the dealership "run your credit" with multiple lenders without your explicit consent and understanding.

Step 5: Finalize the Loan and Read the Fine Print

Once you’ve chosen your vehicle and negotiated a price, it’s time to finalize the loan to buy a car. Carefully review all loan documents. Pay close attention to:

- The APR: Ensure it matches your pre-approved rate or is better.

- The loan term: Understand how long you’ll be making payments.

- Any additional fees: Question anything that seems unclear or unexpected.

- Prepayment penalties: Confirm there are no penalties for paying off the loan early.

Never feel rushed or pressured to sign anything you don’t fully understand. It’s your right to take the documents home and review them thoroughly before signing.

Factors Affecting Your Car Loan Approval and Interest Rate

Several crucial factors play a significant role in determining whether your car loan is approved and, more importantly, the interest rate you’ll be offered. Understanding these elements can help you optimize your financial position before applying.

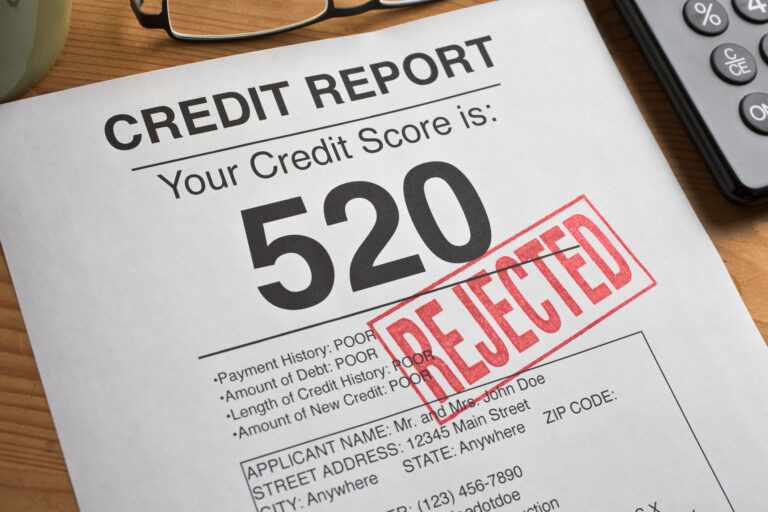

Your Credit Score

This is arguably the single most important factor. Your credit score is a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use it to assess the risk of lending money to you.

- Excellent Credit (780+): You’ll typically qualify for the lowest interest rates and most favorable terms.

- Good Credit (670-779): You’ll still get competitive rates, though perhaps not the absolute best.

- Fair Credit (580-669): You might face higher interest rates and stricter terms.

- Poor Credit (Below 580): Getting approved can be challenging, and interest rates will be significantly higher.

A higher credit score signals to lenders that you are a reliable borrower, making them more willing to offer attractive rates.

Your Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to gauge your ability to take on additional debt. A lower DTI ratio indicates that you have more disposable income to manage new loan payments, making you a less risky borrower.

From my perspective as a finance expert, aim for a DTI ratio below 36%, with no more than 28% going towards housing costs. While car loans are separate, a high overall DTI can still hinder approval or lead to higher rates.

The Loan Amount and Term

The size of the loan and its repayment period also influence the interest rate. Larger loan amounts can sometimes carry slightly higher rates due to increased risk for the lender. Similarly, longer loan terms (e.g., 72 or 84 months) often come with higher interest rates because the lender is exposed to risk for a more extended period.

While a longer term means lower monthly payments, it typically results in paying significantly more interest over the life of the loan. It’s a trade-off that requires careful consideration.

Your Down Payment

Making a substantial down payment reduces the amount you need to borrow, which directly lowers your monthly payments and the total interest paid. Furthermore, a larger down payment demonstrates your financial commitment and reduces the lender’s risk, potentially leading to a better interest rate.

A general recommendation is to aim for at least 10-20% of the car’s purchase price as a down payment. This can also help you avoid being "upside down" on your loan (owing more than the car is worth) early in the loan term.

The Vehicle Type (New vs. Used)

Lenders often view new car loans as less risky than used car loans. New cars generally hold their value better initially, and their depreciation curve is more predictable. As a result, new car loans often come with slightly lower interest rates.

Used car loans, particularly for older models, can carry higher interest rates due to increased risk of mechanical issues and a faster depreciation rate.

Current Economic Conditions and Interest Rates

Broader economic factors, such as the Federal Reserve’s benchmark interest rate, influence the overall lending environment. When interest rates are low across the economy, car loan rates tend to follow suit, making it a more opportune time to borrow. Conversely, in a rising interest rate environment, car loans become more expensive.

Staying informed about these macroeconomic trends can help you decide the best time to apply for a loan to buy a car.

Navigating Different Credit Scenarios for Your Car Loan

Your credit standing significantly shapes your experience when seeking a car loan. Whether your credit is stellar, average, or needs improvement, understanding your options and strategies is crucial.

Excellent Credit: Leveraging Your Advantage

If you have a credit score of 780 or higher, congratulations! You’re in an enviable position. Lenders view you as a low-risk borrower, meaning you’ll qualify for the most competitive interest rates and favorable loan terms.

- Strategy: Don’t settle. Shop around aggressively for the absolute best APR. Banks, credit unions, and manufacturer financing programs will all be vying for your business. Leverage your strong credit to negotiate not just the car price, but also the financing terms.

- Pro Tip: Even with excellent credit, consider making a down payment. It further reduces your total interest paid and can help you pay off the loan faster, freeing up your budget sooner.

Good/Average Credit: Strategies for Better Rates

Most people fall into the good (670-779) or average (580-669) credit categories. While you might not get the rock-bottom rates of those with excellent credit, you still have strong options.

- Strategy: Focus on strengthening your application. A larger down payment can significantly improve your chances of getting a better rate. Consider a shorter loan term if your budget allows, as this often comes with a lower interest rate. Shop multiple lenders – credit unions often offer better rates for this tier of credit than traditional banks.

- Improving Credit: If you have time before buying, work on boosting your score. Pay down existing debts, especially credit card balances, and avoid opening new credit lines. Even a 20-30 point increase can make a difference.

Bad Credit: Options, Pitfalls, and Rebuilding

Having a credit score below 580 presents the most challenges, but it doesn’t necessarily mean you can’t get a loan to buy a car. It does mean you’ll likely face higher interest rates and potentially less flexible terms.

- Strategy: Be realistic about your options. Expect higher APRs, which compensate lenders for the increased risk. Focus on making a significant down payment to reduce the loan amount and demonstrate your commitment.

- Consider a Co-signer: Pro tips from us for those with less-than-perfect credit: If possible, a co-signer with good credit can significantly improve your chances of approval and help you secure a lower interest rate. Ensure both parties understand the responsibilities, as the co-signer is equally liable for the debt.

- Subprime Lenders: Some lenders specialize in bad credit car loans. While they offer solutions, their rates are typically very high. Read all terms carefully.

- Avoid "Buy Here, Pay Here" Lots: While convenient, these dealerships often charge exorbitant interest rates and may not report payments to credit bureaus, which means you won’t build credit history.

- Rebuilding Credit: If you absolutely need a car, take the loan with the understanding that consistent, on-time payments will help rebuild your credit score. After a year or two, you might be able to refinance your car loan at a much lower interest rate.

Regardless of your credit score, transparency and preparedness are your best allies. Be honest about your financial situation and be ready to provide all requested documentation promptly.

Understanding the True Cost of Your Car Loan

Focusing solely on the monthly payment is a common pitfall when securing a loan to buy a car. The true cost of your vehicle goes far beyond that single number, encompassing various fees and charges that can add up significantly over the loan’s lifetime.

Interest Paid Over Time

This is the most substantial "hidden" cost. While a lower monthly payment might seem appealing, it often comes with a longer loan term, meaning you’ll pay interest for more years. For instance, a 72-month loan will almost always result in paying more total interest than a 48-month loan for the same principal amount, even if the interest rate is identical.

A common mistake buyers make is focusing solely on the monthly payment, overlooking the total interest paid. Always ask for the total cost of the loan, including all interest, before signing. Use an online car loan calculator to compare different scenarios.

Fees Associated with the Loan

Beyond interest, several fees can inflate the overall cost of your auto loan. These can include:

- Origination Fees: A fee charged by the lender for processing the loan.

- Documentation Fees (Doc Fees): Charged by dealerships for preparing paperwork. These can vary significantly by state and dealership, so ask for an explanation.

- Registration and Title Fees: Government-mandated fees for registering the vehicle and transferring its title.

- Prepayment Penalties: Though less common now, some loans might charge a fee if you pay off the loan early. Always confirm your loan has no such penalty.

Always inquire about all fees upfront and get them itemized. Some fees are negotiable, especially dealership-specific ones.

Add-Ons and Their Impact

Dealerships often present various "add-ons" during the financing process. While some might offer value, many are high-profit items that can unnecessarily inflate your loan amount and, consequently, your total interest paid.

- Extended Warranties: These provide coverage beyond the manufacturer’s warranty. While peace of mind is valuable, research third-party options and compare costs. Often, dealership extended warranties are overpriced.

- GAP Insurance (Guaranteed Asset Protection): This covers the "gap" between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. It’s often recommended, especially if you have a small down payment or a long loan term. However, you can often get it cheaper from your auto insurance provider or an independent insurer than from the dealership.

- Paint Protection/Fabric Protection: These are typically high-margin products with questionable long-term value. A good car wash and interior detailing kit often achieve similar results for a fraction of the cost.

- Etching/Anti-theft Devices: Often presented as mandatory, these are frequently overpriced. Check if your insurance company offers a discount for such features; if not, they might not be worth the added cost.

Carefully consider each add-on’s necessity and value. Remember, you can almost always decline these products or shop for them elsewhere. Don’t let pressure tactics push you into purchasing items you don’t need or want.

Smart Strategies for Car Loan Repayment and Management

Once you’ve secured your loan to buy a car and are driving your new vehicle, the journey isn’t over. Effective loan management can save you money, improve your financial standing, and ensure a smoother ownership experience.

Making Extra Payments

One of the most effective ways to save money on interest and pay off your car loan faster is to make extra payments whenever possible. Even small additional contributions can significantly reduce the principal balance, meaning less interest accrues over time.

- Bi-weekly Payments: Instead of one monthly payment, split your payment in half and pay every two weeks. This results in 26 half-payments a year, equivalent to 13 full monthly payments, effectively paying an extra month’s payment annually.

- Round Up Payments: If your payment is $375, round it up to $400. That extra $25 goes directly to the principal.

- Windfalls: Use bonuses, tax refunds, or unexpected income to make a lump-sum payment towards the principal.

Always confirm with your lender that extra payments are applied directly to the principal and that there are no prepayment penalties.

Refinancing Your Car Loan

Refinancing involves taking out a new loan to pay off your existing auto loan, ideally at a lower interest rate or with more favorable terms. This can be a smart move if:

- Interest rates have dropped since you took out your original loan.

- Your credit score has significantly improved, qualifying you for a better rate.

- You want to change your loan term – either shorten it to pay off faster or extend it to lower monthly payments (though extending increases total interest).

For more insights into managing your monthly budget, check out our article on . Understanding your cash flow is key to making extra payments or determining if refinancing is viable.

Setting Up Auto-Pay

Most lenders offer the convenience of automatic payments. Setting up auto-pay ensures you never miss a payment, which is crucial for maintaining a good credit score and avoiding late fees. Many lenders even offer a small interest rate discount (e.g., 0.25%) for enrolling in auto-pay.

Just be sure to have sufficient funds in your account on the payment date to prevent overdraft fees.

Budgeting for Car Expenses Beyond the Loan

Remember, a car loan is just one component of car ownership costs. Smart management also involves budgeting for ongoing expenses:

- Insurance: Premiums can be substantial and vary widely.

- Fuel: A consistent and often rising cost.

- Maintenance: Regular oil changes, tire rotations, and unexpected repairs.

- Registration and Taxes: Annual fees required by your state.

- Parking/Tolls: If applicable in your area.

Having a clear budget for these expenses ensures your car remains a convenience, not a financial burden.

When to Consider Refinancing Your Car Loan

Refinancing your auto loan can be a powerful financial tool, potentially saving you a significant amount of money over the life of your loan. It’s essentially replacing your current car loan with a new one, often from a different lender, under new terms.

Lower Interest Rates Are Available

The most common reason to refinance is to secure a lower interest rate. Interest rates fluctuate over time, and if current market rates are significantly lower than what you’re currently paying, refinancing could lead to substantial savings on your total interest paid and potentially lower your monthly payments. This is especially true if you took out your original loan to buy a car when rates were higher.

Your Credit Score Has Improved

When you initially applied for your car loan, your credit score might have been lower. If you’ve diligently made on-time payments, paid down other debts, and seen your credit score improve, you’re now a more attractive borrower. Lenders may offer you a much better interest rate than you initially received. This is a clear indicator that it’s time to explore refinancing options.

You Want to Change Your Loan Term

Refinancing allows you to adjust the length of your repayment period.

- To Lower Monthly Payments: If your financial situation has changed and you need more breathing room in your budget, you could extend your loan term. Be aware that while this reduces your monthly outlay, it will likely increase the total interest paid over the life of the loan.

- To Pay Off Faster: Conversely, if your income has increased, you might want to shorten your loan term. This means higher monthly payments, but you’ll pay off the loan quicker and incur less total interest.

You Want to Remove a Co-signer

If you initially needed a co-signer to get approved for your car loan, but your credit has since improved, refinancing can allow you to remove that co-signer. This frees them from their liability and demonstrates your financial independence.

When NOT to Refinance

While refinancing offers many benefits, it’s not always the best option. Avoid refinancing if:

- Your current interest rate is already very low or if the new rate isn’t significantly better to justify the effort and potential fees.

- You’re near the end of your loan term. The majority of interest is paid at the beginning of a loan; refinancing late in the term might not save you much.

- Your car is "upside down" (you owe more than it’s worth), making it harder to find a lender willing to refinance without additional collateral or a higher interest rate.

Before deciding to refinance, compare the total cost of your current loan with the total cost of the new loan, including any refinancing fees. A valuable external resource for understanding how APR works and comparing loan costs can be found at the Consumer Financial Protection Bureau’s website: External Link: CFPB – What is the Annual Percentage Rate (APR)?

Final Pro Tips for a Smooth Car Loan Journey

Navigating the path to securing a loan to buy a car can feel complex, but with the right mindset and strategies, it can be a smooth and empowering experience. Here are some ultimate pro tips to ensure you make the best decisions.

Do Your Homework Thoroughly

Knowledge is power, especially when it comes to financial decisions. Research not just the cars you’re interested in, but also the lenders, interest rates, and loan terms available. Understand your own credit score and financial standing before you even begin.

This preparation will equip you to ask intelligent questions, spot unfavorable terms, and negotiate with confidence. Don’t rely solely on the dealership for information about financing.

Don’t Rush the Process

Buying a car and securing a loan are significant financial commitments. Avoid making impulsive decisions or allowing yourself to be pressured by salespeople. Take your time to compare vehicles, get multiple loan offers, and review all paperwork carefully.

Rushing often leads to overlooking crucial details that could cost you money in the long run. Patience is a virtue that pays dividends in car financing.

Negotiate Everything

From the car’s purchase price to the trade-in value of your old vehicle, and most importantly, the terms of your auto loan, everything is negotiable. Don’t be afraid to haggle. Dealerships expect it.

Having pre-approved financing from an outside lender gives you immense leverage to negotiate the car’s price independently from the financing. If the dealership can beat your pre-approved rate, that’s a bonus, but always have your own financing in hand as a fallback.

Read the Fine Print – Every Single Word

This tip cannot be stressed enough. Loan agreements are legal documents, and you are bound by their terms once you sign. Carefully read the entire contract, paying close attention to the APR, loan term, total amount financed, any fees, and prepayment clauses.

If you don’t understand something, ask for clarification. If you’re still unsure, consider having a trusted friend or even a financial advisor review the documents with you. Never sign anything you haven’t fully comprehended.

Consider the Total Cost of Ownership

Remember that the loan to buy a car is just one aspect of owning a vehicle. Factor in insurance, fuel, maintenance, and potential repair costs when setting your budget. A car that’s cheap to finance might be expensive to own due to high insurance premiums or frequent repairs.

If you’re also considering how to save for a down payment, our guide on can provide valuable strategies to help you accumulate the funds needed for a stronger start.

Conclusion: Drive Away with Confidence and Financial Savvy

Securing a loan to buy a car is a significant financial step, but it doesn’t have to be a source of stress. By approaching the process with knowledge, diligence, and a strategic mindset, you can navigate the complexities of auto financing with confidence. From understanding the core terms and exploring your lending options to meticulously reviewing your loan agreement and managing your repayments, every step you take contributes to a more favorable outcome.

Remember, the goal isn’t just to get approved for an auto loan; it’s to secure a loan that aligns with your financial goals and empowers you to enjoy your new vehicle without unnecessary financial strain. By following the comprehensive advice outlined in this guide, you’ll be well-equipped to make smart decisions, save money, and truly master the road ahead. Happy driving!