Mastering the Road: Your Comprehensive Guide to a 580 Credit Score Car Loan

Mastering the Road: Your Comprehensive Guide to a 580 Credit Score Car Loan Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. However, for many, the path can seem daunting, especially when faced with a less-than-perfect credit score. If your credit score hovers around 580, you might be wondering if a car loan is even within reach.

The good news is, securing a 580 credit score car loan is absolutely possible. While it presents unique challenges, with the right strategies and a clear understanding of the process, you can drive away in your desired vehicle. This comprehensive guide will equip you with the knowledge, tips, and insights needed to navigate the world of car financing with low credit.

Mastering the Road: Your Comprehensive Guide to a 580 Credit Score Car Loan

We’ll delve deep into what a 580 credit score means for auto lenders, explore effective strategies to improve your chances of approval, and reveal where to find the best loan options. Our ultimate goal is to empower you with the information to make informed decisions and achieve your car ownership dreams.

Understanding Your 580 Credit Score

A FICO credit score of 580 falls within the "Fair" or "Subprime" range. This means that while you’re not in the "Very Poor" category, lenders generally perceive you as a higher risk borrower compared to those with good or excellent credit. This perception is crucial to understand when seeking a bad credit car loan.

Lenders use credit scores to assess the likelihood of you repaying your loan obligations. A 580 score suggests a history that might include late payments, high credit utilization, or even past collections or bankruptcies. Consequently, they often offer less favorable terms to mitigate their risk.

Based on my experience as a financial expert, a 580 credit score signals to lenders that while you have some credit history, there are areas for improvement. It means you’ll likely face higher interest rates and potentially stricter loan conditions than someone with a score above 670. Don’t let this discourage you; instead, let it inform your approach.

Is Getting a Car Loan with a 580 Credit Score Possible?

Absolutely, yes! It’s a common misconception that a 580 credit score automatically disqualifies you from getting a car loan. While it’s true that you won’t qualify for the absolute best interest rates, many lenders specialize in subprime auto loans and are willing to work with individuals in your credit tier.

The key is to approach the process strategically and realistically. You’ll need to demonstrate your ability and willingness to repay the loan, even with a less-than-stellar credit history. This often involves a combination of financial preparation and choosing the right lending partners.

The journey might require a bit more effort and patience, but the rewards of securing a reliable vehicle are well worth it. Think of this as an opportunity to not only get a car but also to begin rebuilding your credit profile.

Key Strategies for 580 Credit Score Car Loan Approval

To maximize your chances of approval and secure the best possible terms for your 580 credit score car loan, consider implementing the following strategies. Each point builds a stronger case for you as a borrower.

A. Save for a Significant Down Payment

One of the most impactful steps you can take is to save for a substantial down payment. A larger down payment significantly reduces the amount you need to borrow, which in turn lowers the lender’s risk. This makes your application much more attractive to them.

Putting down 10% to 20% of the vehicle’s purchase price is often recommended. For a $20,000 car, this would mean a down payment of $2,000 to $4,000. Not only does it help with approval, but it also reduces your monthly payments and the total interest paid over the life of the loan.

Pro tips from us: Start saving early and consider selling an older vehicle to contribute to your down payment. Even an extra few hundred dollars can make a difference in your loan terms. A significant down payment shows financial responsibility and commitment.

B. Find a Co-signer (If Possible)

Bringing a co-signer with good credit onto your application can dramatically improve your chances of approval and help you secure a lower interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default. This significantly reduces the lender’s risk.

A good co-signer is someone with an excellent credit score, a stable income, and a low debt-to-income ratio. This person is typically a trusted family member or close friend. Ensure they understand the full responsibility they are undertaking before agreeing.

Common mistakes to avoid are choosing a co-signer who isn’t financially stable or failing to communicate clearly about payment responsibilities. Remember, their credit is on the line just as much as yours.

C. Improve Your Credit Score (Even Slightly)

While you might need a car now, taking a few weeks or months to make some quick improvements to your credit score can pay dividends. Even a small bump in your score can move you into a better risk category, potentially lowering your interest rate.

Start by checking your credit report from all three major bureaus (Experian, Equifax, TransUnion) for errors. You can do this for free at AnnualCreditReport.com. Dispute any inaccuracies immediately, as these can negatively impact your score.

Focus on paying down existing credit card balances to reduce your credit utilization ratio. Also, make sure all your current bills are paid on time. These actions demonstrate responsible financial behavior to potential lenders.

D. Get Pre-Approved First

Seeking pre-approval for a 580 credit score car loan is a highly recommended step. Pre-approval gives you a clear understanding of how much you can borrow, the estimated interest rate, and the loan terms before you even step onto a dealership lot. This puts you in a much stronger negotiating position.

You can seek pre-approval from various sources, including credit unions, online lenders, and even some traditional banks that specialize in bad credit car loans. Don’t be afraid to apply to a few different lenders within a short timeframe (usually 14-45 days) to compare offers; multiple inquiries for the same type of loan within this window are typically counted as a single hard inquiry.

Knowing your pre-approved amount prevents you from falling in love with a car you can’t afford. It also shifts the focus from "can I get a loan?" to "which car fits my pre-approved budget?".

E. Set a Realistic Budget and Choose the Right Vehicle

When you have a 580 credit score, it’s crucial to set a realistic budget that considers more than just the monthly car payment. Think about the total cost of ownership, which includes insurance, fuel, maintenance, and potential repairs. Opting for a more affordable and reliable vehicle is often the wisest choice.

Based on my experience, many individuals with lower credit scores make the mistake of buying too much car. This can lead to financial strain and even loan default. Focus on a practical, reliable used car that meets your essential needs rather than a luxury model.

A modest, well-maintained used car will be easier to finance, have lower insurance costs, and generally be more forgiving on your budget. Remember, this first car loan is an opportunity to build positive credit history for future, better loans.

F. Be Prepared with Documentation

Lenders will want to see proof that you can consistently afford your loan payments. Being prepared with all necessary documentation streamlines the application process and shows you are serious and organized.

Typically, you’ll need proof of income (pay stubs, tax returns), proof of residence (utility bill), a valid driver’s license, and bank statements. Some lenders may also request references or employment verification. Having these documents ready makes the application smoother.

Being transparent and thorough with your documentation builds trust with the lender. It demonstrates that you have nothing to hide and are a responsible applicant.

Where to Find Lenders for a 580 Credit Score Car Loan

Finding the right lender is paramount when seeking a 580 credit score car loan. Not all lenders are created equal, especially when dealing with subprime credit. Knowing where to look can save you time, effort, and money.

A. Subprime Auto Lenders

Many financial institutions specialize in bad credit car loans. These lenders understand the challenges associated with lower credit scores and have specific programs designed for borrowers in the 500-620 FICO range. They often have more flexible underwriting criteria compared to traditional banks.

You can find these lenders online through dedicated auto loan platforms or by searching for "bad credit car loans near me." Be prepared for higher interest rates, as this is how they offset the increased risk. Always compare offers from multiple subprime lenders.

Pro tips from us: Look for lenders that report to all three major credit bureaus. This ensures that your timely payments will positively impact your credit score, helping you build a better financial future.

B. Credit Unions

Credit unions are often more forgiving than large commercial banks when it comes to car financing with low credit. Because they are member-owned, they tend to prioritize their members’ financial well-being and may offer more personalized service and potentially better rates, even for those with a 580 credit score.

If you are already a member of a credit union, inquire about their auto loan options. If not, consider joining one; many have open membership requirements. They often have lower fees and more competitive interest rates than traditional banks, making them an excellent option for auto loan approval tips.

It’s worth noting that credit unions might still have certain income or debt-to-income ratio requirements. However, their willingness to consider your overall financial picture, beyond just your credit score, can be a significant advantage.

C. Dealership Financing (Buy Here, Pay Here)

Dealership financing, particularly "Buy Here, Pay Here" (BHPH) lots, can be an option for individuals with very low credit scores or limited credit history. These dealerships directly finance the loan themselves, often making approval easier since they set their own lending criteria.

The primary advantage of BHPH dealerships is convenience and high approval rates. However, they typically come with significant drawbacks. Interest rates are notoriously high, often reaching the maximum allowed by law, and vehicle choices can be limited to older, higher-mileage cars.

Common mistakes to avoid are jumping into a BHPH loan without fully understanding the terms or comparing it to other options. Many BHPH lenders do not report payments to credit bureaus, meaning you won’t build credit history, and some may have predatory practices. Always read the fine print carefully and consider other options first.

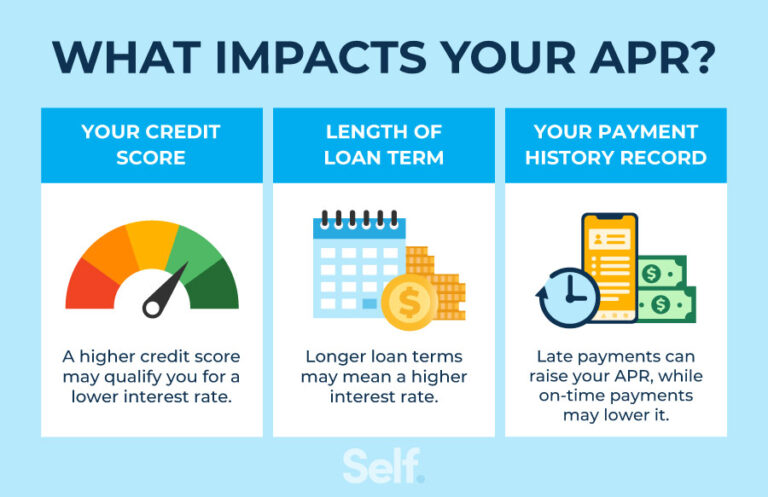

Understanding Interest Rates and Loan Terms

When you’re approved for a 580 credit score car loan, it’s crucial to understand that your interest rate will be higher than someone with excellent credit. This is a direct reflection of the increased risk lenders assume when financing a subprime borrower. Expect rates to be in the double digits.

The Annual Percentage Rate (APR) is the most important number to focus on. It includes not only the interest rate but also any additional fees, giving you the true cost of borrowing. A higher APR means you’ll pay significantly more over the life of the loan.

The loan term, or the length of time you have to repay the loan, also plays a critical role. While a longer loan term (e.g., 72 or 84 months) might offer lower monthly payments, it dramatically increases the total amount of interest you’ll pay. For instance, a loan for $15,000 at 18% APR over 72 months will cost thousands more in interest than the same loan over 48 months.

Pro tips from us: Always try to secure the shortest loan term you can comfortably afford. This minimizes the total interest paid and helps you build equity in your car faster. Focus on the total cost of the loan, not just the monthly payment.

The Application Process for a 580 Credit Score Car Loan

The application process for a 580 credit score car loan is similar to a standard auto loan but with a few extra considerations. Being prepared and understanding what lenders look for will make it smoother.

Lenders will scrutinize your debt-to-income (DTI) ratio. This measures how much of your gross monthly income goes towards debt payments. A lower DTI indicates you have more disposable income to cover a new car payment, making you a more attractive borrower. Aim for a DTI below 40%.

You’ll also need to demonstrate income stability. Lenders prefer to see a consistent employment history, ideally with the same employer for at least six months to a year. This assures them of your ability to make regular payments. Be honest and transparent on your application, as any discrepancies can lead to denial.

After Getting Your Car Loan: Building a Better Financial Future

Securing a 580 credit score car loan is not just about getting a car; it’s a significant opportunity to improve your credit standing. This is where the real value lies for your long-term financial health.

Based on my experience, consistently making your car loan payments on time is one of the most effective ways to improve your credit score. Payment history accounts for 35% of your FICO score. Each on-time payment demonstrates responsible borrowing behavior to credit bureaus.

As your credit score improves over time, you may even have the option to refinance your car loan for a lower interest rate. This could save you hundreds or even thousands of dollars over the remaining loan term. Typically, you’ll want to wait 6-12 months of consistent payments before exploring refinancing options.

Common Mistakes to Avoid When Getting a 580 Credit Score Car Loan

Navigating the world of car financing with low credit can be tricky. Avoiding these common pitfalls will save you stress and money in the long run.

Firstly, not checking your credit report before applying is a major mistake. You need to know exactly where you stand and correct any errors. This sets the foundation for your loan application.

Secondly, not getting pre-approved leaves you vulnerable at the dealership. You lose bargaining power and might feel pressured into accepting less favorable terms. Always secure financing before choosing a car.

Another common error is focusing only on the monthly payment instead of the total cost of the loan. A low monthly payment over a very long term often means paying significantly more in interest. Always consider the total amount you’ll pay back.

Buying more car than you can afford is a recipe for financial trouble. Stick to your budget, even if it means choosing a less flashy vehicle. The goal is reliable transportation and credit improvement, not instant gratification.

Finally, ignoring the total cost of ownership beyond the loan payment is a critical oversight. Factor in insurance, maintenance, fuel, and registration fees into your budget. Overlooking these can lead to unexpected financial strain.

Pro Tips for Navigating the 580 Credit Score Car Loan Landscape

Success with a 580 credit score car loan requires patience, diligence, and smart decision-making. Here are some pro tips from our team to guide you:

- Be Patient and Persistent: It might take a bit longer to find the right loan and vehicle. Don’t rush the process or settle for the first offer you receive. Persistence will pay off.

- Do Your Research: Thoroughly research lenders, vehicles, and their reliability. Knowledge is your best weapon against unfavorable terms. Check out trusted external sources like the Consumer Financial Protection Bureau for general advice on auto loans.

- Read the Fine Print: Always read every line of your loan agreement before signing. Understand all fees, interest rates, and repayment terms. If something isn’t clear, ask for clarification.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, or if the terms are too aggressive, be prepared to walk away. There are always other options available.

- Consider a Smaller Loan Amount: Even if you’re approved for a certain amount, consider borrowing less. This reduces your monthly payments and overall interest, making the loan more manageable. For more tips on budgeting for a vehicle, you might find our article on helpful.

- Explore All Options: Don’t limit yourself to just one type of lender. Look into credit unions, online lenders, and even local banks. The more offers you compare, the better chance you have of finding a competitive rate.

- Understand Your Credit Report: Knowing what’s on your credit report and how it impacts your score is crucial. For an in-depth guide on improving your credit score, consider reading our article on .

Conclusion

Securing a 580 credit score car loan is a challenging but entirely achievable goal. By understanding what your credit score means, implementing smart financial strategies, and diligently researching your lending options, you can successfully navigate the process. Remember, this journey is not just about getting a car; it’s about making a responsible financial decision that can pave the way for a stronger credit future.

With a significant down payment, a reliable co-signer, or a commitment to improving your credit score, you significantly enhance your chances of approval. Always prioritize getting pre-approved, setting a realistic budget, and understanding the full cost of your loan. The road to car ownership with a 580 credit score is open, and with the right approach, you’ll be driving towards a brighter financial horizon. Start planning today, and make your car ownership dreams a reality.