Mastering Your Azura Car Loan Payment: The Ultimate Guide to Financial Confidence

Mastering Your Azura Car Loan Payment: The Ultimate Guide to Financial Confidence Carloan.Guidemechanic.com

Securing a car loan is often a pivotal step towards owning the vehicle of your dreams. For many, Azura provides that crucial bridge, offering financing solutions that make car ownership accessible. However, the journey doesn’t end when you drive off the lot; it begins with effectively managing your Azura car loan payment. This comprehensive guide is designed to empower you with all the knowledge you need to navigate your Azura auto loan with confidence, ensuring financial stability and peace of mind.

Understanding your loan agreement, knowing your payment options, and planning for the future are essential for a stress-free car ownership experience. We’ll delve deep into every aspect of managing your Azura car loan, from making your monthly payment to exploring early payoff strategies and understanding what happens if you hit a bump in the road. Our goal is to make this complex topic simple, clear, and actionable, transforming you into an expert on your own Azura financing.

Mastering Your Azura Car Loan Payment: The Ultimate Guide to Financial Confidence

Unpacking Your Azura Car Loan Agreement: The Foundation of Understanding

Before you make your first Azura car loan payment, it’s paramount to fully understand the agreement you signed. This document isn’t just a formality; it’s the blueprint of your financial commitment. Taking the time to review it thoroughly can prevent misunderstandings and help you plan your finances effectively.

Based on my experience in consumer finance, many people skim through their loan documents, only focusing on the monthly payment amount. This is a common mistake that can lead to unexpected fees or missed opportunities later on. Your loan agreement contains vital information that dictates how your loan operates and how you can best manage it.

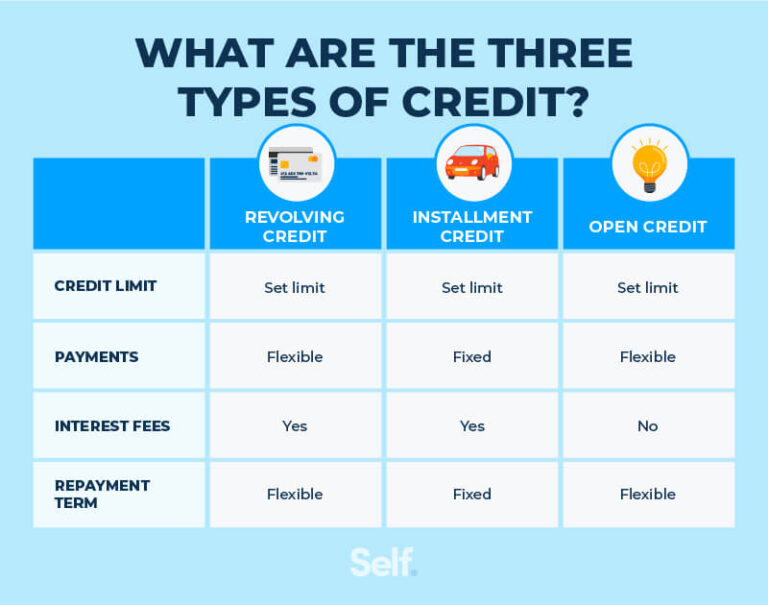

Key Terms You Must Understand

Your Azura car loan agreement is filled with important terms that directly impact your financial obligation. Familiarizing yourself with these ensures you have a complete picture of your loan.

- Annual Percentage Rate (APR): This is more than just your interest rate; it represents the total cost of borrowing, expressed as a yearly percentage. It includes your interest rate plus any fees or additional costs associated with the loan. A lower APR means less money paid over the life of the loan.

- Loan Term: This refers to the duration of your loan, typically expressed in months (e.g., 60 months, 72 months). A longer loan term usually results in lower monthly payments but often means you’ll pay more interest overall. Conversely, a shorter term has higher monthly payments but less total interest.

- Principal Balance: This is the original amount of money you borrowed from Azura to purchase your car, minus any payments you’ve already made that were applied directly to the principal. Every payment you make chipping away at this balance reduces the amount on which interest is calculated.

- Interest: This is the cost of borrowing money. It’s calculated based on your principal balance and your APR. Understanding how interest accrues is key to making informed payment decisions, especially if you consider early payoff strategies.

Locating Your Azura Car Loan Payment Details

Your monthly statement and your online Azura account portal are your primary sources for up-to-date payment information. These resources will clearly show your due date, the minimum payment amount, and your current principal balance.

It’s also where you can often find details about any late fees incurred or additional payments made. Always cross-reference these details with your own records to ensure accuracy. Should anything seem amiss, contacting Azura directly is the best course of action.

Convenient Ways to Make Your Azura Car Loan Payment

Azura understands that convenience is key when it comes to managing your finances. They typically offer a variety of payment methods designed to suit different preferences and ensure you can make your Azura car loan payment on time, every time. Exploring these options will help you choose the most efficient method for your lifestyle.

Choosing the right payment method can save you time, avoid late fees, and provide peace of mind. Each option has its own set of advantages and considerations, so it’s wise to evaluate them based on your personal financial habits.

1. Online Payment Portal: Speed and Control

The Azura online payment portal is arguably the most popular and efficient way to manage your car loan. It offers a secure and user-friendly interface where you can view your loan details, payment history, and make one-time or recurring payments.

To get started, you’ll typically need to register an account using your loan number and personal information. Once set up, you can link your bank account (checking or savings) directly to the portal. This allows for quick electronic transfers, often processed within one to two business days.

Pro tips from us: Setting up automatic payments through the online portal is a game-changer for consistency. You can schedule your Azura car loan payment to be debited automatically on your due date, eliminating the risk of forgetting. This feature ensures you never miss a payment, protecting your credit score and avoiding late fees.

2. Automatic Payments (ACH): Set It and Forget It

Similar to setting up recurring payments online, Automatic Clearing House (ACH) payments allow Azura to automatically withdraw your payment directly from your bank account on your scheduled due date. This method is incredibly reliable and ideal for those who prefer minimal manual intervention.

To enroll in ACH payments, you usually need to provide Azura with your bank account and routing number. You’ll typically receive confirmation of enrollment and details about the withdrawal schedule. This system is designed for maximum convenience and reliability.

While highly convenient, always ensure you have sufficient funds in your account on the scheduled withdrawal date to avoid overdraft fees from your bank. Common mistakes to avoid are not monitoring your bank balance or assuming Azura will notify you if funds are low; it’s your responsibility to maintain adequate funds.

3. Phone Payments: Direct and Personal

If you prefer speaking to a representative or need to make a payment quickly, Azura’s customer service line often facilitates phone payments. This method can be particularly useful if you have questions about your balance or need to discuss specific payment arrangements.

Be aware that some lenders might charge a small processing fee for phone payments made with a representative. Always inquire about any potential fees before proceeding. Have your loan number and payment information (bank account or debit card details) ready to expedite the process.

4. Mail Payments: Traditional and Reliable

For those who prefer a more traditional approach, sending your Azura car loan payment via mail is usually an option. This typically involves sending a check or money order to Azura’s designated payment processing center.

Ensure you allow ample time for your payment to be processed and received before your due date, factoring in mail delivery times. Always include your Azura loan number on your check or money order to ensure it’s correctly applied to your account. Sending certified mail can provide proof of mailing if you’re concerned about delivery.

5. In-Person Payments: When Available

While Azura primarily operates online and by phone, some lenders partner with third-party payment centers or have physical branches where you can make payments in person. This option offers immediate payment confirmation and can be useful if you prefer cash payments or require immediate assistance.

Always check Azura’s official website or contact their customer service to confirm if in-person payment options are available in your area and what methods they accept. Not all lenders offer this, so it’s essential to verify.

Mastering Your Azura Car Loan Payment: Effective Management Strategies

Making your Azura car loan payment on time is the baseline; truly mastering it involves strategic planning and proactive engagement. Effective management can lead to significant savings, a better credit score, and overall financial peace.

Based on my years of helping individuals manage their debt, consistency and foresight are your best allies. Don’t wait for issues to arise; implement strategies that keep you ahead of the curve.

Setting Up Payment Reminders

Even with automatic payments, it’s wise to have multiple layers of reminders. Technology offers numerous tools to help you stay on track.

- Calendar Alerts: Set up recurring events in your digital calendar (Google Calendar, Outlook Calendar) a few days before your Azura car loan payment is due. This gives you a buffer to ensure funds are available or to make a manual payment if needed.

- Banking App Notifications: Many banking apps allow you to set up alerts for upcoming bill payments or low balance warnings. This can be invaluable, especially if you rely on direct deposit schedules.

- Third-Party Reminder Apps: Utilize budgeting apps that specifically offer bill reminders. These can integrate with all your financial accounts, providing a holistic view of your upcoming obligations.

Budgeting for Your Azura Car Loan Payment

Integrating your Azura car loan payment into your monthly budget is non-negotiable for financial stability. This isn’t just about allocating funds; it’s about understanding your overall cash flow.

- Create a Detailed Monthly Budget: List all your income sources and fixed expenses (rent, utilities, insurance, loan payments) first. Then, allocate funds for variable expenses like groceries, fuel, and entertainment. Ensure your car loan payment is a priority in this allocation.

- Emergency Fund: Pro tips from us: Always maintain an emergency fund covering at least 3-6 months of essential expenses, including your car payment. This safety net can be a lifesaver if you face unexpected job loss or medical emergencies, preventing you from missing payments.

- Track Your Spending: Regularly review your spending habits to identify areas where you can cut back, potentially freeing up extra money for your car loan or savings. Tools like budgeting apps or even a simple spreadsheet can make this process straightforward.

Understanding Due Dates and Grace Periods

Every Azura car loan payment has a specific due date. Missing this date can trigger late fees and negatively impact your credit score.

- Grace Period: Many lenders offer a grace period, typically a few days after the official due date, during which you can still make a payment without incurring a late fee. However, interest continues to accrue during this period. It’s crucial to know if Azura offers a grace period and to understand its exact duration.

- Don’t Rely on Grace Periods: While grace periods offer a safety net, they should not be relied upon as your regular payment window. Always aim to pay on or before your official due date. Consistently paying during the grace period can still reflect poorly on internal lender records, even if no late fee is charged.

Proactive Communication with Azura

If you anticipate difficulties making your Azura car loan payment, the single most important action you can take is to contact Azura before the due date.

- Early Contact is Key: Don’t wait until you’ve missed a payment. Explain your situation to Azura’s customer service department. They may be able to offer solutions such as payment deferral, a temporary forbearance, or even a modified payment plan.

- Document Everything: Keep a record of all communications, including dates, names of representatives, and any agreements made. This documentation can be invaluable if any disputes arise later.

What Happens If You Miss an Azura Car Loan Payment?

Life happens, and sometimes, despite our best efforts, a payment might be missed. Understanding the repercussions of a missed Azura car loan payment is crucial for mitigating potential damage and taking corrective action swiftly.

Common mistakes to avoid are ignoring the situation or hoping it will resolve itself. Azura, like any lender, has a process for dealing with missed payments, and being proactive is always in your best interest.

Late Fees and Their Impact

The immediate consequence of a missed payment is usually a late fee. The amount of this fee will be clearly outlined in your loan agreement.

- Fee Structure: Late fees can be a flat amount or a percentage of your overdue payment. These fees add to your outstanding balance, increasing the total cost of your loan.

- Accruing Interest: Even if a grace period is available, interest continues to accrue on your principal balance. A late payment means that more of your next payment might go towards interest rather than reducing your principal.

Impact on Your Credit Score

This is perhaps the most significant long-term consequence. Payment history is the largest factor in calculating your credit score.

- Reporting to Credit Bureaus: If your Azura car loan payment is 30 days or more past due, Azura will likely report this delinquency to the major credit bureaus (Equifax, Experian, TransUnion). A single 30-day late payment can cause a significant drop in your credit score, making it harder to secure future loans or favorable interest rates.

- Long-Term Effects: Negative marks on your credit report can remain for up to seven years, affecting your ability to get mortgages, credit cards, or even certain jobs. Maintaining a perfect payment history is vital for a strong financial future.

Communication from Azura

Expect to hear from Azura promptly if you miss a payment. They will likely send reminders via email, phone calls, or mail.

- Purpose of Communication: These communications serve as a reminder and an opportunity for Azura to understand your situation. They might offer solutions or reiterate the consequences of continued non-payment.

- Don’t Ignore It: Engage with Azura. Ignoring their calls or letters can escalate the situation and limit your options for resolution.

Repossession Risk

For secured loans like car loans, repossession is the ultimate consequence of prolonged non-payment.

- When It Becomes a Concern: While Azura won’t immediately repossess your car after one late payment, consistent delinquency (typically 60-90+ days past due) puts you at risk. The specific terms for repossession are detailed in your loan agreement.

- Legal Action: In some cases, Azura may also pursue legal action to recover the debt. This can lead to additional fees and further damage to your credit.

Potential Solutions for Missed Payments

If you anticipate or have already missed an Azura car loan payment, reach out immediately to discuss possible solutions.

- Payment Deferment or Forbearance: Azura might allow you to temporarily postpone or reduce your payments. Interest usually continues to accrue during this period, and the deferred payments are often added to the end of your loan term.

- Loan Modification: In some cases, Azura might agree to modify the terms of your loan, such as extending the loan term to lower your monthly payments. This can be a significant help in difficult financial times.

- Refinancing: If your credit score is still strong, or if market rates have improved, refinancing your Azura car loan with another lender might offer a more affordable payment. We’ll explore refinancing in more detail below.

Strategies for Early Azura Car Loan Payoff

Paying off your Azura car loan ahead of schedule can save you a substantial amount in interest and free up significant cash flow in your budget. This strategy requires discipline but offers considerable financial rewards.

Based on my experience, proactively tackling debt, especially higher-interest loans, is one of the smartest financial moves you can make. The sooner you eliminate debt, the more flexibility you gain.

Benefits of Early Payoff

- Save on Interest: The most obvious benefit is reducing the total amount of interest paid over the life of the loan. Since interest is calculated on the remaining principal, reducing the principal faster means less interest accrues.

- Financial Freedom: Eliminating a monthly car payment frees up a significant portion of your budget, which can then be allocated to savings, investments, or other financial goals.

- Boost Your Credit Score (Indirectly): While early payoff itself doesn’t directly impact your score as much as consistent payments, reducing your overall debt burden improves your debt-to-income ratio, which is favorable for future credit applications.

Making Extra Payments Towards Principal

One of the simplest and most effective strategies is to make extra payments specifically directed towards your loan’s principal.

- How It Works: When you make an extra payment, explicitly instruct Azura to apply it directly to the principal balance. Otherwise, it might be applied to future interest or fees. Reducing the principal means less interest accrues on the remaining balance from that point forward.

- Methods: You can add a small amount to your regular monthly payment, make an extra payment whenever you have spare cash, or make a larger lump-sum payment (e.g., with a tax refund or work bonus).

Bi-Weekly Payments: A Smart Trick

This strategy involves dividing your monthly Azura car loan payment in half and paying that amount every two weeks.

- The Math: Since there are 52 weeks in a year, you’ll end up making 26 half-payments, which equates to 13 full monthly payments instead of 12. That extra full payment goes directly towards reducing your principal balance each year.

- Savings: Over the life of the loan, this "extra" payment significantly shortens your loan term and reduces the total interest paid, often without feeling like a huge financial strain on a bi-weekly budget.

Refinancing Your Azura Loan

If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, refinancing can be a powerful tool for early payoff.

- Lower Interest Rate: A lower interest rate means more of your payment goes towards principal, accelerating your payoff.

- Shorter Loan Term: You could refinance into a shorter loan term to pay it off faster, though this will likely increase your monthly payment.

Utilizing Windfalls

Any unexpected influx of cash – a work bonus, a tax refund, an inheritance – presents a golden opportunity to make a substantial dent in your Azura car loan.

- Strategic Allocation: Instead of spending a windfall on discretionary items, consider allocating a significant portion (or all) of it to your car loan. This can save you thousands in interest and bring you closer to debt-free car ownership.

Refinancing Your Azura Car Loan: Is It Right for You?

Refinancing your Azura car loan means taking out a new loan, often with a different lender, to pay off your existing Azura loan. This can be a very effective strategy, but it’s not always the best choice for everyone. Understanding the pros and cons is key to making an informed decision.

Pro tips from us: Always shop around for refinancing offers. Don’t just take the first offer you receive; compare rates and terms from multiple lenders to ensure you’re getting the best deal. For more in-depth information, you might find our article, Understanding Auto Loan Refinancing: A Complete Guide, helpful.

When to Consider Refinancing

- Lower Interest Rates: If current auto loan interest rates are significantly lower than when you originated your Azura loan, refinancing could save you a lot of money.

- Improved Credit Score: If your credit score has improved substantially since you took out your original loan, you might qualify for a much better interest rate now.

- Reduced Monthly Payments: If you’re struggling with your current Azura car loan payment, refinancing to a longer term (though not always advisable for total cost) or a lower rate can reduce your monthly burden.

- Change in Financial Situation: A major life event, such as a new job with a higher income, could make you eligible for better loan terms.

- Remove a Co-signer: If you initially needed a co-signer, refinancing could allow you to remove them from the loan once your credit is strong enough.

Benefits of Refinancing

- Lower Interest Rate: This is the most common and compelling reason, leading to significant savings over the life of the loan.

- Lower Monthly Payments: By extending the loan term or securing a lower interest rate, you can reduce your monthly financial outlay, freeing up cash flow.

- Shorter Loan Term: If your financial situation has improved, you might opt for a shorter term, which will increase your monthly payment but drastically reduce the total interest paid and get you debt-free faster.

Drawbacks and Considerations

- New Fees: Refinancing often comes with new fees, such as origination fees, application fees, or title transfer fees. Factor these into your calculations to see if the savings outweigh the costs.

- Extending Loan Term: While a longer term means lower monthly payments, it also means you’ll pay interest for a longer period, potentially increasing the total cost of the loan. You could also end up "upside down" (owing more than the car is worth) for a longer time.

- Impact on Credit Score: Each loan application generates a hard inquiry on your credit report, which can temporarily ding your score. However, applying to multiple auto lenders within a short window (typically 14-45 days) will usually count as only one inquiry.

Steps to Refinance Your Azura Loan

- Check Your Credit Score: Know where you stand. A good score is key to favorable refinancing terms.

- Gather Loan Information: Have your current Azura loan balance, interest rate, and remaining term readily available.

- Shop Around: Contact several banks, credit unions, and online lenders for quotes.

- Compare Offers: Look beyond just the monthly payment. Compare APRs, total interest paid, and any associated fees.

- Apply for the Best Offer: Complete the application with your chosen lender.

- Finalize the Loan: Once approved, the new lender will pay off your Azura loan, and you’ll begin making payments to the new institution.

Azura Car Loan Payment Customer Support & Resources

Even with a thorough understanding of your loan, there may be times when you need to contact Azura directly. Knowing how to reach their customer support and what resources are available can save you time and frustration.

Effective communication with your lender is a cornerstone of responsible financial management. Don’t hesitate to reach out if you have questions or concerns about your Azura car loan payment.

How to Contact Azura

Azura typically offers several channels for customer support:

- Phone: This is often the quickest way to speak to a representative for urgent issues or detailed inquiries. Look for the customer service number on your monthly statement or Azura’s official website.

- Online Chat: Many lenders now offer live chat support through their website, which can be convenient for quick questions during business hours.

- Email/Secure Messaging: For non-urgent inquiries or to send documents, email or a secure messaging system within your online account portal can be an efficient option.

- Mail: For formal correspondence or to submit specific forms, a physical mailing address will usually be provided on your statements or website.

Common Issues Customer Support Can Help With

Azura’s customer support team is equipped to assist with a wide range of inquiries related to your car loan payment.

- Payment Inquiries: Questions about your balance, payment history, or setting up/modifying payments.

- Troubleshooting Online Account Issues: Assistance with logging in, navigating the portal, or technical glitches.

- Loan Information Requests: Obtaining a payoff quote, requesting statements, or clarifying loan terms.

- Financial Hardship Discussions: Exploring options like deferment or forbearance if you’re struggling to make payments.

- Updating Personal Information: Changing your address, phone number, or bank account details.

Online FAQs and Resources

Before contacting support, check Azura’s website for an FAQ (Frequently Asked Questions) section. Many common questions about Azura car loan payment methods, due dates, and general loan management are often answered there.

Additionally, reputable external sources like the Consumer Financial Protection Bureau (CFPB) offer excellent, unbiased advice on managing auto loans. For instance, their guide on Understanding Vehicle Financing can provide valuable general context.

Frequently Asked Questions About Azura Car Loan Payments

To further solidify your understanding, here are answers to some common questions related to your Azura car loan payment.

Can I change my Azura car loan payment due date?

It depends on Azura’s policies. Some lenders allow a one-time change to your due date, often to align with your pay cycle. You’ll typically need to contact customer service to inquire about this option and understand any implications, such as prorated interest.

How do I get my Azura car loan payoff quote?

You can usually obtain a payoff quote directly from your Azura online account portal or by contacting their customer service department. A payoff quote provides the exact amount you need to pay to completely satisfy your loan on a specific date, including any accrued interest.

What if I overpay my Azura car loan?

If you overpay without specific instructions, Azura will typically apply the excess amount to your principal balance. This is generally a good thing as it reduces the amount on which interest is calculated. However, always confirm with Azura that extra payments are applied to the principal to maximize your savings.

Does Azura offer a grace period for late payments?

Most lenders, including Azura, offer a grace period, typically ranging from 5 to 15 days after your due date, during which you can make a payment without incurring a late fee. However, interest continues to accrue during this time. Always check your specific loan agreement or contact Azura to confirm their grace period policy.

Can I set up multiple payment methods for my Azura loan?

Yes, usually you can. While most people stick to one primary method (like automatic payments), you can often make additional, one-time payments from a different source through the online portal or by phone. This is useful if you want to make an extra principal-only payment from a bonus or tax refund.

Conclusion: Your Path to Azura Car Loan Payment Mastery

Managing your Azura car loan payment doesn’t have to be a source of stress. By understanding your loan agreement, leveraging Azura’s convenient payment options, and implementing smart financial strategies, you can take complete control of your auto financing. Remember, proactive communication, diligent budgeting, and exploring options like early payoff or refinancing are powerful tools at your disposal.

We hope this comprehensive guide has provided you with the insights and confidence needed to navigate your Azura car loan journey successfully. Responsible loan management not only leads to significant financial savings but also builds a strong credit foundation for your future endeavors. Take charge, stay informed, and drive towards financial freedom with confidence.

Do you have any personal experiences with Azura car loan payments you’d like to share, or additional tips that have worked for you? Join the conversation in the comments below!