Mastering Your Car Loan Cal: The Ultimate Guide to Smart Auto Financing

Mastering Your Car Loan Cal: The Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is exciting. The smell of a new car, the thrill of the open road, and the promise of new adventures often overshadow one crucial aspect: understanding your car loan. Many prospective buyers get caught up in the allure of the vehicle itself, neglecting the financial intricacies that dictate the true cost of their dream car. This oversight can lead to unexpected financial burdens and buyer’s remorse down the line.

At its core, "Car Loan Cal" isn’t just about punching numbers into an online tool; it’s about gaining a comprehensive understanding of how your auto loan works, empowering you to make informed decisions, and ultimately saving you money. This isn’t merely a transactional process; it’s a strategic financial move that requires careful consideration and calculation. As an expert in car financing, I’m here to guide you through every facet of car loan calculations, ensuring you’re equipped with the knowledge to secure the best possible deal.

Mastering Your Car Loan Cal: The Ultimate Guide to Smart Auto Financing

Why "Car Loan Cal" Matters: Beyond the Sticker Price

The sticker price on a car is just the beginning of your financial commitment. Without a solid grasp of car loan calculations, you risk overpaying, agreeing to unfavorable terms, or even committing to a vehicle that strains your budget. Understanding the mechanics of your loan is paramount for several reasons:

1. Unveiling the True Cost of Ownership:

A car’s price tag doesn’t reflect the total amount you’ll pay over the loan’s lifetime. Interest, fees, and other charges significantly inflate the final cost. By actively engaging in "Car Loan Cal," you can meticulously dissect these components and understand the complete financial picture. This transparency is vital for sustainable car ownership.

2. Empowering Your Negotiation Stance:

Knowledge is power, especially when negotiating with dealerships or lenders. When you walk in with a clear understanding of your budget, desired monthly payment, and the impact of different loan terms, you’re better positioned to negotiate effectively. You won’t be swayed by high-pressure sales tactics designed to focus only on the monthly payment.

3. Avoiding Unpleasant Financial Surprises:

No one wants to discover hidden fees or realize their monthly payments are unsustainable after the deal is done. Thorough calculations beforehand help you anticipate all costs, plan your budget accurately, and avoid any post-purchase financial shocks. This proactive approach ensures a smoother and more confident buying experience.

The Core Components of Your Car Loan Calculation

To truly master your "Car Loan Cal," you need to understand the fundamental elements that determine your monthly payment and the total cost of your loan. Each variable plays a critical role, and manipulating them can significantly alter your financial outcome.

The Principal Loan Amount: What You Borrow

This is the actual amount of money you are borrowing from the lender to purchase the vehicle. It’s not necessarily the car’s sticker price. Instead, it’s the agreed-upon price of the car minus any down payment, trade-in value, or rebates you might have. For instance, if a car costs $30,000 and you put down a $5,000 down payment, your principal loan amount would be $25,000.

Understanding your principal is the starting point for all other calculations. A lower principal means less money to accrue interest on, leading to lower monthly payments and a reduced total cost over the loan’s duration. It’s crucial to know exactly what amount you are financing.

The Interest Rate (APR): The Cost of Borrowing

Your interest rate, often expressed as an Annual Percentage Rate (APR), is the fee the lender charges you for borrowing their money. It’s a percentage of the principal loan amount that you’ll pay back in addition to the principal itself. This rate is a significant determinant of your total loan cost.

A higher interest rate means you’ll pay more over the life of the loan, even if your principal amount remains the same. Factors like your credit score, the loan term, current market rates, and even the type of vehicle (new vs. used) can influence the APR you’re offered. Securing the lowest possible interest rate should always be a primary goal.

The Loan Term: How Long You Pay

The loan term refers to the duration over which you agree to repay your car loan. This is typically expressed in months, such as 36, 48, 60, 72, or even 84 months. The loan term directly impacts both your monthly payment and the total amount of interest you’ll pay.

A shorter loan term generally results in higher monthly payments but significantly less interest paid over the life of the loan. Conversely, a longer loan term will lower your monthly payments, making the car seem more affordable upfront, but it will lead to substantially more interest accruing over time, increasing the total cost of the vehicle. This is a crucial balancing act to consider in your "Car Loan Cal."

The Down Payment: Your Upfront Investment

A down payment is an initial sum of money you pay towards the purchase of a car, reducing the amount you need to borrow. This upfront cash contribution directly lowers your principal loan amount, which in turn reduces your monthly payments and the total interest you’ll pay over the loan’s term.

Making a substantial down payment is one of the smartest financial moves you can make when buying a car. Not only does it decrease your borrowing costs, but it also provides instant equity in the vehicle, protecting you against becoming "upside down" (owing more than the car is worth) early in the loan term. Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment if possible.

Trade-in Value: Leveraging Your Old Vehicle

If you’re replacing an existing car, its trade-in value can act similarly to a down payment. The dealership assesses the value of your old vehicle, and that amount is then deducted from the purchase price of your new car, reducing the principal loan amount you need to finance.

Always research your car’s trade-in value beforehand using reputable sources like Kelley Blue Book (KBB.com) or Edmunds. This preparation ensures you get a fair offer and prevents you from leaving money on the table. A good trade-in can significantly sweeten your deal.

Additional Costs: Taxes, Fees, and Warranties

Beyond the principal and interest, several other expenses contribute to the total cost of your car loan. These can include sales tax, registration fees, documentation fees, and optional add-ons like extended warranties or GAP insurance. While some are mandatory, others are negotiable or elective.

It’s vital to factor these into your overall "Car Loan Cal" to avoid underestimating your total financial commitment. Always ask for a detailed breakdown of all fees before signing any agreement. Understanding these additional costs helps you see the full picture.

How to Use a Car Loan Calculator Effectively

A car loan calculator is your best friend in this process. It’s a powerful tool that allows you to plug in different variables and instantly see the impact on your monthly payment and total loan cost.

1. Step-by-Step Guide to Calculation:

Most online calculators are user-friendly. You’ll typically input the principal loan amount, the interest rate (APR), and the loan term in months. Some calculators also allow you to include a down payment or trade-in value directly. Once these figures are entered, the calculator will instantly display your estimated monthly payment and often the total interest paid over the loan’s life.

2. Playing with Variables: "What If" Scenarios:

This is where the calculator truly shines. Experiment by changing one variable at a time. What if you increase your down payment by $1,000? How does that affect your monthly payment and total interest? What if you opt for a 60-month term instead of 72 months? This allows you to visualize the trade-offs and find the sweet spot that aligns with your budget and financial goals.

3. Online vs. Manual Calculations:

While online calculators are convenient and quick, understanding the underlying formula can provide deeper insight. The standard formula for a fixed-rate loan payment is:

M = P /

Where:

M = Monthly payment

P = Principal loan amount

i = Monthly interest rate (APR divided by 12)

n = Number of months (loan term)

Knowing this formula helps demystify the process, though a calculator handles the complex math for you.

Pro Tip from us: Don’t rely on just one car loan calculator. Use multiple reputable online calculators from different financial institutions or consumer finance sites. This helps cross-reference results and ensures accuracy, as slight differences in calculation methods can sometimes occur.

Unpacking the Impact of Each Variable

Every component of your car loan has a distinct impact on your financial outlay. Understanding these nuances is key to optimizing your deal.

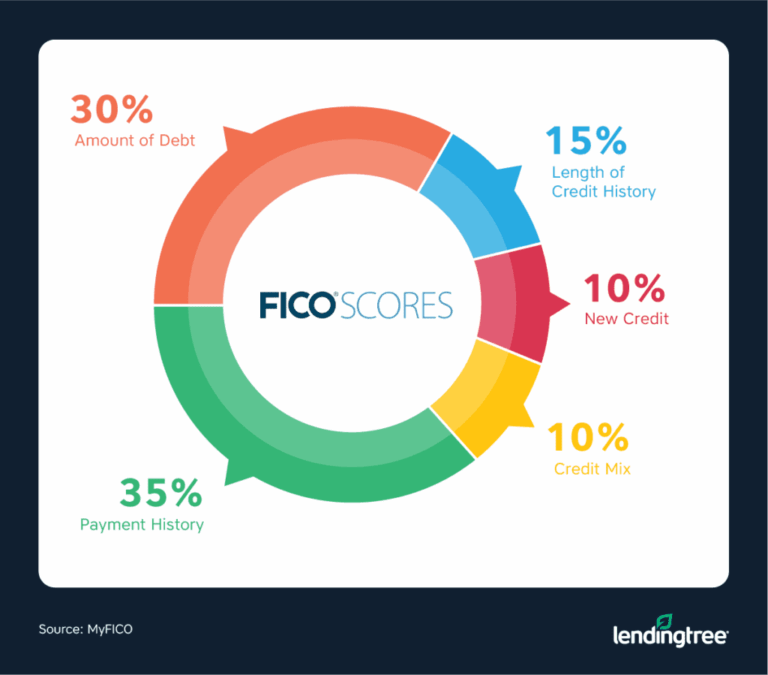

The Interest Rate: How Credit Score Affects It

Your credit score is arguably the most influential factor in determining the interest rate you’ll be offered. Lenders use your credit score to assess your creditworthiness and the likelihood of you repaying the loan. A higher credit score (generally 700+) indicates lower risk, leading to lower interest rates. Conversely, a lower credit score might result in a higher APR, significantly increasing your total loan cost.

Based on my experience, even a difference of one or two percentage points in your APR can translate into hundreds, if not thousands, of dollars in extra interest paid over the life of the loan. It’s always advisable to check and, if necessary, work on improving your credit score before applying for a car loan. Even small improvements can yield significant savings.

The Loan Term: Shorter vs. Longer Terms

The choice between a shorter or longer loan term presents a classic financial dilemma: lower monthly payments now versus lower total cost later.

- Shorter Terms (e.g., 36 or 48 months): These come with higher monthly payments because you’re paying off the principal over a shorter period. However, you pay significantly less interest overall, and you own the car outright much faster. This option is ideal if you can comfortably afford the higher monthly payments.

- Longer Terms (e.g., 72 or 84 months): These offer lower monthly payments, making expensive cars seem more accessible. The downside is that you’ll pay considerably more in interest over the extended duration. You also risk being "upside down" on your loan for a longer period, meaning the car depreciates faster than you pay off the loan balance.

Common mistake to avoid is focusing solely on the monthly payment. While it’s important for budgeting, always consider the total cost of the loan across different terms. A slightly higher monthly payment for a shorter term can save you a substantial amount of money in the long run.

The Down Payment: Reducing Principal, Increasing Equity

The power of a substantial down payment cannot be overstated. By putting more money down upfront, you reduce the principal amount you need to borrow. This directly translates to lower monthly payments and, crucially, less interest accruing over the loan’s term.

Furthermore, a larger down payment gives you immediate equity in the vehicle. Cars start depreciating the moment they leave the lot. A good down payment helps counteract this initial depreciation, reducing the risk of owing more on your car than it’s worth, especially early in the loan. This financial buffer is invaluable.

Beyond the Calculator: Preparing for Your Car Loan

While the "Car Loan Cal" is essential, several preparatory steps can significantly improve your chances of securing favorable terms.

Credit Score Check-up: Importance and Improvement Tips

Before you even start shopping for a car, check your credit score and credit report. You can obtain free copies of your credit report from AnnualCreditReport.com. Review it for any errors or inaccuracies that could negatively impact your score. If your score isn’t where you want it to be, take steps to improve it.

Paying bills on time, reducing outstanding debt, and avoiding new credit applications in the months leading up to your car purchase can all help boost your score. A stronger credit score translates directly into lower interest rates and better loan offers.

Budgeting for a Car: Affordability Analysis

Don’t just think about the car loan payment; consider the entire cost of car ownership. This includes insurance premiums, fuel, maintenance, repairs, and registration fees. Create a detailed budget to determine how much you can truly afford to spend on a car each month, including all these ancillary costs.

Based on my experience, many buyers overlook the "hidden" costs of car ownership, leading to financial strain later. Use a comprehensive budgeting tool or spreadsheet to get a realistic picture of your affordability. You can find excellent resources on personal finance blogs, including our own article on Smart Budgeting for Your Next Car Purchase.

Getting Pre-Approved: A Game-Changer

One of the most powerful strategies for car buyers is to get pre-approved for a loan before stepping foot in a dealership. Pre-approval means a lender (like a bank or credit union) has already reviewed your financial situation and agreed to lend you a specific amount at a certain interest rate, subject to final vehicle selection.

Based on my experience, walking into a dealership with a pre-approval letter in hand gives you immense negotiation power. You become a cash buyer in the dealer’s eyes, and you have a benchmark interest rate to compare against any financing offers they present. If the dealership can beat your pre-approved rate, great! If not, you have a solid offer to fall back on. This simple step can save you hundreds, if not thousands, of dollars.

The Amortization Schedule: Your Loan’s Financial Roadmap

An amortization schedule is a detailed table showing how your loan payments are allocated over time. For each payment, it breaks down how much goes towards paying off the principal and how much goes towards interest.

What It Is and Why It’s Useful

In the early stages of a car loan, a larger portion of your monthly payment goes towards interest. As you progress through the loan term, more of your payment starts to go towards reducing the principal balance. An amortization schedule visually illustrates this shift.

It’s incredibly useful for understanding how your debt is being retired. You can see exactly how much you’ve paid off and how much you still owe at any given point. This transparency empowers you to manage your loan more effectively.

Pro Tip: Use an amortization schedule to plan extra payments. If you make an additional principal payment, you can see how it reduces the remaining principal, shortens your loan term, and saves you significant interest over time.

Common Car Loan Mistakes to Avoid

Even with the best intentions, buyers often fall prey to common pitfalls that can cost them dearly.

1. Ignoring the Total Cost of the Loan:

As mentioned, focusing solely on the monthly payment is a major error. Always ask for the total amount you will pay over the life of the loan, including all interest and fees. This comprehensive figure reveals the true expense.

2. Extending Loan Terms Too Long:

While longer terms offer lower monthly payments, they dramatically increase the total interest paid and keep you in debt longer. They also increase the likelihood of being "upside down" on your loan.

3. Skipping Pre-Approval:

Failing to get pre-approved means you’re negotiating blind. You lose leverage and might accept a higher interest rate than you qualify for, simply because you don’t have an alternative offer.

4. Not Factoring in Insurance and Maintenance:

These are significant ongoing costs that can easily be overlooked. Always get insurance quotes for the specific vehicle you’re considering and research typical maintenance costs before committing.

Advanced Strategies for Smarter Car Loan Management

Once you have your car loan, there are still ways to optimize your finances.

1. Refinancing Options:

If interest rates have dropped, your credit score has improved since you took out the loan, or you’re unhappy with your current loan terms, consider refinancing. Refinancing replaces your existing car loan with a new one, potentially at a lower interest rate or with a different term, which can save you money.

2. Making Extra Payments:

Any extra money you pay towards your principal balance directly reduces the amount of interest you’ll pay over the loan’s life. Even small, consistent extra payments can shorten your loan term and lead to significant savings.

3. Bi-Weekly Payments:

Instead of one monthly payment, some lenders allow you to make half-payments every two weeks. Since there are 26 bi-weekly periods in a year, this effectively results in one extra full monthly payment per year, which can accelerate your loan payoff.

Choosing the Right Lender

The lender you choose for your car loan can significantly impact your rates and terms.

1. Banks, Credit Unions, and Dealership Financing:

- Banks: Offer competitive rates, especially to customers with excellent credit.

- Credit Unions: Often known for offering some of the lowest interest rates and more flexible terms, as they are member-owned.

- Dealership Financing: Convenient, but dealers often mark up interest rates. Always compare their offer to your pre-approval.

2. Comparing Offers:

Always get at least three to four loan offers from different lenders. Compare not just the interest rate, but also any origination fees, prepayment penalties, and the overall loan terms. This comparison shopping is crucial for securing the best possible deal.

For more information on comparing lenders and securing the best rates, check out this valuable resource from the Consumer Financial Protection Bureau on shopping for a car loan.

Conclusion: Your Road to Smart Car Financing

Navigating the world of car loans might seem daunting, but with the right approach to "Car Loan Cal," you can transform a complex process into an empowering financial decision. By understanding the core components of your loan, leveraging calculators effectively, preparing your finances, and avoiding common mistakes, you position yourself for success.

Remember, a car loan is a significant financial commitment. Approaching it with knowledge and strategy ensures you not only drive away in your desired vehicle but do so on terms that align with your financial well-being. Take the time to calculate, compare, and strategize – your wallet will thank you for it. Happy driving!