Mastering Your Car Loan Inquiry: The Ultimate Guide to Driving Away with Confidence

Mastering Your Car Loan Inquiry: The Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

The dream of a new car – the fresh scent of the interior, the smooth hum of the engine, the open road stretching ahead. It’s an exciting prospect, but the path to ownership often feels paved with complex financial decisions, particularly when it comes to securing a car loan. For many, the phrase "car loan inquiry" conjures images of daunting paperwork and confusing terms. However, understanding this process is not just about getting approved; it’s about getting the right approval – one that aligns with your financial health and future goals.

As an expert blogger and professional in the automotive finance space, I’ve seen countless individuals navigate the ups and downs of vehicle financing. This comprehensive guide is designed to demystify the entire car loan inquiry journey, transforming what might seem like a hurdle into a strategic advantage. Our ultimate goal is to equip you with the knowledge and confidence to approach your next car purchase empowered, ensuring you drive away with not just a new car, but also a smart financial decision. Let’s dive deep into becoming a savvy car loan applicant.

Mastering Your Car Loan Inquiry: The Ultimate Guide to Driving Away with Confidence

Understanding the Car Loan Inquiry: More Than Just Asking

A "car loan inquiry" is much more than a simple question; it’s the initial step in formally requesting financing for a vehicle. This process signals to lenders that you are serious about purchasing a car and need their financial assistance to do so. It triggers a review of your financial standing, which lenders use to assess your creditworthiness and determine the terms they are willing to offer.

Being prepared for this inquiry is paramount. Approaching it without prior research or a clear understanding of your financial position can lead to unfavorable loan terms, or even rejection. A well-executed inquiry, however, can unlock competitive interest rates and flexible payment options, saving you thousands over the life of the loan.

Based on my experience, many people mistakenly believe that all inquiries are the same. It’s crucial to understand the difference between a "soft inquiry" and a "hard inquiry." A soft inquiry typically occurs when you check your own credit or when a lender pre-screens you for an offer, and it doesn’t impact your credit score. A hard inquiry, on the other hand, happens when you formally apply for credit, and it can temporarily ding your score. We’ll delve deeper into this distinction later, but for now, remember that preparation minimizes unnecessary hard inquiries.

The Foundation: Your Financial Readiness

Before you even glance at a car dealership or fill out an online form, your first stop should be a thorough assessment of your financial readiness. This foundational step is critical for securing the best possible car loan. It’s about presenting yourself as a low-risk borrower, which directly translates to better rates and terms.

1. Know Your Credit Score Inside and Out

Your credit score is arguably the most significant factor lenders consider when evaluating your car loan inquiry. It’s a three-digit number that represents your creditworthiness, essentially a report card of your financial behavior. A higher score indicates a lower risk to lenders, leading to more attractive interest rates and loan terms.

Why it matters: A difference of even a few points in your credit score can translate into hundreds or thousands of dollars saved on interest over the life of your loan. Lenders use various scoring models, but generally, scores above 700 are considered good, while those above 780 are excellent. Don’t leave this to chance; proactively know where you stand.

How to check it: You are entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months through AnnualCreditReport.com. Reviewing these reports is essential not only for knowing your score but also for identifying any errors that could be negatively impacting it. Dispute any inaccuracies immediately, as correcting them can boost your score.

Pro tips from us: If your credit score isn’t where you want it to be, take steps to improve it before making a car loan inquiry. Pay down existing debts, especially credit card balances, and ensure all your payments are made on time. Even a few months of diligent financial habits can make a noticeable difference. For more in-depth strategies, you might find our article on particularly helpful.

2. Assess Your Debt-to-Income (DTI) Ratio

While your credit score shows your past payment behavior, your Debt-to-Income (DTI) ratio reveals your current capacity to take on new debt. This ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to gauge whether you can comfortably afford the additional monthly car payment without becoming overextended.

What it is and why lenders care: A low DTI ratio signals to lenders that you have sufficient disposable income to handle your existing obligations plus a new car payment. A high DTI, conversely, suggests you might struggle, making you a higher risk. Lenders typically prefer a DTI ratio of 36% or lower, though some may go higher depending on other factors.

How to calculate it: Sum up all your recurring monthly debt payments (mortgage/rent, credit card minimums, student loan payments, personal loans, etc.). Divide this total by your gross monthly income (your income before taxes and deductions). For example, if your monthly debts total $1,000 and your gross monthly income is $3,000, your DTI is 33%.

Ideal ranges: Aim for a DTI as low as possible. While 36% is often a benchmark, a ratio below 20% or 30% makes you an exceptionally attractive borrower. If your DTI is high, consider paying down some existing debts before applying for a car loan.

3. Budgeting for Your Car Loan: Beyond the Monthly Payment

Many prospective car buyers focus solely on the monthly payment, overlooking other significant costs associated with vehicle ownership. A truly responsible car loan inquiry starts with a holistic budget that accounts for all expenses. This prevents "buyer’s remorse" and ensures your new car remains a joy, not a financial burden.

Beyond the monthly payment: Your budget needs to include more than just the principal and interest payment. Factor in car insurance premiums, which can vary significantly based on the car’s value, your driving record, and your location. Don’t forget maintenance costs, fuel expenses, registration fees, and potential repair funds.

Setting a realistic budget: Use an online car loan calculator to estimate potential monthly payments based on various loan amounts, interest rates, and terms. Then, add in your estimated insurance, fuel, and maintenance costs. Can you comfortably afford this total without straining your other financial obligations? Be honest with yourself.

Common mistakes to avoid are: Overlooking insurance costs, especially for a newer or more expensive vehicle, and underestimating fuel consumption. Also, failing to budget for routine maintenance can lead to unexpected financial hits down the line. A new car might have lower immediate maintenance, but it’s still a factor to consider for long-term ownership.

4. Down Payment Strategy: Your Upfront Investment

A down payment is the initial amount of money you pay towards the purchase of a car. It reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest you’ll pay over the loan’s lifetime. It also shows lenders you have skin in the game, making you a less risky borrower.

Benefits of a larger down payment: A substantial down payment (typically 10-20% for used cars, and 20% or more for new cars) offers several advantages. It can secure a lower interest rate, reduce your loan amount, shorten your loan term, and help you avoid being "upside down" on your loan (owing more than the car is worth).

When a smaller down payment might be acceptable: While a larger down payment is generally advisable, a smaller one might be acceptable if you have an excellent credit score, a low DTI, and are comfortable with potentially higher monthly payments and more interest. Some manufacturers or dealerships offer incentives like 0% down, but always read the fine print to understand the true cost.

Impact on loan terms and interest: Even a modest down payment can significantly impact your loan. It reduces the principal, which directly reduces the interest accrued. For example, on a $30,000 car, a $5,000 down payment means you’re only financing $25,000, saving you interest on that initial $5,000.

The Pre-Approval Power Play: Your Secret Weapon

Once you’ve shored up your financial readiness, the next strategic move is to get pre-approved for a car loan. This step is a game-changer and, based on my experience, one of the most underutilized tools in a car buyer’s arsenal. Pre-approval transforms you from a speculative shopper into a serious buyer.

What is pre-approval? Pre-approval means a lender has reviewed your credit and financial information and tentatively agreed to lend you a specific amount of money at a certain interest rate. This isn’t a final commitment, as it’s contingent on the actual vehicle you choose and final documentation, but it provides a clear framework.

Why it’s invaluable before stepping into a dealership: Walking into a dealership with a pre-approval letter in hand gives you immense leverage. It separates the financing negotiation from the car price negotiation, allowing you to focus on getting the best deal on the vehicle itself. You know your maximum budget and your interest rate before the salesperson even starts their pitch.

Benefits of pre-approval:

- Negotiating Power: You’re negotiating as a cash buyer. Dealers know you have financing secured elsewhere, which can push them to offer a better deal or match your pre-approved rate.

- Clarity on Budget: You know exactly how much you can afford, preventing you from falling in love with a car outside your budget.

- Avoiding Dealership Pressure: You won’t feel pressured to accept the dealership’s financing offer, which may not be the most competitive. You can compare it directly with your pre-approval.

- Faster Process: With financing largely sorted, the car buying process at the dealership becomes much quicker.

The pre-approval process: documentation needed: To get pre-approved, you’ll typically need to provide personal identification, proof of income (pay stubs, tax returns), proof of residence (utility bill), and information about your employment. The lender will perform a hard inquiry on your credit during this process, so ensure you’re ready.

Navigating the Lender Landscape

When it comes to car loan inquiries, you have several avenues for financing. Each type of lender offers distinct advantages and disadvantages. Understanding these differences allows you to choose the best fit for your financial situation and car buying strategy.

1. Traditional Banks & Credit Unions

These are often the first places people consider for a loan, and for good reason. They are established financial institutions with a history of providing various loan products.

Pros and cons:

- Pros: Often offer competitive interest rates, especially to existing customers with good credit. They provide a sense of security and familiarity. Credit unions, in particular, are known for having member-friendly rates and personalized service.

- Cons: Application processes can sometimes be slower than online lenders. You might need to be an existing customer to get the very best rates or to qualify easily.

Relationship banking: If you have an existing banking relationship, start there. They may offer preferred rates or streamlined application processes as a perk for your loyalty. Don’t assume they’ll automatically give you the best deal, but definitely inquire.

Pro tips from us: Check with both national banks and local credit unions. Credit unions are often overlooked but can be a treasure trove for excellent car loan rates, as they are non-profit organizations focused on member benefits.

2. Dealership Financing

Dealerships are often a convenient one-stop shop, offering financing directly through their partnerships with various lenders, including captive finance companies (like Toyota Financial Services or Ford Credit).

Convenience vs. potential higher rates:

- Pros: Extremely convenient; you can often complete the financing paperwork right there when you buy the car. Dealers may also offer special promotional rates (like 0% APR for qualified buyers) through their captive lenders.

- Cons: While convenient, dealership financing isn’t always the most competitive. They may mark up interest rates from their lending partners to earn a profit, often referred to as "dealer markup."

"Dealer markup": Be aware that dealers can increase the interest rate offered by the original lender and keep the difference. This is perfectly legal. Your pre-approval from an external lender becomes a powerful tool here, allowing you to compare and challenge their offer.

Common mistakes to avoid are: Accepting the first financing offer from a dealership without comparing it to external pre-approvals. Always remember that the dealer’s primary goal is to maximize their profit, which includes the financing component.

3. Online Lenders

The digital age has brought forth a plethora of online lenders specializing in auto loans. These platforms offer a streamlined, often quick, application process.

Speed and convenience:

- Pros: Online lenders are known for their speed, allowing you to get quotes and even approval within minutes. They offer the convenience of applying from anywhere, anytime. Many also allow for easy comparison shopping across multiple lenders.

- Cons: While fast, the lack of a face-to-face interaction might be a drawback for some. It’s crucial to ensure the online lender is reputable and secure.

Comparison shopping ease: Websites like LendingTree, Credit Karma, or Bankrate can help you compare offers from multiple online lenders side-by-side, making it easy to find the most competitive rates without impacting your credit score with multiple hard inquiries (as these often start with soft inquiries for initial quotes).

When they are a good option: Online lenders are an excellent choice for individuals who value convenience, want to quickly compare rates, or have unique credit situations that might be better addressed by specialized online platforms. They are also ideal for those who prefer to handle the financing independently before stepping into a dealership.

The Application Process: Documentation and Diligence

Once you’ve chosen your lender and are ready to finalize your car loan inquiry, the application process requires attention to detail and a complete set of documentation. This is where your thorough preparation pays off, ensuring a smooth and efficient approval.

List of essential documents: Lenders will typically require a standard set of documents to verify your identity, income, and residence. Be prepared with:

- Government-issued ID: Driver’s license or passport.

- Proof of income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns (if self-employed).

- Proof of residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle information: If you’ve already chosen a car (VIN, make, model, year).

- Proof of car insurance: You’ll need this before driving off the lot.

Accuracy and honesty in application: Always provide accurate and truthful information on your application. Any discrepancies can lead to delays, rejection, or even legal issues. Lenders have sophisticated methods for verifying information, so honesty is the best policy.

Understanding the fine print: Before signing anything, read the entire loan agreement carefully. Pay close attention to the interest rate (APR), the loan term, any fees (origination fees, prepayment penalties), and the total cost of the loan. Don’t hesitate to ask questions if anything is unclear.

The impact of multiple "hard inquiries" within a short period: As mentioned earlier, a hard inquiry can temporarily lower your credit score by a few points. However, credit scoring models are smart. They understand that when you’re rate shopping for a car loan, you’re likely applying to multiple lenders within a short timeframe. Therefore, multiple hard inquiries for the same type of loan (like an auto loan) within a 14-45 day window (depending on the scoring model) are usually treated as a single inquiry. This is why getting multiple pre-approvals within a short window is advisable; it allows comparison shopping without undue credit score damage.

Based on my experience, many people panic about multiple hard inquiries. The key is to consolidate your rate shopping to a focused period. Don’t apply for a car loan, a credit card, and a personal loan all at once, as those would be treated as separate inquiries.

Decoding Loan Terms and Interest Rates

Understanding the language of car loans is crucial for making an informed decision. The interest rate and loan term are the two most impactful factors on your monthly payment and the total cost of your vehicle.

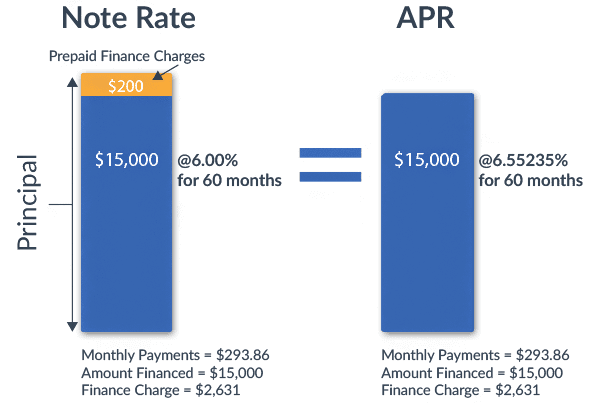

1. APR vs. Interest Rate: Clarifying the Difference

While often used interchangeably, there’s a subtle but important distinction between the interest rate and the Annual Percentage Rate (APR).

Interest Rate: This is the percentage charged by the lender for borrowing the principal amount. It directly affects your monthly payment.

APR (Annual Percentage Rate): The APR is the total cost of borrowing, expressed as an annual percentage. It includes the interest rate plus any additional fees charged by the lender (e.g., origination fees, administrative fees). The APR provides a more accurate representation of the overall cost of the loan. Always compare APRs, not just interest rates, when evaluating loan offers.

2. Loan Term Length: Finding the Right Balance

The loan term is the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This choice significantly impacts your monthly payment and the total amount of interest paid.

Shorter vs. Longer terms:

- Shorter Terms (e.g., 36-48 months): Lead to higher monthly payments but result in less interest paid over the life of the loan. You’ll own the car free and clear sooner.

- Longer Terms (e.g., 72-84 months): Offer lower monthly payments, making the car seem more affordable in the short term. However, you’ll pay significantly more in total interest, and you risk being "upside down" on your loan for a longer period.

Finding the right balance: The ideal loan term balances affordability with total cost. While a longer term can make a car fit into your budget, be mindful of the extra interest and the depreciation of the vehicle. Pro tips from us: Aim for the shortest loan term you can comfortably afford without straining your budget. It’s often better to buy a slightly less expensive car with a shorter term than to stretch into a pricier vehicle with a very long term.

3. Fixed vs. Variable Rates

Most car loans come with fixed interest rates, but it’s good to understand the difference.

Fixed Rates: The interest rate remains the same throughout the entire loan term. Your monthly payment for principal and interest will not change. This provides predictability and stability in your budget. Most auto loans are fixed-rate loans.

Variable Rates: The interest rate can fluctuate over the loan term based on a benchmark index (like the prime rate). This means your monthly payments could go up or down. Variable rates are rare for standard auto loans but can be found in certain niche products or lines of credit. For car loans, fixed rates are almost always preferred due to their stability.

Negotiation Strategies for a Better Deal

Securing a car loan is just one part of the equation; getting the best overall deal on your vehicle purchase requires savvy negotiation. Your pre-approved car loan inquiry is a powerful tool here.

Separating car price from financing: This is a golden rule. Always negotiate the price of the car first, as if you were paying cash. Do not discuss financing until you’ve settled on the vehicle’s purchase price. If you blend the two, dealers can manipulate numbers to make it seem like you’re getting a great deal on one while overpaying on the other.

Using pre-approval as leverage: Once you have a firm price for the car, then you can introduce your pre-approval. This shows the dealer you’re serious and have a competitive financing offer. Ask them to beat or match your pre-approved rate. If they can’t, you simply use your outside financing.

Don’t be afraid to walk away: The most powerful negotiation tactic is your willingness to walk away. If the dealer isn’t meeting your price or financing expectations, be prepared to leave. There are always other dealerships and other cars. This often prompts them to reconsider their offer.

Understanding add-ons and upselling: After agreeing on the car price and financing, you’ll likely be taken to the "F&I" (Finance & Insurance) office. Here, you’ll be offered various add-ons like extended warranties, paint protection, GAP insurance, or anti-theft devices. While some might be worthwhile, many are high-profit items for the dealership.

Common mistakes to avoid are: Feeling pressured into buying add-ons you don’t need or haven’t researched. Politely decline anything you don’t want. If you’re considering an extended warranty, research third-party options which are often more affordable and comprehensive. Remember, these add-ons increase your total loan amount and thus the interest you pay.

Post-Approval and Beyond: What’s Next?

Congratulations, you’ve navigated the car loan inquiry process and secured your financing! But the journey doesn’t end with approval. There are a few final steps and long-term considerations to keep in mind.

Finalizing the paperwork: Carefully review all final documents, ensuring the interest rate, loan term, and total vehicle price match what you agreed upon. Sign only when you are completely satisfied and understand every clause. Get copies of everything for your records.

Setting up payments: Once the loan is finalized, set up your payment method. Many lenders offer automatic payments, which can help you avoid late fees and sometimes even qualify for a small interest rate discount. Mark your payment due date on your calendar.

Refinancing options later: Life circumstances change, and so do interest rates. If your credit score significantly improves after a year or two, or if market interest rates drop, you might be able to refinance your car loan for a lower rate or a different term. This can save you money over the remaining life of the loan. Keep an eye on your credit and market conditions.

Maintaining good financial health: Continue the good financial habits that helped you secure your car loan. Make all payments on time, keep your credit utilization low, and regularly check your credit report for accuracy. This ongoing diligence ensures your financial future remains strong. For more strategies on maintaining excellent financial health, consider reading our post on .

Conclusion: Drive Away with Confidence

Embarking on a car loan inquiry might seem daunting at first, but with the right knowledge and a strategic approach, it becomes a powerful tool for smart financial decision-making. We’ve journeyed through the essentials: from building a strong financial foundation by understanding your credit and DTI, to leveraging the power of pre-approval, navigating diverse lender options, and mastering the application and negotiation phases.

The ultimate goal of this comprehensive guide is to empower you. By taking control of your financial readiness and approaching the car loan inquiry process with diligence and informed decisions, you not only secure the best possible loan terms but also protect your financial well-being. Don’t let the excitement of a new car overshadow the importance of a sound financial plan.

Based on my extensive experience, the most successful car buyers are those who are prepared, patient, and persistent. Armed with the insights from this article, you are now equipped to make your next vehicle purchase a confident and financially astute one. Start your journey today – research, prepare, and drive away knowing you’ve made the smartest possible choice.