Mastering Your Car Loan Journey: A Comprehensive Guide for a Smooth 9 Apr Approval

Mastering Your Car Loan Journey: A Comprehensive Guide for a Smooth 9 Apr Approval Carloan.Guidemechanic.com

Are you eyeing a new set of wheels, perhaps just in time for spring adventures? The thought of a new car is exciting, but securing the right financing can feel like navigating a complex maze. Whether you’re planning to apply for a car loan specifically around April 9th, or simply looking for comprehensive guidance on auto financing in general, this article is your ultimate resource. We’re here to demystify the entire process, ensuring your journey to car ownership is as smooth and successful as possible.

Based on my extensive experience in consumer finance and auto lending, timing and preparation are paramount. Many people rush into car loan applications without understanding the key factors that lenders consider. This often leads to higher interest rates, unfavorable terms, or even outright rejection. Our goal is to equip you with the knowledge and strategies to secure a favorable 9 Apr car loan, or any car loan, with confidence.

Mastering Your Car Loan Journey: A Comprehensive Guide for a Smooth 9 Apr Approval

Understanding the Landscape: What Exactly is a Car Loan?

Before diving into the specifics of securing a 9 Apr car loan, let’s establish a foundational understanding of what a car loan entails. At its core, a car loan is a sum of money borrowed from a financial institution (like a bank, credit union, or online lender) to purchase a vehicle. You agree to repay this amount, plus interest, over a predetermined period.

This agreement forms a legally binding contract between you and the lender. The car itself typically serves as collateral for the loan, meaning if you fail to make payments, the lender has the right to repossess the vehicle. Understanding this basic premise is crucial for any prospective car buyer.

Key Components of Your Car Loan

Every car loan, whether it’s for a new model or a trusty used vehicle, consists of several vital components that directly impact your monthly payments and the total cost of ownership. Familiarizing yourself with these terms will empower you to make informed decisions.

First, there’s the principal, which is the actual amount of money you borrow to buy the car. This is the starting point of your debt. A larger down payment, which we’ll discuss shortly, directly reduces this principal amount.

Next, the interest rate is arguably the most significant factor. This is the percentage charged by the lender for borrowing their money. A lower interest rate means you pay less over the life of the loan, saving you potentially thousands of dollars.

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). While longer terms mean lower monthly payments, they also mean you pay more in interest over time. It’s a delicate balance to strike.

Finally, the Annual Percentage Rate (APR) is the total cost of borrowing money, expressed as a yearly percentage. It includes not just the interest rate but also any additional fees or charges associated with the loan. This is the most accurate figure to compare when evaluating different loan offers.

Preparation is Key: Laying the Groundwork for Your 9 Apr Car Loan Success

Successfully securing a favorable 9 Apr car loan doesn’t happen by chance; it’s the result of thorough preparation. Think of it like training for a marathon: the better prepared you are, the smoother your race will be. This pre-application phase is where you can significantly influence the terms of your loan.

Based on my experience, many applicants overlook these critical steps, only to be disappointed by the offers they receive. Taking the time to get your financial house in order before you even step foot in a dealership or apply online will give you a significant advantage.

The Power of Your Credit Score

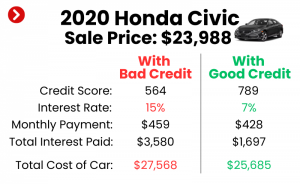

Your credit score is arguably the single most influential factor in determining your car loan interest rate and approval chances. Lenders use it as a snapshot of your financial responsibility and your likelihood of repaying debt. A higher score signals less risk, leading to better terms.

For a prime 9 Apr car loan offer, aiming for a credit score of 700 or higher is ideal. However, even with a lower score, approval is possible, though you might face higher interest rates. It’s crucial to obtain your credit reports from all three major bureaus (Equifax, Experian, Transunion) and review them for errors.

Correcting any inaccuracies can significantly boost your score. Additionally, focusing on paying bills on time, reducing existing debt, and avoiding new credit applications in the months leading up to your car loan application can yield positive results. Building a strong credit profile takes time, but even small improvements can make a difference.

Crafting Your Budget: What Can You Truly Afford?

Before falling in love with a specific car, you need a realistic understanding of what you can comfortably afford. This isn’t just about the monthly car payment; it’s about the total cost of car ownership. This includes insurance, fuel, maintenance, and potential parking fees.

Pro tips from us: Use online car loan calculators to estimate potential monthly payments based on different loan amounts, interest rates, and terms. Work backward from a comfortable monthly payment to determine a realistic maximum loan amount. Remember, just because a lender approves you for a certain amount doesn’t mean you should borrow it all. Stick to a budget that aligns with your overall financial health.

A common mistake to avoid is stretching your budget too thin for a car. This can lead to financial stress and make it difficult to save for other important goals. A comfortable car payment is one that doesn’t jeopardize your other financial commitments.

The Strategic Advantage of a Down Payment

Making a down payment is one of the smartest moves you can make when applying for a car loan. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

Lenders also view a substantial down payment (typically 10-20% of the vehicle’s price) favorably. It demonstrates your commitment to the purchase and reduces their risk, often leading to better interest rates. For a competitive 9 Apr car loan, aim for at least 10%.

Even a small down payment can make a difference, especially for used cars where depreciation can be rapid. Without a down payment, you risk owing more than the car is worth almost immediately, a situation known as being "upside down" on your loan.

Maximizing Your Trade-In Value

If you have an existing vehicle, trading it in can act as a de facto down payment, further reducing your loan amount. Research your car’s trade-in value using reputable sources like Kelley Blue Book (KBB.com) or Edmunds.com before heading to the dealership.

Knowing your car’s worth empowers you during negotiations. While dealerships often offer slightly less than private sale value for convenience, having a realistic expectation helps you get a fair deal. Ensure your trade-in is clean and well-maintained to present it in the best possible light.

Navigating the 9 Apr Car Loan Application Process

Once you’ve done your homework and prepared your finances, it’s time to embark on the application journey for your 9 Apr car loan. This phase involves gathering necessary documents, exploring different lending options, and, most importantly, getting pre-approved.

This is where the rubber meets the road, so to speak. Being organized and strategic here can significantly streamline the process and improve your chances of securing the best possible terms. Don’t rush this stage; careful consideration pays off.

Gathering Your Essential Documents

Lenders require specific documentation to verify your identity, income, and financial stability. Having these ready will make the application process much smoother and faster. Missing documents can cause frustrating delays.

Typically, you’ll need:

- Proof of Identity: Driver’s license or other government-issued ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns (for self-employed individuals).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and year.

Having these documents neatly organized and readily accessible will demonstrate your readiness and seriousness to lenders, contributing to a more efficient 9 Apr car loan application.

Where to Apply: Exploring Your Lending Options

You have several avenues when seeking a car loan, and each comes with its own set of advantages and disadvantages. It’s wise to explore multiple options before committing.

- Banks: Traditional banks often offer competitive rates, especially if you have an existing relationship with them. They provide a sense of security and established customer service.

- Credit Unions: These member-owned financial institutions are renowned for offering some of the lowest interest rates due to their non-profit structure. Becoming a member is usually straightforward.

- Online Lenders: Companies like LightStream or Capital One Auto Finance provide a quick and convenient application process, often with competitive rates and flexible terms. They are great for comparing offers quickly.

- Dealership Financing: While convenient, dealerships often mark up interest rates to earn a profit. However, they can sometimes offer special manufacturer incentives or promotions.

Pro tips from us: Always get pre-approved elsewhere before relying solely on dealership financing. This gives you leverage and a benchmark to compare against.

The Game-Changer: Getting Pre-Approved

One of the most powerful steps you can take is getting pre-approved for a car loan before you even visit a dealership. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate.

This is a game-changer for several reasons:

- Budget Clarity: You know exactly how much you can afford, preventing you from overspending.

- Negotiating Power: You walk into the dealership as a cash buyer, shifting the focus from financing to the car’s price.

- Time Savings: It streamlines the purchase process at the dealership.

- Rate Comparison: You can compare the pre-approved rate with any offers from the dealership, ensuring you get the best deal for your 9 Apr car loan.

Remember, pre-approvals typically involve a "soft" credit inquiry, which doesn’t harm your credit score. Once you proceed, a "hard" inquiry will be made. However, multiple hard inquiries for the same type of loan within a short period (usually 14-45 days) are often counted as a single inquiry, minimizing impact.

Crucial Factors Influencing Your 9 Apr Car Loan Approval

Beyond your credit score and down payment, several other elements weigh heavily on a lender’s decision to approve your 9 Apr car loan and the terms they offer. Understanding these can help you fine-tune your application.

Lenders assess risk from multiple angles. The more stable and less risky you appear, the more likely you are to receive favorable terms. This holistic review ensures they are confident in your ability to repay the loan.

Debt-to-Income Ratio (DTI)

Your DTI is a critical metric that lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments.

Lenders typically prefer a DTI of 36% or less, though some may go higher depending on other factors. If your DTI is high, consider paying down existing debts before applying for a 9 Apr car loan. This demonstrates fiscal responsibility and frees up more of your income.

Employment History and Stability

A stable employment history signals a consistent income stream, which is highly desirable to lenders. They want to see that you have a reliable source of funds to make your loan payments.

Ideally, lenders prefer applicants who have been employed at the same job for at least two years. If you’ve recently changed jobs, especially within the same industry and at a higher pay grade, it might not be a significant issue. However, frequent job changes or periods of unemployment can raise red flags.

Residency Stability

Similar to employment, a stable residency history indicates reliability. Lenders prefer applicants who have lived at the same address for a significant period, typically two years or more. Frequent moves can sometimes be perceived as instability.

If you’ve moved recently, be prepared to explain the circumstances. Providing consistent contact information and demonstrating a stable lifestyle in other areas can help mitigate any concerns.

The Vehicle Itself: New vs. Used, Age, and Mileage

The type of vehicle you intend to purchase also plays a role in loan approval and terms.

- New Cars: Generally come with lower interest rates because they hold their value better initially and are less likely to require immediate repairs.

- Used Cars: While often more affordable, they might carry slightly higher interest rates due to higher perceived risk (e.g., potential for mechanical issues, faster depreciation). Lenders often have restrictions on the age and mileage of used cars they will finance.

Common mistakes to avoid are applying for a loan on a very old or high-mileage vehicle, as many lenders will simply refuse to finance it. Always check a lender’s specific vehicle requirements before falling in love with a particular car.

Securing the Best 9 Apr Car Loan Rates: Negotiation and Due Diligence

Once you’ve been pre-approved and are ready to finalize your purchase, the focus shifts to securing the absolute best terms for your 9 Apr car loan. This is where your preparation truly pays off.

Don’t be afraid to negotiate. Every percentage point off your interest rate can save you hundreds, if not thousands, of dollars over the loan’s lifetime. Approach this stage with confidence and a clear understanding of your options.

Negotiation Strategies that Work

Armed with your pre-approval, you have a powerful tool for negotiation.

- Separate the Car Price from the Loan: First, negotiate the best possible purchase price for the car. Do not discuss financing until a final car price is agreed upon.

- Compare Offers: Present your pre-approval to the dealership and see if they can beat it. If they can, great! If not, you have a solid backup.

- Be Prepared to Walk Away: This is your strongest negotiating tactic. If you’re not getting a fair deal, be ready to take your business elsewhere. There are always other cars and other lenders.

Based on my experience, dealerships are often more flexible on financing terms when they know you have an alternative. They want to make the sale, and sometimes matching or beating an external offer is the easiest way to do that.

Understanding the Fine Print

Before signing any documents, meticulously read the entire loan agreement. Do not rush this step. Ensure all terms, including the interest rate, APR, loan term, and total loan amount, match what you agreed upon.

Look out for hidden fees or charges that weren’t discussed. If anything is unclear, ask for clarification. A reputable lender will be transparent and willing to explain every detail.

Beware of Unnecessary Add-Ons

Dealerships often try to sell you various add-ons like extended warranties, GAP insurance (Guaranteed Asset Protection), paint protection, or fabric protection. While some, like GAP insurance, might be beneficial in certain situations, others can be overpriced or unnecessary.

Common mistakes to avoid are allowing these add-ons to be rolled into your car loan without careful consideration. This increases your principal and, consequently, your interest payments. Evaluate each add-on independently. Can you get it cheaper elsewhere? Do you truly need it? Don’t be pressured into buying something you don’t want or need.

After Approval: What Next for Your 9 Apr Car Loan?

Congratulations! You’ve secured your 9 Apr car loan and are ready to drive off the lot. However, the journey isn’t quite over. There are a few final steps to ensure everything is in order and that you stay on track with your new financial commitment.

This post-approval phase is about finalizing details and setting yourself up for successful loan repayment. Neglecting these steps can lead to unnecessary complications down the line.

Finalizing the Loan and Vehicle Registration

Once you sign the loan agreement, the funds are typically disbursed to the dealership. The dealership will then handle the paperwork for transferring ownership of the vehicle to you and initiating the registration process with your state’s Department of Motor Vehicles (DMV) or equivalent agency.

You will receive temporary plates, and your permanent plates and registration will be mailed to you later. Keep all copies of your signed documents in a safe place, including the loan agreement and bill of sale.

Insurance is Non-Negotiable

Before you can legally drive your new car off the lot, you must have adequate car insurance. Most lenders require comprehensive and collision coverage, not just liability, to protect their investment (the car).

Contact your insurance provider in advance to get quotes and arrange coverage for your new vehicle. Having your insurance policy in place before you pick up the car will prevent any delays.

Making Your Payments On Time

The most crucial step after securing your 9 Apr car loan is to consistently make your payments on time. This is paramount for maintaining a good credit score and avoiding late fees.

Set up automatic payments from your bank account to avoid missing deadlines. If you anticipate financial difficulties, contact your lender immediately. They may be able to offer solutions or payment adjustments to help you through a tough spot. Proactive communication is always better than defaulting on payments.

Refinancing Your Car Loan: A Future Consideration

While you’ve just secured your initial 9 Apr car loan, it’s worth knowing that auto financing isn’t always set in stone. In certain situations, refinancing your car loan down the road can be a smart financial move.

Refinancing means taking out a new loan to pay off your existing car loan, ideally with better terms. This can be particularly beneficial if your financial circumstances have improved since your initial application.

When and Why to Consider Refinancing

You might consider refinancing if:

- Your Credit Score Has Improved: A significantly higher credit score can qualify you for a much lower interest rate.

- Interest Rates Have Dropped: If market rates have fallen since you took out your original loan, you might get a better deal.

- You Need Lower Monthly Payments: You could extend the loan term to reduce your monthly outlay, though this means paying more interest over time.

- You Want to Shorten the Loan Term: If you have more disposable income, you could refinance to a shorter term, pay off the car faster, and save on interest.

It’s always a good idea to periodically check current interest rates and your credit score. If you find a substantial difference, exploring refinancing options could save you a significant amount over the remaining life of your loan. For more detailed information on managing your auto loan, you might find our article on (internal link placeholder) helpful.

Conclusion: Driving Towards Financial Freedom with Your 9 Apr Car Loan

Securing a car loan, whether it’s specifically a 9 Apr car loan or at any other time of the year, doesn’t have to be an intimidating process. By understanding the fundamentals, preparing your finances, knowing your options, and being diligent through the application and negotiation stages, you can confidently drive away with a favorable deal.

Remember, the goal isn’t just to get approved, but to get approved for a loan that aligns with your financial goals and doesn’t become a burden. Take the time to build a strong credit profile, set a realistic budget, and explore all your lending options. Your preparedness will be your greatest asset.

Ready to take the next step in your car buying journey? Start by checking your credit score and researching current interest rates. For reliable credit score information, you can visit a trusted external source like the Consumer Financial Protection Bureau (CFPB) website ConsumerFinance.gov. Your dream car is within reach, and with the right approach, your 9 Apr car loan will be a stepping stone, not a stumbling block, on your path to financial freedom. You might also want to read our guide on (internal link placeholder) for additional insights.