Mastering Your Car Purchase: The Ultimate Guide to the 48 Month Car Loan Calculator

Mastering Your Car Purchase: The Ultimate Guide to the 48 Month Car Loan Calculator Carloan.Guidemechanic.com

Buying a car is one of life’s significant milestones. Whether it’s your very first vehicle, an upgrade for your growing family, or a reliable replacement, the excitement is often matched by the complexities of financing. Understanding how to manage the financial aspect is crucial for a smooth and stress-free purchase.

This is where the 48 Month Car Loan Calculator becomes your indispensable tool. It’s not just a simple online gadget; it’s a powerful financial planner that empowers you to make informed decisions, ensuring your dream car doesn’t turn into a financial burden. In this comprehensive guide, we’ll dive deep into everything you need to know about navigating your car loan, specifically focusing on the popular 48-month term.

Mastering Your Car Purchase: The Ultimate Guide to the 48 Month Car Loan Calculator

Why a 48-Month Car Loan? Understanding the Sweet Spot

When you’re considering a car loan, one of the first decisions you’ll face is the loan term – how long you’ll have to pay back the borrowed money. While options range from 36 months to 84 months (or even longer), a 48-month car loan often strikes a desirable balance for many buyers.

A 48-month term means you’ll be making payments over four years. This duration is generally considered a "sweet spot" in car financing, offering several distinct advantages that make it a popular choice.

The Benefits of a 48-Month Term

Choosing a 48-month term can provide a unique blend of affordability and financial prudence. It’s short enough to save you a substantial amount in interest compared to longer terms, but long enough to keep your monthly payments manageable.

Based on my experience, many buyers find this term length ideal because it allows them to build equity in their vehicle faster. Building equity means that the amount you owe on the car decreases more quickly than its depreciation, reducing the risk of being "upside down" on your loan. Being upside down, or having negative equity, means you owe more on the car than it’s worth.

Furthermore, a 48-month loan typically means you’ll pay significantly less total interest over the life of the loan compared to a 60-month or 72-month term. While the monthly payments might be slightly higher than those longer options, the long-term savings can be substantial, freeing up more of your money down the road.

When is a 48-Month Loan Ideal?

A 48-month loan term is often an excellent choice for individuals who want to minimize the total cost of their car while maintaining a reasonable monthly budget. It’s particularly well-suited for buyers of reliable new or late-model used cars that are expected to hold their value well over the four-year period.

If you have a stable income and a clear financial picture, a 48-month term allows you to pay off your vehicle quickly without the drastic increase in monthly payments often associated with a 36-month loan. It’s a pragmatic choice that aligns well with sound financial planning.

Deconstructing the 48 Month Car Loan Calculator: Your Essential Tool

At its core, a 48 Month Car Loan Calculator is a powerful online tool designed to help you estimate your potential monthly car payments and the total cost of your loan. It takes a few key pieces of information from you and, with a quick calculation, provides a clear financial outlook.

This calculator is more than just a simple arithmetic device; it’s a strategic planning instrument. By inputting different scenarios, you can visualize how various factors impact your monthly obligations and the overall financial commitment.

Key Inputs for the Calculator

To get accurate results from your 48 Month Car Loan Calculator, you’ll need to provide several pieces of information. Each input plays a vital role in determining your estimated payment and total loan cost.

- Vehicle Price (or Amount Borrowed): This is the agreed-upon selling price of the car you’re looking to buy. If you already know how much you plan to borrow after your down payment and trade-in, you can use that figure directly.

- Down Payment: This is the amount of cash you intend to pay upfront towards the vehicle’s purchase. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid.

- Trade-in Value (if applicable): If you’re trading in your current vehicle, its value will also reduce the amount you need to finance. Ensure you get an accurate estimate of your trade-in’s worth before using the calculator.

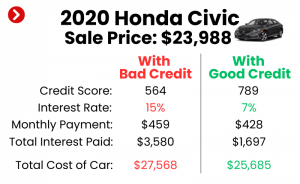

- Interest Rate (APR): This is perhaps the most critical input. The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage. It includes the interest rate plus any additional fees charged by the lender. Your credit score significantly influences the APR you’ll be offered.

- Loan Term (specifically 48 months): For our purposes, this will be set to 48 months. The calculator uses this duration to spread out your payments.

Key Outputs of the Calculator

Once you’ve entered your details, the 48 Month Car Loan Calculator will quickly generate crucial outputs that help you understand your financial commitment. These figures are essential for effective budgeting and decision-making.

- Estimated Monthly Payment: This is the most anticipated output – the amount you’ll need to pay each month for 48 months. It helps you determine if the car fits within your regular budget.

- Total Interest Paid: This figure reveals the entire amount of interest you will pay over the four-year loan term. It’s a critical number often overlooked when buyers only focus on monthly payments.

- Total Cost of the Loan: This output combines the principal amount borrowed with the total interest paid. It gives you the full picture of how much the car will ultimately cost you through financing, beyond its initial sticker price.

How to Effectively Use Your 48 Month Car Loan Calculator

Using a car loan calculator isn’t just about plugging in numbers once. Its real power lies in its ability to facilitate scenario planning. By experimenting with different variables, you can gain a deeper understanding of how each factor influences your overall loan.

Pro tips from us: Start using this tool before you even set foot in a dealership. This proactive approach arms you with knowledge, turning you into a more confident and informed negotiator.

Step-by-Step Guide to Effective Calculation

- Gather Your Information: Before you start, have an estimated car price, your potential down payment amount, and a realistic idea of the interest rate you might qualify for (based on your credit score).

- Input the Initial Scenario: Enter your vehicle price, desired down payment, and an estimated APR. Make sure the loan term is set to 48 months.

- Review the Outputs: Note down the estimated monthly payment, total interest, and total cost of the loan. This is your baseline.

- Perform "What If" Scenarios: This is where the magic happens.

- "What if I increase my down payment?" Try adding a few hundred or a thousand dollars to your down payment. You’ll likely see a noticeable drop in both your monthly payment and the total interest paid.

- "What if I get a lower interest rate?" If you have excellent credit, or are pre-approved, try inputting a lower APR. Even a small percentage point difference can save you hundreds, if not thousands, over 48 months.

- "How does a trade-in affect my payment?" If you have a car to trade, factor its estimated value into your calculations. It acts similarly to a down payment, reducing the amount you need to finance.

Don’t Just Focus on the Monthly Payment

Common mistakes to avoid are getting fixated solely on the monthly payment. While it’s important for budgeting, it doesn’t tell the whole story. A lower monthly payment achieved through a higher interest rate or by adding extra fees can significantly increase the total cost of the loan.

Always look at the "total interest paid" and "total cost of the loan" outputs. These numbers give you the true financial impact of your loan choice. The calculator helps you balance a manageable monthly payment with minimizing your overall expense.

Key Factors Influencing Your 48-Month Car Loan

Securing a favorable 48-month car loan isn’t just about using a calculator; it’s about understanding the underlying factors that lenders consider. Each element plays a crucial role in determining the terms you’re offered.

Being aware of these influences empowers you to improve your position before applying for financing, potentially saving you a significant amount over the loan’s life.

Credit Score: Your Financial Report Card

Your credit score is arguably the most significant factor influencing your car loan’s interest rate. Lenders use it to assess your creditworthiness – essentially, how likely you are to repay your loan on time.

A higher credit score (typically 700+) signals lower risk to lenders, which translates into lower interest rates and better loan terms. Conversely, a lower score indicates higher risk, leading to higher interest rates to compensate the lender for that perceived risk. Pro tips from us: Check your credit score and report well in advance of car shopping. Dispute any errors, and work to improve your score if needed.

Down Payment: Your Upfront Investment

A down payment is the initial cash contribution you make towards the purchase of your vehicle. It directly reduces the amount of money you need to borrow, which has a ripple effect on your loan.

A substantial down payment not only lowers your monthly payments but also decreases the total interest you’ll pay over the 48 months. It also helps you build equity faster and reduces the likelihood of being upside down on your loan. Experts often recommend a down payment of at least 10-20% for new cars, and perhaps more for used cars.

Interest Rate (APR): The Cost of Borrowing

The Annual Percentage Rate (APR) is the actual cost of your loan, expressed as an annual percentage. It’s not just the interest rate; it also includes any lender fees, giving you a more complete picture of your borrowing cost.

Your APR is determined by several factors, including your credit score, the current market rates, the loan term, and the specific lender. Shopping around for the best APR is critical; even a difference of one or two percentage points can save you hundreds or thousands of dollars over a 48-month term.

Loan Term: 48 Months vs. Other Options

While we’re focusing on 48 months, it’s helpful to briefly understand how it compares to other common loan terms. Shorter terms (e.g., 36 months) result in higher monthly payments but significantly less total interest. Longer terms (e.g., 60, 72, or 84 months) offer lower monthly payments but accumulate much more interest over time and increase the risk of negative equity.

The 48-month term is often seen as a sweet spot because it balances manageable monthly payments with a reasonable amount of total interest paid. It helps you pay off the car before major maintenance issues typically arise, and before its value depreciates too heavily.

Vehicle Price & Type: New vs. Used

The actual price of the vehicle directly impacts the amount you need to borrow. A more expensive car naturally leads to a larger loan and higher payments.

Financing a new car versus a used car can also affect your interest rate and available terms. New cars often qualify for lower APRs due to manufacturer incentives and lower perceived risk. Used cars, while generally less expensive upfront, might carry slightly higher interest rates depending on their age and mileage.

Additional Costs: The Hidden Inflators

Beyond the vehicle’s sticker price, remember to account for additional costs that can be rolled into your loan, inflating the total amount borrowed. These include sales tax, registration fees, documentation fees, and optional add-ons like extended warranties or GAP insurance.

While some of these are necessary, carefully consider optional add-ons. Rolling them into your 48-month loan means you’ll pay interest on them, increasing your overall cost. It’s often better to pay for these upfront if possible.

Beyond the Calculator: Securing the Best 48-Month Car Loan

Having a firm grasp of your numbers through the 48 Month Car Loan Calculator is a fantastic start. However, securing the best possible loan terms requires proactive steps that go beyond simple calculations.

These strategies empower you to approach the car buying process with confidence and leverage, ensuring you get a deal that truly benefits your financial health.

Get Pre-Approved: Your Negotiation Superpower

One of the most effective strategies is to get pre-approved for a car loan before you even start serious car shopping. Pre-approval means a lender has reviewed your credit and financial situation and has tentatively agreed to lend you a certain amount at a specific interest rate.

The benefits are immense. You’ll know exactly how much car you can afford, which prevents you from falling in love with a vehicle outside your budget. More importantly, pre-approval gives you a firm interest rate offer, allowing you to negotiate with the dealership on the car price and compare their financing offer against your pre-approval. This puts you in a much stronger negotiating position.

Shop Around for Lenders: Don’t Settle

Never assume the first loan offer you receive is the best one. Just like you’d shop for the best car, you should shop for the best loan. Explore options from various sources:

- Banks: Your current bank might offer competitive rates.

- Credit Unions: Often known for member-friendly rates and terms.

- Online Lenders: Many reputable online platforms specialize in auto loans and can offer quick pre-approvals and competitive rates.

- Dealership Financing: While convenient, dealer financing might not always be the most competitive. Use your pre-approval to ensure their offer is genuinely good.

Comparing multiple offers ensures you’re getting the lowest possible interest rate for your 48-month term.

Negotiate the Car Price, Not Just the Payment

Common mistakes to avoid are letting the dealership focus solely on the monthly payment. While they might try to keep you within a comfortable monthly figure, they could be extending the loan term, increasing the interest rate, or adding costly extras to achieve it.

Always negotiate the total purchase price of the car first, before discussing financing. Once you agree on a fair price, then you can discuss how to finance that specific amount, using your calculator and pre-approval as guides.

Understand the Fine Print: No Surprises

Before signing any loan documents, read them thoroughly. Look for any hidden fees, such as origination fees, administrative charges, or prepayment penalties. A prepayment penalty means you’d be charged extra if you pay off your loan early, which is something to avoid if you plan to make extra payments.

If anything is unclear, ask questions until you fully understand every clause. It’s your right as a borrower to comprehend your financial commitment.

Maintain a Good Credit Score: An Ongoing Effort

Your credit score isn’t just important for getting the loan; maintaining it throughout the loan term is also beneficial. A strong credit history can help you secure better rates on future loans, credit cards, or even insurance.

Continue to make all your payments on time, keep credit card balances low, and regularly check your credit report for accuracy. This ongoing financial discipline will serve you well.

Common Mistakes to Avoid When Financing a Car

Based on my experience in the automotive and finance industries, many car buyers fall into common traps that end up costing them significantly. Being aware of these pitfalls is the first step toward avoiding them and securing a truly advantageous 48-month car loan.

Here are some of the most frequent mistakes to watch out for:

- Not using a calculator before shopping: Going into a dealership without a clear understanding of your budget and potential payments leaves you vulnerable to high-pressure sales tactics. Always do your homework with the 48 Month Car Loan Calculator first.

- Only focusing on the monthly payment: As discussed, this is a dangerous game. A low monthly payment can hide a longer loan term, a higher interest rate, or excessive fees, all of which inflate the total cost of the car.

- Ignoring the total cost of the loan: This is directly related to the point above. Always ask for and compare the total amount you will pay over the life of the loan, including principal and interest.

- Skipping the pre-approval step: Without a pre-approval, you lose significant negotiation power. You won’t know your true borrowing power or the best interest rate you qualify for, making it harder to challenge dealership offers.

- Not shopping around for interest rates: Many buyers accept the first financing offer they get, often from the dealership. This can be a costly mistake. Always compare offers from banks, credit unions, and online lenders.

- Rolling negative equity into a new loan: If you owe more on your current car than it’s worth (negative equity), and you roll that amount into a new 48-month loan, you’re starting off "upside down" on your new vehicle. This can lead to a cycle of debt.

- Buying more car than you can afford: It’s easy to get caught up in the excitement and stretch your budget for a fancier model. Stick to your calculated affordability. Remember to factor in not just the loan payment, but also insurance, fuel, and maintenance.

Building a Budget Around Your 48-Month Car Loan Payment

Your car loan payment is just one piece of the puzzle when it comes to vehicle ownership. To truly manage your finances effectively, you need to integrate that 48-month payment into a comprehensive budget that accounts for all related expenses.

This holistic approach ensures that your car remains an asset, not a source of financial stress.

Integrating the Monthly Payment

Once your 48 Month Car Loan Calculator has given you a realistic monthly payment, allocate this amount in your budget just like any other fixed expense, such as rent or utilities. Ensure it fits comfortably within your disposable income, leaving room for savings and other necessities.

Proactive budgeting for future car needs is also wise. Consider setting aside a small amount each month for future maintenance or even your next down payment, so you’re not caught off guard.

Consider All Related Costs

Don’t forget the other costs of car ownership that aren’t included in your loan payment:

- Car Insurance: This is a mandatory and often significant expense. Get insurance quotes before finalizing your car purchase.

- Fuel: Estimate your monthly fuel costs based on your driving habits and current gas prices.

- Maintenance & Repairs: Even new cars require routine maintenance. Set aside a small emergency fund for unexpected repairs.

- Registration & Licensing Fees: These are annual or biennial costs that need to be budgeted for.

Our article on offers more detailed strategies for managing all these expenses effectively.

Understanding Your Debt-to-Income Ratio

Lenders often look at your debt-to-income (DTI) ratio, which is the percentage of your gross monthly income that goes towards debt payments. A lower DTI ratio (typically below 36%) makes you a more attractive borrower.

When adding a 48-month car loan payment to your existing debts, assess how it impacts your DTI. If it pushes you too high, it might be a sign that you’re overextending yourself.

Amortization and Your 48-Month Loan

Understanding how your 48-month loan is amortized can give you even greater control over your financing. Amortization is the process of paying off a debt over time through regular, equal payments.

In the early stages of your 48-month loan, a larger portion of your monthly payment goes towards interest, and a smaller portion goes towards reducing the principal (the amount you borrowed). As the loan progresses, this ratio gradually shifts, with more of your payment going towards the principal.

Knowing this, you can make informed decisions. For instance, making extra payments, even small ones, early in the loan term can have a significant impact. Because more of your payment initially covers interest, any extra principal payments made early on can dramatically reduce the total interest paid and shorten the overall life of your loan. The 48-month term is a great length for this strategy, as the impact of early extra payments is quite noticeable.

Conclusion

The journey to buying a new car is exciting, but navigating the financial landscape requires preparation and smart tools. The 48 Month Car Loan Calculator is more than just a convenience; it’s your personal financial analyst, empowering you to make decisions that align with your budget and financial goals.

By thoroughly understanding its inputs and outputs, exploring various scenarios, and being aware of the key factors influencing your loan, you can transform a potentially stressful process into a confident and informed purchase. Remember to look beyond just the monthly payment, prioritize the total cost of the loan, and always shop around for the best interest rates.

Armed with this knowledge, you are now well-equipped to take control of your car financing journey. Start calculating today, plan wisely, and drive away with confidence, knowing you’ve secured a smart and sustainable deal.

For general guidance on managing debt and comprehensive financial planning, we highly recommend visiting the Consumer Financial Protection Bureau (CFPB) website, a trusted resource for consumer financial education. You can find valuable information at www.consumerfinance.gov.