Mastering Your Chrysler Car Loan: Your Ultimate Guide to Smart Financing

Mastering Your Chrysler Car Loan: Your Ultimate Guide to Smart Financing Carloan.Guidemechanic.com

The roar of a powerful engine, the elegant lines of a classic sedan, or the robust utility of a modern SUV – a Chrysler isn’t just a car; it’s a statement. For many, owning a Chrysler represents a blend of American heritage, sophisticated design, and reliable performance. But turning that dream into a reality often involves navigating the world of financing. That’s where a well-understood Chrysler car loan becomes your most crucial tool.

Securing the right financing can feel daunting, whether you’re eyeing a brand-new Pacifica, a pre-owned 300, or even exploring the latest electric concepts. This comprehensive guide is designed to demystify the entire process, empowering you with the knowledge and confidence to secure the best possible Chrysler car loan for your unique situation. We’ll delve deep into every aspect, from credit scores to negotiation tactics, ensuring you make an informed decision that drives you forward.

Mastering Your Chrysler Car Loan: Your Ultimate Guide to Smart Financing

The Allure of Chrysler: Why Your Dream Car Needs Smart Financing

Chrysler has a storied history, synonymous with innovation and American automotive excellence. From luxurious sedans to versatile minivans, the brand offers a range of vehicles that appeal to diverse drivers. For many, a Chrysler represents quality, comfort, and a certain level of prestige.

Understanding the value proposition of a Chrysler is the first step. The second, and arguably most important, is understanding how to finance it smartly. A Chrysler car loan is essentially a sum of money borrowed from a lender to purchase your chosen vehicle, which you then repay over a set period with interest. Getting this right means enjoying your Chrysler without financial stress.

Pro Tip from Us: Don’t just fall in love with the car; fall in love with the deal. Early research into financing options can save you thousands over the life of your loan. This proactive approach sets the stage for a smoother, more affordable ownership experience.

Key Factors Influencing Your Chrysler Car Loan Approval & Terms

Securing a favorable Chrysler car loan isn’t solely about finding the right car; it’s heavily dependent on several personal financial factors. Lenders evaluate these elements to assess your creditworthiness and determine the risk associated with lending you money. Understanding these factors is your first step towards empowerment.

Your Credit Score: The Foundation of Your Loan

Your credit score is arguably the most critical number in the car loan application process. It’s a three-digit summary of your financial reliability, based on your payment history, outstanding debts, length of credit history, and types of credit used. Lenders use scores like FICO and VantageScore to gauge your ability to repay borrowed funds.

A higher credit score typically translates into lower interest rates and more favorable loan terms. This is because a strong score signals to lenders that you are a responsible borrower with a history of timely payments. Conversely, a lower score might lead to higher interest rates or even require a larger down payment.

Based on my experience working with countless car buyers, even a seemingly small improvement in your credit score can make a huge difference in the total cost of your loan. Before applying for a Chrysler car loan, it’s wise to check your credit report for any errors and work to improve your score if needed. Paying down existing debts and making all payments on time are excellent starting points.

The Power of a Down Payment

A down payment is the initial sum of money you pay upfront towards the purchase of your Chrysler. It directly reduces the amount you need to borrow, which can significantly impact your monthly payments and the total interest you’ll pay over the life of the loan. A substantial down payment also signals financial stability to lenders.

While there’s no mandatory down payment for every Chrysler car loan, a general recommendation is to put down at least 10% for a used car and 20% for a new one. This not only lowers your principal but also helps to avoid becoming "upside down" on your loan, where you owe more than the car is worth. A larger down payment can also make you eligible for better interest rates, as it reduces the lender’s risk.

Your Debt-to-Income (DTI) Ratio: A Lender’s Perspective

Your Debt-to-Income (DTI) ratio is a crucial metric lenders use to evaluate your capacity to take on new debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. For example, if your monthly debts (rent/mortgage, credit card payments, student loans) total $1,500 and your gross income is $4,500, your DTI is 33%.

Lenders typically prefer a DTI ratio of 36% or lower, though some might go up to 43% depending on other factors. A lower DTI indicates that you have more disposable income available to comfortably manage your new Chrysler car loan payments. If your DTI is on the higher side, consider paying down existing debts or increasing your income before applying.

Understanding Loan Terms: Length Matters

The loan term refers to the duration over which you agree to repay your Chrysler car loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term generally means higher monthly payments but less interest paid overall, as you’re borrowing the money for a shorter period. Conversely, a longer loan term offers lower monthly payments, making the car more "affordable" in the short term.

However, a longer term means you’ll pay significantly more in total interest over the life of the loan. Common mistakes to avoid include focusing solely on the lowest possible monthly payment without considering the total cost. While a 72 or 84-month loan might seem appealing, it often results in paying thousands more in interest and can leave you with negative equity if the car depreciates faster than you pay it off.

The Negotiated Vehicle Price: Your Starting Point

Before you even think about financing, the actual purchase price of your Chrysler is paramount. The lower the price you negotiate for the vehicle, the less money you will need to borrow. This directly impacts your loan amount, which in turn affects your monthly payments and total interest.

Many buyers make the mistake of focusing solely on the monthly payment figure during negotiations. Pro tips from us suggest always negotiating the total "out-the-door" price of the car first, separate from financing discussions. A strong negotiation on the vehicle price lays the groundwork for a more affordable Chrysler car loan from the outset.

Navigating the Chrysler Car Loan Application Process

Once you understand the key factors influencing your loan, the next step is to confidently navigate the application process. This involves strategic preparation, gathering necessary documentation, and choosing the right lender for your needs.

Pre-Approval: Your Secret Weapon for Confidence and Savings

Getting pre-approved for a Chrysler car loan before you even step foot in a dealership is one of the smartest moves you can make. Pre-approval means a lender has conditionally agreed to lend you a specific amount of money at a certain interest rate, based on a review of your credit and financial information. This gives you a clear budget.

The benefits are immense. First, you’ll know exactly how much you can afford, preventing you from falling in love with a car outside your budget. Second, pre-approval gives you significant negotiating power at the dealership; you’re not solely reliant on their financing options. Finally, it streamlines the purchase process, allowing you to focus on the car, not the loan. Most banks, credit unions, and online lenders offer pre-approval services, often with a soft credit inquiry that won’t impact your score.

Gathering Your Essential Documents

A smooth Chrysler car loan application requires having all your ducks in a row. Lenders need to verify your identity, income, and residency. Being prepared with the right paperwork can significantly speed up the approval process.

Common documents you’ll need include:

- Proof of Identity: Driver’s license, passport, or state ID.

- Proof of Income: Recent pay stubs (typically 1-2 months), W-2 forms, tax returns (especially for self-employed individuals).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and mileage.

- Insurance Information: Proof of auto insurance will be required before you can drive off the lot.

Pro Tip: Have both physical and digital copies of these documents ready. This preparedness shows professionalism and makes the application much more efficient.

Where to Secure Your Chrysler Car Loan: Exploring Your Options

When it comes to financing your Chrysler, you have several avenues to explore, each with its own advantages. Comparing these options is crucial for finding the best fit.

-

Chrysler Dealership Financing:

- Pros: Convenience (one-stop shop), access to special manufacturer incentives and promotional rates (often through Chrysler Capital, the captive finance arm), streamlined process. They often work with multiple lenders to find you a deal.

- Cons: May not always offer the absolute lowest rates if you don’t compare, focus might be on monthly payment rather than overall cost.

-

Banks & Credit Unions:

- Pros: Often offer competitive interest rates, especially if you have an existing relationship. Credit unions, in particular, are known for favorable terms as they are member-owned. They provide a more personalized approach.

- Cons: May require an existing account or membership, the application process can sometimes be slower than at a dealership.

-

Online Lenders:

- Pros: Quick application process, easy rate comparison from multiple lenders with a single application, often competitive rates, and great convenience. Many specialize in specific credit profiles.

- Cons: Less personal interaction, requires diligence to research reputable lenders.

For a deeper dive into comparing different lender types and their unique offerings, check out our comprehensive guide on . Understanding the nuances of each can empower your decision-making.

Special Situations & Considerations for Your Chrysler Car Loan

Not every financing journey is straightforward. Life throws curveballs, and sometimes your credit isn’t perfect, or your needs change. Knowing how to approach these special situations can make all the difference in securing your Chrysler car loan.

Bad Credit Chrysler Car Loans: Is It Possible?

Absolutely, it is possible to get a Chrysler car loan even with less-than-perfect credit. While a lower credit score might mean higher interest rates or stricter terms, many lenders specialize in bad credit auto loans. These lenders understand that financial setbacks happen and are willing to work with borrowers to rebuild their credit.

Strategies for securing a bad credit loan include:

- Larger Down Payment: This reduces the lender’s risk and shows your commitment.

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and secure better rates.

- Secured Loan: Some lenders might offer a secured loan where you put up collateral (like another vehicle or savings) to reduce their risk.

- Credit Repair: Taking steps to improve your credit score before applying can yield better results.

From years in the finance world, I’ve seen many individuals overcome credit challenges to secure financing. Patience, persistence, and a willingness to accept initial higher rates as a stepping stone to refinancing later are key. The goal is to get approved, make timely payments, and improve your financial standing over time.

New vs. Used Chrysler Car Loans: What’s the Difference?

The type of Chrysler you choose – new or used – significantly impacts your loan. Lenders view new and used vehicles differently, which affects interest rates and loan terms.

- New Car Loans: Generally come with lower interest rates because new cars are less of a risk for lenders (they hold their value better initially, are less likely to have mechanical issues). Terms can be longer, and manufacturers often offer special low APR promotions.

- Used Car Loans: Typically have slightly higher interest rates due to the perceived higher risk of older vehicles. Loan terms are often shorter, reflecting the vehicle’s remaining lifespan. The advantage, of course, is a lower purchase price and less depreciation.

When deciding between new and used, consider your budget, depreciation rates, and the expected lifespan of the vehicle. A new car offers peace of mind and the latest features, while a used car provides excellent value.

Leasing vs. Buying a Chrysler: Which Path is Right for You?

While this article focuses on car loans, it’s essential to briefly touch upon leasing, as it’s another popular way to acquire a Chrysler. Understanding the distinction is crucial for making the best financial decision.

- Buying (with a loan): You own the vehicle outright once the loan is paid off. You have unlimited mileage, can customize it, and build equity. However, you’re responsible for all maintenance and the full depreciation.

- Leasing: You essentially "rent" the car for a set period (usually 2-4 years) and mileage limit. Monthly payments are typically lower than buying, and you get to drive a new car more frequently. At the end of the lease, you return the car or have the option to buy it. You don’t build equity, and excess mileage or wear can incur fees.

Leasing is often ideal for those who prefer driving new cars every few years and don’t put excessive mileage on their vehicles. Buying is better for those who want long-term ownership, plan to customize, or drive extensively. Explore the full breakdown of leasing vs. buying in our dedicated article: .

Refinancing Your Chrysler Car Loan: Saving Money Down the Road

Even after you’ve secured your initial Chrysler car loan, your financial journey isn’t necessarily over. Refinancing your loan means taking out a new loan to pay off your existing one, often with more favorable terms. This can be a smart move if:

- Interest Rates Have Dropped: Market rates may have decreased since you took out your original loan.

- Your Credit Score Has Improved: If you’ve diligently made payments and improved your credit, you might qualify for a lower rate now.

- You Want Different Terms: You might want to shorten your loan term to pay it off faster or lengthen it to reduce monthly payments (though be mindful of total interest).

Refinancing can save you a significant amount of money over the life of your loan. It’s a straightforward process that involves comparing offers from various lenders, just as you would for an initial loan.

Maximizing Your Chrysler Car Loan Success

Beyond the application itself, there are crucial steps you can take to ensure you get the best deal and manage your Chrysler car loan responsibly. These strategies empower you throughout the entire ownership cycle.

Negotiating Like a Pro: Beyond the Monthly Payment

The dealership finance office can be a place where many buyers lose ground. Remember that your goal is to secure the best overall deal, not just a low monthly payment. Dealers often focus on monthly payments because it can make the car seem more affordable, even if it means a longer loan term or a higher interest rate.

Pro Tips for Negotiation:

- Negotiate the "Out-the-Door" Price First: This is the total price of the car, including taxes, fees, and any add-ons. Agree on this before discussing financing.

- Understand Add-Ons: Be wary of high-pressure sales for extended warranties, paint protection, or other accessories. While some might be valuable, many are highly marked up. Decline anything you don’t genuinely need or can get cheaper elsewhere.

- Compare Your Pre-Approval: Use your pre-approved Chrysler car loan offer as leverage. If the dealership can beat it, great; if not, you have a solid backup.

- Be Prepared to Walk Away: The power of walking away from a deal you’re not comfortable with is immense. There will always be another Chrysler.

Common mistakes to avoid include letting the dealer roll negative equity from your trade-in into a new loan without understanding the full implications, or signing paperwork without a thorough review.

Understanding the Fine Print: APR, Fees, and Penalties

Before you sign any Chrysler car loan agreement, read every single line of the contract. This document is legally binding, and understanding its contents is paramount.

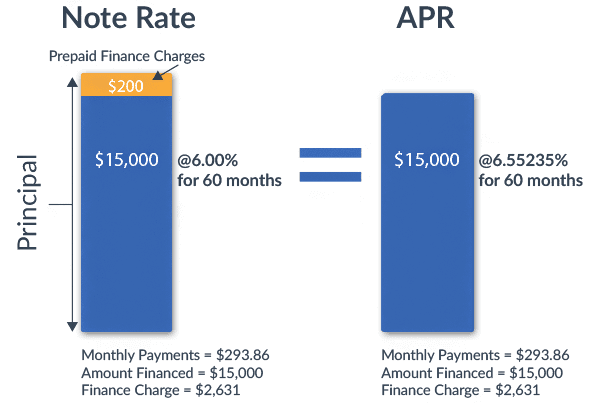

- APR vs. Interest Rate: The Annual Percentage Rate (APR) is the true cost of borrowing, encompassing the interest rate plus any fees associated with the loan. Always compare APRs, not just interest rates, to get an accurate picture of the loan’s cost.

- Hidden Fees: Look for origination fees, documentation fees, or any other charges that might be added to your loan amount. Question anything you don’t understand.

- Prepayment Penalties: Some loans include penalties if you pay off your loan early. While less common now, it’s vital to check for this, especially if you plan to refinance or pay off your Chrysler faster.

For more insights on understanding loan documents and protecting yourself, the Consumer Financial Protection Bureau offers excellent resources: . Knowledge truly is power in these situations.

Post-Approval Best Practices: Managing Your Chrysler Car Loan

Once you’ve driven off the lot in your new Chrysler, your financial responsibility shifts to managing the loan effectively.

- Make Timely Payments: This is the most crucial aspect. Late payments can severely damage your credit score and incur late fees.

- Set Up Auto-Pay: Automating your payments ensures you never miss a due date.

- Monitor Your Credit: Regularly check your credit report to ensure your loan payments are being reported accurately and to catch any potential errors or fraud.

- Consider Extra Payments: If your budget allows, making extra payments (even small ones) can significantly reduce the total interest paid and shorten your loan term.

Your Chrysler Dream, Realized Smartly

Securing a Chrysler car loan doesn’t have to be a stressful ordeal. By understanding the factors that influence your approval, exploring your lending options, and approaching the process with knowledge and confidence, you can drive away in your dream Chrysler with a financing deal that truly serves your financial well-being. This guide has equipped you with the comprehensive insights needed to make informed decisions at every turn.

Remember, a great car is an investment, and a smart loan makes that investment truly rewarding. Take the time to prepare, compare, and negotiate. With this expert advice in hand, you are now well-prepared to navigate the world of Chrysler financing and embark on your journey with peace of mind. Happy driving!