Mastering Your Drive: The Ultimate Guide to the Uccu Car Loan Calculator and Smart Auto Financing

Mastering Your Drive: The Ultimate Guide to the Uccu Car Loan Calculator and Smart Auto Financing Carloan.Guidemechanic.com

The dream of owning a new car, or even a reliable pre-owned vehicle, is a significant milestone for many. It represents freedom, convenience, and often, a new chapter in life. However, the excitement of picking out your perfect ride can quickly turn into anxiety when faced with the complexities of auto financing.

Understanding car loans, interest rates, and monthly payments can feel like navigating a maze without a map. This is where a powerful tool like the Uccu Car Loan Calculator becomes not just helpful, but absolutely indispensable. It’s your personal financial compass, guiding you through the intricacies of car financing.

Mastering Your Drive: The Ultimate Guide to the Uccu Car Loan Calculator and Smart Auto Financing

In this comprehensive guide, we will embark on a deep dive into the Uccu Car Loan Calculator, exploring its features, how to use it effectively, and the critical factors that influence your car loan. Our ultimate goal is to equip you with the knowledge and confidence to make informed decisions, ensuring your car purchase is both exciting and financially sound. Get ready to transform from a hopeful car buyer into a savvy auto financing expert.

What is the Uccu Car Loan Calculator and Why is it Indispensable?

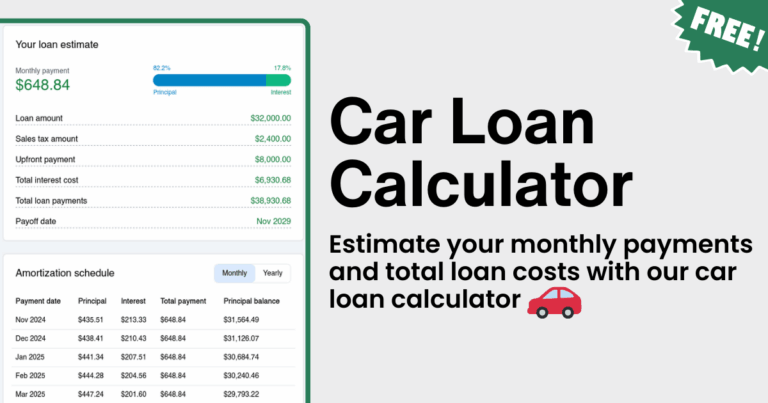

At its core, a car loan calculator is an online tool designed to help you estimate your potential monthly car loan payments. It takes several key pieces of information and, through a series of calculations, provides a clear picture of what your financial commitment will look like. While many financial institutions offer such tools, focusing on a specific one like the Uccu Car Loan Calculator allows us to consider the specific benefits of a credit union.

Based on my experience, many buyers overlook this crucial first step in the car-buying process. They often fall in love with a car before understanding if it truly fits their budget. This backward approach can lead to disappointment or, worse, taking on a loan that stretches their finances too thin.

The Uccu Car Loan Calculator, or any similar robust tool, serves as your financial crystal ball. It empowers you to budget effectively, compare different loan offers with precision, and fully grasp the true cost of borrowing before you even step foot in a dealership. This proactive approach saves you time, stress, and potentially thousands of dollars over the life of your loan. It transforms a vague idea of affordability into concrete, actionable numbers.

Deconstructing the Uccu Car Loan Calculator: Key Inputs You Need

To get the most accurate results from the Uccu Car Loan Calculator, you’ll need to input several pieces of information. Each of these variables plays a significant role in determining your final monthly payment and the total cost of your loan. Understanding them individually is key to manipulating the calculator effectively.

Vehicle Price

This is perhaps the most straightforward input: the selling price of the car you intend to purchase. However, it’s important to remember that this isn’t just the sticker price. Depending on your state, you might also need to factor in sales tax, registration fees, and other dealership charges, which can add hundreds or even thousands to the actual financed amount.

Always consider the "out-the-door" price when possible, or at least have a solid estimate of these additional costs. These seemingly small additions can significantly impact your loan principal. A higher principal means higher monthly payments and more interest paid over time.

Down Payment

Your down payment is the amount of cash you pay upfront toward the purchase of the car. This directly reduces the amount of money you need to borrow, which is a powerful financial move. A larger down payment can lead to a smaller loan, lower monthly payments, and less interest accrued over the loan term.

It also signals financial stability to lenders, potentially qualifying you for better interest rates. Pro tips from us: Aim for at least 10-20% of the vehicle’s price if possible, especially for new cars. This helps mitigate depreciation and can prevent you from being "upside down" on your loan early on.

Trade-in Value (If Applicable)

If you plan to trade in your current vehicle, its value can act much like a down payment. The agreed-upon trade-in amount is subtracted from the purchase price of the new car, further reducing the principal you need to finance. This is a convenient way to lower your loan amount without having to dip deeper into your cash savings.

Ensure you have a realistic estimate of your trade-in’s value before using the calculator. Resources like Kelley Blue Book or Edmunds can provide excellent starting points for valuation. Remember, a dealership’s offer might differ, so use it as a guide.

Interest Rate (APR)

The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage. This is arguably the most critical factor after the principal amount. A lower APR means you pay less in interest over the life of the loan, directly reducing your total cost.

Your credit score, the loan term, and the lender’s specific policies all influence the interest rate you qualify for. Even a difference of one or two percentage points can translate into hundreds or thousands of dollars in savings or additional costs. This is where shopping around for the best rate becomes incredibly valuable.

Loan Term

The loan term is the duration, in months, over which you agree to repay the loan. Common terms range from 36 months (3 years) to 84 months (7 years), or even longer. This choice presents a direct trade-off:

- Shorter Terms (e.g., 36-48 months): Typically result in higher monthly payments but lower overall interest paid. You pay off the loan faster, reducing your exposure to interest rate fluctuations and getting you to a debt-free status sooner.

- Longer Terms (e.g., 60-84 months): Lead to lower monthly payments, making the car seem more affordable upfront. However, you’ll pay significantly more in total interest over the life of the loan. This can also mean your car depreciates faster than you pay off the loan, putting you in a negative equity situation.

Sales Tax & Fees

Don’t forget these "hidden" costs! Sales tax is typically calculated as a percentage of the vehicle’s purchase price and varies by state. There are also various government fees for registration, title, and license plates. Dealerships may also add documentation fees or other administrative charges.

While some of these might be rolled into your loan, others might be due at the time of purchase. Failing to account for them can lead to a budget surprise. Always ask for a full breakdown of all fees involved before finalizing any purchase.

How to Use the Uccu Car Loan Calculator Effectively: A Step-by-Step Guide

Using the Uccu Car Loan Calculator is straightforward, but maximizing its potential requires a strategic approach. It’s not just about plugging in numbers; it’s about understanding what those numbers mean and how different scenarios impact your finances.

Step 1: Gather Your Data

Before you even open the calculator, have your estimated figures ready. This includes the car’s potential price, your desired down payment, and any trade-in value. If you’ve already received pre-approval for a loan, you’ll have an estimated interest rate and a preferred loan term.

Step 2: Input the Figures

Carefully enter each piece of information into the respective fields on the Uccu Car Loan Calculator. Double-check your entries to ensure accuracy. Even a small typo can significantly alter the results.

Step 3: Analyze the Results

The calculator will instantly display your estimated monthly payment and often the total interest you’ll pay over the loan term. Look at both numbers critically. Does the monthly payment fit comfortably within your budget? Is the total interest amount acceptable for the convenience of financing?

Step 4: Experiment with Different Scenarios

This is where the calculator truly shines. Don’t just run one calculation. Pro tips from us: Always run multiple scenarios to understand the full spectrum of possibilities.

- Vary the Down Payment: See how increasing or decreasing your down payment affects your monthly cost and total interest.

- Adjust the Loan Term: Compare a 48-month term against a 60-month or 72-month term. Notice how monthly payments decrease with longer terms, but total interest often climbs significantly.

- Change the Interest Rate: If you’re shopping for rates, input different APRs to understand the impact of even a slight difference. This highlights the importance of good credit and negotiating for the best rate.

By playing with these variables, you gain a clear understanding of the levers you can pull to make a car loan more affordable or efficient. This experimentation phase is crucial for informed decision-making.

Beyond the Calculator: Factors That Influence Your Uccu Car Loan Eligibility & Rates

While the Uccu Car Loan Calculator provides invaluable estimates, actual loan approval and the final interest rate you receive depend on several other critical factors. Lenders, including Uccu, assess your financial profile to determine your creditworthiness.

Your Credit Score

Your credit score is arguably the single most important factor influencing your car loan. This three-digit number summarizes your credit history, indicating to lenders how reliably you’ve managed debt in the past. A higher credit score (typically above 700-720) generally translates to lower interest rates and more favorable loan terms.

Lenders view borrowers with excellent credit as lower risk, making them more willing to offer competitive rates. Conversely, a lower credit score might lead to higher interest rates, or even require a larger down payment or a co-signer for approval. For a deeper dive, check out our guide on ‘Understanding Your Credit Score’ to learn how to improve it.

Debt-to-Income Ratio (DTI)

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to handle additional debt, like a car loan. A lower DTI (generally below 36-43%) indicates that you have more disposable income to cover your new car payment.

If your DTI is too high, lenders may view you as overextended, even with a good credit score. This could lead to a denial or a requirement for a larger down payment to reduce the loan amount. Managing your existing debts is crucial before applying for a new loan.

Loan-to-Value (LTV)

The LTV ratio compares the amount you’re borrowing to the car’s actual value. For example, if you’re borrowing $20,000 for a car worth $20,000, your LTV is 100%. If you put down $4,000, borrowing $16,000, your LTV is 80%. Lenders prefer a lower LTV.

A high LTV, especially above 100% (common if you roll negative equity from a trade-in into a new loan), increases the risk for the lender. It means that if you default, the car might not be worth enough to cover the outstanding loan balance. A strong down payment helps lower your LTV.

Lender Policies

Every financial institution, including Uccu, has its own unique lending policies, risk assessments, and product offerings. While general principles apply, specific eligibility requirements, maximum loan amounts, and rate tiers can vary. What one lender approves, another might deny, or offer at a different rate.

This underscores the importance of not only using a calculator but also reaching out to specific lenders. Understanding Uccu’s specific offerings and any member benefits can be a distinct advantage. Credit unions often have a reputation for more personalized service and potentially better rates for their members.

Strategies for Securing a Better Uccu Car Loan Deal

Once you understand the mechanics of the Uccu Car Loan Calculator and the factors influencing your loan, the next step is proactive planning. There are several strategies you can employ to improve your chances of securing the most favorable terms for your auto loan.

Boost Your Credit Score

This is foundational. Review your credit report for errors and dispute any inaccuracies. Pay all your bills on time, every time, and reduce your outstanding credit card balances to lower your credit utilization. These actions can significantly improve your score over time.

A higher score gives you more leverage when negotiating rates. It signals reliability to lenders, making you a more attractive borrower. Start this process months before you plan to buy a car for the best results.

Increase Your Down Payment

The power of upfront cash cannot be overstated. A larger down payment reduces the principal loan amount, which immediately lowers your monthly payments and the total interest paid over the loan’s life. It also reduces your LTV, making your loan more appealing to lenders.

Furthermore, a substantial down payment helps protect you from being "upside down" on your loan. This means owing more than the car is worth due to rapid depreciation. Aiming for 20% or more is an excellent financial goal.

Shorten Your Loan Term (If Affordable)

While longer terms offer lower monthly payments, they come at the cost of significantly more interest paid. If your budget allows, opt for the shortest loan term you can comfortably afford. This strategy saves you money in the long run and helps you pay off the debt faster.

Use the Uccu Car Loan Calculator to see the difference in total interest paid between a 60-month and a 48-month loan on the same principal. The savings can be substantial, demonstrating the long-term benefit of higher monthly payments.

Shop Around for Rates

Never settle for the first loan offer you receive, even if it seems good. Contact multiple lenders—banks, credit unions like Uccu, and online lenders—to compare their rates and terms. Many offer pre-qualification that allows you to see potential rates without impacting your credit score.

This comparison shopping ensures you get the most competitive rate available to you. Even a half-percentage point difference can save you hundreds of dollars over a 5-year loan. Being prepared with multiple offers gives you strong negotiation power.

Negotiate the Car Price

Your first point of savings often comes before the loan itself: the purchase price of the car. Research market values, understand what similar vehicles are selling for, and be prepared to negotiate with the dealership. A lower purchase price means you need to borrow less, directly impacting your loan.

Don’t let the dealership distract you by focusing solely on monthly payments. Always negotiate the total purchase price first. Our article on ‘Effective Car Price Negotiation Strategies’ offers more insights into this crucial step.

Consider a Co-signer

If your credit score is low or your DTI is high, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. A co-signer essentially guarantees the loan, taking on equal responsibility for repayment.

This is a serious commitment for the co-signer, as any missed payments will negatively affect their credit. Use this option judiciously and only with someone you trust implicitly, and who understands the full implications.

Common Mistakes to Avoid When Using the Uccu Car Loan Calculator and Financing a Car

Even with the best intentions, car buyers can fall into common traps that lead to less-than-ideal financing outcomes. Based on my experience, awareness of these pitfalls is your best defense. Common mistakes to avoid are:

-

Focusing Solely on Monthly Payments: This is perhaps the most prevalent mistake. Dealerships often try to steer conversations toward "what monthly payment are you comfortable with?" While important, focusing exclusively on this number can lead you to accept longer loan terms, higher interest rates, or expensive add-ons just to hit that payment target. Always consider the total cost of the loan.

-

Ignoring Total Interest Paid: A low monthly payment might feel good, but if it comes with a 72 or 84-month term and a high interest rate, you could end up paying significantly more in total interest than the car is worth. The Uccu Car Loan Calculator will show you this total interest figure; pay close attention to it.

-

Not Factoring in Additional Costs: Beyond the loan payment, owning a car comes with insurance, fuel, maintenance, and potential repair costs. Failing to budget for these can quickly make an "affordable" car loan unsustainable. A car is more than just a monthly payment; it’s a bundle of ongoing expenses.

-

Underestimating Your Credit Score’s Impact: Many buyers don’t check their credit score before shopping for a loan. They’re then surprised by high interest rates or loan denials. Your credit score dictates the terms you’ll be offered. Know it, and work to improve it, before you apply.

-

Failing to Pre-Qualify: Walking into a dealership without pre-qualification from your bank or credit union (like Uccu) puts you at a disadvantage. The dealership will likely offer you their own financing, which may not be the best rate. Pre-qualification gives you a benchmark and strengthens your negotiating position.

-

Rolling Negative Equity into a New Loan: If you owe more on your current car than it’s worth (negative equity), some dealers will offer to roll that balance into your new car loan. While it seems convenient, it means you’re immediately "upside down" on your new loan, financing an amount greater than the new car’s value. This is a financially risky move.

Uccu Car Loans: Why Local Credit Unions Can Be a Smart Choice

While the Uccu Car Loan Calculator is a generic tool, the "Uccu" in its name points to a credit union. And when it comes to car financing, credit unions often stand out as a smart choice for several compelling reasons. They operate differently from traditional banks, and these differences can translate into significant benefits for their members.

Firstly, credit unions are not-for-profit organizations. Unlike banks, which are driven by shareholder profits, credit unions are member-owned. This fundamental difference often means they can offer more competitive interest rates on loans, including auto loans, and higher returns on savings accounts. Their primary mission is to serve their members, not to maximize profits.

Secondly, credit unions are renowned for their personalized service. Being smaller and community-focused, they often provide a more tailored and attentive experience. This can be particularly beneficial if your financial situation is complex, or if you appreciate building a relationship with your financial institution. They might be more willing to work with members on unique circumstances compared to larger, more impersonal banks.

Finally, credit unions often have more flexible lending criteria. While they still assess creditworthiness, their member-centric approach might mean they look beyond just a credit score, considering your overall financial picture and your relationship with the credit union. This can be a boon for those with less-than-perfect credit who might struggle to get approved elsewhere. For more insights into the benefits of credit unions, a trusted resource like Investopedia offers excellent general information.

The Road Ahead: Beyond Your Loan Calculation

Using the Uccu Car Loan Calculator is a powerful first step, but smart car ownership extends far beyond the initial purchase and loan agreement. Thinking about the future will ensure your car remains a benefit, not a burden.

Budgeting for ongoing ownership costs is crucial. This includes not just your monthly loan payment, but also insurance premiums, fuel expenses, routine maintenance, and an emergency fund for unexpected repairs. These costs can quickly add up and impact your overall financial health. A comprehensive budget helps you stay on track.

Keep an eye on interest rates even after you’ve secured your loan. If rates drop significantly, or if your credit score improves dramatically, you might consider refinancing your car loan. Refinancing can potentially lower your interest rate, reduce your monthly payments, or shorten your loan term, saving you money in the long run.

Finally, maintaining good credit is an ongoing process. Your car loan is a significant entry on your credit report. Making timely payments will further strengthen your credit score, opening doors to even better financial opportunities in the future. It’s an investment in your financial well-being that pays dividends for years to come.

Conclusion

Navigating the world of car financing doesn’t have to be intimidating. With tools like the Uccu Car Loan Calculator and a solid understanding of the factors involved, you can approach your next vehicle purchase with confidence and clarity. This article has aimed to provide you with that comprehensive understanding, from deconstructing the calculator’s inputs to revealing strategies for securing the best possible loan terms.

Remember, the Uccu Car Loan Calculator is more than just a simple math tool; it’s a gateway to financial empowerment. It allows you to experiment, plan, and make informed decisions that align with your budget and financial goals. By taking a proactive, educated approach, you can avoid common pitfalls and ensure your car ownership journey is a smooth and enjoyable one.

So, take control of your car buying experience. Use the Uccu Car Loan Calculator, apply the strategies discussed, and drive away not just with a new car, but with the peace of mind that comes from making a smart financial choice. Your road to smart auto financing starts now!