Mastering Your Wheels: A Deep Dive into the RBC Car Loan Calculator

Mastering Your Wheels: A Deep Dive into the RBC Car Loan Calculator Carloan.Guidemechanic.com

The open road beckons, the scent of a new car is in the air, and the dream of driving your ideal vehicle is within reach. Buying a car is an exciting milestone, but for many, the financial intricacies can quickly turn excitement into apprehension. How much can you truly afford? What will your monthly payments look like? These crucial questions often lead potential buyers down a rabbit hole of complex calculations and confusing terms.

Fortunately, powerful tools exist to simplify this process. One such invaluable resource is the RBC Car Loan Calculator. This isn’t just a simple number cruncher; it’s a strategic partner in your car buying journey, empowering you to make informed decisions and approach financing with confidence. In this comprehensive guide, we’ll peel back the layers of car financing, explain how the RBC Car Loan Calculator works, and equip you with the knowledge to drive away with a deal that truly fits your budget.

Mastering Your Wheels: A Deep Dive into the RBC Car Loan Calculator

Why a Car Loan Calculator is Your Indispensable Co-Pilot

Think of a car loan calculator as your financial GPS for vehicle acquisition. It doesn’t just give you a destination; it helps you plot the most efficient and affordable route. Before you even step foot on a dealership lot, this tool allows you to simulate various financing scenarios, giving you a clear picture of your potential financial commitment.

The real value of a calculator like RBC’s lies in its ability to transform abstract figures into concrete, understandable monthly payments. It helps you understand the direct impact of different variables – from the car’s price to the interest rate – on your personal budget. This foresight is critical for responsible financial planning.

Based on my experience, many people jump into car shopping without a clear understanding of their borrowing power or what constitutes an affordable payment. This often leads to impulse decisions or taking on more debt than is comfortable. A car loan calculator provides that essential reality check, allowing you to set realistic expectations and avoid future financial strain. It’s about empowerment through knowledge, ensuring your dream car doesn’t become a financial nightmare.

Demystifying the RBC Car Loan Calculator: How It Works

The RBC Car Loan Calculator is designed with user-friendliness in mind, but understanding its underlying mechanics will maximize its utility. At its core, it’s a sophisticated tool that takes several key inputs and, using financial formulas, provides you with crucial outputs, primarily your estimated monthly payment.

Let’s break down the essential components you’ll interact with:

-

Loan Amount (Principal): This is the total amount of money you need to borrow for the car. It’s typically the purchase price of the vehicle minus any down payment or trade-in value you might have. Getting this figure right is your first step.

-

Interest Rate: This is the cost of borrowing money, expressed as a percentage of the principal. It’s one of the most significant factors influencing your total loan cost. While the calculator allows you to input an estimated rate, your actual rate will depend on factors like your credit score and current market conditions.

-

Amortization Period (Loan Term): This refers to the length of time, usually in months or years, over which you will repay the loan. Common terms range from 36 to 84 months. This choice has a profound impact on both your monthly payment and the total interest you’ll pay over the life of the loan.

-

Down Payment (Optional): While not always a direct input field on every calculator, understanding its role is vital. A down payment is an initial lump sum you pay upfront towards the car’s purchase price. The calculator implicitly accounts for this by allowing you to reduce your "Loan Amount" input. The larger your down payment, the less you need to borrow, which directly translates to lower monthly payments and less interest paid over time.

Once you input these figures, the RBC Car Loan Calculator swiftly calculates your estimated monthly payment. It also often provides a breakdown of the total interest you’ll pay and the total cost of the loan, giving you a holistic financial perspective.

Key Variables That Influence Your Car Loan (and How RBC Considers Them)

Understanding the inputs for the RBC Car Loan Calculator is just the beginning. To truly master your car financing, you need to grasp the deeper implications of each variable and how lenders like RBC assess them.

The Power of the Interest Rate

The interest rate is arguably the most impactful number in your car loan equation. It dictates how much extra you’ll pay beyond the principal amount. A seemingly small difference in percentage points can translate into thousands of dollars over the loan’s lifetime.

Your interest rate is primarily determined by several factors:

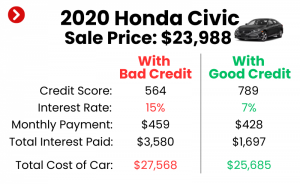

- Your Credit Score: This is a numerical representation of your creditworthiness. A higher score indicates a lower risk to lenders, typically resulting in a lower interest rate. RBC, like other major financial institutions, heavily relies on your credit score during the approval process.

- Market Conditions: General economic factors and the Bank of Canada’s prime lending rate influence all interest rates. What might be a good rate today could differ in a few months.

- Loan Term: Shorter loan terms often come with slightly lower interest rates because the lender’s risk is reduced.

- Lender Policies: Each financial institution, including RBC, has its own risk assessment models and rate structures.

Pro tips from us: Always strive for a strong credit score before applying for a car loan. Even a few points can make a noticeable difference in your approved interest rate, saving you substantial money over time.

Navigating the Loan Term (Amortization Period)

The loan term is the period over which you agree to repay your RBC auto loan. This is where many buyers face a critical trade-off.

- Shorter Terms (e.g., 36-48 months): These typically result in higher monthly payments but significantly less total interest paid. You own the car outright faster, and your overall cost is lower.

- Longer Terms (e.g., 72-84 months): These offer lower monthly payments, making the car seem more affordable upfront. However, you’ll pay substantially more in total interest over the life of the loan, and you might find yourself upside down on your loan (owing more than the car is worth) for a longer period.

Finding the right balance depends on your personal financial situation. While lower monthly payments can be tempting, remember the long-term cost. The RBC Car Loan Calculator allows you to easily compare these scenarios side-by-side, revealing the true cost of extending your loan term.

The Strategic Advantage of a Down Payment

A down payment is your upfront investment in your vehicle. It directly reduces the amount you need to borrow, which has several benefits:

- Lower Monthly Payments: Less principal means smaller installments.

- Reduced Total Interest: You’re paying interest on a smaller sum from day one.

- Improved Approval Chances: A substantial down payment signals financial stability to lenders like RBC, potentially leading to better interest rates.

- Less Risk of Negative Equity: You’re less likely to owe more than the car is worth, especially in the early years of ownership when depreciation is highest.

Common mistakes to avoid are underestimating the power of a good down payment. Even a few thousand dollars can make a significant difference in your monthly budget and overall loan cost. If possible, save up a reasonable down payment before you start shopping for a car.

The Crucial Role of Your Credit Score

Your credit score is your financial report card, and it plays a starring role in securing favorable car loan rates. Lenders use this score to assess the likelihood of you repaying your debt.

- Excellent Credit (760+): You’ll likely qualify for the best interest rates available from RBC.

- Good Credit (660-759): You’ll still get competitive rates, but they might be slightly higher than those with excellent credit.

- Fair Credit (560-659): Rates will be higher, reflecting the increased risk.

- Poor Credit (below 560): Approval might be challenging, and interest rates will be significantly higher.

RBC, like all reputable lenders, wants to ensure you can comfortably manage your loan obligations. A strong credit history demonstrates your reliability. If your credit score isn’t where you want it to be, consider taking steps to improve it before applying for a car loan. This could include paying bills on time, reducing existing debt, and checking your credit report for errors. For a deeper dive into managing your debt, read our guide on .

Beyond the Calculator: Smart Strategies for Your RBC Car Loan

While the RBC Car Loan Calculator is an exceptional tool, it’s part of a larger strategic approach to car buying. Leveraging additional tactics can further enhance your financial position.

The Power of Pre-Approval

Getting car loan pre-approval from RBC before you even visit a dealership is one of the smartest moves you can make. It transforms you from a speculative shopper into a confident buyer with known borrowing power.

- Negotiating Leverage: You walk into the dealership knowing exactly how much you can spend and what interest rate you qualify for. This empowers you to negotiate the car’s price, rather than just focusing on monthly payments dictated by the dealer’s financing.

- Clear Budget: Pre-approval sets a firm ceiling on your spending, preventing you from falling in love with a car outside your financial comfort zone.

- Faster Process: With your financing already lined up, the purchasing process at the dealership becomes much quicker and smoother.

RBC offers a straightforward pre-approval process, allowing you to get a clear picture of your borrowing options before committing to a specific vehicle.

Budgeting Realistically: Beyond the Monthly Payment

Common mistakes to avoid are focusing solely on the monthly payment shown by the calculator. A car’s true cost extends far beyond its purchase price and loan installments.

When budgeting for a car, consider the total cost of ownership:

- Car Insurance: This can be a significant monthly expense, varying wildly based on your vehicle, driving history, and location.

- Fuel Costs: Estimate your weekly or monthly fuel consumption.

- Maintenance and Repairs: All cars require regular servicing. Factor in oil changes, tire rotations, and potential unexpected repairs.

- Registration and Licensing Fees: Annual costs associated with vehicle ownership.

Understanding your full financial picture, including your debt-to-income ratio (your total monthly debt payments divided by your gross monthly income), ensures your car loan remains truly affordable and doesn’t strain your overall finances.

Comparing Offers: Not All Loans Are Created Equal

Even if you’re set on an RBC auto loan, it’s wise to understand the broader financing landscape. While RBC offers competitive rates and excellent service, comparing different financing options can sometimes reveal even better deals or terms.

- Dealer Financing: Dealerships often partner with multiple lenders, including RBC, to offer financing. They might present special promotions or incentives.

- Direct Bank Loans: Applying directly with RBC or another bank often gives you a clear, transparent offer separate from the car purchase itself.

- Credit Unions: Sometimes, local credit unions can offer slightly lower rates due to their non-profit structure.

Always review the full loan agreement, looking for hidden fees, prepayment penalties, and specific terms. Ensure you’re comparing apples to apples when evaluating different offers.

Practical Walkthrough: Using the RBC Car Loan Calculator Effectively

Let’s put theory into practice. Imagine you’re eyeing a new car with a sticker price of $35,000. You have a trade-in worth $5,000, and you’re planning a $2,000 cash down payment. This means your loan amount will be $35,000 – $5,000 – $2,000 = $28,000.

Now, let’s play with the RBC Car Loan Calculator inputs:

Scenario 1: The Affordable Monthly Payment Dream

- Loan Amount: $28,000

- Interest Rate: 6.99% (a reasonable estimate for good credit)

- Loan Term: 84 months (7 years)

- Calculator Output: Your estimated monthly payment might be around $410.

Scenario 2: The Long-Term Savings Approach

- Loan Amount: $28,000

- Interest Rate: 6.99%

- Loan Term: 60 months (5 years)

- Calculator Output: Your estimated monthly payment might jump to around $555, but the total interest paid over the loan term will be significantly less.

Scenario 3: The Impact of a Better Rate

- Loan Amount: $28,000

- Interest Rate: 4.99% (if you have excellent credit or catch a special promotion)

- Loan Term: 60 months

- Calculator Output: Your estimated monthly payment could drop to around $528, further reducing your total interest paid.

This iterative process, adjusting the loan term, interest rate (if you can improve your credit), or down payment, allows you to find your financial sweet spot. It’s about understanding the compromises and benefits of each choice. For a deeper dive into managing your debt, read our guide on .

Common Misconceptions and Pro Tips When Using a Car Loan Calculator

Even with such a powerful tool, it’s easy to fall into common traps. Here are some misconceptions to clarify and pro tips to keep in mind:

Misconception 1: The Calculator is the Final Word

While incredibly accurate for estimations, the RBC Car Loan Calculator provides estimates. Your actual monthly payment and interest rate can vary based on the final negotiation, any additional fees (like registration, documentation fees, extended warranties), and RBC’s final credit assessment.

Misconception 2: Only Focus on the Monthly Payment

From my years of observing car buyers, this is the most prevalent mistake. A low monthly payment can be alluring, but it often masks a longer loan term and a much higher total interest cost. Always look at the total cost of the loan – principal plus interest – not just the monthly installment.

Pro Tip 1: Factor in All Additional Costs

Beyond the loan amount, remember to account for sales tax, licensing, registration, and any administrative fees. These can add several hundred to thousands of dollars to your initial outlay or be rolled into the loan, increasing your principal.

Pro Tip 2: Don’t Extend the Loan Term Solely for Lower Payments

Unless absolutely necessary for your budget, resist the urge to stretch your loan term beyond what’s comfortable. While an 84-month loan might offer a tantalizingly low payment, the extra years of interest can significantly inflate your overall cost. Aim for the shortest term you can comfortably afford.

Why Choose RBC for Your Car Loan?

When it comes to auto loan financing, choosing a reputable and stable financial institution is paramount. RBC stands out for several compelling reasons:

- Reputation and Trust: As one of Canada’s largest banks, RBC brings a high level of trust and financial stability.

- Competitive Rates: RBC consistently offers competitive car loan rates, especially for those with strong credit profiles.

- Flexible Options: They provide a range of financing options to suit different needs, whether you’re buying new or used, from a dealership or privately.

- Convenience: Their online tools, including the RBC Car Loan Calculator, and extensive branch network make the application and management process straightforward.

- Customer Service: RBC is known for its comprehensive customer support, helping you navigate any questions or concerns you might have throughout your loan term.

By choosing RBC, you’re not just getting a loan; you’re partnering with a financial institution committed to helping you achieve your car ownership goals with confidence. Explore their current offerings and use their official calculator at External Link: RBC Car Loans & Financing to start your planning.

Conclusion: Drive Away with Confidence

The journey to owning a new car should be exciting, not intimidating. By understanding the intricacies of car financing and effectively utilizing tools like the RBC Car Loan Calculator, you empower yourself to make smart, informed decisions. This comprehensive guide has equipped you with the knowledge to dissect loan terms, optimize your budget, and approach the car buying process like a seasoned financial expert.

Remember, the goal isn’t just to get a car loan; it’s to secure an affordable car loan that aligns perfectly with your financial health. So, take control, leverage the power of the calculator, plan meticulously, and drive away not just with your dream car, but with the peace of mind that comes from a financially sound choice. Your smart car loan starts here.