Mastering Your Wheels: The Ultimate Guide on How to Pay Your Car Loan Strategically and Save Thousands

Mastering Your Wheels: The Ultimate Guide on How to Pay Your Car Loan Strategically and Save Thousands Carloan.Guidemechanic.com

Owning a car offers unparalleled freedom, but for many, that freedom comes with a significant monthly commitment: the car loan. It’s not just about making the minimum payment; it’s about understanding your loan, leveraging smart strategies, and ultimately, taking control of your financial future. This isn’t just a simple checklist; it’s a deep dive into how to pay car loan effectively, designed to empower you with the knowledge to pay it off faster, save money, and achieve financial peace of mind.

Based on my extensive experience in personal finance and helping countless individuals navigate their debt, the approach you take to your car loan can make a world of difference. It’s a journey that requires a bit of planning, a dash of discipline, and the right information. Let’s embark on this journey together and transform your car loan from a burden into a stepping stone towards greater financial stability.

Mastering Your Wheels: The Ultimate Guide on How to Pay Your Car Loan Strategically and Save Thousands

Understanding the Anatomy of Your Car Loan: The First Step to Control

Before you can strategically tackle your car loan, you need to fully understand its components. This isn’t just fine print; it’s the blueprint of your debt. Knowing these details is crucial for making informed decisions.

Decoding Your Loan Agreement

Every car loan comes with a detailed agreement that outlines the terms of your borrowing. Key elements include the principal amount, which is the total sum you borrowed for the vehicle. Then there’s the interest rate, expressed as an annual percentage rate (APR), which is the cost of borrowing money over a year. The loan term, typically measured in months, dictates how long you have to repay the loan.

The amortization schedule is also vital. This shows how your payments are applied over time, illustrating how much goes towards interest versus the principal balance with each installment. Early in the loan, a larger portion of your payment often goes to interest, gradually shifting towards the principal as the loan matures. Understanding this helps you see the true impact of making extra payments.

Secured vs. Unsecured Loans

Most car loans are "secured" loans, meaning the car itself serves as collateral. If you fail to make payments, the lender has the right to repossess your vehicle to recover their losses. This distinction is important because it highlights the immediate risk of defaulting on your car loan. Unsecured loans, like personal loans, don’t have collateral, but they are rare for car purchases and often come with much higher interest rates.

Knowing these fundamental aspects of your car loan agreement is the bedrock upon which all effective payment strategies are built. It allows you to visualize the journey ahead and identify potential shortcuts.

Core Strategies: How to Pay Car Loan Effectively

Now that you understand the basics, let’s explore the powerful strategies that can help you pay off your car loan smarter and faster. These methods range from consistent good habits to more aggressive financial maneuvers.

1. The Power of Consistent, On-Time Payments

This might seem obvious, but its importance cannot be overstated. Making your payments on time, every single month, is the absolute foundation of responsible car loan management. It protects your credit score, prevents late fees, and keeps you in good standing with your lender.

Why Consistency Matters More Than You Think:

- Credit Score Impact: Your payment history is the most significant factor in your credit score calculation. Late payments can drastically reduce your score, impacting your ability to secure future loans or even housing.

- Avoiding Penalties: Lenders impose late fees, which are essentially penalties for not adhering to your agreement. These fees add up quickly and don’t contribute to paying down your principal.

- Maintaining Trust: A consistent payment history builds trust with your lender, which can be beneficial if you ever need to discuss options during a financial hardship.

Pro Tip: Set up automatic payments directly from your bank account. This ensures you never miss a due date and removes the mental burden of remembering to pay each month. Based on my experience, automation is the simplest yet most effective habit for managing recurring bills.

2. Accelerating Your Payoff: Making Extra Payments

This is where you start taking control and truly saving money. Every extra dollar you pay towards your principal reduces the amount of interest you’ll owe over the life of the loan. The earlier you start, the greater the impact.

Strategies for Making Extra Payments:

- Round-Up Payments: If your payment is $347, round it up to $350 or even $375. Those small, consistent additions can shave months off your loan term and save hundreds in interest without feeling like a major sacrifice.

- Bi-Weekly Payments: Instead of one full payment per month, divide your monthly payment in half and pay that amount every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments annually instead of 12. This subtle shift effectively adds one extra payment per year.

- Applying Windfalls: Did you receive a tax refund, a work bonus, or an unexpected gift? Instead of spending it, consider applying a portion or all of it directly to your car loan principal. This can have a dramatic effect on your payoff timeline and total interest paid.

- One Extra Payment Annually: If bi-weekly payments feel too frequent, commit to making one extra full payment per year. You can do this by saving a little extra each month or by using a year-end bonus.

Crucial Step: When making extra payments, always specify that the additional amount should be applied directly to the principal balance. Some lenders will automatically apply extra funds to future interest, which defeats the purpose of accelerating your payoff. A quick call to your lender or a clear notation on your payment can ensure your money works effectively for you.

3. Refinancing Your Car Loan

Refinancing involves taking out a new loan, usually with a different lender, to pay off your existing car loan. This strategy can be incredibly powerful if you can secure a lower interest rate or a more favorable loan term.

When Refinancing Makes Sense:

- Lower Interest Rates: If your credit score has improved since you first took out the loan, or if market interest rates have dropped, you might qualify for a significantly lower APR. This directly reduces your monthly payment and the total interest you’ll pay.

- Shorter Loan Term: You might refinance to a shorter term, which typically comes with a lower interest rate. While your monthly payment might increase slightly, you’ll pay off the loan much faster and save a substantial amount on interest.

- Improved Financial Standing: If your income has increased, or your debt-to-income ratio has improved, lenders may view you as a less risky borrower, offering better terms.

Pro Tips from Us: Before refinancing, always compare offers from multiple lenders. Check your credit score first, as a good score is key to securing the best rates. Also, be wary of extending your loan term just to lower your monthly payment, as this often leads to paying more interest over time. For more in-depth information, you might find our article, "Is Refinancing Your Car Loan Right for You?", incredibly helpful. (Internal Link 1: Assuming a blog post on refinancing exists)

4. Budgeting for Your Car Loan

A well-structured budget is the bedrock of all successful financial strategies, including how to pay car loan. It allows you to see exactly where your money is going and identify areas where you can free up funds to put towards your loan.

Integrating Car Payments into Your Budget:

- Track Your Spending: Use a budgeting app, spreadsheet, or pen and paper to meticulously track every dollar you spend for a month or two. This will reveal your true spending habits.

- Identify Areas for Cuts: Are there subscriptions you don’t use? Can you cut back on dining out? Even small adjustments can free up $20, $50, or $100 per month that can be directed to your car loan principal.

- Allocate "Extra" Funds: Once you’ve identified potential savings, intentionally allocate those funds to your car loan. Don’t let them disappear into general spending.

- The 50/30/20 Rule: Consider adopting a budgeting framework like the 50/30/20 rule, where 50% of your income goes to needs (including your car payment), 30% to wants, and 20% to savings and debt repayment. This helps ensure your car loan is part of a balanced financial plan.

A consistent budget empowers you to proactively manage your finances rather than reactively dealing with bills. For further guidance on managing your money effectively, check out our comprehensive guide on "Mastering Your Monthly Budget: A Practical Approach to Financial Freedom." (Internal Link 2: Assuming a blog post on budgeting exists)

Advanced Car Loan Management & Considerations

Beyond the core strategies, there are other important aspects to consider when managing your car loan, especially if you encounter financial difficulties or want to optimize your long-term financial health.

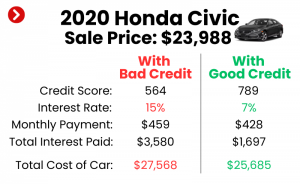

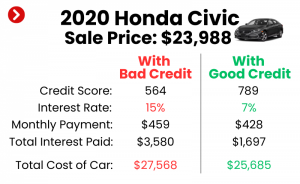

Impact of Your Credit Score

Your credit score isn’t just a number; it’s a reflection of your financial reliability. A good credit score is crucial for securing favorable terms when you initially finance a car, and it becomes even more important if you consider refinancing. Lenders use your score to assess risk, and a higher score often translates to lower interest rates.

Maintaining a healthy credit score by making on-time payments and keeping your credit utilization low should always be a priority. This discipline pays dividends far beyond your current car loan.

Understanding Early Payoff Penalties

While rare for car loans, some loan agreements may include an "early payoff penalty" or "prepayment penalty." This is a fee charged by the lender if you pay off your loan before the scheduled term. Lenders include these clauses to recoup some of the interest they would have earned.

How to Check for Penalties: Always review your original loan agreement carefully. The penalty, if any, will be clearly stated. If you’re unsure, contact your lender directly and ask. Most standard car loans today do not have prepayment penalties, especially if they are simple interest loans, but it’s always wise to verify. Common mistakes to avoid are assuming there are no penalties without checking, as this could lead to unexpected fees.

Dealing with Financial Hardship

Life is unpredictable, and sometimes financial difficulties arise that make it challenging to meet your car loan obligations. Ignoring the problem is the worst thing you can do.

Proactive Steps During Hardship:

- Communicate with Your Lender: As soon as you anticipate difficulty making a payment, contact your lender. They may be willing to work with you to find a solution.

- Explore Options: Lenders might offer options such as:

- Deferment: Temporarily pausing your payments, often with interest still accruing.

- Forbearance: Allowing you to make reduced payments or no payments for a short period.

- Loan Modification: Adjusting the terms of your loan, possibly extending the term to lower monthly payments.

- Avoid Default: Defaulting on your car loan can lead to repossession, severe damage to your credit score, and additional fees. Exploring your options with the lender is always preferable to simply missing payments.

Based on my experience, lenders are often more willing to help if you reach out proactively rather than waiting until you’re already behind. They want to avoid the costly process of repossession as much as you do.

The Undeniable Benefits of Paying Off Your Car Loan Early

While the strategies might seem like extra effort, the rewards of paying off your car loan ahead of schedule are substantial and far-reaching.

- Significant Interest Savings: This is often the most tangible benefit. By reducing the loan term, you pay interest for a shorter period, potentially saving hundreds or even thousands of dollars that would have gone to the lender.

- Financial Freedom and Reduced Stress: Imagine one less monthly bill! Paying off your car loan frees up a significant portion of your income, giving you more flexibility and reducing financial stress.

- Improved Debt-to-Income Ratio: A lower debt-to-income (DTI) ratio is favorable for future borrowing, such as a mortgage. It shows lenders that you manage your debt responsibly.

- More Disposable Income: The money you were allocating to your car payment can now be directed towards other financial goals, such as building an emergency fund, investing, saving for a down payment on a home, or tackling other high-interest debt.

- Building Equity Faster: When your loan is paid off, you own your car outright. This means you have full equity in the vehicle, which can be beneficial if you decide to sell or trade it in the future.

- Peace of Mind: There’s an undeniable sense of accomplishment and security that comes with knowing you own your vehicle free and clear.

These benefits underscore why learning how to pay car loan strategically isn’t just about managing debt; it’s about building a stronger financial foundation for your future.

Tools and Resources to Help You on Your Journey

You don’t have to navigate your car loan payment strategy alone. Several tools and resources can empower you:

- Online Loan Amortization Calculators: These free tools allow you to input your loan details and see how extra payments impact your payoff date and total interest. They provide a clear visual of your savings.

- Budgeting Apps: Apps like Mint, YNAB (You Need A Budget), or Personal Capital can help you track spending, create budgets, and monitor your progress towards debt repayment goals.

- Credit Monitoring Services: Many banks and credit card companies offer free credit monitoring, allowing you to track your credit score and reports, which is essential if you plan to refinance.

- Trusted Financial Education Websites: Reputable sites like the Consumer Financial Protection Bureau (CFPB) offer unbiased advice and resources on managing various types of debt, including car loans. (External Link: https://www.consumerfinance.gov/)

Utilizing these resources can significantly enhance your ability to manage and pay off your car loan effectively.

Pro Tips from Our Experts and Common Mistakes to Avoid

Drawing from years of experience in personal finance, here are some final pieces of advice and pitfalls to steer clear of:

Expert Pro Tips:

- Always Read the Fine Print: Never sign a loan agreement without fully understanding every clause. If something is unclear, ask for clarification.

- Automate Everything You Can: From payments to savings, automation removes the human error factor and ensures consistency.

- Regularly Review Your Financial Situation: Your income and expenses change. Periodically revisit your budget and car loan strategy to ensure it still aligns with your goals.

- Prioritize High-Interest Debt: If you have other debts with significantly higher interest rates than your car loan (like credit card debt), consider tackling those first after ensuring your car payments are consistent.

- Don’t Forget About Insurance and Maintenance: Factor these into your overall car ownership budget. A paid-off car still requires ongoing costs.

Common Mistakes to Avoid:

- Only Paying the Minimum: While it keeps you current, it maximizes the interest you pay over the loan’s lifetime.

- Not Understanding Your Loan Terms: This leaves you vulnerable to unexpected fees or missing opportunities to save.

- Refinancing Without a Clear Benefit: Don’t refinance just for the sake of it. Ensure it genuinely offers a lower rate, shorter term, or better overall terms.

- Ignoring Financial Struggles: Hoping problems will go away rarely works. Proactive communication with your lender is key.

- Using Your Car as an ATM: Avoid taking out title loans or using your car as collateral for other high-interest loans, as this can put you in a worse financial position.

Conclusion: Drive Towards Financial Freedom

Paying off your car loan isn’t just a chore; it’s an opportunity to build robust financial habits and significantly improve your personal finances. By understanding the intricacies of your loan, adopting strategic payment methods, and leveraging available resources, you can transform your approach to debt. Whether you choose to make extra payments, refinance for a better rate, or meticulously budget, each step brings you closer to owning your vehicle outright and enjoying the true freedom it offers.

The journey to financial independence is paved with smart decisions, and mastering how to pay car loan is a crucial milestone on that path. Take control today, and enjoy the substantial rewards of being debt-free.

What strategies have you used to pay off your car loan? Share your experiences and tips in the comments below!