MSU Car Loan Rates: Your Expert Guide to Securing the Best Auto Financing as a Spartan

MSU Car Loan Rates: Your Expert Guide to Securing the Best Auto Financing as a Spartan Carloan.Guidemechanic.com

The dream of cruising through East Lansing in your own car is a common one for many Michigan State University students, alumni, and faculty. Whether you’re commuting to class, heading to an internship, or exploring the beautiful Michigan landscape, having reliable transportation offers unparalleled freedom and convenience. However, turning that dream into a reality often involves navigating the complex world of auto financing.

Understanding "MSU car loan rates" isn’t just about finding a loan; it’s about finding the right loan that fits your financial situation, offers competitive interest rates, and sets you up for financial success. This comprehensive guide, crafted by an expert in auto finance and SEO content, will demystify the process. We’ll explore where to find the best rates, what factors influence them, and how to position yourself as a prime borrower. Our ultimate goal is to equip you with the knowledge to secure an excellent car loan, ensuring a smooth ride from application to ownership.

MSU Car Loan Rates: Your Expert Guide to Securing the Best Auto Financing as a Spartan

Unpacking "MSU Car Loan Rates": What Does It Really Mean?

When you search for "MSU car loan rates," it’s important to clarify what this term actually signifies. Michigan State University itself does not directly offer car loans to its students, faculty, or alumni. Instead, the phrase typically refers to the favorable auto loan rates and terms available to the MSU community through financial institutions that serve them, particularly credit unions closely associated with the university.

These institutions understand the unique financial situations of students, often characterized by limited credit history or fluctuating income, as well as the stable profiles of faculty and alumni. They tailor their offerings to meet these diverse needs. While general market rates are always a factor, these community-focused lenders often provide an edge.

For instance, the MSU Federal Credit Union (MSUFCU) is a prime example of a financial institution deeply embedded in the MSU community. As a member-owned cooperative, credit unions like MSUFCU are known for generally offering lower interest rates and fewer fees compared to traditional banks. Their primary mission is to serve their members, not to maximize profits for shareholders. This member-centric approach can translate directly into more competitive car loan rates for anyone affiliated with MSU.

The distinction between a university-specific program and a community-focused lender is crucial. While you won’t walk into the university’s financial aid office for a car loan, leveraging your MSU affiliation with institutions like MSUFCU can be a highly strategic move. They often provide personalized service and a deep understanding of their members’ circumstances, which can be invaluable when securing an auto loan.

Key Factors That Drive Your Car Loan Rate

Understanding what influences your car loan rate is the first step toward securing the best possible deal. Several critical factors come into play, each playing a significant role in how lenders assess your risk and, consequently, the interest rate they offer. Knowing these elements allows you to strategically improve your position before even applying.

Your Credit Score: The Ultimate Indicator

Without a doubt, your credit score is the single most impactful factor determining your car loan rate. Lenders use scores like FICO and VantageScore to gauge your creditworthiness – essentially, how reliable you are at repaying debts. A higher score signals lower risk to lenders, which translates directly into lower interest rates and more favorable loan terms.

For example, someone with an excellent credit score (typically 760+) might qualify for rates as low as 3-5%, while a borrower with a fair score (580-669) could face rates of 10% or even higher. This difference can amount to thousands of dollars in interest paid over the life of the loan. Based on my experience, many first-time borrowers, particularly students, underestimate the power of their credit score. Taking steps to build or improve your credit before applying is a wise investment.

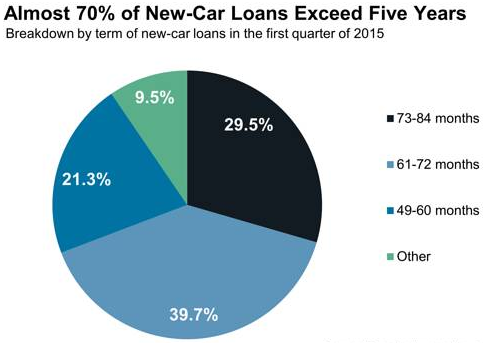

The Loan Term: Length Matters

The loan term refers to the duration over which you agree to repay the loan, commonly expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term typically means higher monthly payments but less total interest paid over the life of the loan. This is because you’re paying off the principal faster, giving interest less time to accrue.

Conversely, a longer loan term will result in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, the trade-off is often a higher total interest cost and potentially a slightly higher interest rate from the lender due to the increased risk associated with a longer repayment period. Lenders perceive longer terms as higher risk because more can change in your financial situation over an extended period.

Your Down Payment: Showing Commitment

Making a substantial down payment on your vehicle can significantly improve your car loan rate. A down payment reduces the amount of money you need to borrow, which lowers the lender’s risk. When you have more equity in the vehicle from the start, you’re less likely to default on the loan.

Lenders often reward this reduced risk with lower interest rates. Additionally, a larger down payment helps prevent you from being "upside down" on your loan, a situation where you owe more on the car than it’s worth. This can happen quickly with depreciation, and a solid down payment provides a buffer.

Interest Rate Type: Fixed vs. Variable

Most auto loans come with a fixed interest rate. This means your interest rate, and consequently your monthly payment (excluding any changes due to escrow if applicable, though less common with auto loans), will remain the same for the entire loan term. Fixed rates offer predictability and stability, which is highly desirable for budgeting.

While less common for car loans, some lenders might offer variable interest rates. These rates can fluctuate based on market conditions, typically tied to a benchmark index. While a variable rate might start lower than a fixed rate, it carries the risk of increasing over time, leading to higher monthly payments. For the vast majority of car buyers, a fixed-rate loan is the safer and more popular choice.

Vehicle Type: New or Used?

The type of vehicle you intend to purchase also impacts your loan rate. New cars generally qualify for lower interest rates than used cars. This is because new vehicles are perceived as less risky by lenders; they have warranties, predictable maintenance costs initially, and a known history.

Used car loan rates can vary significantly based on the vehicle’s age, mileage, and overall condition. An older, higher-mileage vehicle typically carries a higher risk for the lender due to potential mechanical issues and faster depreciation, leading to higher interest rates. Lenders also consider the resale value of the car as part of their risk assessment.

Lender Type: Who You Borrow From

The type of financial institution you choose can also influence your rate. Banks, credit unions, online lenders, and dealership financing each have their own rate structures and eligibility requirements. As discussed, credit unions often offer some of the most competitive rates due to their non-profit structure. We’ll delve deeper into this in the next section.

Your Debt-to-Income (DTI) Ratio

Lenders will also look at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income to cover your loan payments, making you a less risky borrower. A high DTI can signal that you are overextended, potentially leading to a higher interest rate or even loan denial.

Where MSU Students, Faculty & Alumni Can Find Competitive Car Loan Rates

Finding the best car loan rates requires strategic shopping and an understanding of where to look. For the MSU community, specific avenues often provide more favorable terms than the general market. Leveraging your affiliation can unlock significant savings.

Credit Unions: A Spartan’s Best Bet

For anyone connected to Michigan State University, credit unions are often the first and best place to start your search for competitive car loan rates. These member-owned financial cooperatives are renowned for their commitment to offering lower interest rates and fewer fees than traditional banks. Their primary goal is to serve their members, not to generate profits for shareholders.

MSU Federal Credit Union (MSUFCU) stands out as a premier option. As a credit union specifically serving the MSU community, they have a deep understanding of the financial needs and challenges faced by students, faculty, staff, and alumni. Their eligibility requirements are broad, often extending to family members of eligible individuals.

- Benefits of MSUFCU and other credit unions:

- Lower Interest Rates: Often significantly better than those offered by large commercial banks.

- Personalized Service: As a member, you’re more than just a customer; you’re an owner.

- Fewer Fees: Credit unions typically have lower or no fees for many services.

- Financial Education Resources: Many offer guidance tailored to students and young professionals.

Pro tips from us: Always check with MSUFCU first. Even if you’re not yet a member, exploring their membership eligibility criteria is highly recommended. Their rates are often a benchmark for what you should expect elsewhere.

Local and National Banks: Traditional Options

Traditional banks, ranging from large national institutions to smaller community banks, also offer auto loans. These can be a viable option, especially if you already have an established banking relationship with them. Many banks offer rate discounts for existing customers who set up automatic payments from their checking accounts.

While banks might not always match credit union rates, they offer convenience and a wide range of financial products. It’s worth comparing their offers, especially if you have a strong credit history. Remember, your relationship with a bank can sometimes be leveraged for a slightly better deal.

Online Lenders: Speed and Convenience

The rise of online lenders has revolutionized the car loan market, offering a convenient and often speedy application process. Websites like Capital One Auto Finance, LightStream, and others allow you to apply for pre-approval from the comfort of your home, often receiving decisions within minutes.

- Advantages of online lenders:

- Quick Pre-Approval: Streamlined applications mean fast decisions.

- Comparison Tools: Many sites allow you to compare multiple offers without impacting your credit score initially.

- Competitive Rates: Online lenders often have lower overheads, which can translate into competitive rates.

The key with online lenders is to thoroughly vet their reputation and read reviews. While they offer convenience, ensuring transparency and reliable customer service is paramount.

Dealership Financing: Proceed with Caution

Dealerships frequently offer financing options directly through their partnerships with various banks and captive finance companies (e.g., Ford Credit, Toyota Financial Services). This can be incredibly convenient, allowing you to handle the car purchase and financing in one place.

However, dealership financing isn’t always the most cost-effective option. While they might advertise attractive "special rates," these are often reserved for buyers with impeccable credit. Furthermore, dealerships sometimes mark up interest rates to increase their profit margins.

Pro tip: Always secure a pre-approval from an external lender (like MSUFCU or an online lender) before stepping onto the dealership lot. This gives you leverage to negotiate and ensures you have a benchmark rate to compare against any offers from the dealer. If the dealer can beat your pre-approved rate, that’s great; otherwise, you have a solid backup.

The Car Loan Application Process: A Step-by-Step Guide for Spartans

Navigating the car loan application process can seem daunting, but breaking it down into manageable steps makes it much clearer. For MSU students, faculty, and alumni, being prepared is your greatest asset. Follow this guide to ensure a smooth and successful experience.

1. Preparation is Your Secret Weapon

Before you even think about looking at cars, gather your financial intel. This foundational step is critical for a strong application.

- Check Your Credit Score and Report: Obtain a copy of your credit report from one of the three major bureaus (Experian, Equifax, TransUnion). Review it for errors and understand your current credit score. Knowing your score allows you to anticipate what rates you might qualify for. For more in-depth guidance on improving your credit score, check out our article on .

- Gather Essential Documents: Lenders will require documentation to verify your identity, income, and residency.

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs, tax returns, or offer letters (for new jobs). Students might use scholarship documentation, proof of part-time employment, or co-signer income.

- Proof of Residency: Utility bills, lease agreement, or bank statements.

- Proof of Enrollment (for students): Letter from the registrar’s office or student ID.

2. Budget Wisely: Know Your Limits

Don’t just focus on the car’s sticker price. A smart budget considers the total cost of car ownership, which goes far beyond the monthly loan payment.

- Determine Your Monthly Payment Comfort Zone: Use online calculators to estimate payments based on different loan amounts, terms, and interest rates.

- Factor in Additional Costs: Remember insurance (which can be substantial for younger drivers), fuel, maintenance, registration fees, and potential parking costs. Overlooking these can lead to financial strain. If you’re unsure about budgeting for a vehicle, our comprehensive guide to can provide further assistance.

3. Get Pre-Approved: Your Negotiating Powerhouse

Pre-approval is arguably the most crucial step in the car buying process. It means a lender has conditionally agreed to lend you a specific amount of money at a particular interest rate, based on your creditworthiness.

- How it Works: You submit a loan application to a credit union (like MSUFCU), bank, or online lender. They review your financial information and, if approved, issue a pre-approval letter.

- Benefits:

- Know Your Budget: You walk into the dealership knowing exactly how much you can afford.

- Shop Like a Cash Buyer: With pre-approval in hand, you can focus on negotiating the car’s price, not the monthly payment.

- Rate Benchmark: You have a firm interest rate to compare against any offers from the dealership, ensuring you get the best deal.

4. Shop for Your Car: With Confidence

Now, with your pre-approval in hand and a clear budget, you can confidently shop for a vehicle. This is where the fun begins, but stay disciplined.

- Stick to Your Budget: Don’t be swayed by persuasive sales tactics to go beyond what you can comfortably afford.

- Research Vehicles: Look up reliability ratings, safety features, and resale values for cars that fit your needs and budget.

- Test Drive Thoroughly: Ensure the car meets your expectations and feels right for you.

- Negotiate the Price: Remember, you’re negotiating the price of the car, not just the monthly payment. Your pre-approval gives you a strong position.

5. Finalize Your Loan: Read Every Detail

Once you’ve agreed on a vehicle, it’s time to finalize the financing. This is not the time to rush.

- Review All Loan Documents: Carefully read the loan agreement, including the interest rate, APR (Annual Percentage Rate), loan term, total loan amount, and any fees. Ensure there are no hidden costs or terms you don’t understand.

- Understand Your Payment Schedule: Confirm when your first payment is due and the exact monthly amount.

- Ask Questions: If anything is unclear, ask for clarification. Don’t sign until you are completely comfortable with all the terms.

Pro Tips for Securing the Best MSU Car Loan Rates

As an expert in auto financing, I’ve seen countless individuals navigate the loan process. Here are some invaluable pro tips to help you secure the most competitive car loan rates, especially as a member of the MSU community.

Boost Your Credit Score Before Applying

This cannot be stressed enough. A few points on your credit score can make a significant difference in your interest rate. Pro tips from us include:

- Pay Bills on Time: Payment history is the biggest factor in your credit score.

- Reduce Existing Debt: Lowering your credit utilization ratio (how much credit you’re using vs. available) can quickly improve your score.

- Avoid New Credit Applications: Don’t open new credit cards or loans just before applying for a car loan, as this can temporarily lower your score.

Save for a Larger Down Payment

A larger down payment is a powerful tool. It reduces the amount you need to borrow, which directly lowers your monthly payments and total interest. More importantly, it signals to lenders that you are a serious and lower-risk borrower, making them more likely to offer you a better interest rate. Aim for at least 10-20% of the car’s purchase price if possible.

Consider a Co-signer (Especially for Students)

If you’re a student with a limited credit history or a lower credit score, a co-signer can be a game-changer. A co-signer with excellent credit provides additional security for the lender, potentially helping you qualify for a much lower interest rate than you could achieve on your own.

- Important Note: A co-signer is equally responsible for the loan. If you miss payments, it impacts their credit, and they are legally obligated to repay the debt. Ensure both parties fully understand this commitment.

Shop Around and Compare Offers Aggressively

Never settle for the first loan offer you receive. Get pre-approvals from multiple lenders – your credit union (like MSUFCU), a local bank, and at least one online lender. Each lender will have slightly different criteria and rates, and comparing them ensures you find the most favorable terms. All hard inquiries for auto loans within a short period (typically 14-45 days) are often counted as a single inquiry, minimizing the impact on your credit score.

Negotiate the Car Price, Not Just the Loan

Remember, the lower the purchase price of the car, the less money you need to borrow. Focus your negotiation efforts on getting the best possible price for the vehicle first. Once you have a firm vehicle price, then you can apply your pre-approved loan or compare it with dealership financing. Negotiating both aspects separately ensures you’re getting the best deal on both ends.

Understand All Fees and Fine Print

Before signing any loan agreement, meticulously read through all documents. Ensure you understand every fee, term, and condition. This includes origination fees, documentation fees, and any early payoff penalties. Don’t be afraid to ask questions until you’re completely clear on what you’re signing. Ignorance can be very costly.

Common Mistakes MSU Students and Alumni Make When Applying for Car Loans

Even with the best intentions, borrowers often fall into common pitfalls that can lead to higher interest rates, financial strain, or even loan denial. Being aware of these mistakes is the first step to avoiding them.

1. Not Checking Their Credit Score First

Many applicants jump into the car buying process without knowing their credit score or reviewing their credit report. This puts them at a significant disadvantage. Common mistakes to avoid are:

- Surprise Denials: Not knowing your score can lead to unexpected loan rejections.

- Accepting High Rates: Without knowing your score, you can’t accurately gauge if an offered rate is fair for your credit profile, potentially accepting a higher rate than you deserve.

- Unaddressed Errors: Credit reports can contain errors that negatively impact your score. Discovering these late in the process can cause delays.

2. Only Applying to One Lender

As discussed, shopping around is crucial. Relying on a single loan offer, especially from a dealership, almost guarantees you won’t get the best possible rate. This limits your options and gives you no leverage in negotiations. Always get at least three pre-approvals from different types of lenders.

3. Focusing Solely on Monthly Payments

It’s tempting to fixate on the lowest possible monthly payment. However, this often leads to choosing a longer loan term, which means you’ll pay significantly more in total interest over the life of the loan. A low monthly payment can mask a much higher overall cost. Always consider the total amount you will pay back, including all interest and fees.

4. Skipping a Down Payment

While it might seem easier to finance 100% of the car’s value, skipping a down payment is a common mistake. It increases the total amount you borrow, leads to higher interest payments, and often results in a higher interest rate because the lender perceives greater risk. Moreover, you’re immediately "upside down" on your loan, owing more than the car is worth, which can be problematic if you need to sell or if the car is totaled.

5. Letting the Dealership Handle Everything Without External Pre-Approval

While convenient, allowing the dealership to be your sole source of financing without having an external pre-approval is a common misstep. Dealerships have an incentive to maximize their profit, which can sometimes include marking up the interest rate. Based on my experience, going to the dealership with your own financing already secured gives you significant bargaining power and helps ensure you get a fair deal.

6. Buying More Car Than You Can Afford

This is a classic mistake. The excitement of a new car can lead to emotional decisions, pushing you to buy a vehicle that exceeds your practical budget. Remember to factor in not just the loan payment, but also insurance, fuel, maintenance, and potential repairs. An expensive car can quickly become a financial burden if it stretches your budget too thin.

Understanding the True Cost of Your Car Loan

Beyond the sticker price and the seemingly manageable monthly payment, it’s vital to grasp the true, long-term cost of your car loan. This comprehensive view helps you make an informed financial decision and avoid surprises down the road.

The true cost of your car loan encompasses more than just the principal amount you borrow. It includes the total interest paid over the life of the loan, any origination or documentation fees, and potentially other charges. For instance, a small difference in interest rate can translate into hundreds, even thousands, of dollars over several years