My Unshakeable Belief Statement Regarding Car Loans: Navigating the Road to Smart Car Ownership

My Unshakeable Belief Statement Regarding Car Loans: Navigating the Road to Smart Car Ownership Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, symbolizing freedom, convenience, and a step forward in life. Yet, beneath the shiny exterior and the allure of a new ride lies one of the most significant financial commitments most individuals will make outside of a home purchase: the car loan. It’s a decision fraught with potential pitfalls and opportunities for smart financial growth.

As an expert blogger and professional in the realm of financial literacy, I’ve witnessed firsthand the profound impact a well-managed car loan can have on an individual’s financial health – and, conversely, the detrimental effects of poor borrowing choices. This isn’t just about securing transportation; it’s about making a responsible investment that aligns with your broader financial goals.

My Unshakeable Belief Statement Regarding Car Loans: Navigating the Road to Smart Car Ownership

This article isn’t merely a collection of tips; it’s a deep dive into the philosophy that should guide every car loan decision. It’s my "I Believe Statement Regarding Car Loans," a set of core principles designed to empower you to make informed, strategic choices. We’ll explore why having such a philosophy is crucial, delve into my specific beliefs, and provide actionable steps to implement them, ensuring your journey into car ownership is both joyful and financially sound.

Why a Personal Car Loan Philosophy Matters More Than You Think

Many people approach car buying with an emotional mindset, driven by desire or immediate need. They fall in love with a particular model, focus solely on the monthly payment, and often overlook the intricate financial details that truly define the deal. This reactive approach can lead to costly mistakes, trapping borrowers in cycles of debt, negative equity, and financial stress.

Having a well-defined car loan philosophy, a personal "I Believe Statement," shifts the power dynamic. It transforms you from a passive consumer into an empowered negotiator, armed with principles that prioritize your long-term financial well-being over fleeting impulses. This isn’t just about saving money; it’s about building good financial habits and making conscious decisions that support your overall wealth creation.

Based on my experience, individuals who approach car loans with a clear set of guiding principles are far less likely to regret their purchase. They understand the true cost, avoid common traps, and ultimately enjoy their vehicle without the burden of financial strain. This proactive stance ensures you’re not just buying a car, but investing wisely in your future.

My Core Beliefs Regarding Smart Car Loans

My "I Believe Statement Regarding Car Loans" is built upon a foundation of financial prudence, foresight, and a deep understanding of how these loans impact personal wealth. Each belief is designed to guide your decision-making process, transforming a potentially complex transaction into a clear, strategic path.

I Believe in Affordability First, Desire Second.

The allure of a new car can be intoxicating. We often find ourselves drawn to vehicles that might stretch our budget simply because they offer appealing features or a certain status. However, a fundamental principle of smart car loans dictates that true affordability must always precede desire. This means thoroughly understanding what you can comfortably afford, not just what a lender might approve you for.

This belief extends beyond just the monthly payment. It encompasses the entire cost of ownership, including insurance, maintenance, fuel, and registration. Pro tips from us: utilize a comprehensive budget planner to assess your current income and expenses. Calculate your debt-to-income ratio to ensure your new car payment won’t overextend your financial capacity. A car that feels like a burden every month isn’t a good deal, no matter how attractive its price tag.

I Believe Knowledge is Power: Research Before You Borrow.

Entering a car dealership or a lender’s office without prior research is like going into battle unarmed. The car loan landscape is complex, with varying interest rates, loan terms, fees, and lending institutions. Understanding these elements before you even start looking at cars puts you in a position of strength. This proactive approach allows you to compare offers effectively and identify the best possible terms for your situation.

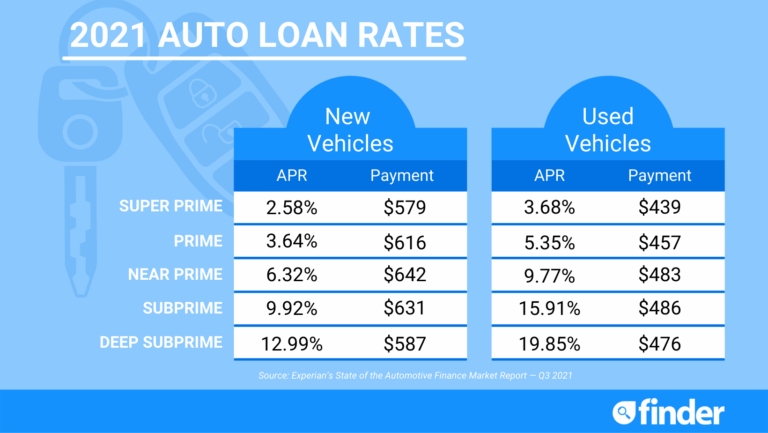

Common mistakes to avoid are signing on the dotted line without fully comprehending the Annual Percentage Rate (APR), which includes the interest rate plus other loan fees. Familiarize yourself with the difference between banks, credit unions, and dealership financing, as each offers distinct advantages and disadvantages. Credit unions, for instance, often provide more competitive rates due to their member-focused structure.

I Believe in the Power of the Down Payment.

A substantial down payment is one of the most powerful tools in your car loan arsenal. It directly reduces the amount you need to borrow, which, in turn, lowers your monthly payments and significantly decreases the total interest paid over the life of the loan. Furthermore, a larger down payment helps you build equity in your vehicle faster, reducing the risk of being "upside down" (owing more than the car is worth).

Based on my experience, aiming for at least a 20% down payment on a new car and 10% on a used car is an excellent financial strategy. While not always feasible for everyone, even a modest down payment can make a noticeable difference. It signals to lenders that you’re a serious borrower and can often lead to better interest rates. Consider saving specifically for this purpose before you even begin your car search.

I Believe in Shorter Loan Terms, When Feasible.

The temptation of lower monthly payments offered by longer loan terms (e.g., 72 or even 84 months) is strong, but it’s often a financial trap. While a longer term reduces your immediate financial outlay, it dramatically increases the total amount of interest you’ll pay over the life of the loan. It also prolongs the period you spend in debt, tying up your financial resources for years.

I advocate for the shortest loan term that you can comfortably afford. This might mean a slightly higher monthly payment, but the long-term savings in interest can be substantial. For example, a 36 or 48-month loan for a used car, or a 60-month loan for a new one, is generally more financially sound. Avoid extending your loan term just to fit a more expensive car into your budget; instead, adjust your car choice to fit a shorter, more responsible loan term.

I Believe in Pre-Approval as a Negotiation Tool.

Separating the car buying process from the financing process is a game-changer. Obtaining pre-approval for a car loan from an independent lender (like your bank or credit union) before stepping foot in a dealership is a crucial step. This means you know exactly how much you can borrow, at what interest rate, and under what terms, before you even start looking at vehicles.

With a pre-approval in hand, you become a cash buyer in the dealership’s eyes. This eliminates the uncertainty of financing and allows you to focus solely on negotiating the car’s price. You’re no longer at the mercy of the dealer’s financing department, which often has incentives to steer you towards higher-interest loans. for more on this. You can compare the dealer’s offer against your pre-approval, ensuring you get the best deal possible.

I Believe in Understanding the Total Cost of Ownership.

The price tag and the monthly payment are just the tip of the iceberg when it comes to car ownership. My belief system emphasizes a holistic view, requiring you to consider the total cost of ownership (TCO) before making a purchase. This comprehensive financial planning includes all recurring and incidental expenses associated with owning and operating a vehicle.

Beyond the loan payment, TCO encompasses:

- Insurance: Premiums vary significantly based on vehicle type, your driving record, and location.

- Fuel: Consider the car’s fuel efficiency and your typical mileage.

- Maintenance & Repairs: All cars require regular servicing, and older vehicles may incur unexpected repair costs.

- Registration & Taxes: Annual fees and potential sales tax.

- Depreciation: The loss of value over time, which is the single largest cost of car ownership.

Factoring in these elements ensures you don’t just afford the payment, but can comfortably manage the entire financial burden of your chosen vehicle.

I Believe in Protecting My Investment (Wisely).

While it’s important to protect your automotive investment, it’s equally crucial to distinguish between genuinely valuable protections and unnecessary upsells. Many dealerships will offer a myriad of add-ons, from extended warranties to paint protection packages. My belief is to scrutinize each offer with a critical eye, asking if it truly adds value and aligns with your financial plan.

One common protection often offered is GAP (Guaranteed Asset Protection) insurance. This can be beneficial if you make a small down payment and have a long loan term, as it covers the "gap" between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. However, it’s often cheaper to purchase GAP insurance from your own auto insurer or credit union than from the dealership. Extended warranties, while potentially useful for high-reliability vehicles, often have strict clauses and can be overpriced. Always research third-party options and consider the vehicle’s inherent reliability before committing.

I Believe in Regular Review and Early Payoff (If Possible).

A car loan isn’t a set-it-and-forget-it commitment. My final belief emphasizes the importance of regularly reviewing your loan terms and actively seeking opportunities for early payoff. Financial circumstances change, and what was the best loan for you initially might not remain so over time.

This means periodically checking interest rates for refinancing opportunities, especially if your credit score has improved since you took out the original loan. Even making small extra payments each month or applying any windfalls (like a bonus or tax refund) directly to your principal can significantly reduce the total interest paid and shorten your loan term. Staying out of long-term debt cycles is a cornerstone of robust financial health.

Implementing Your Car Loan Philosophy: Practical Steps

Having a robust "I Believe Statement Regarding Car Loans" is only half the battle; the other half is putting it into action. Here’s a practical roadmap to guide you:

- Assess Your Financial Health: Before you even dream of a car, create a detailed budget. Understand your income, fixed expenses, variable expenses, and how much you can truly allocate to a car payment and the associated costs of ownership without compromising other financial goals (like savings or retirement).

- Define Your "Affordable" Limit: Based on your budget, set a strict maximum for your total car payment (including insurance and potential maintenance savings). Don’t let a salesperson push you beyond this limit.

- Shop for the Loan First: Contact your bank, credit union, and reputable online lenders to get pre-approved for a loan. Compare their offers, focusing on the APR and loan term. This empowers you with a strong negotiating position.

- Negotiate with Confidence: With your pre-approval in hand, you can negotiate the car’s price separately from the financing. Don’t be afraid to walk away if the deal isn’t right. Remember, there are always other cars and other dealerships.

- Read the Fine Print: Before signing anything, meticulously review the entire loan agreement. Ensure all terms, rates, and fees match what was discussed. If you don’t understand something, ask for clarification. Don’t rush this critical step. for more detailed steps.

Common Car Loan Mistakes to Avoid

Even with the best intentions, it’s easy to fall prey to common car loan pitfalls. By understanding these, you can actively steer clear of them:

- Focusing Only on the Monthly Payment: This is perhaps the biggest mistake. A low monthly payment often comes with a much longer loan term and significantly more interest paid over time. Always consider the total cost.

- Ignoring the APR: The Annual Percentage Rate (APR) is the true cost of borrowing. Don’t just look at the interest rate; the APR includes all fees and gives you a more accurate picture.

- Not Getting Pre-Approved: As discussed, skipping pre-approval leaves you vulnerable to dealership financing that might not be in your best interest.

- Rolling Negative Equity into a New Loan: If you owe more on your current car than it’s worth, and you roll that amount into a new loan, you’re starting off "underwater." This can lead to a never-ending cycle of debt.

- Buying Too Much Car: Overspending on a vehicle that exceeds your practical needs or financial capacity is a recipe for regret. Prioritize reliability and affordability over unnecessary luxury.

- Skipping the Budget for Total Ownership Cost: Failing to account for insurance, maintenance, fuel, and depreciation means you’re only seeing part of the financial picture. These costs can quickly add up and strain your budget.

Common mistakes we often see also include not negotiating the price of the car itself. Many buyers get so caught up in the financing that they forget to haggle for a better vehicle price first. Always negotiate the car price before discussing financing options.

Conclusion: Driving Towards Financial Freedom

Adopting a robust "I Believe Statement Regarding Car Loans" isn’t about denying yourself the pleasure of car ownership; it’s about making choices that empower your financial future. It’s about approaching one of life’s significant purchases with clarity, intelligence, and a commitment to long-term well-being. By prioritizing affordability, thorough research, smart down payments, shorter terms, and proactive financial management, you transform a potential financial burden into a responsible asset.

Remember, a car loan should serve you, not the other way around. By embracing these core beliefs, you’re not just buying a car; you’re investing in peace of mind, financial stability, and the freedom that comes with smart, responsible car ownership. Drive wisely, live freely.

What are your core beliefs when it comes to car loans? Share your thoughts and experiences in the comments below!