Navigate the Road to Your Dream Car: A Deep Dive into Getting a Car Loan with Navy Federal

Navigate the Road to Your Dream Car: A Deep Dive into Getting a Car Loan with Navy Federal Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect, but the financing aspect can often feel like navigating a complex maze. For military personnel, veterans, and their families, a beacon of clarity and support often emerges: Navy Federal Credit Union (NFCU). Known for its unwavering commitment to its members, Navy Federal stands out as a top choice for auto loans, offering competitive rates, flexible terms, and exceptional service.

This comprehensive guide will demystify the process of getting a car loan with Navy Federal. We’ll cover everything from understanding membership requirements to securing your pre-approval and driving off in your new car. Our ultimate goal is to equip you with the knowledge and confidence to make informed decisions, ensuring a smooth and successful auto financing experience.

Navigate the Road to Your Dream Car: A Deep Dive into Getting a Car Loan with Navy Federal

Why Navy Federal Stands Out for Your Auto Loan Needs

Before diving into the "how-to," it’s crucial to understand why Navy Federal is such a highly regarded option for car loans. Their member-centric approach sets them apart from traditional banks and other lenders. Based on my experience in the financial realm, credit unions like Navy Federal often provide a more personalized touch and better terms because their primary focus is member benefit, not shareholder profit.

Here are some compelling reasons to consider an NFCU auto loan:

- Competitive Interest Rates: Navy Federal consistently offers some of the most attractive interest rates in the market. This can translate into significant savings over the life of your loan, reducing your monthly payments and the total cost of your vehicle.

- Flexible Loan Terms: Whether you prefer a shorter term to pay off your loan faster or a longer term to reduce monthly payments, Navy Federal provides a variety of options. They work with you to find a repayment schedule that fits your budget and financial goals.

- Exceptional Member Service: From the initial inquiry to the final signing, Navy Federal’s team is renowned for its helpfulness and expertise. They are committed to guiding you through every step, answering your questions, and ensuring you feel comfortable and informed.

- Streamlined Pre-Approval Process: Getting pre-approved with Navy Federal is a straightforward process that empowers you with negotiating power at the dealership. It allows you to shop for your car with a clear understanding of your budget and approved loan amount.

- No Hidden Fees: Transparency is a cornerstone of Navy Federal’s operations. You won’t encounter unexpected application fees or hidden charges, ensuring clarity and peace of mind throughout your loan journey.

- Support for Various Credit Profiles: While a strong credit score is always beneficial, Navy Federal is often more understanding and willing to work with members who might have less-than-perfect credit. They look at your overall financial picture, not just a single number.

These benefits make Navy Federal an incredibly attractive option, especially for those who qualify for membership. Let’s explore that crucial first step.

Unlocking the Door: Navy Federal Membership Eligibility

The very first step to getting a car loan with Navy Federal is, naturally, becoming a member. Unlike traditional banks, credit unions serve a specific field of membership. Fortunately, Navy Federal’s eligibility is quite broad, encompassing a significant portion of the military and their families.

You are eligible to join Navy Federal Credit Union if you are:

- Active Duty, Retired, or Veteran: All branches of the U.S. Armed Forces, including the Army, Marine Corps, Navy, Air Force, Coast Guard, and Space Force, are eligible. This includes reservists and National Guard members.

- Department of Defense (DoD) Civilians: DoD civilian employees, including contractors and civil service employees, are also eligible.

- Family Members: This is where eligibility extends significantly. Spouses, parents, grandparents, siblings, children, grandchildren, and even household members of current Navy Federal members are often eligible to join.

The membership process itself is typically straightforward and can be completed online, over the phone, or at a branch. You’ll need to provide some personal information and make a small initial deposit into a savings account, usually just $5. Once you’re a member, a world of financial products and services, including their highly-rated auto loans, becomes available to you.

Preparing for Success: Key Prerequisites for a Navy Federal Car Loan

Securing a car loan isn’t just about filling out an application; it’s about presenting yourself as a reliable borrower. Navy Federal, like any lender, will assess your financial health to determine your eligibility and the terms of your loan. Understanding these prerequisites and preparing accordingly can significantly improve your chances of approval and help you secure the best possible rates.

-

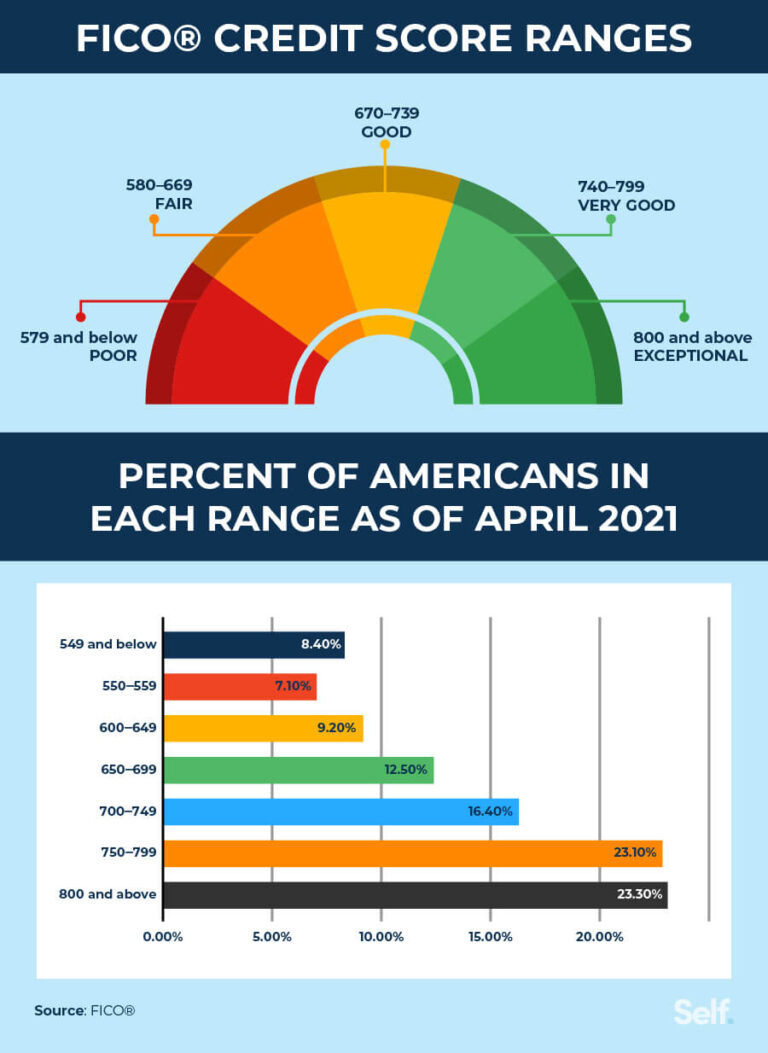

Your Credit Score: The Financial Report Card

Your credit score is a numerical representation of your creditworthiness. It tells lenders how responsibly you’ve managed credit in the past. While Navy Federal is often more flexible than other lenders, a strong credit score is your biggest asset.- What’s a "Good" Score? Generally, FICO scores above 700 are considered good, with 750+ being excellent. However, you can still get approved with scores in the mid-600s, though your interest rate might be higher.

- How to Check: You can obtain your credit report for free once a year from each of the three major credit bureaus (Experian, Equifax, TransUnion) at AnnualCreditReport.com. Reviewing it for errors is a pro tip from us – mistakes can unfairly lower your score.

- Improving Your Score: If your score needs a boost, focus on paying bills on time, reducing credit card balances, and avoiding opening too many new credit accounts simultaneously. Consistency is key to long-term credit health.

-

Debt-to-Income Ratio (DTI): A Measure of Affordability

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to take on additional debt.- Understanding DTI: If your total monthly debt payments (including existing loans, credit card minimums, and the prospective car payment) are $1,500 and your gross monthly income is $4,000, your DTI is 37.5% ($1,500 / $4,000).

- What Lenders Prefer: Most lenders prefer a DTI ratio below 43%, with lower being better. A high DTI suggests you might be stretched too thin financially, making it riskier to approve another loan.

- Lowering Your DTI: Prioritize paying down existing debts, especially high-interest credit cards, before applying for a car loan. This demonstrates financial discipline and frees up more of your income.

-

Stable Income and Employment History:

Lenders want assurance that you have a consistent source of income to make your loan payments. A stable employment history, typically 1-2 years with the same employer or in the same field, is highly favorable. If you’ve recently started a new job, be prepared to explain the circumstances, especially if it’s a promotion or a career advancement. -

The Value of a Down Payment:

While not always strictly required, making a down payment on your car loan offers several significant advantages.- Lower Loan Amount: A down payment reduces the principal amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan.

- Improved Loan-to-Value (LTV): LTV compares the loan amount to the car’s value. A lower LTV makes you a less risky borrower in the eyes of the lender.

- Better Rates: Lenders often offer better interest rates to borrowers who make a substantial down payment, as it demonstrates your commitment and reduces their risk.

- Protection Against Negative Equity: Cars depreciate rapidly. A down payment helps prevent you from owing more on your car than it’s worth, a situation known as being "upside down" or having "negative equity."

By addressing these prerequisites proactively, you’ll not only strengthen your application but also set yourself up for a more favorable and affordable car loan with Navy Federal.

Your Roadmap to Approval: The Step-by-Step Navy Federal Car Loan Process

Getting a car loan with Navy Federal is a structured process designed to be as straightforward as possible for members. By following these steps, you can navigate the application with confidence and efficiency.

Step 1: Confirm Your Navy Federal Membership & Eligibility

As we discussed, this is the foundational step. If you’re not already a member, take the time to determine your eligibility and complete the membership application. It’s a quick process that opens the door to all of NFCU’s benefits. Ensure your contact information and personal details are up-to-date with the credit union.

Step 2: Assess Your Financial Health and Credit Standing

Before you even think about cars, take a critical look at your finances.

- Get Your Credit Reports: Request your free credit reports from AnnualCreditReport.com. Scrutinize them for any inaccuracies or fraudulent activity. If you find errors, dispute them immediately.

- Understand Your Credit Score: Use a reliable source to check your FICO score. Many credit card companies and banks now offer free credit score access. Knowing your score gives you a realistic expectation of the rates you might qualify for.

- Calculate Your DTI: Gather all your monthly debt obligations (mortgage/rent, student loans, credit card minimums, etc.) and compare them to your gross monthly income. This will give you a clear picture of your capacity for a new car payment. If your DTI is high, consider paying down some existing debts first.

Step 3: Determine Your Realistic Budget

This step goes beyond just the car payment. A common mistake to avoid is focusing solely on the monthly loan payment without considering the total cost of car ownership.

- Calculate Total Ownership Costs: Factor in insurance premiums (which can vary significantly based on the car, your driving history, and location), fuel costs, maintenance, registration fees, and potential repair costs, especially for used vehicles.

- Set a Max Loan Amount: Based on your DTI, income, and other expenses, determine the maximum loan amount you are truly comfortable with. Remember, just because you’re approved for a certain amount doesn’t mean you have to spend it all.

Step 4: Get Pre-Approved with Navy Federal (Highly Recommended)

This is a game-changer in the car buying process. Pre-approval means Navy Federal has reviewed your financial information and tentatively approved you for a specific loan amount at a particular interest rate, before you even choose a car.

- How it Works: You’ll apply for pre-approval through Navy Federal’s website, mobile app, or by calling them directly. You’ll provide income details, employment history, and authorize a credit check.

- Benefits of Pre-Approval:

- Empowered Negotiation: You walk into the dealership as a cash buyer, knowing exactly how much you can spend. This shifts the focus from financing to the vehicle price itself, often leading to better deals.

- Clear Budget: You know your financial limits upfront, preventing you from falling in love with a car outside your budget.

- Faster Purchase: The financing is already largely in place, speeding up the actual purchase process at the dealership.

- Rate Lock: Often, Navy Federal will lock in your pre-approved rate for a certain period (e.g., 30-60 days), protecting you from potential rate increases.

Step 5: Shop for Your Vehicle

With your pre-approval in hand, you’re ready to find your perfect car.

- New vs. Used: Consider the pros and cons of each. New cars come with warranties and the latest features but depreciate quickly. Used cars offer better value but might require more maintenance. Navy Federal offers loans for both.

- Research & Compare: Use online resources to research different makes and models, read reviews, and compare prices. Sites like Kelley Blue Book (KBB) or Edmunds are invaluable for this.

- Test Drive: Always test drive any vehicle you’re seriously considering. Pay attention to comfort, handling, and any unusual noises.

- Negotiate Like a Pro: Armed with your pre-approval, focus on negotiating the vehicle’s purchase price, not the monthly payment. Remember, you can always walk away if the deal isn’t right. Pro tips from us: always be prepared to say no, and don’t be afraid to compare offers from different dealerships.

Step 6: Finalize Your Loan and Purchase

Once you’ve chosen your vehicle and negotiated a price, it’s time to finalize the loan with Navy Federal.

- Provide Vehicle Details: You’ll provide Navy Federal with the vehicle’s specific information (VIN, make, model, year, mileage). They will verify its value.

- Required Documents: Be ready to provide any additional documents requested, such as proof of income, proof of insurance, and the purchase agreement from the dealership.

- Review Loan Documents: Carefully read all loan documents before signing. Ensure the interest rate, loan term, and all fees match what you were quoted. If anything is unclear, ask questions.

- Sign and Drive: Once everything is in order, sign the paperwork, and you’ll be the proud owner of your new car! Navy Federal can often send funds directly to the dealership or provide you with a check.

This structured approach, especially utilizing the pre-approval process, significantly streamlines your car buying experience and puts you in a position of strength.

Key Factors Influencing Your Navy Federal Car Loan Rate

While Navy Federal strives to offer excellent rates, the specific interest rate you receive will depend on several factors unique to your situation and the vehicle you’re purchasing. Understanding these can help you optimize your application.

- Your Credit Score: This is arguably the most significant factor. Borrowers with higher credit scores typically qualify for the lowest interest rates because they are considered less risky.

- Loan Term (Length of the Loan): Shorter loan terms (e.g., 36 or 48 months) usually come with lower interest rates than longer terms (e.g., 60 or 72 months). While longer terms mean lower monthly payments, you’ll pay more interest over the life of the loan.

- Vehicle Age and Mileage: New cars generally qualify for lower rates than used cars. For used cars, very old vehicles or those with exceptionally high mileage might be subject to slightly higher rates or specific lending criteria due to perceived higher risk of mechanical issues.

- Loan-to-Value (LTV) Ratio: This ratio compares the amount you borrow to the car’s appraised value. A lower LTV (meaning you’re borrowing less relative to the car’s value, often due to a larger down payment) can result in a better interest rate.

- Down Payment Amount: As mentioned earlier, a substantial down payment reduces the amount you need to finance, lowering the lender’s risk and potentially earning you a better rate.

Common Mistakes to Avoid When Getting a Car Loan

Even with the best intentions, it’s easy to make missteps during the car loan process. Being aware of these common pitfalls can save you time, money, and stress.

- Not Checking Your Credit Beforehand: Failing to review your credit report and score can lead to unpleasant surprises. You might discover errors or realize your score isn’t where you thought it was, impacting your loan terms.

- Applying to Too Many Lenders: While it’s good to compare offers, submitting multiple loan applications within a short period can lead to several "hard inquiries" on your credit report. Too many hard inquiries can temporarily lower your credit score. Stick to a few trusted lenders like Navy Federal.

- Buying More Car Than You Can Afford: It’s tempting to stretch your budget for a nicer car, but this can lead to financial strain down the road. Stick to your pre-determined budget, considering all ownership costs.

- Skipping Pre-Approval: Going to a dealership without pre-approval puts you at a disadvantage. You’re negotiating blindly and giving the dealership control over the financing, which might not be in your best interest.

- Focusing Only on the Monthly Payment: Dealers often try to distract you by focusing solely on a "manageable" monthly payment. This can obscure a higher purchase price, a longer loan term, or a higher interest rate. Always focus on the total cost of the car and the total cost of the loan.

- Ignoring the Fine Print: Common mistakes to avoid include not thoroughly reading the loan agreement. Pay close attention to the interest rate, loan term, any fees, and prepayment penalties (though Navy Federal typically doesn’t have these for auto loans). If something isn’t clear, ask for clarification.

Pro Tips for a Smooth Navy Federal Car Loan Experience

To truly maximize your experience and ensure a hassle-free process, consider these expert tips:

- Maintain Open Communication: If you encounter any issues or have questions during the application or while shopping, don’t hesitate to contact Navy Federal directly. Their member service is a valuable resource.

- Consider Refinancing: If interest rates drop significantly after you’ve secured your loan, or if your credit score improves considerably, Navy Federal allows you to refinance your existing auto loan. This could lead to a lower interest rate and reduced monthly payments. It’s always worth checking if you can save money.

- Utilize Navy Federal’s Online Resources: Their website and mobile app offer a wealth of tools, including payment calculators, articles on car buying, and easy access to your loan details. Make the most of these digital conveniences.

- Explore Auto Buying Services: Navy Federal often partners with auto buying services (like TrueCar) that can help you find vehicles and negotiate prices, sometimes even offering additional discounts for members.

- Don’t Forget About Insurance: Get insurance quotes before finalizing your car purchase. The type of vehicle can significantly impact your premiums. Navy Federal may also offer insurance products or partner with providers. For more details on managing your finances, check out our guide on Budgeting for Your First Car (Internal Link Placeholder).

- Understand Loan Protection Options: Navy Federal may offer options like Guaranteed Asset Protection (GAP) insurance or Payment Protection. While these are optional, understand what they cover and if they are right for your situation before adding them to your loan.

- Review Your Credit Regularly: Even after approval, continue to monitor your credit score and report. This practice is crucial for overall financial health and will serve you well for future financial endeavors. Learn more about improving your credit score in our detailed article: How to Boost Your Credit Score for Better Loan Rates (Internal Link Placeholder).

Frequently Asked Questions (FAQs) About Navy Federal Car Loans

We’ve covered a lot of ground, but you might still have some specific questions. Here are answers to some of the most common inquiries regarding Navy Federal auto loans:

Q1: Can I get a Navy Federal car loan with bad credit?

A: While a higher credit score will always yield better rates, Navy Federal is often more willing to work with members who have less-than-perfect credit than traditional banks. They consider your overall financial picture, including your membership history, income stability, and DTI. It’s always best to apply and discuss your options directly with them. They might offer a loan with a slightly higher interest rate or suggest ways to improve your credit first.

Q2: How long does Navy Federal pre-approval last?

A: Typically, a Navy Federal pre-approval is valid for 30 to 60 days. This gives you ample time to shop for a vehicle without feeling rushed. Always confirm the exact duration of your pre-approval when you receive it. If it expires, you can usually reapply.

Q3: Can I use a Navy Federal auto loan for a private party sale?

A: Yes, Navy Federal offers auto loans for both new and used vehicles purchased from dealerships and for private party sales. The process might involve a few extra steps for private sales, such as verifying the vehicle’s title and condition, but it’s a common and straightforward option. You’ll need to provide details about the seller and the vehicle for them to process the loan.

Q4: What documents do I need to apply for a Navy Federal car loan?

A: While the exact requirements can vary slightly, you’ll generally need:

- Proof of Navy Federal membership.

- Government-issued ID (driver’s license).

- Social Security Number.

- Proof of income (pay stubs, tax returns, W-2s).

- Employment information.

- Details of the vehicle you intend to purchase (if you’re not pre-approved yet, you’ll provide this later).

It’s always a good idea to have these documents ready to expedite the application process.

Q5: Does Navy Federal offer rate discounts?

A: Yes, Navy Federal often offers rate discounts for various reasons. These can include discounts for setting up automatic payments from a Navy Federal checking account, or for using their car buying service partners. Always ask about current discount opportunities when you apply. You can also explore their official auto loan page for the most current offerings and rates: Navy Federal Auto Loans (External Link Placeholder).

Driving Forward with Confidence

Getting a car loan with Navy Federal offers a unique blend of competitive rates, flexible terms, and unparalleled member service, making it an excellent choice for those who qualify. By understanding the membership requirements, preparing your finances, leveraging the power of pre-approval, and navigating the process strategically, you can secure the best possible loan and drive away in your desired vehicle with peace of mind.

Remember, this journey is about more than just a car; it’s about making a sound financial decision. With Navy Federal as your partner, you’re well-equipped to make that decision with confidence and clarity. Start your application today and embark on the road to car ownership with a trusted financial ally.