Navigate Your Dream Car Purchase: The Ultimate Guide to Navy Federal Car Loan Prequalification

Navigate Your Dream Car Purchase: The Ultimate Guide to Navy Federal Car Loan Prequalification Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone, but the financing aspect can often feel daunting. For military members, veterans, and their families, Navy Federal Credit Union stands out as a trusted financial partner. Their car loan options are renowned for competitive rates and member-centric service. The smartest way to approach a car purchase with Navy Federal, or any lender, is through Navy Federal Car Loan Prequalification.

This comprehensive guide will demystify the prequalification process, showing you exactly how it empowers you as a buyer. We’ll delve deep into what prequalification means, why it’s a game-changer, and how to navigate each step to secure the best possible financing. Get ready to transform your car buying experience from stressful to seamless!

Navigate Your Dream Car Purchase: The Ultimate Guide to Navy Federal Car Loan Prequalification

What Exactly is Car Loan Prequalification, and Why Does It Matter?

Before we dive into the specifics of Navy Federal, let’s clarify what prequalification entails. Many people confuse prequalification with pre-approval, but there’s a distinct difference. Prequalification is an initial, informal assessment of your creditworthiness based on information you provide. It gives you an estimate of how much you might be able to borrow and at what interest rate, all without a hard inquiry on your credit report.

This preliminary step is incredibly valuable. It acts as a financial compass, guiding your car search by establishing a realistic budget. You’ll walk into dealerships with confidence, knowing your approximate borrowing power before you even set foot on the lot.

On the other hand, pre-approval involves a more thorough review, including a hard credit inquiry, and results in a conditional offer for a specific loan amount and rate. While pre-approval is closer to a guaranteed loan, prequalification serves as the crucial first step, giving you an excellent head start without impacting your credit score.

Why Choose Navy Federal for Your Auto Loan? A Member-Centric Advantage

For those eligible for membership, Navy Federal Credit Union offers a compelling package for auto financing. Their commitment to serving the military community translates into unique benefits that often surpass those of traditional banks.

First and foremost, Navy Federal consistently offers competitive interest rates. As a not-for-profit credit union, their primary focus is returning value to members, which often means lower rates and fewer fees compared to commercial lenders. This can translate into significant savings over the life of your car loan.

Beyond rates, their member service is exceptional. Based on my experience and countless member testimonials, Navy Federal’s loan officers are known for their helpfulness and understanding of the unique financial situations of military families. They offer personalized guidance, making the financing process less intimidating.

They also provide a variety of loan options, whether you’re buying new, used, or looking to refinance. This flexibility ensures that no matter your car buying scenario, Navy Federal likely has a product that fits your needs. Opting for Navy Federal Car Loan Prequalification is the ideal first step to unlock these member-exclusive advantages.

The Step-by-Step Guide to Navy Federal Car Loan Prequalification

Navigating the prequalification process with Navy Federal is straightforward once you understand the requirements and steps involved. Here’s a detailed breakdown:

Step 1: Ensure Membership Eligibility

The very first prerequisite for any Navy Federal service, including car loan prequalification, is membership. Navy Federal serves a specific demographic:

- All branches of the armed forces (Army, Marine Corps, Navy, Air Force, Coast Guard, Space Force).

- Veterans, retirees, and annuitants.

- Department of Defense (DoD) civilian personnel.

- And, significantly, their family members, including parents, grandparents, spouses, siblings, children, and grandchildren.

If you or a family member falls into one of these categories, you’re likely eligible. You can easily check your eligibility and join online, by phone, or in person at a branch. This foundational step is non-negotiable before you can proceed with any loan application.

Step 2: Gather Your Financial Information

Before you start the prequalification process, it’s wise to have your financial ducks in a row. While prequalification is less intensive than a full application, having key information readily available will streamline the process. You’ll typically need:

- Income Details: Your gross monthly income, employment history, and employer information. This helps Navy Federal assess your ability to repay the loan.

- Existing Debts: A general understanding of your current monthly debt obligations, such as credit card payments, student loans, or mortgages. This contributes to your debt-to-income (DTI) ratio, a crucial factor.

- Housing Information: Whether you rent or own, and your monthly housing payment.

Based on my experience, having these documents and figures handy, even if approximate for prequalification, makes the initial conversation or online form much smoother. It shows preparedness and can speed up the estimated offer.

Step 3: Understand Your Credit Score and Its Impact

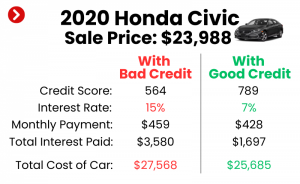

Your credit score is a numerical representation of your creditworthiness, and it significantly influences the interest rate you’ll be offered. For car loans, lenders typically look at scores from all three major credit bureaus (Equifax, Experian, TransUnion).

- Excellent Credit (780+): Likely to receive the best interest rates.

- Good Credit (670-739): Still qualifies for competitive rates.

- Fair Credit (580-669): May qualify, but with higher interest rates.

- Poor Credit (below 580): Approval might be challenging, or rates will be substantially higher.

Pro tips from us: Regularly check your credit report for accuracy through AnnualCreditReport.com. Dispute any errors immediately. Knowing your score beforehand helps set realistic expectations for your Navy Federal Car Loan Prequalification offer. If your score is lower than you’d like, consider taking steps to improve it before applying, such as paying down existing debt or avoiding new credit inquiries.

Step 4: The Prequalification Application Process

Navy Federal offers several convenient ways to prequalify for a car loan:

- Online: This is often the quickest and most popular method. You’ll fill out a simple online form with your basic financial information.

- By Phone: You can call their member service line and speak with a representative who will guide you through the questions.

- In-Branch: Visit a Navy Federal branch to speak with a loan officer in person.

During this process, Navy Federal will ask for details like your desired loan amount, the type of car (new or used), and your income and debt information. Crucially, prequalification typically involves a soft credit inquiry, which does not impact your credit score. This is a significant advantage, allowing you to explore your options without any negative repercussions.

Step 5: Reviewing Your Prequalification Offer

Once you submit your information, Navy Federal will provide you with an estimated loan amount and interest rate. This offer is not a firm commitment but a strong indicator of what you can expect if you proceed with a full application.

- Understand the Terms: Pay close attention to the estimated interest rate and the maximum loan amount. This forms the basis of your car buying budget.

- It’s an Estimate: Remember, the final rate and loan amount can vary slightly based on the full application, which involves a hard credit pull and verification of all your financial details. However, the prequalification offer gives you a very solid baseline.

This estimated offer is your golden ticket. It empowers you to shop for a car with a clear financial boundary, preventing you from falling in love with a vehicle outside your means.

Maximizing Your Chances of Navy Federal Car Loan Approval

While prequalification gives you an estimate, turning that into a full approval for a great rate requires a bit more strategic planning. Here’s how to put yourself in the best position:

Boost Your Credit Score

A higher credit score invariably leads to better loan terms. Before you apply for the full loan:

- Pay Bills On Time: Payment history is the biggest factor in your credit score.

- Reduce Credit Card Balances: Aim to keep credit utilization below 30% of your available credit.

- Avoid New Debt: Don’t open new credit lines or make large purchases on existing ones.

- Check for Errors: Regularly review your credit report for inaccuracies that could be dragging your score down.

Reduce Your Debt-to-Income (DTI) Ratio

Your DTI ratio is the percentage of your gross monthly income that goes towards debt payments. Lenders prefer a lower DTI, typically below 43%.

- Pay Down Existing Debts: Prioritize paying off high-interest debts like credit cards.

- Increase Income: If possible, look for ways to boost your income.

A lower DTI signals to Navy Federal that you have ample disposable income to comfortably manage your car loan payments.

Increase Your Down Payment

A larger down payment reduces the amount you need to borrow, which can lead to:

- Lower Monthly Payments: Less principal means smaller installments.

- Reduced Interest Paid: You’re borrowing less, so you pay less interest over time.

- Better Loan-to-Value (LTV) Ratio: Lenders see less risk when the loan amount is significantly less than the car’s value.

Even a modest down payment can make a difference in your final loan terms.

Consider a Co-signer (If Necessary)

If your credit score is fair or you have a limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and secure a better interest rate.

- Choose Wisely: A co-signer is equally responsible for the loan, so ensure it’s someone you trust and who understands the commitment.

- Only If Needed: This should be a last resort, as it places a financial burden on another individual.

Common mistakes to avoid are applying for multiple types of credit simultaneously, making late payments just before applying, or underestimating your current debt obligations. Being transparent and proactive about your financial health will serve you best.

What Happens After Prequalification? The Next Steps

Congratulations, you’ve received your Navy Federal Car Loan Prequalification offer! What now? This is where the real power of prequalification comes into play, transforming your car buying experience.

Shopping with Confidence

With your estimated loan amount and interest rate in hand, you can confidently shop for a vehicle within your budget. You know your financial limits, so you won’t waste time on cars you can’t afford. This knowledge also equips you to negotiate with dealerships more effectively.

Transitioning to Full Pre-Approval/Application

Once you’ve found the perfect car, the next step is to move from prequalification to a full loan application. This will involve:

- Specific Car Details: Providing Navy Federal with the exact make, model, year, and VIN of the vehicle you intend to purchase.

- Hard Credit Inquiry: At this stage, Navy Federal will perform a hard credit pull, which will temporarily ding your credit score by a few points. However, multiple hard inquiries for the same type of loan within a short window (typically 14-45 days) are often treated as a single inquiry, so don’t hesitate to shop for rates once you’re serious.

- Income and Employment Verification: You may need to provide pay stubs, W-2s, or other documents to verify your income and employment.

This step is where your estimated offer becomes a firm commitment, provided all information checks out.

Finalizing the Loan

Once approved, Navy Federal will provide you with all the final loan documents. You’ll review and sign these, and the funds will be disbursed directly to the dealership or to you, depending on the arrangement. This seamless process allows you to drive away in your new car without the last-minute stress of securing financing at the dealership.

Based on my years in the auto financing world, having your prequalification letter in hand changes the dynamic significantly. Dealerships know you’re a serious buyer with financing already secured, which often leads to a more straightforward and less pressured negotiation process.

Pro Tips for a Smooth Car Buying Journey with Navy Federal

Beyond the prequalification process, a few additional strategies can ensure your overall car buying experience is as smooth as possible.

Negotiate Like a Pro

Your prequalification offer gives you leverage. Don’t be afraid to negotiate the car’s price. You know your financing is secured elsewhere, so you can focus solely on getting the best deal on the vehicle itself. If the dealership tries to offer their own financing, you can compare it directly to your Navy Federal offer.

Don’t Forget Insurance

Before you drive off the lot, ensure you have adequate car insurance. Most lenders, including Navy Federal, require comprehensive and collision coverage for the duration of the loan. Get quotes from several providers to find the best rate.

Read the Fine Print

Always, always read all loan documents carefully before signing. Understand the interest rate, the total amount you’ll pay, any fees, and the repayment schedule. If anything is unclear, ask questions until you’re completely satisfied. Transparency is key to a good financial decision.

Consider GAP Insurance

Guaranteed Asset Protection (GAP) insurance can be a smart addition, especially for new cars. If your car is totaled or stolen, GAP insurance covers the difference between what your insurance company pays out (actual cash value) and the remaining balance on your loan. This prevents you from being upside down on your loan.

Frequently Asked Questions (FAQs) About Navy Federal Car Loan Prequalification

Let’s address some common questions to further clarify the process.

1. Is Navy Federal membership required for car loan prequalification?

Yes, absolutely. You must be a member of Navy Federal Credit Union to utilize any of their financial products, including car loans and the prequalification service. Eligibility is open to military members, veterans, DoD civilians, and their families.

2. Does prequalification hurt my credit score?

No, Navy Federal Car Loan Prequalification typically involves a "soft" credit inquiry, which does not negatively impact your credit score. A "hard" inquiry only occurs if you proceed with a full loan application.

3. How long is a prequalification offer valid?

The validity period for a prequalification offer can vary. It’s usually a good idea to act on it within a reasonable timeframe, often 30-60 days, as market rates and your financial situation can change. Always confirm the exact expiration with Navy Federal.

4. Can I prequalify for a used car loan through Navy Federal?

Yes, Navy Federal offers prequalification for both new and used car loans. The terms and rates might differ slightly depending on the age and mileage of the used vehicle, but the process remains the same.

5. What if I don’t get the rate I expected?

If your prequalification offer isn’t as favorable as you hoped, don’t despair. Review your credit report for any errors, consider improving your credit score, increasing your down payment, or exploring the option of a co-signer. You can also re-apply for prequalification after making improvements to your financial profile.

6. Can I use my Navy Federal prequalification offer at any dealership?

Yes, your Navy Federal prequalification (and subsequent pre-approval) gives you the flexibility to shop at any dealership. You are not tied to a specific dealer’s financing. This empowers you to negotiate the best vehicle price independently of the financing.

Conclusion: Empower Your Car Purchase with Navy Federal Prequalification

Embarking on the car buying journey can be incredibly rewarding, especially when you feel confident and prepared. Navy Federal Car Loan Prequalification is not just a preliminary step; it’s a strategic advantage that puts you in the driver’s seat of your financial future. By understanding your borrowing power upfront, you gain the clarity, confidence, and negotiating leverage needed to secure the best deal on your dream car.

For eligible members, Navy Federal offers a powerful combination of competitive rates, dedicated service, and a straightforward process. Take the first step today: explore your prequalification options with Navy Federal and transform your car buying experience from a guessing game into a well-executed plan. Your next vehicle awaits, and with Navy Federal by your side, you’re ready for the road ahead.