Navigate Your Drive: Mastering the Navy Federal Car Loan Calculator for a Smarter Purchase

Navigate Your Drive: Mastering the Navy Federal Car Loan Calculator for a Smarter Purchase Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone, but it’s also a significant financial decision. For many, securing the right auto loan is a crucial step in this journey. If you’re a service member, veteran, or part of the Department of Defense community, Navy Federal Credit Union stands out as a highly respected and reliable option. But simply knowing about Navy Federal isn’t enough; truly optimizing your car purchase means understanding and leveraging their powerful financial tools.

This comprehensive guide will dive deep into the Navy Federal Car Loan Calculator, an indispensable resource designed to empower you with clarity and confidence. We’re not just scratching the surface; we’re exploring every facet of this tool, how it works, why it matters, and how to use it to secure the best possible deal. Our goal is to equip you with the knowledge to make informed decisions, ensuring your car buying experience is smooth, transparent, and financially sound.

Navigate Your Drive: Mastering the Navy Federal Car Loan Calculator for a Smarter Purchase

Understanding the Power of the Navy Federal Car Loan Calculator

In today’s complex financial landscape, knowledge truly is power. A car loan calculator isn’t just a simple math tool; it’s a strategic planner for your automotive dreams. It helps demystify the numbers behind your car purchase, transforming vague ideas into concrete financial projections. This foresight is critical for responsible budgeting and preventing future financial stress.

What makes Navy Federal unique in this context? As a credit union, Navy Federal operates with a member-first philosophy, often translating into more competitive rates and flexible terms compared to traditional banks. Their commitment to the military community also means a deep understanding of their members’ unique financial situations. The Navy Federal Car Loan Calculator brings this ethos directly to your fingertips, allowing you to explore these member-exclusive benefits with ease.

Ultimately, the calculator serves as your personal financial simulator. It allows you to adjust various parameters – such as loan amount, interest rates, and repayment terms – to see how each change impacts your potential monthly payment and the total cost of your loan. This proactive approach ensures you enter the dealership armed with a clear understanding of what you can comfortably afford, putting you in a stronger negotiating position.

Who Can Benefit from Navy Federal’s Auto Loans? (Membership Eligibility)

Before you even touch the calculator, it’s essential to understand if you’re eligible to join the Navy Federal family. Their exclusive membership is a cornerstone of their service, and access to their competitive auto loans, including the calculator, hinges on meeting specific criteria. This isn’t just a formality; it’s the gateway to a world of financial advantages tailored for those who serve or have served.

Membership is primarily open to individuals who have a connection to the armed forces. This includes all active duty members of the Army, Marine Corps, Navy, Air Force, Coast Guard, and Space Force. Furthermore, veterans, retirees, and annuitants of these branches are also eligible, honoring their service with continued access to beneficial financial products.

Beyond active service and veteran status, Department of Defense (DoD) civilians, contractors, and their families can also qualify. This extensive reach ensures that a broad segment of the military community and its support system can benefit. If you have immediate family members – such as parents, grandparents, spouses, siblings, children, or even household members – who are already Navy Federal members, you might also be eligible to join through their existing membership.

Verifying your eligibility is the foundational step. Once you confirm your connection, becoming a member is a straightforward process, typically involving a small initial deposit. This step unlocks not only the car loan calculator but also a full suite of financial products and services designed with your unique needs in mind.

Diving Deep: How the Navy Federal Car Loan Calculator Works

The Navy Federal Car Loan Calculator is more than just an input-output tool; it’s a dynamic simulator that helps you dissect the complexities of an auto loan. To truly master it, you need to understand each component and how it influences your overall loan structure. Let’s break down the key variables you’ll encounter and manipulate.

Understanding the Key Variables

1. Loan Amount: This is the total sum you intend to borrow after factoring in any down payment or trade-in value. It represents the purchase price of the vehicle minus your upfront contributions. Be realistic about the car’s actual cost, including potential taxes and fees, to ensure your loan amount is accurate.

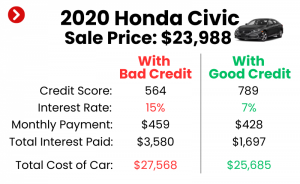

2. Interest Rate (APR): The Annual Percentage Rate (APR) is arguably the most critical factor. It’s the cost of borrowing money, expressed as a percentage of the loan amount over a year. Your credit score, the loan term, the vehicle’s age (new vs. used), and current market conditions all play a significant role in determining the APR you’ll be offered. A lower APR translates to less interest paid over the life of the loan.

3. Loan Term: This refers to the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or 84 months). A shorter loan term means higher monthly payments but significantly less total interest paid. Conversely, a longer term offers lower monthly payments, making the car seem more affordable, but you’ll end up paying substantially more in interest over time.

4. Down Payment: This is the amount of money you pay upfront towards the purchase of the vehicle. A larger down payment reduces the total amount you need to borrow, which in turn lowers your monthly payments and the overall interest you’ll pay. It also signals to lenders that you’re a lower-risk borrower.

5. Trade-in Value: If you’re trading in your current vehicle, its estimated value can act similar to a down payment. This amount is subtracted from the car’s purchase price, reducing the principal loan amount. It’s wise to get an independent appraisal of your trade-in before heading to the dealership.

6. Sales Tax & Fees: Don’t forget these additional costs! Sales tax, registration fees, title fees, and documentation fees can add hundreds or even thousands to the total cost. While not always directly calculable within the loan itself, you need to factor these into your overall budget. Some lenders allow you to roll these into the loan, but it means borrowing more and paying interest on those amounts.

A Hypothetical Walkthrough

Imagine you’re eyeing a new car priced at $30,000. You have a $5,000 down payment and your credit score is excellent.

- Input Loan Amount: You’d start by entering $25,000 ($30,000 – $5,000).

- Estimate APR: Based on Navy Federal’s current rates for new cars and your excellent credit, you might estimate an APR of 3.5%.

- Choose Loan Term: You could try a 60-month term.

- Calculate: The calculator would instantly display your estimated monthly payment and the total interest paid over 60 months.

Now, you can experiment. What if you put down $8,000? Or extended the term to 72 months? The calculator will show you how these adjustments impact your monthly outlay and the final cost. This iterative process is where the true power of the tool lies, allowing you to fine-tune your financial strategy before committing.

Unlocking the Benefits: Why Choose Navy Federal for Your Auto Loan?

Beyond the mechanics of the calculator, understanding the intrinsic advantages of choosing Navy Federal for your auto loan can significantly enhance your car buying experience. Their unique position as a credit union serving the military community translates into tangible benefits that set them apart. Based on my experience in the financial sector, these advantages are consistently highlighted by their members.

1. Competitive Interest Rates: Navy Federal is renowned for offering some of the most competitive interest rates in the market. As a not-for-profit institution, their primary focus is returning value to their members, not maximizing shareholder profits. This often results in lower APRs, which can save you hundreds or even thousands of dollars over the life of your loan. Always check their current rates directly on their website, as they are updated regularly.

2. Flexible Loan Terms: They understand that one size doesn’t fit all when it comes to financing. Navy Federal offers a wide range of loan terms, from shorter periods like 36 months to extended terms of up to 84 months for qualified vehicles and borrowers. This flexibility allows you to tailor your monthly payments to fit your budget while still having options to minimize total interest paid.

3. Streamlined Pre-Approval Process: Getting pre-approved for an auto loan before you step foot in a dealership is a game-changer. Navy Federal’s pre-approval process is typically quick and straightforward, often done online or over the phone. A pre-approval letter gives you concrete buying power, transforming you into a cash buyer in the eyes of the dealer. This not only speeds up the purchasing process but also puts you in a much stronger position to negotiate the vehicle’s price, as you already have your financing secured.

4. Exceptional Member Service: Pro tips from us: The customer service at Navy Federal is consistently praised. Their representatives are often knowledgeable, empathetic, and dedicated to helping members understand their options. Whether you have questions about the calculator, the application process, or specific loan terms, you can expect clear and helpful guidance. This level of support adds significant value to your overall experience, especially for first-time car buyers.

5. No Hidden Fees: Transparency is a hallmark of Navy Federal’s operations. You won’t typically find unexpected application fees or prepayment penalties with their auto loans. This straightforward approach means you can budget with confidence, knowing exactly what you’re signing up for without any unpleasant surprises down the road.

6. Refinancing Options: If you already have an auto loan with another lender, Navy Federal also offers attractive refinancing options. If interest rates have dropped or your credit score has improved since you originally financed your car, refinancing through Navy Federal could significantly lower your monthly payments or reduce the total interest you’ll pay. This is a valuable tool for optimizing existing debt.

Pro Tips for Maximizing Your Car Loan Calculator Experience

To truly leverage the Navy Federal Car Loan Calculator, it’s not enough to just input numbers. You need a strategic approach that integrates financial planning with the tool’s capabilities. Based on my experience, these pro tips can transform your car buying journey.

1. Get Your Credit Score in Shape: Your credit score is the single most influential factor in determining the interest rate you’ll be offered. Before you even think about applying for a loan, check your credit report for any errors and work to improve your score. Pay down existing debts, make all payments on time, and avoid opening new lines of credit. A higher score translates directly to a lower APR, saving you substantial money.

2. Play with Different Scenarios: Don’t just run one calculation. The power of the calculator lies in its flexibility. Experiment with various down payment amounts, loan terms, and even hypothetical interest rates. See how a larger down payment impacts your monthly payment, or how extending the loan term by 12 months affects the total interest paid. This allows you to find the sweet spot between affordability and cost-efficiency.

3. Don’t Forget Additional Costs: While the calculator focuses on the loan itself, a car’s true cost extends beyond the purchase price. Factor in ongoing expenses like auto insurance, registration fees, routine maintenance, and fuel. A low monthly loan payment might seem appealing, but if other costs strain your budget, you could face financial difficulties. Budget holistically for your new vehicle.

4. Pre-Approval is Your Best Friend: Pro tips from us: Always get pre-approved before visiting a dealership. This critical step empowers you with a maximum loan amount and a confirmed interest rate. It gives you the confidence to negotiate the vehicle’s price as if you were a cash buyer, removing the uncertainty of financing from the negotiation table. Navy Federal’s pre-approval process is straightforward and highly beneficial.

5. Consider a Shorter Loan Term if Possible: While a longer loan term offers lower monthly payments, it invariably leads to paying significantly more in total interest. If your budget allows, opt for the shortest loan term you can comfortably afford. This strategy minimizes the amount of interest you accrue over time, getting you out of debt faster and saving you money in the long run.

6. Read the Fine Print: Once you receive a loan offer, whether from Navy Federal or another lender, meticulously read all the terms and conditions. Understand any potential fees, the exact APR, and the full repayment schedule. Don’t hesitate to ask questions if anything is unclear. Clarity on these details ensures there are no surprises after you’ve signed on the dotted line.

Common Mistakes to Avoid When Using a Car Loan Calculator

Even with the best tools, missteps can happen. Understanding common pitfalls when using a car loan calculator can save you from costly errors and buyer’s remorse. Based on my observations, these are frequently encountered mistakes that savvy buyers learn to circumvent.

1. Ignoring Your Credit Score: A prevalent mistake is to use the calculator with an assumed "average" interest rate without first understanding your own credit standing. The interest rate offered to you can vary wildly based on your credit score. Underestimating the impact of a poor or even fair credit score can lead to a significant discrepancy between your calculator’s estimate and the actual loan offer, causing budgeting issues.

2. Focusing Only on Monthly Payments: Many buyers fall into the trap of prioritizing the lowest possible monthly payment above all else. While an affordable monthly payment is important, it often comes at the cost of a longer loan term and, consequently, much higher total interest paid over the life of the loan. Always consider the total cost of the loan, not just the monthly outlay.

3. Not Accounting for a Down Payment: Failing to factor in a substantial down payment can inflate your perceived loan amount and monthly payments. A down payment directly reduces the principal you need to borrow, thereby decreasing your monthly payments and the total interest. Overlooking this crucial element can make an otherwise affordable car seem out of reach.

4. Skipping Pre-Approval: This is a critical error. Entering a dealership without pre-approval from a lender like Navy Federal means you’re negotiating on two fronts: the car’s price and the financing terms. This puts you at a disadvantage, as the dealer might focus on adjusting loan terms to make the car seem affordable, rather than offering their best price for the vehicle itself.

5. Forgetting About Insurance and Maintenance: Common mistakes to avoid are neglecting the full scope of car ownership costs. The calculator gives you a loan payment, but it doesn’t account for the mandatory expenses of car insurance, routine maintenance, and potential repairs. Budgeting solely based on the loan payment is a recipe for financial strain down the line.

6. Not Comparing Offers: Even with competitive lenders like Navy Federal, it’s always wise to compare at least a few loan offers. While Navy Federal often provides excellent rates, other institutions might have specific promotions or terms that could suit your unique situation better. A little comparison shopping can ensure you’re truly getting the best deal available to you.

Beyond the Calculator: The Navy Federal Auto Loan Application Process

Once you’ve mastered the calculator and feel confident in your budget, the next logical step is applying for your Navy Federal auto loan. The process is designed to be user-friendly, allowing you to move from estimation to realization smoothly.

1. Online Application: Navy Federal provides a convenient online application portal, allowing you to apply from the comfort of your home. The application will ask for personal details, employment information, and your financial history. It’s a secure process, ensuring your data is protected.

2. Required Documents: While applying, be prepared to provide certain documents. This typically includes proof of income (pay stubs, tax returns), identification (driver’s license, military ID), and potentially vehicle information if you’ve already chosen a specific car. Having these ready will expedite the process.

3. Decision & Funding: After submitting your application, Navy Federal will review your information and credit history. You’ll typically receive a decision relatively quickly, often within the same day for online applications. If approved, you’ll receive details about your loan, including the specific APR and terms. You can then use this pre-approval to finalize your car purchase, often with direct funding options available to the dealership.

Real-World Scenarios: Putting the Calculator to the Test

Let’s illustrate the Navy Federal Car Loan Calculator’s utility with a few practical examples. These scenarios highlight how the tool helps you visualize different financial outcomes.

Example 1: New Car Purchase with Excellent Credit

- Scenario: You want a new sedan costing $35,000. You have an excellent credit score (780+) and plan a $7,000 down payment.

- Calculator Input: Loan Amount: $28,000. Estimated APR (Navy Federal, excellent credit, new car): 3.29%. Loan Term: 60 months.

- Calculator Output: Estimated monthly payment: ~$507. Total interest paid: ~$2,420.

- Insights: A strong credit score and a good down payment result in an attractive interest rate and manageable total interest. Experimenting with a 72-month term might lower the monthly payment but increase total interest.

Example 2: Used Car Purchase with a Moderate Credit Score

- Scenario: You’re looking at a used SUV for $20,000. Your credit score is moderate (680), and you can put down $3,000.

- Calculator Input: Loan Amount: $17,000. Estimated APR (Navy Federal, moderate credit, used car): 6.49%. Loan Term: 60 months.

- Calculator Output: Estimated monthly payment: ~$331. Total interest paid: ~$2,860.

- Insights: A lower credit score and used car status lead to a higher APR. The calculator helps you see this impact clearly. You might consider a slightly longer term (e.g., 72 months) to reduce the monthly payment, but be aware of the increased total interest.

Example 3: Refinancing an Existing Loan

- Scenario: You currently have a $15,000 loan balance on your car at 9% APR for 48 months remaining. Your credit has improved, and Navy Federal offers you 4.5% APR.

- Calculator Input (New Loan): Loan Amount: $15,000. Estimated APR (Navy Federal, improved credit, refinance): 4.5%. Loan Term: 48 months.

- Calculator Output (New Loan): Estimated monthly payment: ~$342. Total interest paid: ~$1,420.

- Original Loan (Comparison): Original monthly payment: ~$373. Total interest remaining: ~$2,880.

- Insights: Refinancing through Navy Federal could save you around $31 per month and nearly $1,460 in total interest over the remaining loan term.

Frequently Asked Questions about Navy Federal Auto Loans

Here are some common questions prospective borrowers have about Navy Federal’s auto loan offerings:

Q: Can I get a Navy Federal auto loan if I’m not a member yet?

A: No, you must be a Navy Federal Credit Union member to apply for any of their loans, including auto loans. However, if you’re eligible, joining is a straightforward process.

Q: What credit score do I need for a Navy Federal auto loan?

A: While Navy Federal doesn’t publish a minimum score, generally, a higher credit score will qualify you for the best rates. Scores in the "good" to "excellent" range (typically 670+) are most favorable. They do consider various factors beyond just the score, however, reflecting their member-centric approach.

Q: Does Navy Federal offer loans for motorcycles or RVs?

A: Yes, Navy Federal offers financing for a wide range of vehicles, including new and used cars, trucks, motorcycles, boats, and RVs. The terms and rates may vary depending on the vehicle type.

Q: How long does the pre-approval last?

A: Navy Federal auto loan pre-approvals typically last for a specific period, often 45-60 days. This gives you ample time to find your desired vehicle without the pre-approval expiring. Always confirm the exact duration when you receive your pre-approval.

Conclusion

The Navy Federal Car Loan Calculator is far more than a simple online tool; it’s a gateway to informed decision-making and a smarter car purchase. For those eligible to join Navy Federal, it represents an invaluable resource in securing competitive financing, understanding your budget, and negotiating with confidence. By meticulously exploring loan amounts, interest rates, terms, and the impact of down payments, you transform a potentially daunting financial commitment into a transparent and manageable process.

Remember, the goal isn’t just to buy a car, but to buy it wisely. Leveraging the calculator, understanding Navy Federal’s unique benefits, and applying our pro tips will empower you to navigate the auto loan landscape with expertise. Take control of your car buying journey today by visiting Navy Federal’s website, using their calculator, and stepping into your next vehicle with complete financial clarity. Your future self, and your wallet, will thank you.