Navigate Your Next Car Loan: The Unseen Power of a Soft Inquiry (And How It Saves Your Credit Score!)

Navigate Your Next Car Loan: The Unseen Power of a Soft Inquiry (And How It Saves Your Credit Score!) Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, yet the financing aspect often brings a wave of anxiety. Will I qualify? What will my interest rate be? And perhaps the biggest question haunting credit-conscious consumers: Will simply checking my eligibility hurt my credit score?

This is where the often-misunderstood Car Loan Soft Inquiry enters the picture, acting as your financial crystal ball. As an expert in car financing, I’ve seen firsthand how a strategic understanding of soft inquiries can transform a stressful car-buying process into an empowering, confident journey. It’s a powerful tool that every prospective car buyer should master.

Navigate Your Next Car Loan: The Unseen Power of a Soft Inquiry (And How It Saves Your Credit Score!)

Understanding the Basics: What Exactly is a Car Loan Soft Inquiry?

Imagine you’re dipping your toe into the water before taking a full plunge. That’s precisely what a soft inquiry is for your credit. In the world of car loans, a soft inquiry is a preliminary check of your credit history that does not impact your credit score. It’s a way for lenders to get a quick, high-level snapshot of your financial reliability without leaving a mark on your credit report that other lenders can see or that affects your score.

This is a crucial distinction. Unlike a "hard inquiry," which occurs when you formally apply for credit and can temporarily lower your score by a few points, a soft inquiry is practically invisible to other lenders and credit scoring models. It allows you to explore your options, gauge your eligibility, and understand potential terms without any financial repercussions.

For car buyers, this is a game-changer. It means you can confidently shop around, compare pre-qualification offers from various lenders, and gain a clear understanding of your borrowing power long before you step onto a dealership lot or commit to a specific vehicle.

The "Why" Behind the Soft Check: Lenders’ Perspective

Why do lenders bother with soft inquiries if they don’t provide a full credit report? The answer lies in efficiency and risk management for both parties. From a lender’s viewpoint, soft inquiries serve as an excellent pre-screening mechanism. They allow financial institutions to quickly assess a potential borrower’s general creditworthiness.

This process helps lenders determine if a customer meets their basic lending criteria. They can then offer pre-qualification estimates or personalized rate quotes to individuals who are likely to be approved for a loan. This saves both the lender and the consumer valuable time, preventing full applications that might lead to a rejection.

Based on my experience, lenders use soft inquiries to generate qualified leads and tailor their marketing efforts. By knowing a consumer’s general credit profile, they can offer more relevant products and rates, increasing the likelihood of converting a browsing customer into a funded loan. It’s a smart business practice that ultimately benefits the consumer by streamlining the process.

How Does a Soft Inquiry Work? A Peek Behind the Curtain

So, how does this "invisible" credit check actually function? When you submit information for a soft inquiry – perhaps through an online pre-qualification form or by asking a dealership for an initial estimate – the lender accesses a limited version of your credit report. This isn’t the full, detailed report that a hard inquiry pulls.

Instead, they typically receive a summary that includes key information like your credit score range, public records, and general payment history. They’re looking for major red flags or clear indicators of strong credit. This brief overview helps them quickly determine if you fall within their lending parameters without needing to delve into every single account detail.

It’s important to understand that while a soft inquiry appears on your credit report, it’s only visible to you. No other lenders or creditors can see these inquiries, and credit scoring models like FICO and VantageScore do not factor them into your score calculation. This truly makes it a consequence-free way to explore your financing options.

The Consumer’s Advantage: Benefits of Using Soft Inquiries

For you, the car buyer, the benefits of leveraging soft inquiries are numerous and significant. Embracing this strategy can lead to a smoother, more informed, and ultimately more affordable car-buying experience.

No Impact on Your Credit Score

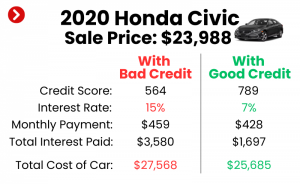

This is, without a doubt, the single biggest advantage. Unlike hard inquiries, which can temporarily ding your credit score by a few points, a soft inquiry leaves no trace. This means you can check your eligibility with multiple lenders without worrying about damaging your credit, which is especially beneficial if you’re close to a credit score threshold or planning other significant credit applications soon.

Stress-Free Shopping and Comparison

Imagine being able to shop for car loan rates like you shop for a new television – comparing features and prices without commitment. Soft inquiries make this a reality. You can gather pre-qualification offers from various banks, credit unions, and online lenders, giving you a clear picture of the best rates and terms available to you. This empowers you to make a truly informed decision, rather than settling for the first offer you receive.

Realistic Expectations and Budgeting

Knowing your potential interest rate and loan amount upfront allows you to set realistic expectations for your car purchase. You’ll understand what price range of vehicles you can comfortably afford, avoiding the disappointment of falling in love with a car that’s financially out of reach. This knowledge also helps you build a more accurate budget, factoring in your potential monthly car payments.

Empowerment in Negotiation

Armed with pre-qualification offers, you gain significant leverage at the dealership. You won’t be at the mercy of the dealership’s financing department. Instead, you can walk in knowing the rates you’ve been offered elsewhere, giving you a strong bargaining chip to secure the best possible deal – whether through the dealer or an external lender.

When Do Soft Inquiries Happen in Your Car Buying Journey?

Soft inquiries are integrated into several common steps of the car loan process, often without you even realizing it. Knowing when they occur can help you strategize your approach.

One of the most frequent instances is when you use online pre-qualification forms. Many bank websites, credit union portals, and even third-party auto loan aggregators offer tools to "check your rate" or "get pre-qualified" by simply entering some basic personal and financial information. These tools almost always initiate a soft inquiry.

Dealerships also utilize soft inquiries during their initial screening process. When you first sit down with a sales associate or finance manager and provide your basic information for an "estimate" or to see "what you qualify for," they might run a soft check. This helps them understand your credit tier before pulling a full report for a specific loan application. Recognizing these moments can help you confirm with the lender whether they are performing a soft or hard pull.

From Soft to Hard: The Transition to a Formal Application

While soft inquiries are incredibly useful for exploration, there comes a point in the car-buying process where a hard inquiry becomes necessary. This transition happens when you decide to move forward with a specific loan offer.

A hard inquiry is typically triggered when you submit a formal, full credit application with the explicit intent to obtain a loan. This occurs after you’ve chosen a vehicle, agreed on terms, and are ready to finalize the financing. At this stage, the lender needs a comprehensive view of your entire credit history, including all accounts, payment history, and any past inquiries.

Based on my experience, the temporary dip in your credit score from a hard inquiry is usually minor, often just a few points, and recovers within a few months. Furthermore, credit scoring models are designed to recognize "rate shopping" for specific types of loans, like mortgages and auto loans. Multiple hard inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are often counted as a single inquiry, minimizing the cumulative impact on your score. This allows you to compare final offers without significant credit damage.

Pro Tips from Our Experience: Maximizing Your Soft Inquiry Strategy

To truly harness the power of soft inquiries, a strategic approach is key. Here are some professional tips to guide you:

Shop Around Extensively Using Soft Inquiries

Don’t settle for the first pre-qualification offer you receive. Based on my experience in the industry, taking the time to gather offers from at least three to five different lenders—including traditional banks, credit unions, and online lenders—can reveal a significant difference in interest rates. Use those soft inquiry tools widely to cast a broad net.

Understand Your Credit Report Before You Start

Before even initiating your first soft inquiry, it’s a pro tip to pull your own credit report from each of the three major bureaus (Experian, Equifax, TransUnion). You are entitled to a free report annually from AnnualCreditReport.com. Review it for accuracy, identify any potential errors, and understand the factors influencing your score. This proactive step allows you to address discrepancies and improve your credit standing if needed, which can lead to better loan offers.

Be Honest and Consistent with Your Information

When filling out pre-qualification forms, ensure the information you provide is accurate and consistent across all lenders. Any discrepancies between your soft inquiry data and your actual credit report or personal details could lead to a different (and potentially less favorable) final offer when the hard inquiry is eventually performed. Accuracy from the start helps manage expectations.

Don’t Be Afraid to Ask Questions

Always confirm with a lender whether their pre-qualification or rate-check tool involves a soft or hard inquiry. While most online tools explicitly state "no credit impact," it’s always wise to clarify, especially if you’re dealing with a human representative. Being informed helps you maintain control over your credit profile.

Leverage Pre-Qualifications as Negotiation Tools

Once you have a few strong pre-qualification offers in hand, use them to your advantage. Present your best external offer to the dealership’s finance department and ask them to beat it. This strategy, based on my observations, often encourages dealers to be more competitive with their own financing options, potentially saving you hundreds or even thousands over the life of the loan.

Common Mistakes to Avoid When Pursuing a Car Loan

Even with the best intentions, car buyers can fall into common traps. Being aware of these pitfalls can save you money and stress.

One of the most common mistakes is not utilizing pre-qualification offers at all. Many buyers simply walk into a dealership and let the finance manager dictate their options, without having done any homework. This leaves you vulnerable to potentially higher interest rates because you lack comparison points. Always secure at least one pre-qualification before engaging with a dealership.

Another pitfall is assuming the first offer is the best or only offer. Dealerships often present their preferred financing option first. Without external pre-qualification offers, you have no benchmark to evaluate if that deal is truly competitive for your credit profile. Always compare and contrast.

A third mistake, especially after securing a pre-qualification, is applying for too many hard inquiries in a very short timeframe across different types of loans. While rate shopping for car loans is usually grouped as one inquiry, opening multiple new credit cards or other lines of credit simultaneously can significantly impact your score and potentially jeopardize your car loan approval. Focus your hard inquiries on the car loan once you’re ready to commit.

Finally, not knowing your budget beyond the monthly payment is a frequent error. Buyers often fixate solely on the monthly payment figure without considering the total cost of the loan, including interest over the full term. Use a loan calculator to understand the overall financial commitment, not just the immediate monthly outgoing.

Beyond the Inquiry: What Lenders Really Look At

While your credit inquiries and score are crucial, they’re just one piece of the puzzle for lenders. When assessing your full car loan application, other significant factors come into play:

Debt-to-Income (DTI) Ratio: Lenders want to ensure you can comfortably afford your new car payment alongside your existing financial obligations. Your DTI ratio, which compares your total monthly debt payments to your gross monthly income, is a critical indicator of your capacity to take on more debt. A lower DTI ratio generally signals less risk.

Employment Stability: A consistent employment history demonstrates your ability to generate a steady income to repay the loan. Lenders typically prefer applicants with stable employment, often looking for at least one to two years at the same job. This indicates reliability and financial consistency.

Down Payment: The size of your down payment plays a significant role. A larger down payment reduces the loan amount, thereby lowering the lender’s risk. It also often translates to lower monthly payments and less interest paid over the life of the loan. From a lender’s perspective, a substantial down payment shows serious commitment.

Vehicle Choice and Value: The car you choose also influences the loan. Lenders assess the vehicle’s market value and its depreciation rate. They want to ensure that the loan amount doesn’t exceed the car’s value, protecting their investment in case of default. This is why some older or less reliable vehicles can be harder to finance. For more detailed information on how these factors influence your approval, you might find our article on "Factors Affecting Your Car Loan Approval" helpful.

The Long-Term Picture: Managing Your Credit for Future Loans

Understanding car loan soft inquiries is not just about your immediate car purchase; it’s about fostering responsible credit management for your entire financial future. Every financial decision you make, from paying your bills on time to how many credit accounts you open, contributes to your overall credit health.

A successful car loan, managed responsibly with on-time payments, can significantly boost your credit score over time. It demonstrates your ability to handle installment debt, which is a positive mark on your credit report. This, in turn, can open doors to better rates on future loans, whether for another car, a home, or even personal credit lines.

To truly stay on top of your credit, regularly monitor your credit report. You can obtain free copies from AnnualCreditReport.com from each of the three major credit bureaus. For ongoing credit monitoring and detailed reports, reputable sources like Experian offer valuable insights and tools to help you understand and improve your credit standing. Knowledge is power when it comes to your financial well-being.

Frequently Asked Questions (FAQ) About Car Loan Soft Inquiries

Do all lenders use soft inquiries for pre-qualification?

Most reputable lenders and online platforms offering "check your rate" or "get pre-qualified" tools use soft inquiries. However, it’s always a good practice to look for explicit statements like "no impact on your credit score" or "soft credit pull only" before proceeding. If unsure, ask the lender directly.

How long does a soft inquiry stay on my credit report?

Soft inquiries typically remain on your credit report for 12 to 24 months. However, remember that they are only visible to you and do not affect your credit score or other lenders’ perception of your creditworthiness.

Can I get a car loan with bad credit using a soft inquiry?

A soft inquiry can help you determine if you pre-qualify for a car loan even with bad credit. While it won’t guarantee approval or the best rates, it allows you to see what options might be available without further damaging your score. It’s an excellent way to explore specialized lenders who cater to subprime borrowers.

What’s the difference between pre-qualification and pre-approval?

Pre-qualification, often initiated by a soft inquiry, gives you an estimate of what you might qualify for, based on a general review of your credit. Pre-approval, on the other hand, usually involves a hard inquiry and means a lender has conditionally approved you for a specific loan amount at a particular interest rate, subject to final verification and vehicle choice. Pre-approval is a more solid offer.

Conclusion: Drive Away with Confidence

The journey to buying a new car doesn’t have to be fraught with financial uncertainty. By understanding and strategically utilizing the power of a Car Loan Soft Inquiry, you can transform your car-buying experience into an informed, stress-free, and ultimately more affordable process. It’s your secret weapon for confident car shopping.

From stress-free rate shopping to empowering negotiation at the dealership, soft inquiries put you in the driver’s seat of your financial future. So, before you fall in love with your next set of wheels, take the time to pre-qualify, compare offers, and ensure you’re getting the best possible deal for your financial situation. Drive away with confidence, knowing you’ve made a smart and informed decision.