Navigate Your Next Car Purchase with Confidence: The Ultimate Guide to the AFCU Car Loan Calculator

Navigate Your Next Car Purchase with Confidence: The Ultimate Guide to the AFCU Car Loan Calculator Carloan.Guidemechanic.com

Buying a new or used car is often an exhilarating experience. The smell of new leather, the gleam of fresh paint, or the satisfaction of finding that perfect pre-owned gem – it’s a significant moment. However, beneath the excitement lies a crucial financial decision that can impact your budget for years to come. This is where understanding your financing options becomes paramount, and a reliable tool like the AFCU Car Loan Calculator can be your most valuable co-pilot.

For many, the process of securing an auto loan feels daunting, shrouded in complex terms and numbers. Without a clear picture of what you can truly afford, you risk overextending your budget or missing out on better deals. This comprehensive guide will demystify the car loan process, spotlight the power of the AFCU Car Loan Calculator, and equip you with the knowledge to make informed decisions, ensuring your next vehicle purchase is both exciting and financially sound.

Navigate Your Next Car Purchase with Confidence: The Ultimate Guide to the AFCU Car Loan Calculator

Why a Car Loan Calculator is Your Indispensable Financial Tool

Imagine walking into a dealership without a clear understanding of your borrowing power. You’re at the mercy of the salesperson, who might steer you towards a vehicle or financing package that isn’t ideal for your financial situation. This scenario is all too common, and it’s precisely why a car loan calculator is not just a convenience, but a necessity.

Beyond simply revealing a potential monthly payment, a robust calculator empowers you with critical insights. It allows you to experiment with different variables – loan amounts, interest rates, and repayment periods – to see their direct impact on your budget. This proactive approach transforms you from a passive recipient of loan offers into an informed negotiator.

Based on my experience in personal finance, failing to utilize such a tool is one of the biggest missteps car buyers make. It’s like setting sail without a compass; you might eventually reach your destination, but the journey will be fraught with uncertainty and potential detours. A good calculator helps you chart the most efficient and affordable course.

Introducing the AFCU Car Loan Calculator: Your Trusted Financial Partner

When it comes to financial tools, trust and reliability are paramount. The AFCU Car Loan Calculator stands out as a user-friendly and highly effective resource, especially for those considering financing through a credit union. AFCU, like other credit unions, operates with a member-first philosophy, often translating into competitive rates and personalized service.

This calculator isn’t just a generic online widget; it’s designed to provide insights relevant to the credit union lending environment. It helps prospective borrowers understand the financial implications of their loan choices within a framework that prioritizes their financial well-being. Using it means you’re leveraging a tool from an institution that aims to serve its members, not just profit from them.

The AFCU Car Loan Calculator is a cornerstone for anyone looking to budget wisely for their next vehicle. It provides clarity on what your potential monthly payments will look like, helping you align your car dreams with your financial realities. This transparency is crucial for making smart, long-term financial decisions.

Deconstructing the Inputs: What You Need to Know Before You Calculate

To get the most accurate and useful results from any car loan calculator, including the AFCU Car Loan Calculator, you need to understand the key variables you’ll be inputting. Each piece of information plays a significant role in determining your final monthly payment and the total cost of the loan. Let’s break down these essential components in detail.

1. The Loan Amount: Understanding Your True Borrowing Need

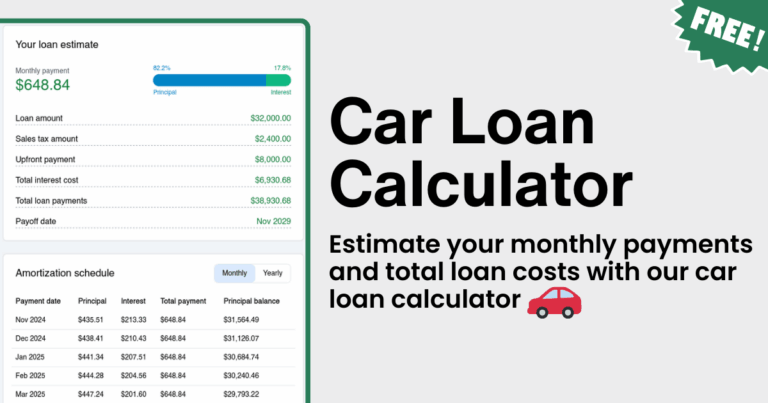

The "loan amount" isn’t always just the sticker price of the car. It represents the total sum you need to borrow after accounting for any down payment, trade-in value, and other fees. For instance, if a car costs $30,000, but you have a $5,000 down payment and a $3,000 trade-in, your actual loan amount would be $22,000 (excluding taxes and fees).

It’s crucial to consider the "out-the-door" price of the vehicle, which includes sales tax, registration fees, and any dealer add-ons. These can significantly increase the total amount you need to finance. Failing to factor these in can lead to a surprise when you get to the finance office.

Pro Tip: Always try to get a breakdown of the "out-the-door" price from the dealer before you start calculating. This ensures your loan amount input is as precise as possible, giving you a realistic monthly payment estimate.

2. The Interest Rate: The Cost of Borrowing

The interest rate is perhaps the most critical factor influencing the total cost of your loan. It’s the percentage charged by the lender for the privilege of borrowing money. A lower interest rate means you pay less over the life of the loan, saving you potentially thousands of dollars.

Several factors determine the interest rate you’ll be offered. Your credit score is paramount; individuals with excellent credit typically qualify for the lowest rates. The loan term, the specific lender (like AFCU), and prevailing market conditions also play significant roles. Even a difference of one or two percentage points can have a substantial impact on your monthly payment and total interest paid.

Based on my experience, securing a pre-approval from a credit union like AFCU before you even step foot in a dealership is a game-changer. This gives you a concrete interest rate to input into the calculator, providing a highly accurate estimate and giving you strong negotiation leverage.

3. The Loan Term (Duration): The Time vs. Money Trade-off

The loan term, or duration, refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This variable creates a direct trade-off: a longer loan term usually means lower monthly payments, but you’ll pay significantly more in total interest over the life of the loan.

Conversely, a shorter loan term results in higher monthly payments but substantially less total interest paid. It also means you own the car outright sooner, freeing up your budget for other financial goals. When using the AFCU Car Loan Calculator, experiment with different terms to see how they affect both your monthly outlay and the overall cost.

Common mistakes to avoid are automatically opting for the longest term just to achieve the lowest possible monthly payment. While it might seem appealing initially, this approach can trap you in a cycle of paying more interest and potentially owning a car for longer than its useful life, increasing the risk of negative equity.

4. Down Payment: Your Upfront Investment

A down payment is the amount of cash you pay upfront towards the purchase of the vehicle. This reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. A substantial down payment also provides an immediate buffer against depreciation, reducing the risk of being "upside down" on your loan (owing more than the car is worth).

Even a small down payment can make a difference, but generally, the more you can put down, the better your financial position will be. It signals to lenders that you are a serious and responsible borrower, which can sometimes even lead to slightly better interest rates. The AFCU Car Loan Calculator will clearly show you the impact of varying down payment amounts.

5. Trade-in Value: Leveraging Your Current Asset

If you’re planning to trade in your current vehicle, its value acts similarly to a down payment. The agreed-upon trade-in amount is deducted from the purchase price of your new car, reducing the principal loan amount. This can significantly lower your monthly payments and overall interest.

Before using the calculator, it’s wise to get an estimate of your current car’s trade-in value from reputable sources like Kelley Blue Book (KBB) or NADA Guides. This empowers you to assess the fairness of any offer you receive from a dealership and accurately input the figure into the calculator. Don’t underestimate the power of knowing your trade-in’s worth.

Step-by-Step Guide: How to Use the AFCU Car Loan Calculator Effectively

Using the AFCU Car Loan Calculator is straightforward, designed to be intuitive and user-friendly. However, to truly harness its power, it’s essential to approach it systematically. Follow these steps to get the most accurate and insightful results for your car buying journey.

- Gather Your Data: Before you even open the calculator, have your key figures ready. This includes your estimated loan amount (car price minus potential down payment/trade-in), an estimated interest rate (ideally from a pre-approval), and various loan terms you’re considering.

- Input the Estimated Loan Amount: Start by entering the principal amount you anticipate needing to borrow. Remember, this is the final figure after any down payment or trade-in has been applied to the vehicle’s total cost.

- Enter Your Interest Rate: Input the interest rate you expect to receive. If you have a pre-approval from AFCU, use that exact rate for the most accurate calculation. If not, use an estimated rate based on your credit score and current market averages, but always seek pre-approval for a concrete number.

- Select Your Loan Term: Experiment with different loan durations (e.g., 48 months, 60 months, 72 months). Observe how changing this variable drastically alters your estimated monthly payment and the total interest you’ll pay over time. This step is crucial for balancing affordability with overall cost.

- Factor in Down Payment/Trade-in (if applicable): Many calculators have dedicated fields for down payment and trade-in value. Entering these will automatically adjust the net loan amount and provide a more precise monthly payment. Don’t skip this if you plan to use these options.

- Analyze the Results: The calculator will instantly display your estimated monthly payment. But don’t stop there! Look for details like the total interest paid over the life of the loan. This often overlooked figure reveals the true cost of borrowing and helps you compare different scenarios more effectively.

- Run Multiple Scenarios: This is where the calculator truly shines. Don’t just run one calculation. Try different combinations:

- A smaller down payment with a longer term.

- A larger down payment with a shorter term.

- Slightly different interest rates (if you’re unsure of your exact rate).

- This iterative process allows you to find the sweet spot that fits your budget and financial goals.

By diligently following these steps, you’ll gain a crystal-clear understanding of what your potential car loan will entail. This knowledge is your greatest asset in the negotiation room and in ensuring your car purchase aligns perfectly with your financial health.

Beyond the Calculator: Maximizing Your Car Buying Journey

While the AFCU Car Loan Calculator is an incredible tool, it’s just one component of a successful car buying strategy. To truly maximize your car buying journey and secure the best possible deal, you need to consider a broader financial landscape. Here are some critical aspects to master.

The Power of Pre-Approval: Your Negotiation Ace

As mentioned earlier, getting pre-approved for a car loan before you visit a dealership is arguably the most impactful step you can take. A pre-approval from AFCU, for instance, means you know exactly how much you can borrow and at what interest rate. This transforms you into a cash buyer in the eyes of the dealership.

When you have pre-approval in hand, you can focus solely on negotiating the vehicle’s price, separate from the financing. This prevents the "payment packing" trick where dealers might adjust loan terms to make a higher car price seem affordable. You dictate the terms, not them.

Understanding Your Credit Score: The Gateway to Better Rates

Your credit score is the single most influential factor in determining the interest rate you’ll be offered. Lenders use it to assess your creditworthiness – essentially, how likely you are to repay the loan. A higher score (generally 700+) typically qualifies you for the lowest rates, while a lower score will result in higher rates.

Before applying for any loan, check your credit report and score. You’re entitled to a free credit report from each of the three major bureaus (Experian, Equifax, TransUnion) annually via AnnualCreditReport.com. Address any errors you find, as even small discrepancies can negatively impact your score. Improving your score, even by a few points, can translate into significant savings on interest over the life of your car loan. For more in-depth advice on improving your credit, you might find our article on "Building a Strong Credit Profile for Auto Loans" helpful.

Budgeting Holistically: Beyond the Monthly Payment

The car loan calculator focuses on the loan, but a car’s cost extends far beyond its monthly payment. You need to budget for insurance premiums, which can vary wildly depending on the vehicle, your driving record, and your location. Factor in fuel costs, routine maintenance (oil changes, tire rotations), and potential repair costs, especially for used vehicles.

Overlooking these "hidden" costs can quickly turn an affordable monthly payment into a financial strain. Create a comprehensive budget that includes all car-related expenses to ensure your chosen vehicle truly fits into your overall financial picture.

The Art of Negotiation: Armed with Data

With your AFCU Car Loan Calculator results and pre-approval, you’re armed with powerful data. You know what you can afford, what a fair interest rate looks like, and what your trade-in is worth. Use this information to negotiate confidently on the vehicle price.

Don’t be afraid to walk away if the deal isn’t right. There are always other cars and other dealerships. Remember, the goal is to get the best possible overall deal, not just the lowest monthly payment. For further tips on this, consider reading our post on "Effective Strategies for Car Price Negotiation".

Refinancing Considerations: An Option for Future Savings

Even if you don’t secure the absolute best rate initially, perhaps due to a lower credit score at the time of purchase, refinancing is often an option down the road. If your credit score improves, or if interest rates drop, you might be able to refinance your existing car loan for a lower rate or a more favorable term.

Many credit unions, including AFCU, offer competitive refinancing options. Keep an eye on market conditions and your credit health; refinancing could save you hundreds or even thousands of dollars over the remaining life of your loan.

Common Mistakes to Avoid: Learn from Others’ Errors

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of the loan. Another frequent error is not getting pre-approved, which leaves you vulnerable at the dealership. Failing to check your credit score and report before applying for a loan is also a significant misstep. Lastly, always remember to budget for all car-related expenses, not just the loan payment. Avoiding these pitfalls will put you in a much stronger financial position.

For additional unbiased car buying advice and resources, a trusted external source like Consumer Reports provides excellent insights into vehicle reliability and owner satisfaction, which can complement your financial planning.

The AFCU Advantage: Why a Credit Union Loan Might Be Right for You

Beyond the calculator itself, understanding the benefits of financing through a credit union like AFCU can significantly enhance your car buying experience. Credit unions are member-owned financial cooperatives, which means their primary focus is on serving their members, not external shareholders.

This member-centric philosophy often translates into several advantages for auto loan borrowers:

- Potentially Lower Interest Rates: Credit unions are frequently able to offer more competitive interest rates compared to traditional banks, as they pass profits back to members in the form of better rates and lower fees.

- Personalized Service: You’re not just an account number; you’re a member. This often leads to more personalized attention and flexible lending solutions tailored to your specific situation.

- Community Focus: Credit unions are deeply rooted in their communities, often understanding local economic conditions and being more responsive to their members’ needs.

- Favorable Terms: Beyond rates, credit unions may offer more flexible loan terms and conditions, making it easier to find a repayment plan that truly works for your budget.

Using the AFCU Car Loan Calculator is the first step in exploring these advantages. It allows you to see firsthand how AFCU’s potential offerings could align with your financial goals, often providing a more favorable outcome than you might find elsewhere.

Conclusion: Empower Your Car Purchase with Knowledge

Navigating the complexities of car financing doesn’t have to be a source of stress. With the right tools and a solid understanding of the process, you can approach your next vehicle purchase with confidence and clarity. The AFCU Car Loan Calculator is more than just a numbers cruncher; it’s an empowering financial instrument that puts you in control.

By meticulously understanding the inputs, exploring various scenarios, and combining the calculator’s insights with smart financial planning, you transform uncertainty into informed decision-making. You’ll not only secure a car that fits your lifestyle but also a loan that fits your budget, allowing you to enjoy your new ride without financial worries.

Don’t leave your car financing to chance. Take the driver’s seat of your financial future. Utilize the AFCU Car Loan Calculator today, get pre-approved, and embark on your car buying journey with the ultimate peace of mind. Your dream car, financed intelligently, is well within reach.