Navigating a $10,000 Car Loan: Your Ultimate Guide to Smart Payments and Affordable Ownership

Navigating a $10,000 Car Loan: Your Ultimate Guide to Smart Payments and Affordable Ownership Carloan.Guidemechanic.com

Securing a reliable vehicle is often a necessity, not just a luxury, for countless individuals and families. For many, a budget of around $10,000 strikes a sweet spot, offering access to a wide range of dependable used cars without breaking the bank. However, understanding how to approach a $10,000 car loan and manage its payments effectively can feel like navigating a complex maze.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to secure an affordable $10,000 car loan, understand its intricacies, and ensure your monthly payments fit comfortably within your financial plan. We’ll delve deep into every aspect, from pre-application considerations to post-purchase financial management, making your journey to car ownership smooth and stress-free.

Navigating a $10,000 Car Loan: Your Ultimate Guide to Smart Payments and Affordable Ownership

Understanding the $10,000 Car Loan Landscape

A $10,000 car loan is a significant financial commitment, but it opens doors to a vast market of pre-owned vehicles. This budget segment typically includes well-maintained sedans, compact SUVs, and even some older luxury models that offer excellent value. The key is to approach this purchase with a clear understanding of what a $10,000 budget entails.

Why $10,000 is a Common Car Budget

The $10,000 price point is popular for several reasons. It’s often the threshold for a second family car, a first car for a new driver, or a practical upgrade for someone seeking reliability without the depreciation hit of a brand-new vehicle. This budget allows for a reasonable monthly car loan payment without imposing an overwhelming financial burden.

Based on my experience, many buyers find this figure achievable through a combination of savings, a trade-in, and a manageable loan. It represents a sweet spot where quality and affordability intersect, making it a highly sought-after segment in the used car market.

What Kind of Cars Can You Expect for $10,000?

With a $10,000 budget, you’re primarily looking at used cars, often 5-10 years old, with varying mileage. You can find excellent value in popular models known for their reliability, such as certain Honda Civics, Toyota Corollas, Ford Focuses, or Mazda 3s. The focus here should be on condition, maintenance history, and overall longevity rather than just the make and model.

Pro tips from us: Always prioritize a vehicle’s maintenance records and get a pre-purchase inspection from an independent mechanic. This due diligence can save you from significant headaches and unexpected repair costs down the line, ensuring your $10,000 car loan is truly for a reliable asset.

Factors Influencing Your $10k Car Loan Payments

When you apply for a $10,000 car loan, several critical factors will determine your actual monthly payments and the total cost of borrowing. Understanding these elements is crucial for securing the best possible terms.

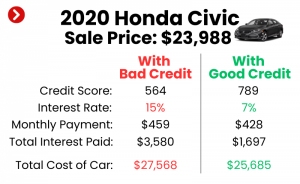

Your Credit Score: The Cornerstone of Affordability

Your credit score is arguably the most significant factor lenders consider. It reflects your creditworthiness and your history of managing debt. A higher credit score signals lower risk to lenders, leading to more favorable interest rates and better loan terms for your $10k car loan.

Based on my experience, a good credit score (typically 670 and above) can save you hundreds, if not thousands, of dollars over the life of a loan. It’s not just about getting approved; it’s about getting approved for an affordable car loan with manageable 10k car loan payments.

If your credit score isn’t where you want it to be, take steps to improve it before applying. Pay down existing debts, make all payments on time, and dispute any errors on your credit report. For a deeper dive into improving your credit score, check out our guide on .

The Interest Rate: Your Cost of Borrowing

The interest rate is the percentage charged by the lender for the money you borrow. It directly impacts your monthly payments and the total amount you’ll repay. A lower interest rate means a more affordable loan.

Interest rates are influenced by your credit score, the loan term, current market conditions, and the specific lender. Always compare offers from multiple lenders to ensure you’re getting a competitive rate.

Loan Term (Duration): Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60 months). A longer loan term results in lower monthly payments, but you’ll pay more in total interest over the life of the loan. Conversely, a shorter term means higher monthly payments but less overall interest paid.

Common mistakes to avoid are extending the loan term too much just to get the lowest possible monthly payment. While it might seem appealing initially, you could end up paying significantly more for your $10,000 car loan than the car is even worth by the end of the term. Aim for the shortest term you can comfortably afford.

Your Down Payment: Reducing Your Loan Amount

A down payment is the initial amount of money you pay upfront for the car. Making a substantial down payment reduces the principal amount you need to borrow, directly lowering your monthly payments and the total interest paid. It also shows lenders you’re committed to the purchase.

Pro tips from us: Aim for at least a 10-20% down payment if possible, even on a $10k car loan. On a $10,000 car, that would be $1,000 to $2,000, which can significantly improve your loan terms and make your 10k car loan payments much more manageable.

Trade-in Value: Another Way to Lower Your Loan

If you have an existing vehicle, trading it in can act like a down payment. The value of your trade-in is deducted from the purchase price of the new car, reducing the amount you need to finance. Be sure to research your car’s trade-in value beforehand so you can negotiate effectively.

Additional Costs: Don’t Forget the Extras

Beyond the car’s price and loan interest, there are other costs associated with buying a vehicle that can impact your overall financial picture. These include sales tax, registration fees, title fees, and potentially documentation fees from the dealership. While not directly part of your 10k car loan payments, they are part of the total cost of ownership.

Calculating Your Potential $10k Car Loan Payments

Understanding how $10,000 car loan payments are calculated is essential for budgeting. While exact figures depend on your specific loan terms, we can illustrate potential scenarios.

The Basic Formula and Online Calculators

Loan payments are typically calculated using a formula that takes into account the principal loan amount, the interest rate, and the loan term. Fortunately, you don’t need to be a math whiz to figure this out. Online car loan calculators are widely available and incredibly useful tools.

These calculators allow you to input your desired loan amount (e.g., $10,000), an estimated interest rate, and various loan terms to see projected monthly payments. This helps you quickly assess what fits your budget.

Example Scenarios for a $10,000 Car Loan

Let’s look at some hypothetical scenarios for a $10,000 car loan (assuming no down payment for simplicity, though a down payment is highly recommended):

-

Scenario 1: Excellent Credit (e.g., 5% APR)

- 36-month term: Approx. $299 per month

- 48-month term: Approx. $230 per month

- 60-month term: Approx. $189 per month

-

Scenario 2: Good Credit (e.g., 8% APR)

- 36-month term: Approx. $313 per month

- 48-month term: Approx. $244 per month

- 60-month term: Approx. $203 per month

-

Scenario 3: Average Credit (e.g., 12% APR)

- 36-month term: Approx. $332 per month

- 48-month term: Approx. $263 per month

- 60-month term: Approx. $222 per month

As you can see, even a few percentage points difference in the interest rate can significantly impact your 10k car loan payments. The loan term also plays a major role in affordability, but remember the trade-off with total interest paid.

Budgeting for Your $10k Car Loan

Beyond the monthly payments, responsible car ownership requires a holistic budget. Failing to account for all costs can lead to financial strain, even if your $10,000 car loan payments seem manageable.

Assessing Your Financial Health

Before committing to any loan, conduct a thorough review of your personal finances. What is your stable monthly income? What are your fixed expenses (rent, utilities, existing debts)? What are your variable expenses (groceries, entertainment)?

Based on my experience, many people underestimate the true cost of car ownership. A clear picture of your disposable income will help you determine how much you can truly afford for a car payment and associated costs.

The 20/4/10 Rule (or Similar Budgeting Advice)

A popular guideline for car affordability is the 20/4/10 rule:

- 20% down payment: This minimizes your loan amount.

- 4-year (48-month) loan term: This helps reduce total interest and ensures you don’t "underwater" on your loan.

- 10% of gross monthly income: Your total car expenses (payment, insurance, fuel) should not exceed 10% of your gross monthly income.

While this is a guideline, it provides an excellent framework for ensuring your $10,000 car loan and overall car expenses are sustainable. Adjust it based on your specific financial situation and priorities. Want to explore more budgeting strategies for car ownership? Read our comprehensive article on .

Creating a Realistic Monthly Budget

Once you have a car in mind and an estimated loan payment, integrate it into a detailed monthly budget. Don’t forget to include:

- Car Loan Payment: The fixed amount you’ll pay monthly.

- Car Insurance: Get quotes before buying the car, as this can vary widely.

- Fuel Costs: Estimate based on your daily commute and driving habits.

- Maintenance Fund: Set aside money for routine service, unexpected repairs, and tires.

- Registration/License Fees: Annual costs to keep your car legal.

Common mistakes to avoid are neglecting to budget for maintenance and insurance. These can add hundreds of dollars to your monthly outlay and quickly turn an "affordable" car into a financial burden.

Finding the Best $10k Car Loan

Securing the best possible terms for your $10,000 car loan requires a proactive approach and some diligent shopping around. Don’t just take the first offer you receive.

Shop Around: Banks, Credit Unions, Online Lenders, Dealerships

There are multiple avenues for obtaining an affordable car loan:

- Banks: Traditional financial institutions often offer competitive rates, especially if you have an existing relationship with them.

- Credit Unions: Known for their member-focused approach, credit unions often have some of the most favorable interest rates and terms.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, or others specialize in online lending, offering quick approvals and competitive rates.

- Dealership Financing: While convenient, dealership financing sometimes carries higher rates. However, they can sometimes offer special promotions, so it’s worth comparing.

Pro tips from us: Get pre-approved by at least 2-3 external lenders (banks, credit unions, online) before stepping onto a dealership lot. This gives you a benchmark rate and empowers you to negotiate confidently.

The Pre-Approval Process

Pre-approval is a crucial step. It involves a lender reviewing your financial information and credit history to determine how much they are willing to lend you and at what interest rate. This is usually a "soft inquiry" on your credit, which doesn’t hurt your score.

Having a pre-approval in hand for your $10k car loan provides several benefits: it clarifies your budget, streamlines the car-buying process, and gives you leverage when negotiating with dealerships.

Understanding Loan Offers

When comparing loan offers, look beyond just the monthly payment. Pay close attention to:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and some fees.

- Total Cost of the Loan: How much you will pay back over the entire loan term.

- Any Prepayment Penalties: Ensure you can pay off your loan early without extra fees.

- Loan Fees: Are there origination fees or other charges?

Strategies for Lowering Your Monthly $10k Car Payments

Even with a $10,000 car loan, there are strategies you can employ to make your monthly payments more affordable.

Increase Your Down Payment

As discussed, a larger down payment directly reduces the loan amount, leading to lower monthly payments. Every extra dollar you put down can save you more over the life of the loan.

Improve Your Credit Score Before Applying

If time permits, focus on boosting your credit score. A few months of diligent credit management can significantly lower the interest rate you’re offered, resulting in noticeably smaller 10k car loan payments.

Choose a Shorter Loan Term (If Affordable)

While a longer term means lower monthly payments, a shorter term can lead to substantial savings on total interest. If your budget allows for a slightly higher monthly payment, opt for a 36 or 48-month term instead of 60 months or more.

Refinancing (When Applicable)

If you’ve already secured a $10,000 car loan but your credit has improved, or interest rates have dropped, consider refinancing. Refinancing replaces your existing loan with a new one, potentially at a lower interest rate or with different terms, which can reduce your monthly payments.

Negotiating the Car Price

Remember, the car’s price is often negotiable. Even saving a few hundred dollars on the purchase price can translate into lower 10k car loan payments and less interest over the life of the loan. Don’t be afraid to haggle.

Managing Your $10k Car Loan After Approval

Once your $10,000 car loan is approved and you’ve driven off the lot, the journey isn’t over. Proper loan management is crucial for maintaining good financial health.

Making Payments on Time, Every Time

This is non-negotiable. Late payments not only incur fees but also negatively impact your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Understanding Your Loan Agreement

Keep a copy of your loan agreement and understand all its terms. Know your interest rate, loan term, payment due date, and any specific clauses regarding late payments or early payoffs.

Accelerated Payments/Paying Extra

If your budget allows, consider paying more than the minimum monthly payment. Even an extra $20-$50 per month can significantly reduce the total interest you pay and shorten the loan term. Ensure your extra payments are applied directly to the principal balance.

What If You Face Financial Hardship?

Life happens, and sometimes financial difficulties arise. If you anticipate trouble making your 10k car loan payments, contact your lender immediately. They may offer options like deferment, forbearance, or a modified payment plan. Ignoring the problem will only worsen it.

Beyond the Monthly Payment: The True Cost of Car Ownership

While your $10,000 car loan payments are a major part of your car budget, they are far from the only cost. Understanding the full spectrum of expenses is vital for long-term financial stability.

Car Insurance

This is a mandatory and often substantial expense. Factors like your age, driving record, location, and the specific car you purchase will influence your premiums. Always get quotes before finalizing your car purchase.

Maintenance and Repairs

Even a reliable $10,000 car will require routine maintenance (oil changes, tire rotations) and potentially unexpected repairs. Setting aside a dedicated fund for these costs is a smart financial move. Older vehicles, while more affordable upfront, can sometimes incur higher maintenance costs.

Fuel Costs

With fluctuating gas prices, fuel can be a significant monthly expense. Consider the car’s fuel efficiency based on your driving habits and commute.

Registration and Fees

Annual vehicle registration, license plate renewals, and emission testing fees are recurring costs that need to be factored into your overall budget.

Common Mistakes to Avoid When Getting a $10k Car Loan

Based on my experience, certain pitfalls commonly trip up buyers seeking an affordable car loan. Being aware of these can save you a lot of trouble.

- Focusing Only on Monthly Payments: This is perhaps the biggest mistake. A low monthly payment achieved by extending the loan term too much means paying significantly more in total interest. Always look at the total cost of the loan.

- Not Shopping Around for Loans: Settling for the first loan offer, especially from a dealership, can mean missing out on better rates from other lenders. Always compare multiple offers.

- Ignoring Your Credit Score: A low credit score translates directly to higher interest rates and more expensive 10k car loan payments. Invest time in improving it before applying.

- Buying More Car Than You Need (or Can Afford): It’s easy to get excited and overspend. Stick to your budget and prioritize reliability and affordability over unnecessary features.

- Skipping the Pre-Approval Process: Without pre-approval, you’re negotiating blind at the dealership, lacking the leverage to secure the best financing terms.

- Neglecting Additional Costs: Forgetting to budget for insurance, fuel, maintenance, and registration can quickly derail your financial plan, making your seemingly affordable $10,000 car loan burdensome.

Conclusion: Your Path to Affordable $10,000 Car Ownership

Securing a $10,000 car loan and managing its payments doesn’t have to be daunting. By understanding the key factors that influence your loan, diligently shopping around for the best terms, and meticulously budgeting for all aspects of car ownership, you can achieve your goal of affordable and reliable transportation.

Remember, the ultimate goal is not just to get approved for a loan, but to secure an affordable car loan with manageable 10k car loan payments that align with your overall financial health. Take your time, do your research, and make informed decisions. Your wallet will thank you.

Start your journey today by assessing your credit, exploring your budget, and getting pre-approved. With smart planning, your ideal $10,000 car is well within reach.

External Resource: For up-to-date interest rate benchmarks and economic data that can influence car loan rates, a trusted source like the Federal Reserve Economic Data (FRED) provides valuable insights.