Navigating a $20,000 Car Loan Over 72 Months: Your Ultimate Guide to Smart Auto Financing

Navigating a $20,000 Car Loan Over 72 Months: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Securing a new or used vehicle is an exciting milestone, but the financing aspect can often feel daunting. Many prospective car owners find themselves exploring options like a $20,000 car loan over 72 months. This specific loan term, stretching over six years, has become increasingly popular due to its ability to make monthly payments more manageable. However, like any significant financial decision, it comes with its own set of advantages and potential drawbacks.

This comprehensive guide is designed to equip you with all the knowledge you need to confidently approach a 20000 car loan 72 months. We’ll delve into the mechanics of such a loan, dissect the factors influencing your approval and costs, and provide expert tips to ensure you make the most informed decision possible. Our goal is to empower you to drive away not just with your dream car, but with a financing plan that truly works for your financial well-being.

Navigating a $20,000 Car Loan Over 72 Months: Your Ultimate Guide to Smart Auto Financing

Understanding the Landscape of a 72-Month Car Loan

When you opt for a 72-month car loan, you’re essentially committing to repaying your borrowed amount over six full years. This extended repayment period is a significant factor in shaping your monthly financial obligations. For a loan amount like $20,000, stretching payments across 72 months can drastically reduce the individual payment size compared to shorter terms.

The allure of lower monthly payments is undeniable. It allows buyers to afford more expensive vehicles or simply free up more cash flow for other expenses. However, this convenience often comes with a trade-off, primarily in the form of increased total interest paid over the life of the loan. Understanding this fundamental dynamic is crucial before proceeding.

Why 72 Months is a Popular Choice

From my experience in auto financing, the 72-month term gained traction during economic periods when buyers sought ways to mitigate the rising costs of vehicles. It effectively lowers the barrier to entry for many car purchases. A $20,000 car loan over 72 months means your financial commitment is spread thin, which can make luxury or newer models seem more accessible.

This term also offers a degree of financial flexibility. Lower payments can reduce stress on your monthly budget, especially for those with fluctuating incomes or other significant financial commitments. However, it’s vital to look beyond just the monthly figure and consider the long-term implications.

The Math Behind Your Monthly Payments

To truly grasp a 20000 car loan 72 months, you need to understand how interest rates and the loan term combine to determine your monthly payment and overall cost. The core formula involves the principal amount, the interest rate (APR), and the loan term. While online calculators can give you precise figures, understanding the impact of each variable is key.

How Interest Rates Impact Payments

The interest rate, expressed as an Annual Percentage Rate (APR), is arguably the most critical factor after the loan amount itself. A difference of even a few percentage points can lead to hundreds, if not thousands, of dollars in extra costs over a 72-month term. For a $20,000 car loan, a higher APR means a significantly larger portion of your initial payments goes towards interest rather than reducing the principal.

Pro tips from us: Don’t just accept the first interest rate offered. Shopping around for the best APR can save you a substantial amount of money over six years. This is where pre-approval from multiple lenders becomes incredibly valuable.

Factors Affecting Your Interest Rate

Several elements converge to determine the interest rate you’ll be offered for your 20000 car loan 72 months:

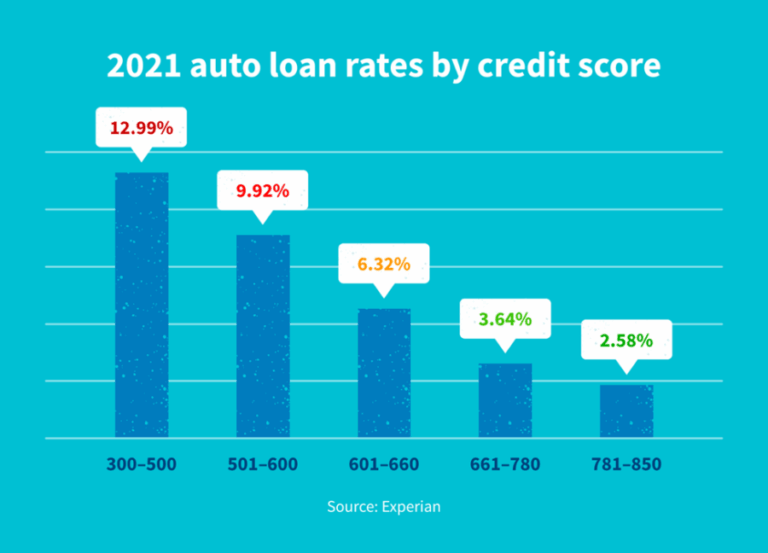

- Credit Score: This is paramount. Borrowers with excellent credit (720+) typically secure the lowest rates. Good credit (660-719) still offers competitive rates, while fair (600-659) or poor credit (<600) will result in much higher APRs. Lenders see a lower credit score as a higher risk.

- Debt-to-Income (DTI) Ratio: Lenders assess your ability to manage additional debt. If your existing debt payments consume a large portion of your income, it might signal a higher risk, leading to a higher interest rate or even loan denial.

- Loan Term: Longer loan terms, such as 72 months, often come with slightly higher interest rates than shorter terms (e.g., 36 or 48 months). This is because the lender is taking on risk for a longer period.

- Down Payment: A larger down payment reduces the amount you need to borrow, which can sometimes lead to a lower interest rate as it signals a reduced risk for the lender.

- Vehicle Age/Type: New cars generally qualify for lower rates than used cars. Certain high-risk or very old vehicles might also have higher rates.

Estimated Monthly Payments for a $20,000 Loan (72 Months)

Let’s look at some examples to illustrate the impact of different APRs on your 20000 car loan 72 months payment:

- At 5% APR: Your estimated monthly payment would be around $322. The total interest paid over 72 months would be approximately $3,184.

- At 8% APR: Your estimated monthly payment would increase to about $362. The total interest paid would jump to roughly $6,064.

- At 10% APR: The monthly payment would be around $386. The total interest paid would be close to $7,792.

As you can see, the difference in total interest paid between a 5% and 10% APR is over $4,600 – a significant amount that underscores the importance of securing the best possible rate.

Pros and Cons of a 72-Month Car Loan

While a 20000 car loan 72 months offers attractive benefits, it’s crucial to evaluate both sides of the coin. A balanced perspective ensures you’re making a decision that aligns with your long-term financial goals.

Advantages of a 72-Month Loan

- Lower Monthly Payments: This is the most compelling advantage. Stretching the loan over six years significantly reduces the amount you pay each month, making the vehicle more affordable on a day-to-day basis. This can free up cash for other essential expenses or savings.

- Access to Better Vehicles: With lower monthly payments, you might be able to afford a newer model, a car with more features, or a more reliable vehicle that might otherwise be out of reach with a shorter loan term.

- Financial Flexibility: Lower payments provide more breathing room in your budget. This can be particularly beneficial if you anticipate other large expenses or want to maintain a healthy emergency fund.

Disadvantages of a 72-Month Loan

- Higher Total Interest Paid: This is the primary drawback. While individual payments are lower, you’ll pay significantly more in interest over the life of the loan compared to a 36 or 48-month term. Our previous examples clearly demonstrated this financial reality.

- Longer Period of Debt: You’ll be indebted to the lender for six years. This can feel like a long time, especially if your financial situation changes or if you wish to upgrade your vehicle sooner.

- Increased Risk of Negative Equity (Being Upside Down): Cars depreciate rapidly. With a long loan term, especially one with a small or no down payment, you might owe more on the car than it’s worth for an extended period. This is known as negative equity, and it can be a significant problem if you need to sell or trade in the car before the loan is paid off.

- Higher Maintenance Costs Towards the End of the Loan: By the time your 72-month loan is paid off, your car will be six years older. At this point, it’s more likely to require significant maintenance and repairs, which can become an additional financial burden just as you finish paying off the loan.

Common mistakes to avoid are focusing solely on the monthly payment. Always ask for the total cost of the loan, including all interest and fees, to get the full picture.

Key Factors Influencing Your Loan Approval

For a 20000 car loan 72 months, lenders scrutinize several aspects of your financial profile. Understanding these can significantly improve your chances of approval and help you secure the best possible terms.

Your Credit Score: The Cornerstone

Your credit score is the most influential factor. It’s a numerical representation of your creditworthiness, derived from your payment history, amounts owed, length of credit history, new credit, and credit mix.

- Excellent Credit (720+): You are a prime candidate for the lowest interest rates and easiest approval. Lenders see you as very low risk.

- Good Credit (660-719): You’ll likely qualify for competitive rates, though perhaps not the absolute lowest. Approval is still very probable.

- Fair Credit (600-659): Approval is possible, but you’ll face higher interest rates. Lenders will look closely at other factors.

- Poor Credit (<600): Securing a 20000 car loan 72 months will be challenging and, if approved, will come with very high interest rates. You might need a co-signer or a larger down payment.

Based on my experience, improving your credit score before applying for an auto loan is one of the most impactful steps you can take. Paying down existing debt, making all payments on time, and correcting any errors on your credit report can make a huge difference.

Income & Debt-to-Income (DTI) Ratio

Lenders need assurance that you can comfortably afford the monthly payments for your 20000 car loan 72 months. They assess this through your income and DTI ratio.

- Stable Income: A consistent and verifiable income source is essential. Lenders typically prefer applicants with steady employment.

- Debt-to-Income Ratio: This ratio compares your total monthly debt payments (including the proposed car payment) to your gross monthly income. A lower DTI (ideally below 36-40%) indicates you have more disposable income to cover your new car payment, making you a more attractive borrower.

The Power of a Down Payment

A down payment is money you pay upfront for the car, reducing the amount you need to borrow. For a 20000 car loan 72 months, even a modest down payment can yield significant benefits:

- Reduces Loan Amount: Less borrowed means less interest paid over time.

- Lower Monthly Payments: A smaller principal leads to smaller monthly installments.

- Improved Loan Terms: Lenders often offer better interest rates to borrowers who put money down, as it reduces their risk.

- Avoids Negative Equity: A down payment helps cushion against rapid depreciation, making it less likely you’ll owe more than the car is worth.

Pro tips from us: Aim for at least a 10-20% down payment if possible. For a $20,000 loan, that would be $2,000-$4,000, which can make a noticeable difference in your total cost.

Vehicle Choice and Trade-in Value

The vehicle itself can influence your loan approval. Lenders prefer vehicles that hold their value well, as this provides better collateral for the loan. Newer, more reliable models are generally viewed more favorably.

If you have a current vehicle, using its trade-in value as a down payment is an excellent strategy. It functions just like cash, reducing your loan amount and potentially improving your loan terms. Ensure you get a fair trade-in valuation from multiple sources.

Preparing for Your 20000 Car Loan Application

Preparation is key to a smooth and successful auto financing experience. Before you even set foot in a dealership or apply online, take these crucial steps.

Check Your Credit Report and Score

Before any lender does, you should know exactly where you stand. Obtain your credit report from all three major bureaus (Experian, Equifax, TransUnion) and check your credit score.

- Review for Accuracy: Dispute any errors or inaccuracies immediately, as they can negatively impact your score.

- Understand Your Score: Knowing your score allows you to anticipate the kind of interest rates you might qualify for and helps you negotiate effectively.

- Internal Link: For a deeper dive, check out our guide on .

Gather Necessary Documentation

Lenders will require various documents to verify your identity, income, and residency. Having these ready will streamline the application process for your 20000 car loan 72 months:

- Proof of Income: Recent pay stubs (last 2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residency: Utility bills, lease agreement, or mortgage statement.

- Proof of Identity: Driver’s license or other government-issued ID.

- Bank Statements: To show financial stability and available funds for a down payment.

- Trade-in Information: If applicable, title, registration, and lienholder details for your current vehicle.

Get Pre-Approved for Your Loan

This is perhaps the most powerful step you can take. Pre-approval means a lender has conditionally agreed to lend you a specific amount (e.g., up to $20,000) at a specific interest rate, before you even choose a car.

- Negotiating Power: With pre-approval in hand, you walk into the dealership as a cash buyer. You can negotiate the car price without the added pressure of simultaneously arranging financing.

- Clear Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your budget.

- Rate Comparison: Get pre-approved by multiple lenders (banks, credit unions, online lenders). This allows you to compare offers and choose the best terms for your 20000 car loan 72 months. Multiple inquiries within a short period (typically 14-45 days) are usually counted as a single inquiry by credit bureaus, minimizing the impact on your score.

Budgeting: Understanding What You Can Truly Afford

While a 72-month loan can make a $20,000 car seem affordable, it’s crucial to look beyond just the monthly payment. Consider the total cost of car ownership:

- Loan Payment: Your fixed monthly installment.

- Insurance: Get quotes for the specific vehicle you’re considering. This can be a significant monthly expense.

- Fuel: Estimate your weekly or monthly fuel costs based on your driving habits.

- Maintenance & Repairs: Budget for routine servicing (oil changes, tire rotations) and potential repairs as the car ages.

- Registration & Taxes: Annual fees and upfront sales tax.

Common mistakes to avoid are stretching your budget too thin. Always leave a buffer for unexpected expenses.

Where to Secure Your Car Loan

You have several avenues for obtaining a 20000 car loan 72 months. Each option has its own characteristics, and exploring all of them is part of securing the best deal.

Dealership Financing

Most car dealerships offer in-house financing or work with a network of lenders.

- Convenience: It’s a one-stop-shop, simplifying the process of buying and financing.

- Special Offers: Dealerships may offer promotional rates or incentives on specific models, sometimes even 0% APR (though these are rare for used cars and typically require excellent credit and shorter terms).

- Markup Potential: Dealerships can sometimes mark up interest rates to earn a profit, meaning you might not get the absolute lowest rate.

Banks & Credit Unions

Traditional financial institutions are often excellent sources for auto loans.

- Competitive Rates: Banks and credit unions frequently offer very competitive interest rates, especially to their existing customers or members.

- Relationship Banking: If you have a long-standing relationship with a bank or credit union, they might offer you more favorable terms.

- Credit Unions: Often known for generally lower interest rates and more personalized service due to their member-focused structure.

Online Lenders

The digital age has brought a surge of online-only auto lenders.

- Speed & Convenience: You can apply and get approved from the comfort of your home, often within minutes.

- Broad Comparison: Online platforms allow you to easily compare offers from multiple lenders without visiting physical locations.

- Variety of Options: Many online lenders specialize in different credit tiers, so you might find options even with less-than-perfect credit.

Pro tips from us: Always apply for pre-approval from at least one bank/credit union and one online lender, in addition to checking dealership offers. This ensures you have a strong comparison point for your 20000 car loan 72 months.

Navigating the Loan Process and Avoiding Pitfalls

Once you’ve secured a pre-approval or are ready to discuss financing, vigilance is key. This is where many buyers can make costly mistakes.

Read the Fine Print, Every Single Word

Before signing anything, thoroughly review the loan agreement for your 20000 car loan 72 months. Don’t be rushed.

- Interest Rate (APR): Confirm it matches what you were quoted.

- Total Loan Amount: Ensure it reflects the agreed-upon price minus your down payment/trade-in.

- Loan Term: Verify it’s 72 months.

- Fees: Look for origination fees, documentation fees, or any other charges.

- Prepayment Penalties: Some loans charge a penalty if you pay them off early. Ideally, avoid loans with these clauses.

Beware of Unnecessary Add-ons

Dealerships often present a myriad of add-on products and services during the financing process. While some may offer value, many are overpriced or unnecessary for your 20000 car loan 72 months.

- Extended Warranties: Research third-party options. Dealership warranties are often marked up significantly.

- GAP Insurance: Guaranteed Asset Protection (GAP) covers the difference between what you owe on your loan and what your insurance company pays if your car is totaled or stolen. This can be valuable, especially if you have a low down payment or a long loan term (like 72 months) where negative equity is a risk. However, compare prices – your auto insurer might offer it for less.

- Paint Protection, Fabric Protection, VIN Etching: These are almost always overpriced and have minimal real value. Decline them.

Common mistakes to avoid are feeling pressured to add extra features. Politely but firmly decline anything you don’t understand or genuinely need. Remember, these add-ons increase your total loan amount and, therefore, your monthly payment.

Don’t Overextend Yourself: The "Payment Trap"

The 72-month term is designed to make a $20,000 loan feel manageable. However, this ease can lead to the "payment trap," where you buy more car than you can truly afford because the monthly payment seems low.

Always remember the total cost of the loan, including all the interest you’ll pay over six years. Consider what else you could do with that extra money if you chose a less expensive car or a shorter loan term.

Managing Your Loan Post-Approval

Once you’ve secured your 20000 car loan 72 months, your financial journey isn’t over. Proactive management can save you money and protect your credit.

On-Time Payments: The Golden Rule

This cannot be stressed enough. Making your car loan payments on time, every time, is critical.

- Credit Score Impact: Timely payments build a positive payment history, which is the largest factor in your credit score. Late payments, conversely, can severely damage your score.

- Avoid Late Fees: Late payments incur fees, adding to your overall cost.

- Maintain Good Standing: Ensures you remain in good standing with your lender, which can be beneficial if you need financing in the future.

Refinancing Opportunities

Life changes, and so do interest rates. If your credit score improves significantly after you take out your 20000 car loan 72 months, or if market rates drop, refinancing could be a smart move.

- Lower Interest Rate: The primary goal of refinancing is often to secure a lower APR, which reduces your monthly payment and/or the total interest paid.

- Shorter Term: You might also be able to refinance to a shorter loan term, allowing you to pay off the car faster, especially if your financial situation has improved.

- Reduce Monthly Payment: If you’re struggling with current payments, refinancing to a lower rate (or even extending the term again, though this is generally not advised) can offer relief.

Based on my experience, many people overlook refinancing, leaving money on the table. It’s always worth checking your options a year or two into your loan, especially if your financial health has improved.

Paying Off Early: Benefits and Considerations

If you find yourself with extra funds, paying off your 20000 car loan 72 months early can be highly advantageous.

- Save on Interest: This is the biggest benefit. Every extra dollar you put towards the principal reduces the amount of interest you’ll pay over the remaining loan term.

- Freedom from Debt: Being debt-free is a powerful financial position. It frees up cash flow for other goals like saving for a home, retirement, or investments.

- No Prepayment Penalties: Most auto loans do not have prepayment penalties, but always double-check your loan agreement.

Pro tips from us: Even small extra payments can make a difference. Consider adding an extra $25-$50 to your monthly payment, or applying any windfalls (tax refunds, bonuses) directly to the principal.

Alternative Considerations

While a 20000 car loan 72 months is a common path, it’s not the only one. Briefly considering alternatives can further solidify your decision.

Leasing vs. Buying

Leasing offers lower monthly payments and the ability to drive a new car every few years. However, you don’t own the vehicle, have mileage restrictions, and don’t build equity. For long-term ownership and customization, buying is generally preferred.

Shorter Loan Terms

If your budget allows, a shorter loan term (e.g., 48 or 60 months) will save you significant money in interest. While monthly payments will be higher, the total cost of ownership will be less, and you’ll be debt-free sooner. This is often the more financially prudent choice if affordable.

Conclusion: Drive Smart with Your $20,000 Car Loan Over 72 Months

Securing a $20,000 car loan over 72 months can be a strategic move for many car buyers, offering manageable monthly payments and access to the vehicles they desire. However, an informed approach is paramount to avoid common pitfalls and ensure long-term financial health.

By understanding the impact of interest rates, diligently preparing your application, shopping around for the best terms, and managing your loan responsibly, you can transform this six-year commitment into a positive asset. Remember, the goal is not just to get approved, but to secure a loan that truly aligns with your financial capabilities and goals. Drive away with confidence, knowing you’ve made a smart and well-researched decision.

For more detailed financial planning advice, consider consulting resources like the . And if you’re ready to explore your car buying journey further, our is a great next step!